Asking for a credit limit increase is a common move for people trying to build their credit or get a bit more financial flexibility.

But one question often comes up: does requesting a credit increase hurt your credit score?

Here’s the quick answer: sometimes it can, but it depends on the process your credit card issuer uses. Some requests trigger a “hard inquiry,” which could cause a small point reduction on your score.

On the other hand, a credit limit increase can help in the long run by lowering your credit utilization rate. Which is a key factor that makes up 30% of your credit score.

In this guide, we’ll cover:

- When a credit increase request can help or hurt your score.

- How a hard vs. soft credit inquiry works.

- Tips on the best times to request a credit limit increase.

Let’s start by exploring how credit limit increases actually work and the impact they might have on your score.

What is a Credit Limit Increase?

A credit limit increase means your credit card issuer raises the maximum amount you’re allowed to borrow on your existing card.

When you ask your credit card issuer for a higher credit limit, you’re essentially asking them to lend you more money. A higher limit means more available credit, which can be useful for handling large expenses or improving your credit utilization ratio (more on that later).

Let’s say you have a $1,000 limit and get approved for an increase—now you might have access to $2,000.

How is This Different from Getting a New Card?

With a credit limit increase, you’re adjusting the borrowing power on a card you already have.

Getting a new card, on the other hand, means opening an entirely new account, which adds a fresh line of credit to your report.

Benefits of a Credit Limit Increase

Some credit repair experts suggest a credit limit increase as an action when improving a credit score.

Why?

Because it can give you..

More Flexibility

With a higher limit, you have added spending power. This can help in emergencies or when you need a little more room in your budget.

Potential for a Credit Score Boost

If you keep your spending low, a higher credit limit can reduce your credit utilization rate. Credit utilization—how much of your available credit you’re using—makes up about 30% of your credit score. So, using your new limit responsibly might give your score a lift.

Using a credit limit increase wisely can give you added financial flexibility and even improve your credit score. Keep an eye on your spending, and you’ll be set to make the most of this boost.

How Requesting a Credit Limit Increase Hurt Your Score?

When you request a credit limit increase, the impact on your credit score depends on how the bank or credit card company handles your request.

They can do this in two main ways: with a hard inquiry or a soft inquiry.

Let’s look at each:

Hard Inquiries

As I just mentioned, requesting a credit limit increase often leads to a hard inquiry.

(Not everyone know’s about this, Read: Can my Credit Score Drop for No Reason.)

A hard inquiry is when a lender reviews your full credit report to determine your creditworthiness.

The effect?

If your lender performs a hard inquiry, it’s like they’re doing a more thorough check of your credit. Every time a hard inquiry occurs, your credit score can dip slightly — typically by 5 to 10 points. This is because credit reporting agencies see it as you actively trying to access more credit, which could mean a higher risk.

Hard inquiries only stay on your credit report for two years, but they typically only affect your score for about 12 months. So, while it’s something to keep in mind, it’s not a long-term issue.

However, if you’ve already applied for several lines of credit or other loans recently, these inquiries can start to add up. Multiple hard inquiries in a short period may suggest to lenders that you're desperate for credit, which can negatively impact your score.

Soft Inquiries

Now, if it’s a soft inquiry, you’re in luck—this won’t impact your score at all.

Soft inquiries are often used for customers who already have a bank account or credit card with the lender. This way, they can check your credit history without affecting your score.

So, if you’re thinking about requesting a credit increase, it’s a good idea to ask the lender if it will be a hard or soft inquiry. This way, you’ll know exactly what to expect for your score.

When Requesting a Credit Increase NOT Hurt Your Score

Soft inquiry a little-known trick that can help you avoid the hard inquiry altogether.

Here are a few ways to increase your chances of getting a soft inquiry when requesting a credit increase:

Pre-Approved Credit Limit Increases: Some issuers will automatically increase your credit limit if you’ve demonstrated responsible behavior, like paying on time and keeping your utilization low. In these cases, no inquiry (hard or soft) is required, and you benefit from the higher limit without any hit to your score.

Customer-Initiated Soft Inquiries: In some cases, you can ask your credit card issuer if they’ll consider your request for a higher limit without performing a hard inquiry. There’s no guarantee, but it’s worth asking. They may review your account history and approve your request based on that alone.

Pros and Cons of Requesting a Credit Increase

Requesting a credit increase can be both beneficial and, in some cases, a bit risky.

Knowing these pros and cons can help you decide if it’s the right move.

Pros of a Credit Increase

1. Lowers Credit Utilization

One of the biggest benefits of a higher credit limit is how it affects your credit utilization ratio. Credit utilization refers to the amount of credit you're using compared to your total available credit. It’s a significant factor in determining your credit score — accounting for about 30% of your FICO score.

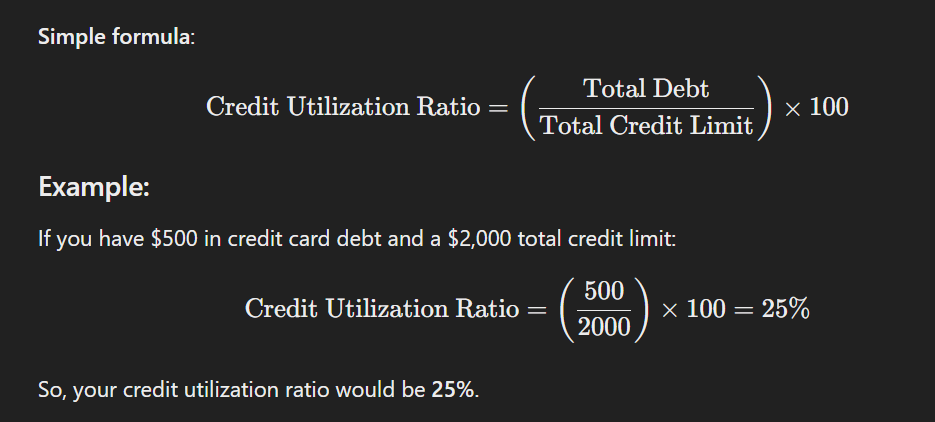

Here’s the formula:

- Total up your debt: Add up all your credit card balances.

- Total up your credit limits: Add up the credit limits for all your credit cards.

- Divide and multiply: Divide the total debt by the total credit limit, then multiply by 100 to get a percentage.

If you increase your credit limit to $10,000 but continue to only use $2,000, your new utilization ratio is 20%. That’s much better for your score!

2. Adds Flexibility for Emergencies

With a higher credit limit, you have a cushion for unexpected expenses like car repairs or medical bills. It’s a way to add financial flexibility without opening a new credit account.

3. Better Debt-To-Income Ratio

Another indirect benefit of requesting a credit limit increase is how it can improve your debt-to-income (DTI) ratio. While DTI doesn’t directly impact your credit score, lenders use it to evaluate your ability to manage debt. By increasing your available credit (without increasing your debt), you may appear less risky to lenders.

So, requesting a credit limit increase could actually help you get approved for loans or other credit products in the future, as long as you don’t increase your spending alongside it.

4. Better Position for Major Loans

A higher credit limit with responsible use can also make your credit report look more favorable to lenders. If you’re planning to apply for a mortgage or car loan, showing you can manage a higher credit limit responsibly could strengthen your application.

Should You Increase Your Credit Limit?

The benefits are great, right? But if you are still not sure if a credit limit increase is right for you.

Here are a few situations where it might make sense:

- Building an Emergency Fund: An increased limit can provide a financial cushion in case of emergencies.

- Consolidating Debt: If you’re managing multiple balances, a higher limit on one card could help simplify things.

- Preparing for a Big Purchase: If you’re planning to apply for a loan, improving your credit score with a lower utilization rate can help.

Consider your situation and needs.

If a higher limit helps you responsibly manage your finances, it could be a positive move.

Cons of a Credit Increase

1. Temporary Score Drop from a Hard Inquiry

This is the most obvious downside of a credit increase. When you ask for a credit limit increase, your lender may check your credit report with a "hard inquiry." This is a detailed look at your credit, and it can cause your score to drop by a few points, usually no more than 5.

While the drop is small and temporary, it’s still worth to note. Especially if you’re planning to apply for a loan soon. But don’t worry! If you keep managing your credit well, your score will bounce back quickly.

2. Potential Overspending

Although a higher credit limit sounds great, there are situations where it can work against you. The most common issue? Overspending. With more available credit, it can be tempting to spend more than usual, which can lead to bigger balances, higher payments, and ultimately, more debt. If you’re not careful, this can hurt your finances in the long run.

Some people think keeping a low credit limit will help them avoid debt, but that’s not entirely accurate. The key isn’t the size of the limit—it’s how you manage it. A responsible spending habit, like only charging what you can pay off in full each month, is what keeps debt in check, not necessarily a low limit.

3. Denial Impacts Future Requests

I might not have mentioned it yet, but you should all know that not all credit limit increase request can be granted.

If a lender denies your request, it could limit your ability to secure another increase in the near term. Lenders might view frequent requests for credit as a red flag, signaling financial strain or the need for more credit than you can handle.

Common Reasons Credit Limit Increase Requests Are Denied

If your request gets denied, don’t worry; it’s common and often temporary. Here are some reasons why it might happen:

- Short Account History: Lenders prefer seeing a longer credit history before they increase limits.

- Low Income: If your income isn’t high enough to support a bigger credit limit, this could be a reason.

- Missed or Late Payments: Even one recent late payment can hurt your chances.

- High Credit Utilization: If you’re using a high percentage of your available credit, lenders may hesitate to offer more.

To improve your chances next time, work on these areas—build a solid payment history, lower your utilization, and consider waiting until your financial situation improves.

How to Request a Credit Increase Without Hurting Your Score

Here’s a step-by-step guide to maximizing your chances of getting a credit limit increase without damaging your credit score:

1. Know Your Credit Score

Before you even consider asking for a credit limit increase, you need to know where you stand. Review your credit report for any potential red flags like missed payments or high utilization ratios. If your credit score isn’t in good shape, it may be worth working on improving it before requesting a credit increase.

2. Ask About the Inquiry Type

As I mentioned earlier, not all credit card issuers will perform a hard inquiry when you request an increase. When you call or apply online, ask them directly if they’re going to perform a hard or soft pull on your credit. If it’s a soft pull, you can proceed without worrying about your score. If it’s a hard inquiry, you’ll need to decide whether the short-term dip in your score is worth the potential long-term benefits of the increase.

3. Pick the Right Time

Timing matters when requesting a credit limit increase. Here are a few times when it’s best to make the request:

- After a salary increase: If your income has gone up, this signals to your credit card issuer that you’re less likely to default on payments, which increases your chances of approval.

- After paying down debt: If you’ve recently paid off a large chunk of debt, this can improve your creditworthiness in the eyes of lenders.

- When you haven’t opened new accounts recently: If you’ve applied for several new credit cards or loans in the last few months, it’s best to wait before requesting an increase. Too many inquiries in a short period can make you look risky to lenders.

On the other hand, there are times when you might want to hold off on a request.

For example, if you’re planning to apply for a mortgage or other loan soon, a hard inquiry might briefly lower your score, which can impact those applications. Also, avoid requesting an increase if your score recently dropped, as lenders may see this as a sign of financial stress.

4. Keep Your Utilization Low After the Increase

Once you’ve successfully increased your credit limit, the key is to avoid maxing it out. Remember, the goal is to lower your credit utilization ratio, not raise it. Keep your spending at the same level or lower to see the full benefit of the increased limit.

Avoiding a Credit Limit Reduction

But did you know that lenders can also lower your credit limit if they see certain spending habits? Maintaining a high credit limit requires showing lenders you’re a responsible borrower. Here are a few ways to keep your limit intact:

- Keep Utilization Below 30%: Avoid using too much of your available credit, as high usage may prompt your issuer to lower your limit.

- Pay On Time: Paying you debts on time show lenders you're reliable.

- Avoid Sudden Large Purchases: Large spending surges can raise lender concerns about your financial stability.

Following these habits reassures lenders that you’re a low-risk borrower, which helps secure your new credit limit.

Is Requesting a Credit Limit Increase Worth It?

So, does requesting a credit increase hurt your score?

In most cases, the answer is no — at least not significantly.

While a hard inquiry may temporarily lower your score by a few points, the long-term benefits of a higher credit limit (like improved credit utilization) can far outweigh the short-term dip.

Here’s a quick recap:

- A credit limit increase can result in a hard inquiry, but the impact is usually small and short-lived.

- Increasing your limit can lower your credit utilization ratio, which can improve your credit score.

- You can sometimes avoid a hard inquiry by asking for a soft inquiry or taking advantage of automatic increases.

In the end, requesting a credit limit increase can be a smart move if you’re looking to improve your credit score or need a little extra spending power.

Don’t forget to manage it responsibly and keep an eye on your overall credit health.

If you need help, remember that we at ASAP Credit Repair are here with you along the way!