TL;DR: ECSI default is typically the result of multiple missed payments, not a single late payment. Once a loan enters default, borrowers may face collections, negative credit reporting, added costs, and fewer repayment options. Addressing delinquency early can help prevent more serious consequences.

If you've missed a payment on an account serviced by Educational Computer Systems, Inc. (ECSI), you're probably wondering what happens next.

Many borrowers assume a missed payment is a temporary issue that can be addressed later. The reality is that student loan delinquency progresses gradually. The consequences becoming more severe the longer an account remains unpaid.

According to a New York Times article, student loan borrowers are among the largest groups affected by serious delinquency. With millions of accounts reported past due each year.

Educational Computer Systems, Inc. (ECSI) services several types of educational debt, including Perkins Loans, institutional loans, tuition payment plans, and other school-based financing programs. Because these loans are often administered directly for colleges and universities, borrowers may not realize that missed payments can eventually be reported to credit bureaus, transferred to collections, or result in default depending on the terms of the agreement.

At ASAP Credit Repair, we see credit reports where borrowers discover an ECSI-related delinquency only after applying for a mortgage, auto loan, or credit card. In many cases, the borrower missed several notices before realizing the account had become a credit reporting issue.

Understanding what happens after an ECSI payment is missed, how default occurs, and what options may be available before collections begin can help borrowers protect their credit and avoid more costly consequences.

ECSI Default: What Happens After Missed Payments?

Missing an ECSI payment can result into one thing, and that's a direct credit score damage.

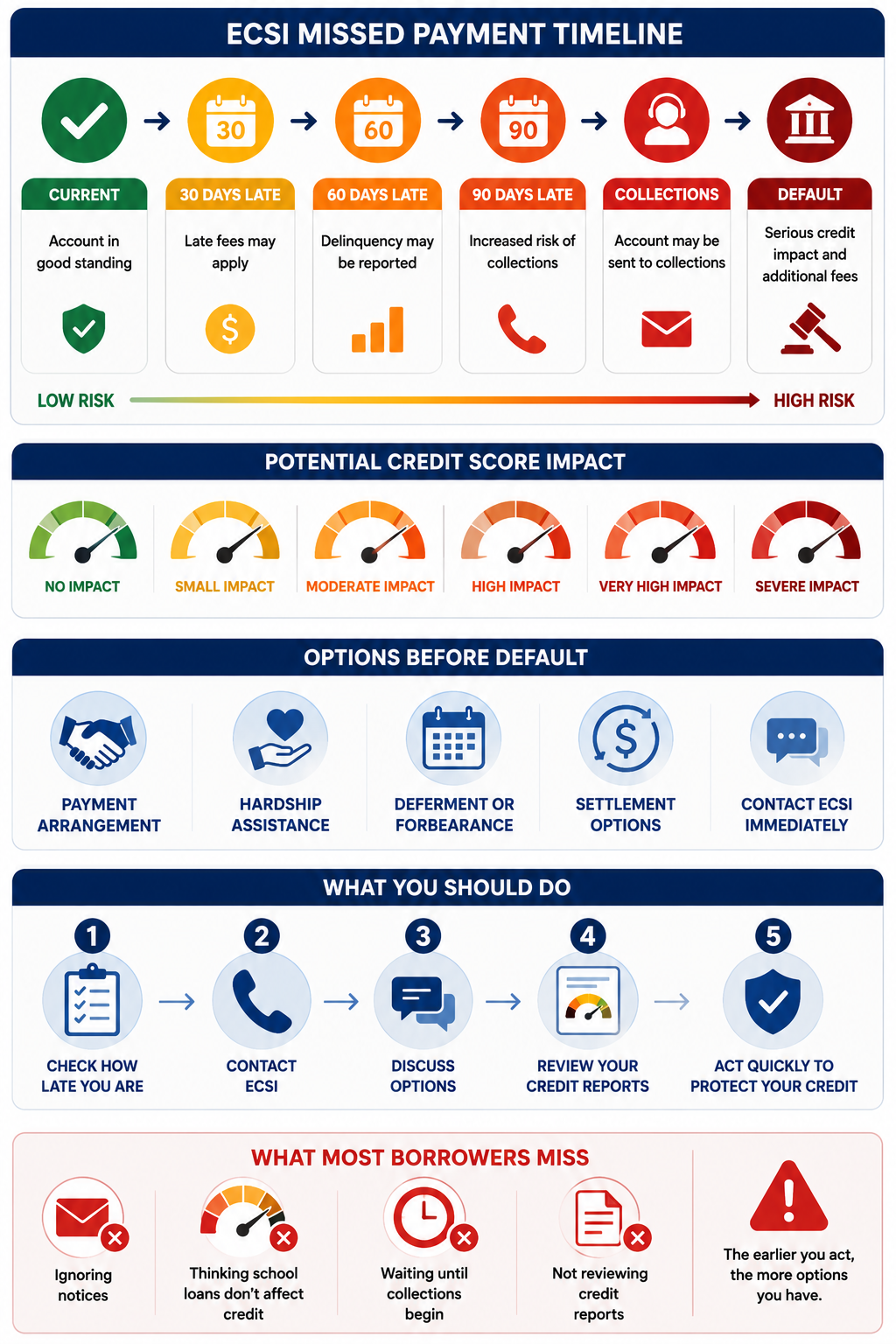

The infographic below shows the typical progression from a missed ECSI payment to delinquency, collections, and potential default. Including the points where borrowers may still have options to prevent further damage.

What Is ECSI and Why Is It Servicing Your Loan?

Educational Computer Systems, Inc. (ECSI) is a loan servicer that manages educational debt on behalf of colleges, universities, and the U.S. Department of Education. It does not own the debt. It collects payments, processes requests, and reports account status to credit bureaus on behalf of the institution. The institution — not ECSI — sets repayment terms and default thresholds.

ECSI services several types of accounts. Understanding which type you have determines what rules apply to your situation.

| Loan or Account Type | Who Sets Terms | Default Authority | Federal Protection |

|---|---|---|---|

| Federal Perkins Loans | Department of Education, administered by school | 240 days non-payment under federal guidelines | Yes — federal rules apply |

| Institutional Loans | The school | School sets threshold. Often 90 to 180 days. | Partial — school-specific rules |

| Campus-Based Loans | School + federal program structure | School policies govern, within federal framework | Partial |

| Tuition Payment Plans | School | Contractual. Plan terms set missed payment consequences. | No — contract law only |

| Student Account Receivables | School | School's billing and collection policies govern | No |

ECSI is not a debt collector under the Fair Debt Collection Practices Act. It is a servicer. However, if the institution assigns a delinquent account to a third-party collection agency, that agency is subject to FDCPA protections. The distinction matters for your legal rights and what letters you can send to challenge the account.

In 2024, ECSI paid $3.65 million to settle a class-action lawsuit covering approximately 552,293 Perkins Loan borrowers who were charged illegal payment processing fees between December 2018 and October 2023. This settlement, approved by U.S. District Court Judge Patricia A. Dodge, confirmed that ECSI had assessed fees on online and phone payments that violated federal and state consumer protection laws. If you paid ECSI processing fees during that period, you may have received or may still receive a pro-rata refund from the settlement fund.

Does One Missed ECSI Payment Mean Default?

No. One missed payment produces delinquency, not default. Default requires sustained non-payment over a period defined by the loan type and institution. For Perkins Loans, federal guidelines set that threshold at 240 days. For institutional loans, the school may set it at 90 to 180 days. The progression from delinquency to default is not automatic or immediate.

Payments are being made on schedule. ECSI reports the account as current to Experian, Equifax, and TransUnion. No late fees. No collection activity. All repayment benefits and options remain available.

ECSI may charge a late fee depending on the loan agreement. No credit bureau reporting occurs before the 30-day mark. Paying now prevents all credit damage. Contact ECSI during this window to ask about payment arrangements or a one-time hardship accommodation before any mark hits the report.

ECSI reports the account as 30 days past due to all three bureaus. The mark can lower a credit score by 60 to 100 points depending on starting score. Communication from ECSI escalates. Options including payment plans and hardship accommodations are still available at this stage.

A 60-day mark and then a 90-day mark are each reported as separate delinquency entries on top of the 30-day mark. Each adds scoring damage. For institutional loans, many schools trigger collection review at the 90-day point. For Perkins Loans, the 90-day mark is documented as part of the federal required notification process before collection referral.

Many institutions trigger third-party collection referral between 120 and 180 days for institutional loans. Federal Perkins Loans approach the 240-day federal default threshold. A separate collection account tradeline may now appear on the credit report in addition to the original loan's delinquency marks. Collection fees may be added to the balance.

Default triggers the full collection process. For Perkins Loans, the school may assign the loan to the Department of Education or a federal collection contractor. For institutional loans, the school's collection policies apply. Repayment benefits including deferment and cancellation options may be suspended. The default notation on the credit report is separate from and in addition to all prior delinquency marks.

What Happens Immediately After Missing an ECSI Payment?

Three things happen in the first 30 days after a missed payment. A late fee is assessed. Collection notices begin by email, letter, or phone. Repayment benefits may be affected depending on the loan agreement. None of these involve bureau reporting yet. That starts at day 30.

The notices ECSI sends during the first 30 days are not junk mail. They document the beginning of the delinquency timeline. The U.S. Department of Education's Federal Student Aid Handbook, Chapter 5, requires servicers to send specific notifications at defined delinquency stages before escalating a Perkins Loan to collection. Ignoring those notices does not stop the timeline. It removes your opportunity to respond.

When Does ECSI Report Late Payments to Credit Bureaus?

ECSI reports delinquencies to Experian, Equifax, and TransUnion at the 30-day mark. Additional reports occur at 60, 90, 120, and 150 days. Each tier is a separate negative entry. A payment that reaches 60 days late has both a 30-day and a 60-day mark on the credit report. Both remain for seven years from the original missed payment date under the Fair Credit Reporting Act.

| Delinquency Tier | Reported to Bureaus | Typical Score Impact | What Can Still Be Done |

|---|---|---|---|

| 1–29 days | No | 0 points — late fee only | Pay now, prevent all credit damage |

| 30 days | Yes | 60–100 points drop | Payment plan, hardship accommodation still available |

| 60 days | Yes | 80–130 points drop (cumulative) | Options narrowing. Contact ECSI immediately. |

| 90 days | Yes | 100–150 points drop (cumulative) | Collection referral likely. Deferment may still be possible. |

| 120–180 days | Yes + possible collection account | Maximum delinquency damage + separate collection impact | Negotiate with collector. Verify collection account accuracy. |

| Default | Yes — separate default notation | All prior marks plus default notation | Rehabilitation, settlement, or dispute of inaccuracies |

As a student loan specialist reviewing a credit file with ECSI delinquencies would note, the scoring damage from multiple delinquency tiers on a single account is often larger than borrowers anticipate because each tier is treated as a distinct negative entry by FICO scoring models, not as a single late payment event.

In 2025, the Federal Reserve Bank of New York reported that 2.2 million student loan borrowers experienced credit score drops from missed payments as federal delinquency reporting restarted after the COVID-19 payment pause ended. Some experts cited drops of up to 175 points for borrowers who entered default. Understanding why your credit score can drop suddenly because of student loans explains how servicer transfers, reporting restarts, and delinquency tiers interact on the same credit file.

What Happens When an ECSI Account Defaults?

Default triggers four consequences. Collection activity escalates. Additional fees may be added to the balance. The credit report shows a default notation on top of all prior delinquency marks. For Perkins Loans, the Department of Education becomes involved in collection. Each consequence creates additional financial and credit damage beyond what the delinquency alone produced.

Collection Activity

For Perkins Loans, federal law allows the school to assign the defaulted loan to the Department of Education. The Department may then hire federal collection contractors to pursue repayment. For institutional loans, the school's collection policies govern what happens. Third-party collection agencies working on behalf of the institution may report a separate collection account to all three bureaus, creating a second negative entry with its own seven-year window.

Collection Fees Added to Balance

Federal Perkins Loan regulations allow collection costs to be added to the principal balance after default. This means the amount you owe grows beyond what you originally borrowed. For institutional loans, the school's collection agreement with any third party may similarly allow fee additions. The balance you see after default is often higher than the balance at the time of the last payment.

Loss of Repayment Benefits

Perkins Loans carry specific cancellation benefits for qualifying professions including teaching, nursing, law enforcement, and public service. These benefits may be suspended after default and may require loan rehabilitation before they can be reinstated. Deferment and forbearance options are also generally unavailable on defaulted accounts.

Credit Report Damage

The default notation appears as a separate item from all prior delinquency marks. A borrower who reaches default on an ECSI-serviced Perkins Loan may have a 30-day mark, a 60-day mark, a 90-day mark, a collection account tradeline from a third-party agency, and a default notation, each with its own seven-year reporting window starting from its respective date. The combined credit damage from all of these entries is more severe than any single mark alone.

Understanding how long student loans stay on your credit report after default and which removal strategies apply at each stage gives you a realistic picture of the recovery timeline before you decide how to respond.

Is an ECSI Delinquency or Collection Reported Accurately on Your File?

Servicer transfers, incorrect delinquency dates, wrong balances, and duplicate entries are common reporting errors on student loan accounts. A free 3-bureau audit across Equifax, Experian, and TransUnion shows exactly what is being reported and whether any entry contains disputable inaccuracies under the Fair Credit Reporting Act.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card requiredCan ECSI Send Your Account to Collections?

Yes. Schools and institutions that use ECSI for servicing can assign delinquent accounts to third-party collection agencies. ECSI itself may assist with early collection activity. Once a third-party collector receives the account, that agency reports a separate collection tradeline to the credit bureaus, adding a second seven-year negative entry on top of the existing delinquency marks from the original loan.

When a collection agency takes over an ECSI-serviced account, the FDCPA applies to the collector's behavior. You have the right to request written debt validation within 30 days of first contact. The collector must stop collection activity until they verify the debt. If they cannot verify it, the collection may be removed.

Collection agencies that work with educational institutions often receive incomplete documentation. Account histories, original promissory notes, and transfer records are not always included in what the collector receives from the school or ECSI. That documentation gap creates opportunities to challenge the account's validity and accuracy.

National Enterprise Systems, one of the major third-party collectors that works with over 150 colleges and universities, is one of the most complained-about collectors in the country. If an ECSI-managed institutional account from your school was assigned to a collector, understanding how National Enterprise Systems operates and what your rights are covers exactly what to do when a higher education collection agency contacts you or appears on your report.

What Options Exist Before an ECSI Account Defaults?

You have more options before default than after it. Options narrow as delinquency progresses. Act within 30 days of a missed payment to preserve the full range of available accommodations. After 90 days, most hardship options that do not require formal qualification are no longer accessible.

| Option | Loan Types It Applies To | When to Request | What It Does |

|---|---|---|---|

| Payment Arrangement | All ECSI-serviced loan types | Before 90 days delinquent | Modified payment schedule that fits current income. Prevents further delinquency tiers from being added. |

| Deferment | Perkins Loans, some campus-based loans | Before default | Pauses required payments during qualifying periods (enrollment, unemployment, economic hardship, military service). Interest rules vary by loan type. |

| Forbearance | Perkins Loans, some institutional loans | Before default | Temporary payment pause or reduction for up to 12 months in some cases. Interest may accrue. Must be requested and approved. |

| Cancellation | Perkins Loans only | Anytime a qualifying condition exists | Partial or full loan cancellation for teachers, nurses, law enforcement, Peace Corps volunteers, and other qualifying service. Cannot be requested after default without rehabilitation. |

| Hardship Accommodation | Institutional loans, tuition plans | As early as possible | School-specific programs vary. Some institutions offer income-based adjustments or temporary hardship pauses. Availability depends on the school's policies. |

| Settlement Discussion | Institutional loans, some campus-based | Before or after collections, case by case | Some schools accept less than the full balance to resolve the account. Federal Perkins Loan settlements are governed by stricter federal rules. Availability is not guaranteed. |

Deferment is one of the most overlooked options on Perkins Loans. Federal Perkins Loan deferment is available for borrowers who are enrolled at least half-time, unemployed, experiencing economic hardship, serving in the military, or working in certain qualifying professions. These deferments can pause payments without triggering additional delinquency reporting. Requests must be submitted to ECSI using the appropriate form before the deferment period begins.

Cancellation is available for Perkins Loans held by qualifying teachers, nurses, medical technicians, law enforcement officers, and other service workers. If you work in a qualifying field, you may be entitled to have a portion of the loan cancelled each year of qualifying service. This benefit is not automatic. You must apply through ECSI using the appropriate cancellation form. Default ends access to cancellation unless the loan is rehabilitated first.

What Should You Do Right Now After Missing an ECSI Payment?

Five steps in order. The sequence matters. Each action either stops additional damage or positions you for removal or recovery. Do not wait until collections contact you to start this process.

Log into ECSI's borrower portal at heartland.ecsi.net. Check the exact number of days past due and the current balance including any fees added. Review the loan type listed on the account. Federal Perkins Loan, institutional loan, and tuition payment plan each have different timelines and different options. You need to know which one you have before you can ask for the right accommodation.

Do this today | Establishes your exact position on the timelineDo not call and ask generally for help. Ask specifically: Is my loan eligible for deferment? Is forbearance available? Does my institution offer a hardship accommodation? What is the exact date a collection referral would be made? What is the total current balance including all fees? Write down the name of the representative, the date, and what was said. Every communication matters if you later need to dispute how the account was handled.

Do this same day | Options depend on what you ask for specificallyGo to AnnualCreditReport.com and pull Equifax, Experian, and TransUnion. Check whether any delinquency marks are already on the report. Verify the date of first delinquency, the creditor name, the account number, and the balance. If anything is wrong, file a dispute immediately. Common errors on ECSI-serviced accounts include wrong delinquency dates, balances that include fees not authorized by the original loan agreement, and duplicate entries after servicing transfers. Any inaccuracy is disputable under the FCRA.

Do within 7 days | Identifies errors before they compoundSend a written debt validation request to the collection agency within 30 days of first contact. The agency must stop collection activity until they provide verification. If the account was assigned without complete documentation, which is common with educational institution accounts transferred through multiple parties, validation may produce information gaps that support a dispute. Knowing how to identify which collection agency has your account and what information to request covers the exact process for finding the collector and sending the right letter.

If a collector has contacted you | 30-day window is criticalECSI and any assigned collection agency may continue updating the account status each month. New delinquency tiers, balance changes, and status updates all affect your score. Monitoring monthly lets you catch new inaccuracies within the 30-day window when disputes are most effective. Set a calendar reminder to pull reports the same week each month until the account is fully resolved and the correct status is confirmed on all three bureaus.

Ongoing | New reporting activity can appear months after initial delinquencyCan a Defaulted ECSI Account Be Removed From Your Credit Report?

Not simply because you paid the debt. Payment resolves the financial obligation. It does not remove the credit reporting. However, if the account contains inaccuracies such as wrong delinquency dates, incorrect balances, duplicate entries, or errors in account status, those entries are disputable and removable under the Fair Credit Reporting Act regardless of whether the underlying debt was valid.

Three situations allow removal before the seven-year window expires.

FCRA dispute for reporting errors. If the date of first delinquency is wrong, if the balance reflects unauthorized fees, if the account appears twice, or if the creditor name or account number does not match the original loan, any of these errors is grounds for a successful dispute. The bureau has 30 days to investigate. If the furnisher cannot verify the reported information, the entry must be corrected or removed.

Identity error or mixed file. If the account does not belong to you, or if information from another borrower's file was merged with yours during a servicer transfer, a dispute citing identity error can remove the account entirely. Mixed file errors are more common after loan transfers between servicers than most borrowers expect.

Goodwill request after rehabilitation. For borrowers who complete a formal Perkins Loan rehabilitation program or who bring an institutional loan current and maintain clean payments for an extended period, a goodwill letter to the original creditor requesting removal of prior delinquency marks sometimes works. This is not guaranteed and requires a documented history of responsible behavior after the delinquency period. It is more likely to succeed with a single isolated delinquency than with a pattern of missed payments.

Common Mistakes Borrowers Make With ECSI Accounts

After reviewing client files involving ECSI-serviced accounts, the same four mistakes appear. Each one is avoidable. Each one makes the situation harder to resolve than it would have been with early action.

Ignoring early notices. ECSI sends email and mail notices at each delinquency stage. Many borrowers stop opening mail once they fall behind, assuming the notices are just bills they cannot pay. Those notices document the delinquency timeline and contain information about options still available at each stage. Missing the response window at 30 days closes the door on accommodations that remain open at 60 days. Missing the 60-day window closes additional options that remain at 90 days.

Assuming school loans do not affect credit. Many borrowers believe institutional loans from their college are informal arrangements that will not appear on credit reports. ECSI reports Perkins Loans and many institutional loans to all three bureaus. A delinquency on a campus-based loan affects a credit score the same way a delinquency on a bank loan does. The source of the debt does not determine whether it is reported.

Waiting until collections begin before acting. Once an ECSI-managed account is assigned to a third-party collector, the borrower now has two problems instead of one. The original loan delinquency remains on the report. A new collection account from the third-party agency appears separately. Both need to be addressed. Acting before collection referral keeps the situation to one set of marks and one reporting entity.

Not reviewing credit reports after a missed payment. Many borrowers discover ECSI reporting errors months after they first appear. Reporting errors identified and disputed within 30 to 60 days of appearing on the report are resolved faster and with less credit damage than errors discovered a year later. Pull all three bureau reports within one week of any missed payment to establish a baseline of what is currently being reported.

From the perspective of a credit analyst reviewing a mortgage application denial tied to an ECSI delinquency, the most common avoidable outcome is a borrower who had a legitimate deferment qualification available at 45 days past due but did not contact ECSI until 110 days had passed, by which point the institutional loan had already been referred to a collection agency and the option to prevent the collection account entry no longer existed.

What happens if I miss an ECSI payment?

A late fee may be assessed. If the payment remains unpaid past 30 days, ECSI reports the delinquency to Experian, Equifax, and TransUnion. Additional delinquency tiers are reported at 60 and 90 days. If the account remains unpaid long enough, it may be referred to a third-party collection agency that adds a separate collection account to your credit report. Acting within the first 30 days preserves the most options.

Does ECSI report to credit bureaus?

Yes, depending on the loan program. Federal Perkins Loans and institutional loans serviced by ECSI can be reported to all three major credit bureaus. Late payments are typically reported starting at 30 days past due. The reporting continues at each 30-day tier until the account is brought current or reaches default.

Can ECSI send my account to collections?

Yes. Schools and institutions that use ECSI for servicing can assign delinquent accounts to third-party collection agencies after extended non-payment. Once assigned, the third-party agency may report a separate collection account to all three bureaus, creating additional credit damage beyond the original loan's delinquency marks.

How much will ECSI hurt my credit score?

A 30-day late payment can drop a credit score by 60 to 100 points depending on starting score. A 60-day late can produce 80 to 130 points of cumulative damage. A default notation adds further damage on top of all prior marks. A separate collection account from a third-party agency assigned by the institution adds its own scoring impact independently. The total damage from a single missed payment that escalates through all stages can exceed 150 points.

Is ECSI a debt collector?

No. ECSI is a loan servicer, not a debt collector under the FDCPA. It manages accounts on behalf of schools and the Department of Education. If ECSI transfers an account to a third-party collection agency, that agency is subject to FDCPA rules and you have the right to request debt validation, dispute inaccurate reporting, and stop collection contact in writing.

How do I avoid default on an ECSI loan?

Contact ECSI before reaching 60 days past due. Ask specifically about deferment, forbearance, payment plan arrangements, and any hardship accommodations available for your loan type and institution. For Perkins Loans, deferment is available for enrollment, unemployment, economic hardship, military service, and qualifying professional service. For institutional loans, the school determines what accommodations exist. Acting early preserves options that close as delinquency progresses.

Can a defaulted ECSI account be removed from my credit report?

Not simply by paying the debt. Payment resolves the financial obligation but does not remove the reporting. Inaccurate entries including wrong dates, incorrect balances, duplicate tradelines, and errors in account status are disputable under the FCRA and removable if the furnisher cannot verify the reported information. Accurate entries remain for seven years from the original delinquency date.

What should I do after missing a student loan payment?

Contact ECSI the same day at heartland.ecsi.net. Ask about payment plans, deferment, forbearance, and any hardship accommodations for your loan type. Pull all three bureau reports from AnnualCreditReport.com within one week. Verify what is being reported and check for errors. If a collection agency contacts you, send a written debt validation request within 30 days. Do not wait for the situation to resolve itself.

ECSI Delinquency or Collection Showing on Your Report? Start Here.

A free 3-bureau audit shows exactly what Equifax, Experian, and TransUnion are reporting on every account including ECSI-serviced loans, third-party collection accounts assigned by the institution, and any entry with wrong dates, incorrect balances, or inaccurate status under the FCRA. 20+ years in business. 3,000+ five-star reviews. 100% money-back guarantee on inaccurate item removal.

Get My Free Credit Blueprint → Secure · No hard inquiry · No credit card required-

Why Your Credit Score Dropped Suddenly Because of a Student Loan September 2025 — Covers the 2025 student loan credit crisis, how delinquency reporting restarts after payment pauses affect borrowers who thought they were current, how servicer transfers reset payment history, and the four-step dispute process for inaccurate student loan marks. Directly relevant for any borrower whose ECSI account status changed unexpectedly.

-

How Long Do Student Loans Stay on Your Credit Report After Default? September 2025 — Exact timelines for how long defaulted student loans report across Equifax, Experian, and TransUnion, which removal strategies apply at each stage, and how to rebuild your score while the marks are still present. Covers Perkins Loans, institutional loans, and federal loan defaults including the rehabilitation process that restores eligibility for deferment and cancellation benefits.

-

ConServe Student Loan Collections: Complete Guide to Protecting Your Credit May 2025 — Covers what happens after a student loan is assigned to a third-party collection agency, your FDCPA debt validation rights, how to negotiate settlement on institutional loan collections, and what pay-for-delete and dispute strategies are available once a collector is involved. Directly relevant for any ECSI account that has been referred to an external agency.