Quick Answer: Elan Financial Services is likely a credit card you have through your bank or credit union. They're a division of U.S. Bank that issues cards for over 1,400 financial institutions.

Here's how to identify which card it is and what to do about it.

What is Elan Financial Services?

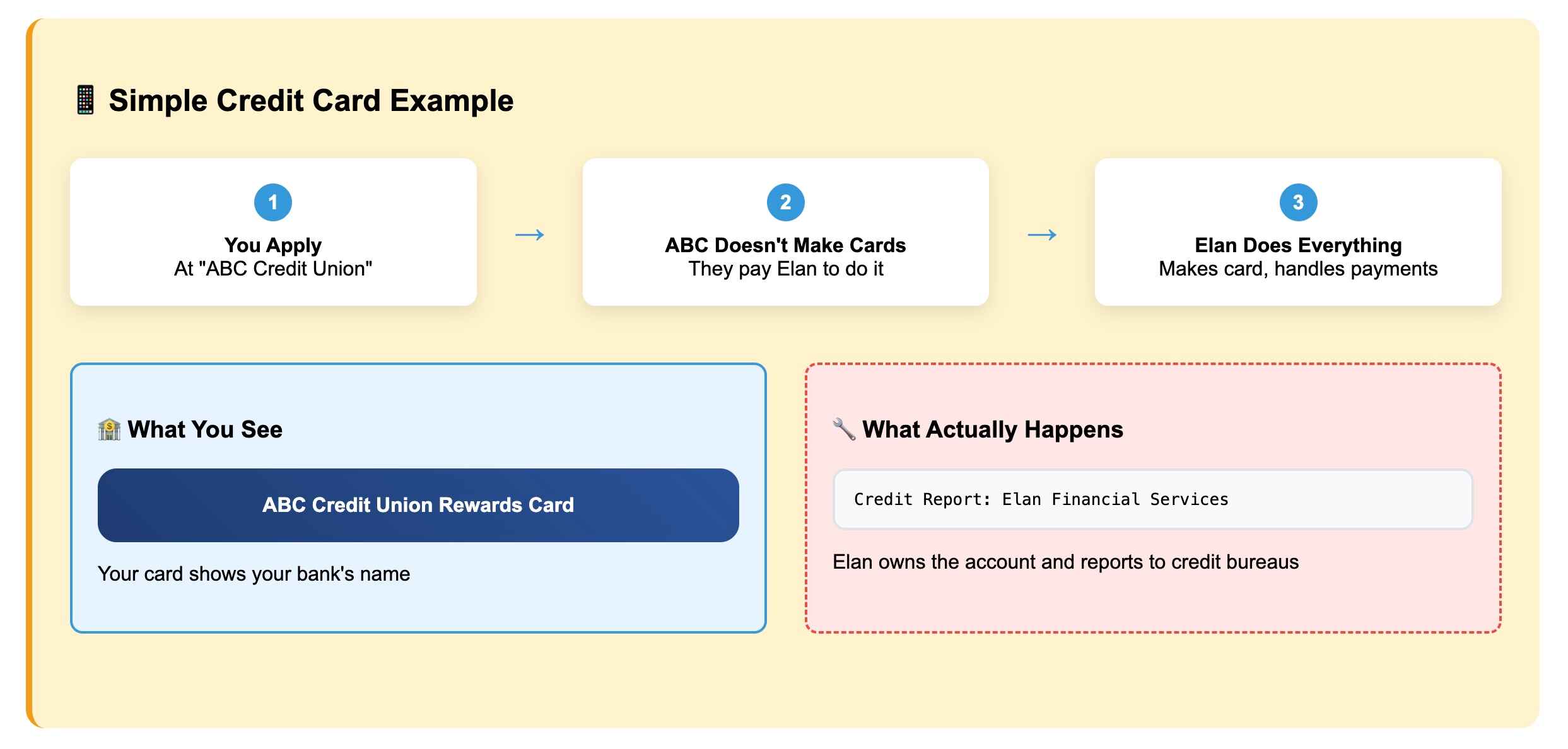

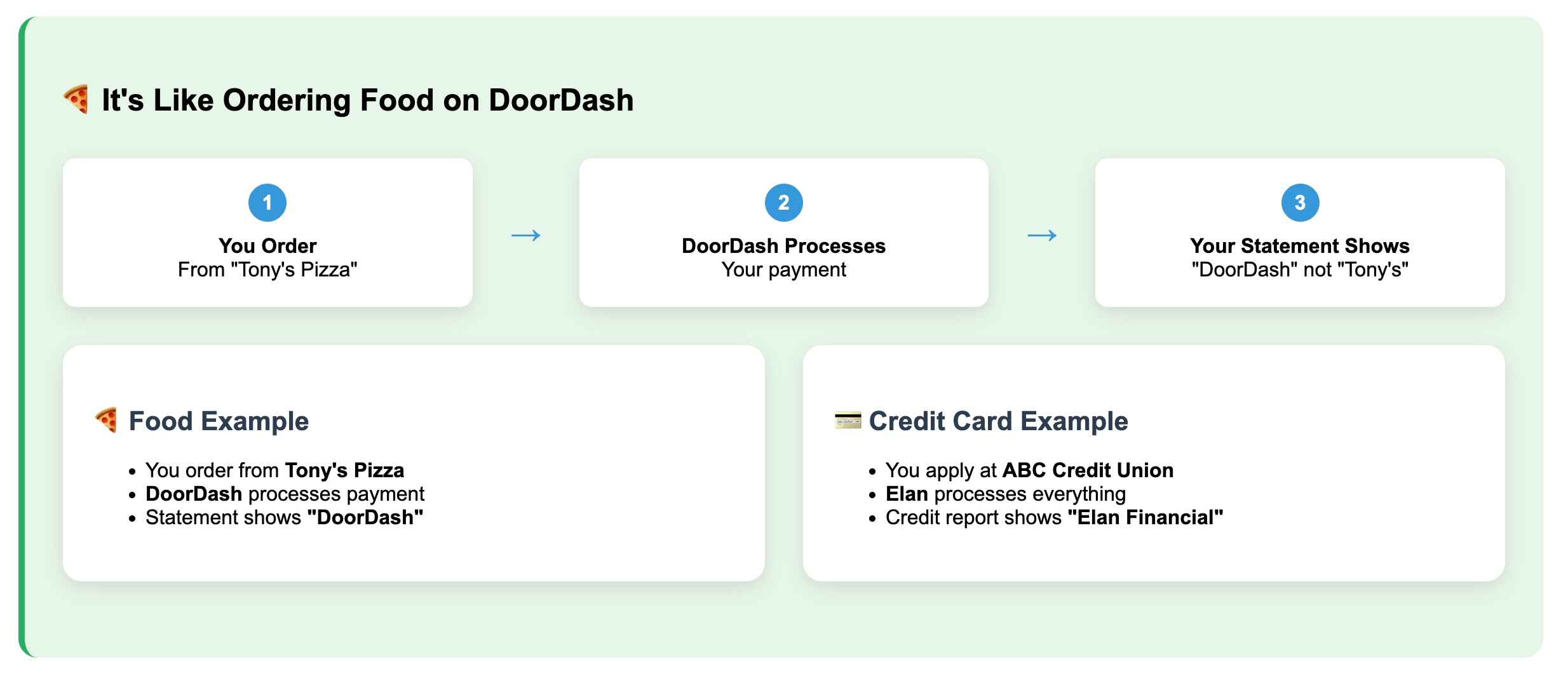

Elan Financial Services is U.S. Bank's credit card division that partners with local banks and credit unions. When you apply for a credit card at your community bank, Elan often handles the actual credit card operations behind the scenes.

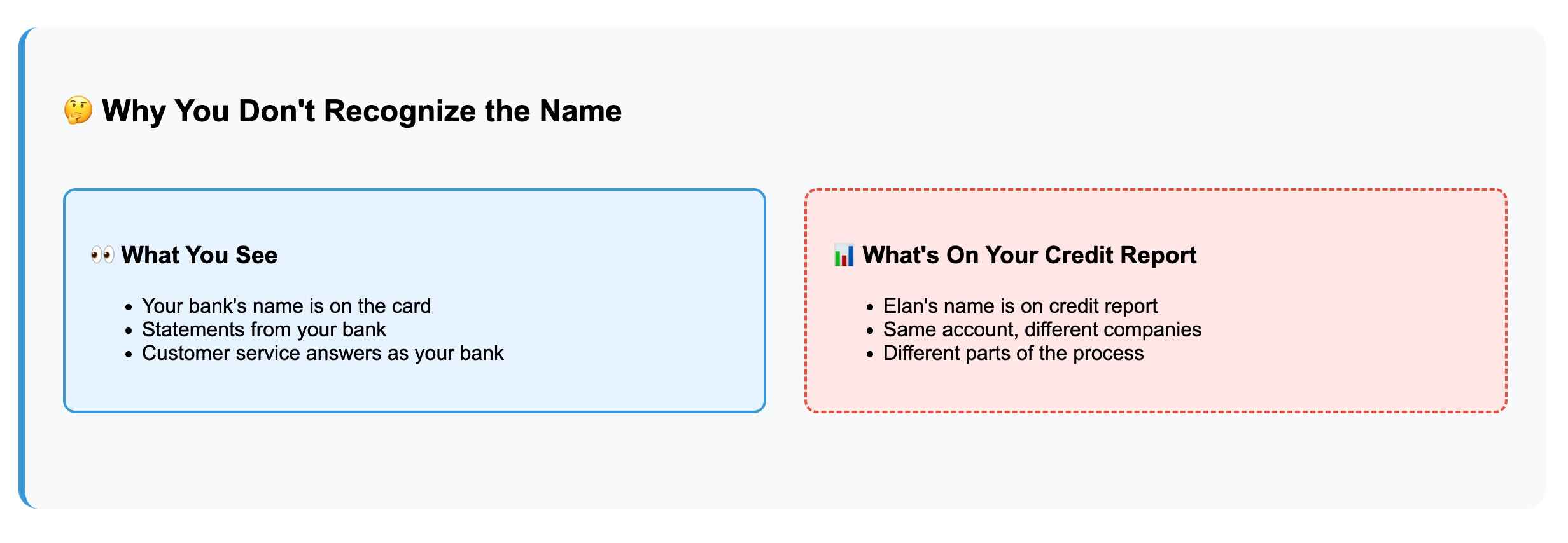

Why you don't recognize the name: Your card shows your bank's name, but Elan reports to credit bureaus since they're the actual issuer.

Understanding What Elan Financial Services Do

Elan Financial Services operates as a "white label" credit card processor. Here's how their business model works:

The Partnership Model: Elan partners with smaller community banks and credit unions that want to offer credit cards to their customers but don't have the infrastructure, expertise, or resources to manage credit card operations themselves. Running a credit card program requires significant technology, compliance, fraud detection, customer service, and regulatory expertise.

Behind-the-Scenes Operations: When you get a credit card from your local bank or credit union, Elan often handles:

- Credit underwriting and approval decisions

- Card production and mailing

- Transaction processing

- Monthly billing and statements

- Customer service calls

- Fraud monitoring

- Regulatory compliance

- Reporting to credit bureaus

Why It's Confusing: It’s the part is that while your card displays your local bank's branding and you think you're dealing with them, Elan is actually the entity that:

- Makes credit decisions

- Reports your account to credit bureaus (which is why "Elan Financial Services" appears on your credit report, not your local bank)

- Handles most operational aspects

The Value Proposition:

- For small banks/credit unions: They can offer competitive credit cards without massive infrastructure investment

- For customers: You get to bank locally while accessing sophisticated credit card features

- For Elan/U.S. Bank: They expand their credit card portfolio through partnerships

This “private label" model is common in banking, where one company provides the backend operations while another company provides the customer-facing brand.

This simple model below shows how Elan Financial Services work:

How to Identify Your Elan Financial Services Card

Finding "Elan Financial Services" on your credit report without knowing which card it represents can be stressful. Many people's first thought is identity theft or credit report errors.

The Reality: In 95% of cases, this is simply a credit card you legitimately have through your bank or credit union. The confusion comes from the behind-the-scenes business relationships you weren't aware of.

Here are four simple steps to identify exactly which of your credit cards is connected to that mysterious "Elan Financial Services" entry on your credit report.

Step 1: Check Your Credit Cards

On the Back of Your Card:

- Flip over every credit card you have

- Look for tiny text at the bottom (you might need reading glasses!)

- Search for these exact phrases:

- "Issued by Elan Financial Services"

- "Serviced by U.S. Bank"

- "Member FDIC U.S. Bank"

- Sometimes just "Elan" in small print

Example: Your card says "First Community Credit Union" on the front, but the back might say "Issued by Elan Financial Services, Member FDIC"

On Your Statements:

- Return address on mailed statements: Look for "Elan Financial Services" or "U.S. Bank" in the return address

- Email statements: Check the "from" address - might be something like "noreply@elanfinancialservices.com"

- Payment address: Where you mail payments - often shows Elan's address

Step 2: Match Credit Report Details

Get Your Credit Report First:

- Go to AnnualCreditReport.com (the official free site)

- Download your report from one of the three bureaus

Look for the Elan Entry: Find "Elan Financial Services" in your accounts list and write down these key details:

Account Opening Date:

- Credit report shows: "Opened 03/2022"

- Think: "Which card did I get in March 2022?"

- Check your cards - when did you apply for each one?

Credit Limit:

- Credit report shows: "$5,000 limit"

- Check your cards: Which one has exactly $5,000 limit?

- This is usually the easiest way to match

Current Balance:

- Credit report shows: "$1,247 balance"

- Check your card balances: Which one owes about $1,247?

- Balances change daily, so it might be close but not exact

Example Match:

- Credit report: Elan Financial, opened 03/2022, $5,000 limit, $1,200 balance

- Your First Community card: Got it March 2022, $5,000 limit, current balance $1,180

- Match! Your First Community card is the Elan account

Step 3: Check Online Accounts

Log Into Your Bank's Website: Go to your bank's credit card section and look in these specific places:

Account Details Page:

- Sometimes shows "Serviced by Elan Financial Services"

- Might be in small print at bottom of page

- Look for "Powered by U.S. Bank" or similar

Terms of Service:

- Click on "Terms and Conditions"

- Search (Ctrl+F) for "Elan" or "U.S. Bank"

- Often buried in legal text

Customer Service Info:

- Look at the customer service phone number

- If it's 1-800-236-8873, that's Elan

- Compare with numbers on your physical cards

Download Statements:

- PDF statements sometimes show more detail

- Look in headers, footers, or fine print

- Might show processing company information

Step 4: Call Customer Service

What to Say: "Hi, I see this card on my credit report under 'Elan Financial Services' - is this card serviced by them?"

Don't say: "I don't recognize Elan Financial Services" (they might think it's fraud)

What They'll Tell You:

- "Yes, your account is serviced by Elan Financial Services"

- Or: "Your account is processed through U.S. Bank's Elan division"

- They should confirm immediately - this isn't secret information

If They Don't Know:

- Ask to speak to a supervisor

- Some front-line reps might not know the backend details

- Be patient - smaller banks sometimes train staff differently

Phone Numbers to Try:

- Call the number on the back of each card

- Customer service hours vary by bank

- Have your account number ready

Real-World Example Walkthrough

Sarah's Situation:

- Sees "Elan Financial Services" on credit report

- Has cards from: Chase, Local Credit Union, Capital One

Step 1 - Physical Check:

- Chase card back: "Issued by JPMorgan Chase"

- Credit Union card back: "Member FDIC, Serviced by U.S. Bank"

- Capital One card back: "Issued by Capital One"

Step 2 - Credit Report Match:

- Elan entry: Opened 06/2023, $3,000 limit

- Credit Union card: Applied June 2023, $3,000 limit

Step 3 - Online Check:

- Logs into credit union website

- Customer service number: 1-800-236-8873 (That's Elan's number!)

Step 4 - Confirmation Call:

- Calls credit union: "Is my card serviced by Elan?"

- Rep: "Yes, we partner with Elan Financial Services for credit cards"

Result: Mystery solved! Her credit union card is the Elan account.

Common Financial Institutions That Uses Elan Financial Services

Elan partners with over 1,400 institutions, including:

- Community banks

- Credit unions

- Regional banks

- University credit unions

- Employee credit unions

Personal Experience Note: I've helped dozens of clients identify these accounts. In 95% of cases, it's a legitimate card from their local bank or credit union that they simply didn't realize was backed by Elan.

What to Do If You Still Don't Recognize It

If You Can't Identify the Account:

- Call Elan directly: 1-800-236-8873

- They can verify if you have an account

- Ask for account opening details

- Request application copy

- See where and when it was opened

- Check for address discrepancies

If it's fraud:

- File a police report

- Place fraud alert on credit reports

- Dispute with credit bureaus

Red Flags to Watch For:

- Account opened at address you never lived at

- Different phone number on application

- No memory of applying for credit

How Elan Financial Services Affects Your Credit Score

If you've been paying your Elan card on time, it's contributing positively to your credit score in multiple ways.

Many people don't realize that an account they didn't recognize was actually boosting their credit the whole time.

Payment History - 35% of Your Credit Score

What to Look For on Your Credit Report:

- "Current" - You're up to date with payments

- "Paid as Agreed" - You're following the original terms

- "30 days late," "60 days late," etc. - These hurt your score

Real Impact:

- Every on-time payment on your Elan card adds to your positive payment history

- Even if you only pay the minimum, it counts as "on time"

- Late payments stay on your report for 7 years and hurt your score

Example: If your Elan account shows 24 months of "Paid as Agreed," that's 24 positive marks helping your credit score, even if you didn't know it was Elan reporting them.

Credit Utilization - 30% of Your Credit Score

What This Means:

- Formula: Current Balance ÷ Credit Limit = Utilization Rate

- Good: Under 30% utilization

- Better: Under 10% utilization

- Best: Under 5% utilization

Real Examples:

- Elan card: $500 balance, $2,000 limit = 25% utilization (Good)

- Elan card: $1,800 balance, $2,000 limit = 90% utilization (Bad)

Your Elan card's utilization affects both your individual card utilization AND your overall credit utilization across all cards.

Double Impact:

- Individual card utilization: Each card should be under 30%

- Overall utilization: All your cards combined should be under 30%

Account Age - 15% of Your Credit Score

How It Helps:

- Average Account Age: Older accounts increase your average

- Credit History Length: Shows you can maintain accounts long-term

- Established Credit: Demonstrates stability to lenders

Real Impact: If your Elan account is 3 years old, it's contributing to making your overall credit history look more established and mature.

Example:

- Your cards: 6 months old, 1 year old, 3 years old (Elan)

- Average age: 1.5 years (better than without the Elan account)

Why You Shouldn't Close the Account

The Danger: Closing your Elan account (unless it's fraudulent) can hurt your credit score in several ways:

1. Immediate Utilization Increase:

- Before closing: $1,000 total balances, $10,000 total limits = 10% utilization

- After closing Elan ($3,000 limit): $1,000 total balances, $7,000 total limits = 14% utilization

- Higher utilization = lower credit score

2. Future Account Age Impact:

- Closed accounts eventually fall off your credit report (after 10 years)

- When they do, your average account age decreases

- This can hurt your score years later

3. Loss of Credit Mix:

- Having different types of credit (cards, loans, etc.) helps your score

- Closing accounts reduces your credit mix

How Elan Financial Services Affects Your Credit Score

If you've been paying your Elan card on time, it's contributing positively to your credit score in multiple ways.

Many people don't realize that an account they didn't recognize was actually boosting their credit the whole time.

Payment History - 35% of Your Credit Score

Payment history tracks whether you make your credit card and loan payments on time. It's the most important factor in your credit score calculation.

What to Look For on Your Credit Report:

"Current" - You're up to date with payments

"Paid as Agreed" - You're following the original terms "30 days late," "60 days late," etc. - These hurt your score

Impact: Every on-time payment on your Elan card adds to your positive payment history Even if you only pay the minimum, it counts as "on time". Late payments, on the other hand, stay on your report for 7 years and hurt your score

Example: If your Elan account shows 24 months of "Paid as Agreed," that's 24 positive marks helping your credit score, even if you didn't know it was Elan reporting them.

Credit Utilization - 30% of Your Credit Score

Credit utilization measures how much of your available credit you're currently using. It's calculated by dividing your current balance by your credit limit.

Formula: Current Balance ÷ Credit Limit = Utilization Rate

- Good: Under 30% utilization

- Better: Under 10% utilization

- Best: Under 5% utilization

Example:

Elan card: $500 balance, $2,000 limit = 25% utilization (Good)

Elan card: $1,800 balance, $2,000 limit = 90% utilization (Bad)

Your Elan card's utilization affects both your individual card utilization AND your overall credit utilization across all cards.

Double Impact: Individual card utilization: Each card should be under 30% Overall utilization: All your cards combined should be under 30%

Account Age - 15% of Your Credit Score

According to Nerdwallet, account age considers how long you've had your credit accounts open. Lenders view longer credit histories as a sign of financial stability and responsible credit management.

How It Helps:

- Average Account Age: Older accounts increase your average

- Credit History Length: Shows you can maintain accounts long-term

- Established Credit: Demonstrates stability to lenders

Real Impact: If your Elan account is 3 years old, it's contributing to making your overall credit history look more established and mature.

Example: Your cards: 6 months old, 1 year old, 3 years old (Elan) Average age: 1.5 years (better than without the Elan account)

Why You Shouldn't Close an Elan Financial Services Account

Closing your Elan account (unless it's fraudulent) can hurt your credit score in several ways:

Immediate Utilization Increase:

- Before closing: $1,000 total balances, $10,000 total limits = 10% utilization

- After closing Elan ($3,000 limit): $1,000 total balances, $7,000 total limits = 14% utilization

- Higher utilization = lower credit score

Future Account Age Impact:

- Closed accounts eventually fall off your credit report (after 10 years)

- When they do, your average account age decreases

- This can hurt your score years later

Loss of Credit Mix:

- Having different types of credit (cards, loans, etc.) helps your score

- Closing accounts reduces your credit mix

What Each Elan Financial Services Credit Report Status Means

Every account on your report, including those from Elan Financial Services, tells a story about your payment habits and financial responsibility. Understanding what each status means can help you maintain a strong credit profile and catch potential issues early.

Positive Statuses (Good for Your Score):

- "Current" - Account is up to date

- "Paid as Agreed" - Following original terms

- "Account Closed by Consumer" - You closed it, but payment history remains

Negative Statuses (Bad for Your Score):

Understanding how much each negative status can impact your credit score helps you prioritize which issues to address first:

- "30 Days Past Due" - Minor negative impact (10-25 point drop)

- "60 Days Past Due" - Moderate negative impact (25-50 point drop)

- "90+ Days Past Due" - Major negative impact (50-80 point drop)

- "Charge-off" - Severe negative impact (80-120 point drop)

- "Collections" - Very severe negative impact (100-150 point drop)

Note: The actual impact varies based on your overall credit profile, with higher scores typically seeing larger drops from negative marks.

Action Steps Based on Your Account Status

If Your Elan Account Shows "Current" or "Paid as Agreed":

- Keep the account open

- Continue making on-time payments

- Keep utilization low

- Celebrate - it's helping your credit!

If Your Elan Account Shows Late Payments:

- Call customer service to discuss payment plans

- Set up autopay to avoid future late payments Make payments on time going forward

- Wait - negative marks fade over time

If Your Elan Account Shows Charge-off or Collections:

- Contact Elan immediately to discuss resolution

- Consider settlement if you can't pay in full

- Get any agreement in writing

- Monitor your credit report for updates

- Work with a reputable credit repair company

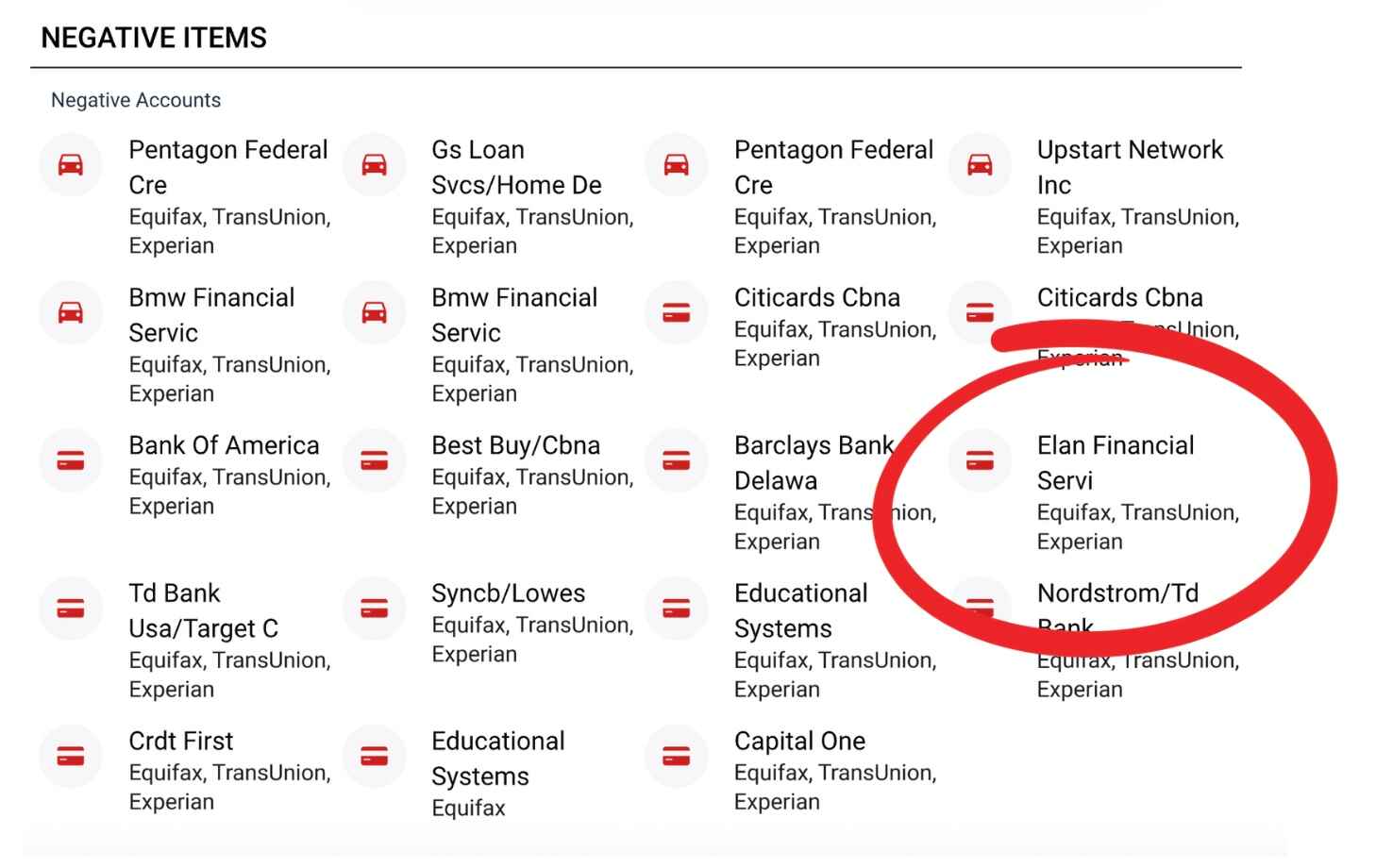

What If You See Elan Financial Services as a Negative Item?

When Elan Financial Services appears as a negative entry on your credit report, it typically indicates an unresolved issue with a credit card account they service. Understanding the nature of the negative entry and taking appropriate action can help minimize its impact on your credit score.

First, Don't Panic

Most negative Elan entries fall into common categories that many people face. You might be dealing with late payments from a card you forgot about, charge-offs from an account you stopped paying, collections from unpaid balances, or even fraudulent accounts opened in your name. Each situation has a path forward, so take a deep breath and focus on taking the right steps.

Start by Verifying the Account

Before you do anything else, make sure this account actually belongs to you. Check the account details on your credit report carefully. Do you remember getting a card around the opening date listed? Does the credit limit match any card you had? Was it opened at your current or previous address? These details will help you determine if you're dealing with a legitimate debt or potential fraud.

You Can Contact Elan Financial Services Directly

Call 1-800-236-8873 and ask specific questions about the account. You'll want to verify that the account belongs to you, understand the current status and balance, and explore what options you have to resolve the issue. During this conversation, document everything including the date, time, representative's name, and any reference numbers they provide. This documentation will be crucial if you need to reference the conversation later.

If It's a Legitimate Debt You Recognize

For recent late payments, your best bet is to set up autopay immediately to prevent future issues. You can also ask if they'll remove the late payment as a goodwill gesture, especially if you've been a good customer otherwise. The key is to continue making on-time payments going forward, as consistent positive payment history will gradually outweigh the negative mark.

If you're dealing with a charge-off, don't ignore it hoping it will disappear.

Ask about rehabilitation programs or request a payment plan you can realistically afford. Always get any agreement in writing before making payments, and remember that charge-offs can potentially lead to lawsuits if left unresolved.

Collections require a slightly different approach.

Request debt validation in writing first, then ask about "pay for delete" agreements where they remove the negative mark in exchange for payment. If you can't pay the full amount, negotiate a settlement, but again, get everything in writing before sending any money.

If It's Not Your Account

Suspected fraud requires immediate action across multiple fronts. Contact all three credit bureaus to place fraud alerts, file disputes with each bureau, and file a police report. You'll also need to contact Elan directly to report the fraudulent account. Going forward, monitor your credit reports closely for any additional suspicious activity.

Focus on Recovery

While the negative item will hurt your score initially, you can minimize the damage through positive actions. Pay down other credit card balances to improve your utilization ratio, make all other payments on time, and avoid closing other credit accounts. Consider becoming an authorized user on someone else's account if they have excellent payment history. Most importantly, be patient because negative items hurt less over time as you build positive payment history.

Remember that even with a negative Elan entry, you can still rebuild your credit effectively. Focus on positive actions going forward rather than dwelling on past mistakes. Your credit score isn't permanent, and consistent good habits will gradually overshadow any negative marks from the past.

How to Dispute Elan Financial Services Charges

If you need to dispute charges or account issues:

Step 1: Try Direct Resolution

- Call customer service first: 800-236-8873

- Have your account number and specific details ready

- Ask for a supervisor if the first representative can't help

- Get a reference number for your call

Step 2: File a Formal Dispute

- Write a dispute letter if phone doesn't work

- Include: Account number, transaction details, reason for dispute

- Send certified mail to: P.O. Box 790084, St. Louis, MO 63179-0084

- Keep copies of everything

Step 3: Contact Your Original Bank

Remember: Your local bank/credit union may also help

- They have a relationship with Elan and can sometimes resolve issues faster

- This is often overlooked but very effective

Step 4: File Complaints if Needed

- Consumer Financial Protection Bureau (CFPB): consumerfinance.gov

- Better Business Bureau

- Your state's attorney general office

How to Make Payments to Elan Financial Services

If you have a credit card issued through Elan Financial Services, you'll need to make payments directly to them rather than your local bank.

Here are your payment options to ensure your payments are processed correctly and on time.

- Online: myaccountaccess.com

- Phone: 800-236-8873 (may have fees)

- Mail Payment Address: P.O. Box 790084, St. Louis, MO 63179-0084

Payment Tips:

- Allow 3-5 business days for mailed payments.

- Online payments typically post same day if made before cutoff.

- Set up autopay to avoid late fees.

- Keep confirmation numbers for all payments.

Elan Financial Services Contact Information

- Main Customer Service: 800-236-8873

- Hours: 8:00 a.m. - 9:00 p.m. CT Monday-Thursday, 8:00 a.m. - 5:00 p.m. CT Friday, 9:00 a.m. - 1:00 p.m. CT Saturday

- Payment Address: P.O. Box 790084, St. Louis, MO 63179-0084

Common Consumer Issues with Elan Financial Services

Based on customer reviews, here are common problems:

- Payment Issues

- Late payment processing

- Autopay failures

- Payment posting delays

- Difficulty making payments online

Elan Financial Services Reviews

- Long wait times (average customer rating: 1.4/5)

- Difficulty reaching representatives

- Inconsistent information from different agents

- Policy enforcement issues

- Account Management Problems

- Unexpected credit limit decreases

- Account closure without notice

- Difficulty updating account information

Why These Issues Matter to Your Credit Score

The most serious concern is how payment problems can devastate your credit.

When Elan's system failures cause:

- Missed payments - Even one late payment can drop your score 60-110 points

- Payment posting delays - Your payment might arrive on time but post late, triggering late fees and credit damage

- Autopay failures - You think you're covered, but the payment doesn't go through

The Credit Score Impact:

- Payment history is 35% of your credit score - the largest factor

- Late payments stay on your report for 7 years

- Recent late payments hurt more than older ones

- Multiple late payments compound the damage

What to Do:

- Monitor your account obsessively. Check that payments post correctly.

- Pay early, not on the due date. Give yourself a buffer for processing delays.

- Get confirmation numbers for all payments and requests.

- Set up alerts for due dates and payment confirmations.

- Document everything. Keep records of all communications.

- Follow up in writing for important issues.

From 17 years of credit counseling experience: The biggest mistake people make is assuming their payment system works perfectly. With Elan's documented payment processing issues, you need to be extra vigilant like consistently MONITORING your credit score for your protection. You can start with a credit analysis.

When to Seek Help

Contact a credit repair expert if:

- You find multiple unrecognized accounts

- You're overwhelmed by credit report errors

- You need help understanding your credit situation

- You're having ongoing disputes with Elan

Free Resource: National Foundation for Credit Counseling (NFCC.org) offers free credit counseling.

Bottom Line When You Have Elan Financial Services on Credit Report

Finding Elan Financial Services on your credit report is typically not a problem - it's just the behind-the-scenes name for a credit card you legitimately have. Use the steps above to identify which card it is, and remember that if you've been paying on time, this account is actually helping your credit score.

Key Takeaway: The credit industry has many partnerships that aren't obvious to consumers. Understanding these relationships helps you better manage your credit and avoid unnecessary worry.

Still confused? Call Elan at 1-800-236-8873 or contact your bank's customer service. They can quickly clarify which account this represents and put your mind at ease.

This guide is based on real client experiences and industry knowledge. Always verify account details directly with your creditors if you have concerns about entries on your credit report.

Recommended Articles

SynCom Collections: How to Deal with Synergetic Communication Debt Collectors

How to Remove Cedars Business Services from Your Credit Report (Step-by-Step)

Columbia Debt Recovery: Who They Are and How to Deal with Them