This comprehensive guide, inspired by the widely recognized 50/30/20 rule, provides a practical framework for taking charge of your finances and ensuring you not only avoid financial pitfalls but also build a secure financial future. By understanding this simple yet powerful rule, you'll learn how to allocate your income effectively, prioritize your financial goals, and make informed decisions that align with your long-term aspirations.

By embracing the principles outlined in this comprehensive guide, you'll embark on a journey towards financial well-being and secure a brighter future. With discipline, informed decisions, and a commitment to your financial goals, you can achieve financial stability, overcome financial hurdles, and unlock a path towards a fulfilling and prosperous life.

Contents:

- Decoding the 50/30/20 Rule

- Budgeting for Every Income Bracket

- Smart Money Allocation: Needs, Wants, and Savings

- Customize Your Plan with Our Calculator: Embracing Financial Empowerment

- Planning for Retirement: A Glimpse into Financial Freedom

- Conclusion: Embracing a Secure and Fulfilling Future

Decoding the 50/30/20 Rule

In the realm of personal finance, the 50/30/20 rule stands as a cornerstone of effective budgeting. This simple yet powerful guideline provides a framework for allocating your income towards essential expenses, discretionary spending, and financial goals. By adhering to this rule, individuals can achieve a sense of balance and control over their finances, paving the way for a secure and fulfilling financial future.

Understanding the 50/30/20 Breakdown

The 50/30/20 rule divides your after-tax income into three distinct categories:

Needs (50%): These are the non-negotiable expenses that you must cover to maintain your basic living standards. They encompass housing, food, utilities, transportation, healthcare, and minimum debt payments.

Wants (30%): These are the discretionary expenses that enhance your lifestyle but are not essential for survival. They include dining out, entertainment, travel, hobbies, and non-essential clothing purchases.

Savings and Debt Repayment (20%): This category is dedicated to securing your financial future. It includes contributions to savings accounts, retirement plans, and debt repayment towards credit cards, loans, or other outstanding debts.

Adapting the Rule to Your Income

The beauty of the 50/30/20 rule lies in its flexibility. It serves as a guideline rather than a rigid directive, allowing you to adjust the percentages based on your unique financial circumstances. For instance, if you have high housing costs, you may need to allocate more than 50% to needs. Conversely, if you are debt-free and have a secure income, you may choose to allocate more than 20% to savings and investments.

Benefits of Embracing the 50/30/20 Rule

Adopting the 50/30/20 rule offers a multitude of benefits:

Promotes Financial Awareness: The rule encourages you to track your income and expenses, fostering a deeper understanding of your financial habits.

Encourages Responsible Spending: By allocating a specific percentage to wants, the rule curbs impulse spending and promotes mindful financial decisions.

Prioritizes Savings and Financial Goals: The rule ensures that a significant portion of your income is dedicated to savings and debt repayment, laying the groundwork for long-term financial security.

Provides a Sense of Control: The rule empowers you to take charge of your finances, reducing stress and anxiety related to money.

Implementing the 50/30/20 Rule in Practice

To effectively implement the 50/30/20 rule, follow these steps:

Calculate Your After-Tax Income: Subtract taxes from your gross income to determine your disposable income.

Categorize Your Expenses: Track your expenses for a month to categorize them as needs, wants, or savings/debt repayment.

Allocate Your Income: Divide your after-tax income according to the 50/30/20 rule.

Create a Budget: Use a budgeting tool or spreadsheet to manage your income and expenses effectively.

Review and Adjust: Regularly review your budget and make adjustments as your income or expenses change.

Remember, the 50/30/20 rule is a starting point, not a rigid formula. Tailor it to your specific financial situation and lifestyle to achieve a balanced and sustainable approach to money management.

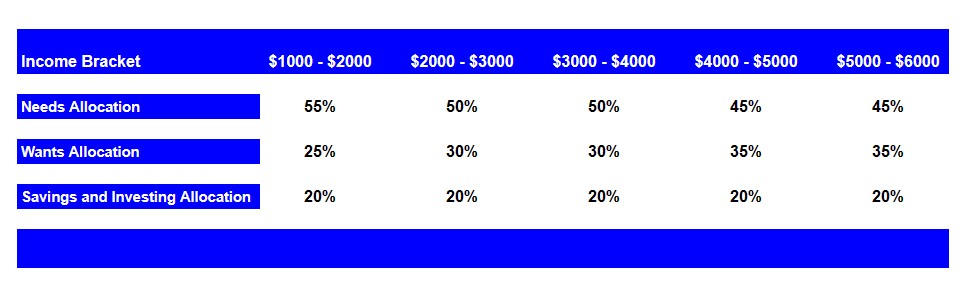

Budgeting for Every Income Bracket

Regardless of your income level, effective budgeting is the cornerstone of achieving financial stability and pursuing your long-term goals. Here's a comprehensive guide to budgeting tailored to different income brackets, ensuring you make the most of your hard-earned money.

Income Bracket: $1,000 - $2,000

In this income bracket, prioritizing essential expenses and making prudent financial decisions is crucial. Allocate:

55% to Needs: Focus on covering housing, food, utilities, transportation, and minimum debt payments.

25% to Wants: Enjoy occasional dining out, entertainment, or hobbies, but be mindful of your spending.

20% to Savings and Debt Repayment: Start building an emergency fund and prioritize debt repayment.

Income Bracket: $2,000 - $3,000

With a slightly higher income, you can gradually increase your savings while still enjoying some flexibility:

50% to Needs: Continue covering essential expenses while exploring cost-saving measures.

30% to Wants: Allow yourself more occasional indulgences and start saving for short-term goals.

20% to Savings and Debt Repayment: Increase contributions to savings and debt repayment, aiming to eliminate high-interest debts.

Income Bracket: $3,000 - $4,000

At this income level, you can strike a balance between needs, wants, and financial goals:

50% to Needs: Maintain essential expenses while considering upgrades or improvements to your lifestyle.

30% to Wants: Enjoy regular dining out, entertainment, and travel without overspending.

20% to Savings and Debt Repayment: Boost savings for long-term goals, such as a down payment on a house or retirement planning.

Income Bracket: $4,000 - $5,000

With a more comfortable income, you can prioritize financial security and future aspirations:

45% to Needs: Maintain essential expenses while considering larger purchases or investments.

35% to Wants: Enjoy regular dining out, entertainment, and travel while saving for short-term goals.

20% to Savings and Debt Repayment: Maximize savings for long-term goals, such as retirement or children's education.

Income Bracket: $5,000 - $6,000

In this income bracket, you can focus on financial growth and achieving your long-term dreams:

45% to Needs: Maintain essential expenses while considering significant upgrades to your lifestyle.

35% to Wants: Enjoy regular dining out, entertainment, and travel while saving for short-term goals.

20% to Savings and Debt Repayment: Aggressively save for long-term goals and invest in wealth creation strategies.

Remember, these are just guidelines, and your actual budget will vary depending on your individual circumstances, such as family size, location, and lifestyle choices.

Additional Budgeting Tips:

Create a budget: Use a budgeting method that suits your style, such as the 50/30/20 rule or zero-based budgeting.

Track your expenses: Regularly monitor your spending to identify areas where you can cut back.

Automate savings: Set up automatic transfers from your checking account to savings and investment accounts.

Review and adjust: Regularly review your budget and make adjustments as your income or expenses change.

By following these budgeting strategies and adapting them to your specific financial situation, you can take control of your finances, secure your future, and achieve your financial goals.

Smart Money Allocation: Needs, Wants, and Savings

Effective money allocation is the cornerstone of financial well-being. It's about understanding your income, expenses, and financial goals, and then distributing your hard-earned money in a way that aligns with your priorities. By striking a balance between needs, wants, and savings, you can achieve financial stability, fulfill your aspirations, and secure a prosperous future.

Understanding the Three Pillars of Money Allocation

Needs: These are the essential expenses that you must cover to maintain your basic living standards. They include housing, food, utilities, transportation, healthcare, and minimum debt payments.

Wants: These are the discretionary expenses that enhance your lifestyle but are not essential for survival. They include dining out, entertainment, travel, hobbies, and non-essential clothing purchases.

Savings and Investing: This category is dedicated to securing your financial future. It includes contributions to savings accounts, retirement plans, and debt repayment towards credit cards, loans, or other outstanding debts.

Allocating Your Income Based on Income Level

The ideal allocation of your income will depend on your specific financial situation, including your income level, family size, location, and lifestyle choices. However, as a general guideline, you can follow these suggested percentages:

Prioritizing Needs and Building a Financial Foundation

Regardless of your income level, it's crucial to prioritize your needs. These are the non-negotiable expenses that ensure your basic well-being and enable you to function in society. Covering your needs should be your top financial priority before allocating funds to wants or savings.

Balancing Wants and Enjoying Life's Pleasures

While needs are essential, wants also play a role in your overall well-being and happiness. Allocating a portion of your income to wants allows you to enjoy life's pleasures, pursue hobbies, and engage in activities that bring you fulfillment. The key is to balance your wants with your financial responsibilities and avoid overspending.

Investing in Your Future: Savings and Debt Repayment

Saving for the future is essential for achieving long-term financial security. Whether it's building an emergency fund, saving for a down payment on a house, or planning for retirement, regular contributions to savings accounts and investment plans are crucial. Additionally, prioritizing debt repayment, especially high-interest debts, can reduce your financial burden and improve your overall financial health.

The Art of Balancing Financial Priorities

Balancing your financial priorities is an ongoing process that requires self-awareness, discipline, and regular adjustments. Here are some tips for achieving a balanced approach to money allocation:

Track Your Income and Expenses: Use a budgeting tool or spreadsheet to track your income and expenses regularly. This will give you a clear picture of where your money is going and help you identify areas for improvement.

Create a Realistic Budget: Develop a budget that aligns with your income, expenses, and financial goals. Allocate a specific percentage of your income to each category of needs, wants, and savings.

Review and Adjust: Regularly review your budget and make adjustments as your income or expenses change. This will ensure that your budget remains relevant and effective.

Remember, effective money allocation is not about deprivation or strict limitations. It's about making conscious choices that align with your values, priorities, and long-term financial well-being. By striking a balance between needs, wants, and savings, you can achieve financial stability, fulfill your aspirations, and secure a prosperous future.

Customize Your Plan with Our Calculator: Embracing Financial Empowerment

Navigating the world of personal finance can be daunting, especially when it comes to creating a personalized budget that aligns with your unique financial situation. To ease this burden, have a user-friendly calculator that empowers you to take control of your finances and craft a budget tailored to your specific needs and goals.

Unveiling the Power of the Budget Calculator

Our intuitive calculator provides a straightforward platform to personalize your budget. Simply input your income, expenses, and financial objectives, and let the calculator work its magic. It will automatically calculate the ideal allocation of your income across the essential categories of needs, wants, and savings, ensuring a balanced and sustainable financial plan.

Step-by-Step Guide to Financial Clarity

Gather Your Financial Information: Before embarking on your budgeting journey, gather all your relevant financial information, including your income statements, expense records, and any outstanding debts.

Access the Budget Calculator: Visit the website or download the mobile app to access our user-friendly budget calculator.

Input Your Income: Start by entering your monthly after-tax income, which represents the amount of money you have left after taxes have been deducted from your gross pay.

Categorize Your Expenses: Divide your expenses into three categories: needs, wants, and savings.

Needs: These are the non-negotiable expenses that you must cover to maintain your basic living standards, such as housing, food, utilities, transportation, and healthcare.

Wants: These are the discretionary expenses that enhance your lifestyle but are not essential for survival, such as dining out, entertainment, travel, hobbies, and non-essential clothing purchases.

Savings: This category encompasses contributions to savings accounts, retirement plans, and debt repayment towards credit cards, loans, or other outstanding debts.

Enter Your Expenses: For each category, enter your average monthly expenses. This will give the calculator a clear picture of your spending patterns.

Set Your Financial Goals: Clearly define your short-term and long-term financial goals. This could include building an emergency fund, saving for a down payment on a house, or planning for retirement.

Calculate Your Personalized Budget: Once you've entered all the necessary information, click the "Calculate" button. Our calculator will analyze your inputs and generate a personalized budget that aligns with your financial situation and objectives.

Review and Adjust: Regularly review your budget and make adjustments as your income or expenses change. This will ensure that your budget remains effective and adaptable to your evolving financial circumstances.

Embrace Financial Wellness and Peace of Mind

By utilizing our budget calculator and adopting a mindful approach to money management, you can take control of your finances, alleviate financial stress, and pave the way for a secure and fulfilling financial future. Remember, financial wellness is a journey, not a destination. Embrace the process, make informed decisions, and celebrate your progress along the way.

Planning for Retirement: A Glimpse into Financial Freedom

Retirement, a time often envisioned as a period of leisure, relaxation, and pursuing personal passions, is a significant milestone in one's life. However, achieving a comfortable and secure retirement requires careful planning and proactive financial management. Strategic saving and investing throughout your working years can pave the way for a fulfilling and financially independent retirement.

The Power of Early Planning and Compounding

The key to unlocking the doors to a comfortable retirement lies in the power of early planning and compounding. When you start saving and investing early, you allow your money to grow over time through the magic of compounding. Compounding refers to the phenomenon where your investment earnings generate additional earnings, creating an exponential growth effect.

By starting to save for retirement early, even if it's just a small amount, you can harness the power of compounding and accumulate a substantial nest egg over time. This accumulated wealth can provide you with a steady stream of income during your retirement years, ensuring financial stability and peace of mind.

Strategies for Retirement Savings and Investments

A variety of savings and investment options are available to help you reach your retirement goals. Here are some of the most common and effective strategies:

Employer-Sponsored Retirement Plans: Many employers offer retirement plans, such as 401(k)s, that allow you to save for retirement through payroll deductions. These plans often come with employer matching contributions, essentially free money that can significantly boost your savings.

Individual Retirement Accounts (IRAs): IRAs are tax-advantaged retirement savings accounts that offer various tax benefits, such as tax-deferred or tax-free withdrawals in retirement. Two common IRA types are Traditional IRAs and Roth IRAs, each with distinct tax implications and eligibility requirements.

Investments: Diversifying your investments across different asset classes, such as stocks, bonds, and real estate, can help manage risk and potentially enhance returns over time. Consider investing in mutual funds or exchange-traded funds (ETFs) for a more diversified portfolio.

The Path to Early Retirement in Four Decades

Retiring comfortably in just four decades is an ambitious goal, but achievable with careful planning and disciplined execution. Here are some key strategies to consider:

Start Saving Early: As mentioned earlier, the power of compounding is most pronounced when you start saving early. Even small amounts saved consistently over time can accumulate significantly.

Maximize Employer Contributions: Take full advantage of employer matching contributions in your retirement plan. This is essentially free money that can significantly boost your savings.

Live Below Your Means: Adopting a frugal lifestyle and spending less than you earn can free up more money to save and invest for retirement.

Increase Savings Rate: As your income grows, consider increasing your savings rate to accelerate your retirement savings.

Make Wise Investment Choices: Educate yourself about different investment options and make informed decisions that align with your risk tolerance and investment horizon.

Remember, retirement planning is a journey, not a destination. Regularly review your progress, adjust your strategies as needed, and stay committed to your long-term financial goals. By taking charge of your finances today, you can secure a comfortable and worry-free retirement in the future.

Conclusion: Embracing a Secure and Fulfilling Future

As we conclude our exploration of budgeting, saving, and investing strategies, it's essential to recognize that mastering your finances is the cornerstone of a secure and fulfilling future. By taking control of your money today, you lay the foundation for a lifetime of financial well-being.

The 50/30/20 rule provides a simple yet effective framework for allocating your income towards essential needs, discretionary wants, and long-term financial goals. Adapt this rule to your unique circumstances, ensuring a balance that aligns with your priorities and aspirations.

Effective money management extends beyond budgeting and saving. It encompasses a mindset of financial responsibility, making informed decisions that align with your long-term objectives. Avoid impulse purchases, resist overspending, and prioritize building a solid financial foundation.

Your path to financial well-being starts with the decision to take control of your finances. Embrace the principles outlined in this guide, customize your strategies, and embark on a journey towards a secure and fulfilling financial future.

Remember, financial wellness is not a destination; it's an ongoing journey of mindful financial management.

Take the first step today and pave the way for a lifetime of financial stability and prosperity.