Your credit score is just one piece of the puzzle. I've been in the credit repair industry for over 15 years, and I've seen countless clients with good credit scores get denied for loans.

What Lenders Really Look at Beyond Your Credit Score

Lenders dig much deeper than your three-digit number. They analyze your entire financial picture. Understanding these hidden factors helps you prepare better applications and increase your approval chances.

Most consumers focus only on raising their credit score. They miss the other critical elements that determine approval or denial.

Your Debt-to-Income Ratio Matters More Than You Think

Debt-to-income ratio (DTI) is one of the most important factors lenders check. This measures how much of your monthly income goes toward debt payments.

Calculate your DTI by dividing your total monthly debt payments by your gross monthly income. Multiply by 100 to get a percentage.

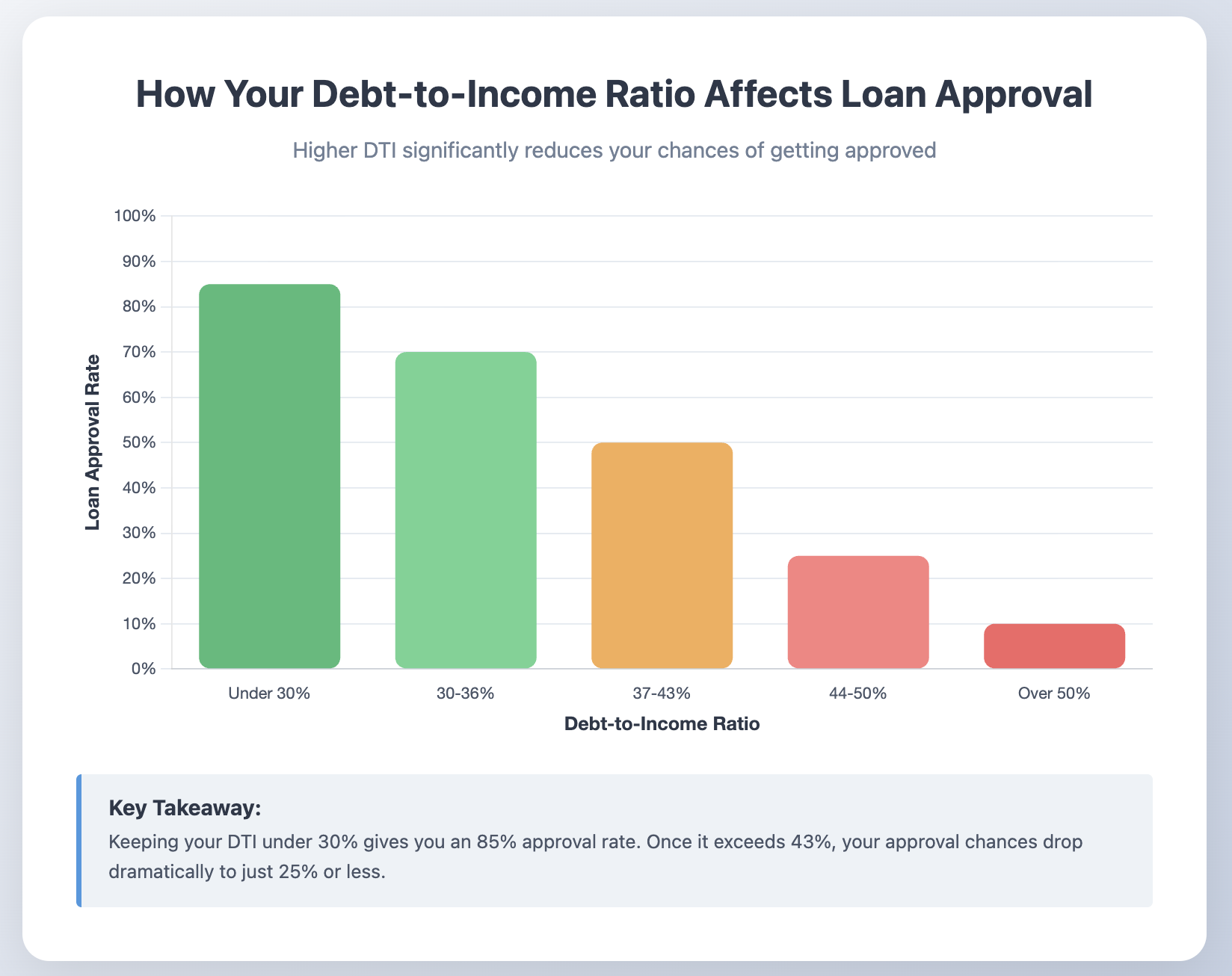

For example, if you earn $5,000 monthly and pay $1,500 in debts, your DTI is 30%.

Most lenders want to see a DTI below 43% for mortgage approval. Credit cards and personal loans have different thresholds. Some lenders prefer a DTI under 36%.

According to the Consumer Financial Protection Bureau, DTI is a strong predictor of loan default risk. Borrowers with high DTI struggle more to make payments when unexpected expenses arise.

I've seen clients with 750 credit scores get denied because their DTI exceeded 50%. Meanwhile, clients with 680 scores got approved with DTI under 30%.

Lower your DTI by paying down existing debts before applying for new credit. Increasing your income also helps, but that takes more time.

Here's a bar graph showing loan approval rates by DTI ranges:

Employment History and Income Stability

Lenders want to see stable employment. They check how long you've been at your current job and your employment history for the past two years.

Frequent job changes raise red flags. Lenders worry you might lose income and default on payments.

Most mortgage lenders require at least two years of employment history. They prefer you stay at the same company or in the same industry. Gaps in employment need explanation.

Your income type matters too. W-2 employees have an easier time than self-employed borrowers. Lenders view regular paychecks as more stable than business income.

Self-employed applicants need to provide two years of tax returns. Lenders average your income over those years. If your income dropped recently, you might qualify for less than expected.

I've helped many self-employed clients who were surprised their stated income didn't match what lenders approved. Tax deductions that lower taxable income also lower qualifying income for loans.

Seasonal workers face similar challenges. Lenders' average income over 12 months. This can significantly reduce your qualifying amount.

Before applying, gather at least two years of W-2s or tax returns. Prepare explanations for any employment gaps or income fluctuations.

Your Banking Behavior Gets Scrutinized

Lenders review your bank statements more carefully than most people realize. They look for patterns that indicate financial stress or irresponsible behavior.

Overdrafts are major red flags. Multiple overdrafts in recent months signal poor money management. Even one overdraft can raise questions during mortgage underwriting.

Non-sufficient funds (NSF) fees show you're living paycheck to paycheck. Lenders worry you can't handle additional monthly payments.

Large unexplained deposits trigger scrutiny. Lenders need to verify the source of any large deposits. They want to ensure you're not borrowing money to fake your down payment.

Gift funds for down payments require documentation. The gift giver must provide a letter stating the money is a gift, not a loan.

Consistent minimum balances matter. Lenders want to see you maintain steady account balances. Accounts that frequently drop to zero suggest financial instability.

I tell my clients to avoid making large deposits or withdrawals in the 60 days before applying for a mortgage. Every unusual transaction requires written explanation and documentation.

Keep your accounts stable. Avoid overdrafts. Build a cushion of at least two months' expenses in savings.

Payment History Beyond Your Credit Report

Your credit report shows payment history for credit accounts. But lenders dig deeper into other payment obligations.

- Rental payment history is increasingly important. Some lenders now check with landlords or property management companies. Late rent payments hurt your application even if they don't appear on credit reports.

- Utility payment history can be reviewed. While most utilities don't report to credit bureaus, lenders can request this information directly. Late utility payments suggest payment struggles.

- Cell phone bills may be checked. Many phone companies now report to credit bureaus, but some don't. Lenders might verify directly with providers.

- Child support and alimony payments must be current. Court-ordered payments take priority over other debts. Lenders check compliance carefully. Past-due support can disqualify you entirely.

According to Experian, alternative data like rent and utility payments can help thin-file consumers build credit. However, negative payment histories on these accounts hurt applications significantly.

I've seen mortgage applications denied because applicants had perfect credit reports but habitually paid rent 5 to 10 days late.

Pay everything on time, not just credit accounts. Lenders verify more than what appears on your credit report.

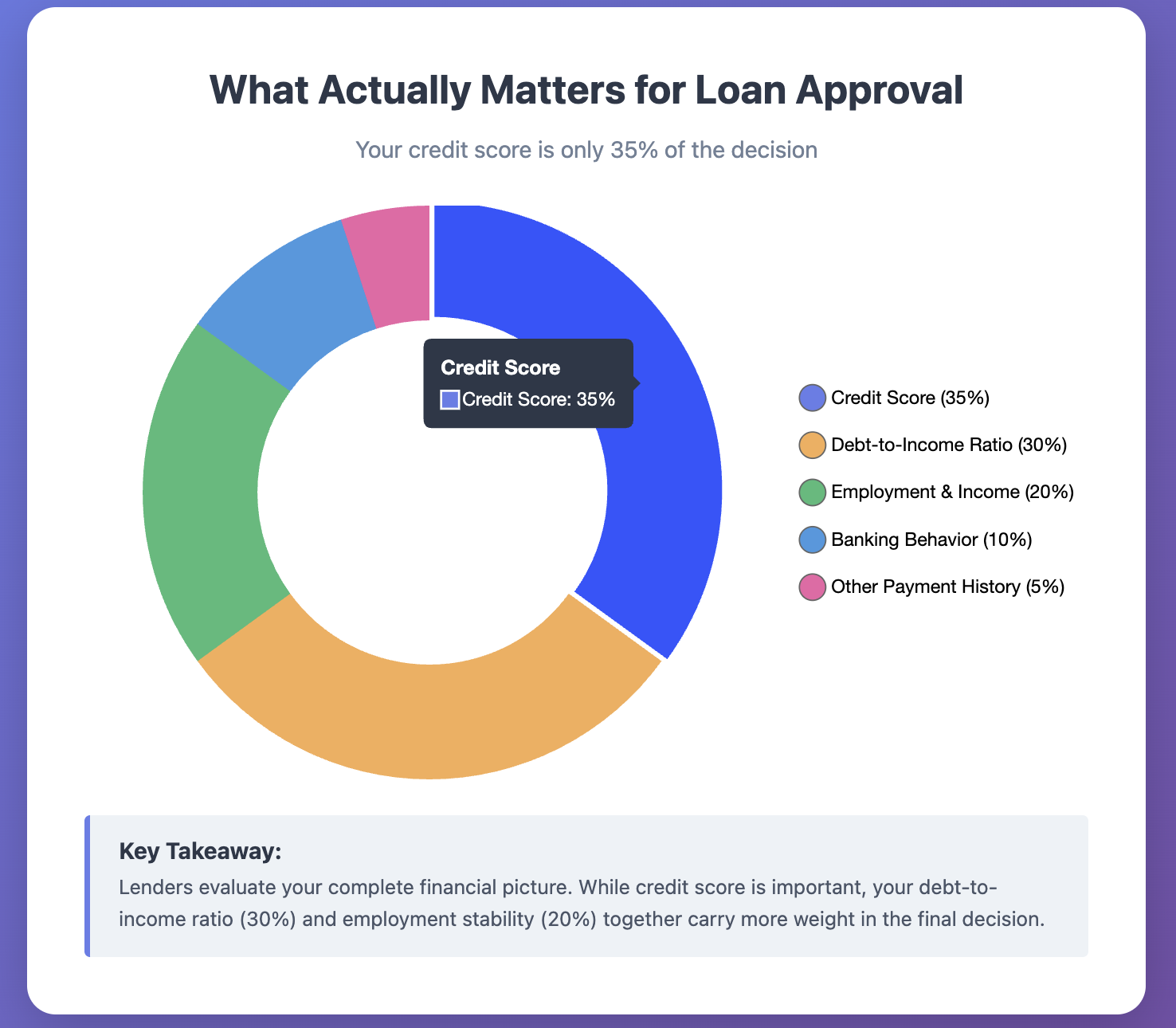

Belos is a Pie chart showing factors that impact loan approval:

Your Existing Relationship with the Lender

Banks favor existing customers. If you have accounts with a bank, you're more likely to get approved for their credit products.

This is called relationship banking. Lenders see your deposit account history, direct deposits, and overall account management.

Having checking and savings accounts with a bank gives them more confidence. They can see your cash flow patterns and financial stability.

Some banks offer relationship discounts on interest rates and fees. You might get 0.25% to 0.50% off your mortgage rate as an existing customer.

Credit unions especially value member relationships. They're more likely to work with members who have marginal credit if they've maintained good accounts.

I advise clients to open accounts with their target lender at least six months before applying for major loans. Build a relationship first.

Use the account actively. Set up direct deposit. Maintain good balances. Avoid overdrafts.

When application time comes, mention your existing relationship. It can tip decisions in your favor.

The Property or Collateral Value

For secured loans, the collateral value directly impacts approval and terms.

Loan-to-value ratio (LTV) measures the loan amount against the asset's value. Lower LTV means less risk for lenders.

Mortgage lenders typically cap LTV at 80% without private mortgage insurance. Higher LTV requires additional insurance, increasing your costs.

Auto lenders check vehicle value through guides like Kelley Blue Book. They won't lend more than the car is worth. Negative equity from a trade-in complicates approval.

Appraisal results can make or break mortgage applications. If the home appraises below the purchase price, you need a larger down payment or must renegotiate the price.

I've seen deals fall apart because appraisals came in 5% to 10% below contract price. Buyers couldn't bridge the gap.

The property condition matters too. Homes needing significant repairs may not qualify for conventional financing. You might need renovation loans with stricter requirements.

Choose properties wisely. Get pre-appraisals when possible. Understand that collateral value affects more than just your loan amount.

Recent Credit Applications and Hard Inquiries

Every credit application generates a hard inquiry. Too many inquiries in a short time hurt your application.

Lenders see multiple recent inquiries as desperate behavior. They worry you're taking on too much debt or getting rejected elsewhere.

Credit score formulas penalize excessive inquiries. FICO groups similar inquiries within 14 to 45 days as one inquiry for mortgages and auto loans. But credit card inquiries count individually.

Applying for five credit cards in two months tanks your score and raises red flags.

Lenders also check if recent applications resulted in new accounts. Opening several new accounts quickly suggests financial stress or overspending.

I tell clients to avoid all new credit applications for at least six months before applying for mortgages. Even one new inquiry during underwriting can delay or derail approval.

Space out credit applications. Only apply when you have strong approval chances. Avoid shopping around excessively.

Public Records and Legal Issues

Public records impact loan decisions even when they don't affect credit scores directly.

Bankruptcies require waiting periods. Chapter 7 bankruptcy requires two to four years before qualifying for conventional mortgages. FHA loans have shorter waiting periods.

Foreclosures create three to seven-year waiting periods, depending on loan type.

Tax liens must be resolved before approval. The IRS can seize property if you default, making lenders nervous. Most require payment plans or full resolution before lending.

Judgments need payment or explanation. Outstanding judgments often require payment at closing from loan proceeds.

Evictions show up in court records. While not on credit reports, landlord verification may reveal them. This damages rental and mortgage applications.

Divorce proceedings complicate applications. Lenders need final divorce decrees showing debt division and support obligations.

Many people don't realize these public records get checked separately from credit reports. Lenders search county court records during underwriting.

Resolve legal issues before applying. Get letters showing payment plans or settlements. Be upfront about anything in public records.

Your Social Media and Online Presence

Some lenders now check social media profiles. This practice is controversial but growing.

Lenders look for lifestyle inconsistencies. If you claim low income but post pictures of expensive vacations and luxury purchases, they question your application honesty.

Employment verification can happen through LinkedIn. Lenders check if your stated employer matches your profile.

Business owners get extra scrutiny. Lenders check business social pages to verify the company exists and appears active.

I don't recommend this practice, but I tell clients to be aware. Review your public profiles before applying for major loans.

Set profiles to private when possible. Remove posts showing excessive spending or financial irresponsibility.

Don't lie on applications. Social media can expose inconsistencies that lead to immediate denial or even fraud charges.

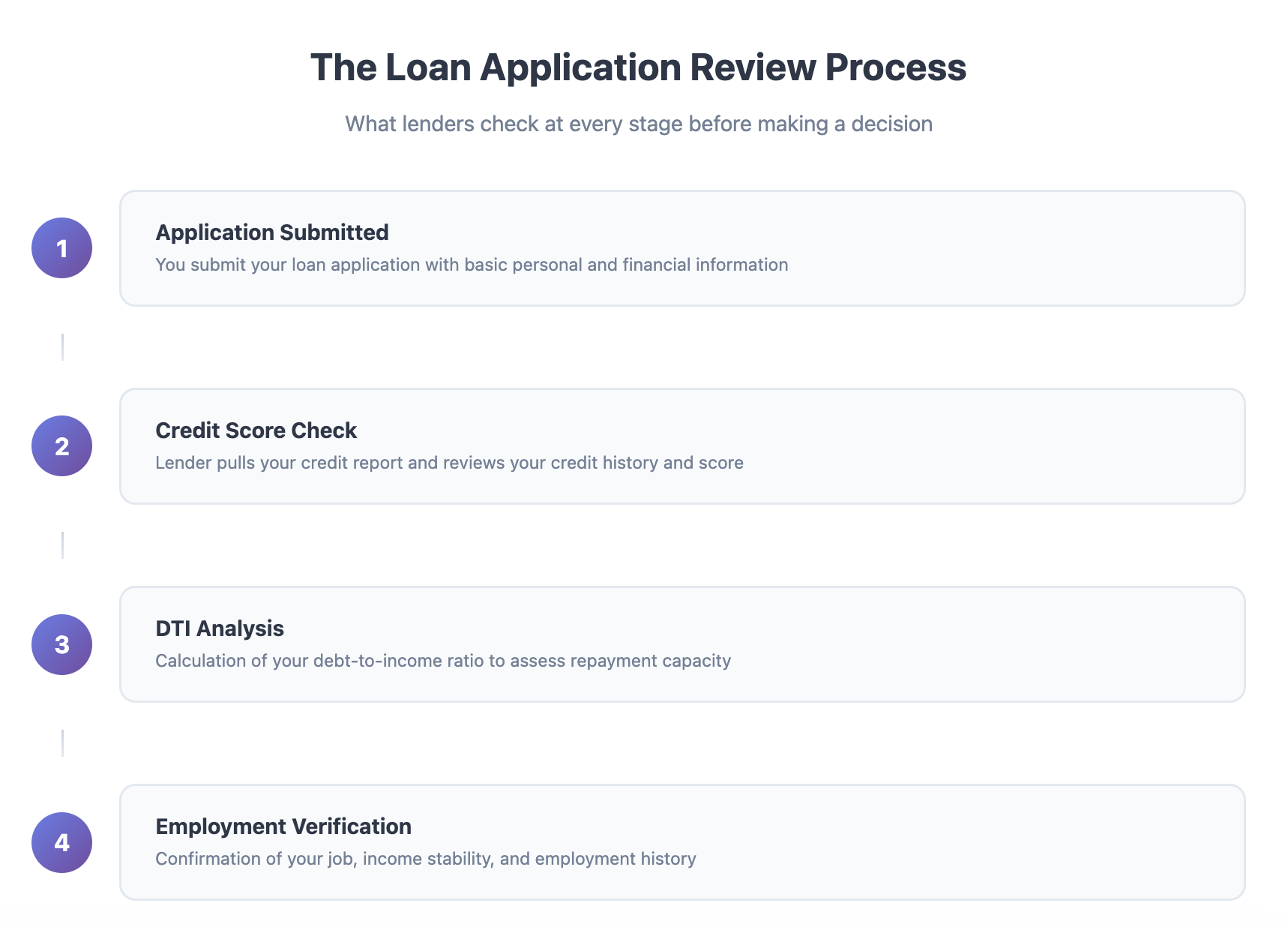

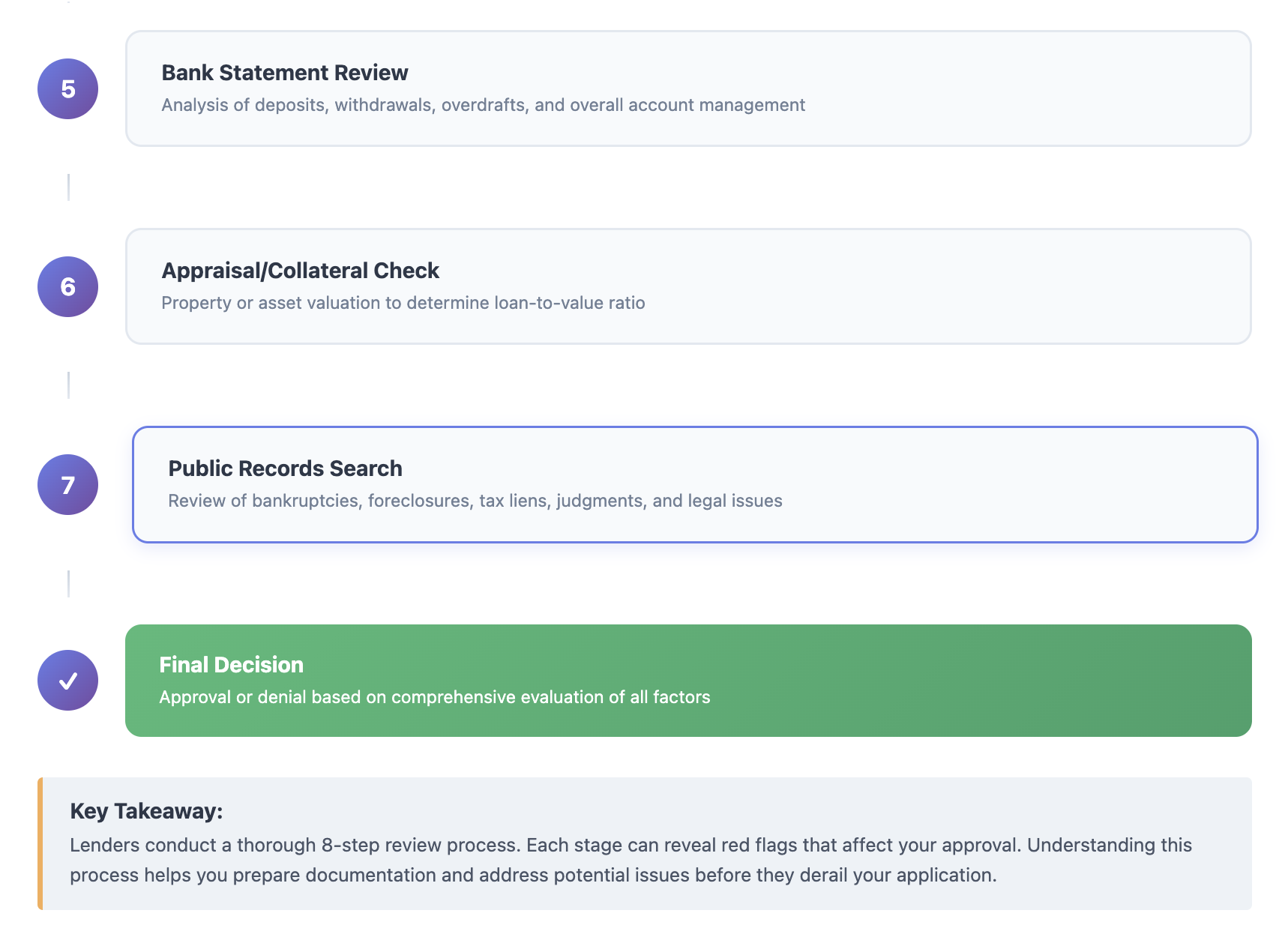

Here's a sample flowchart showing the loan application review process:

Geographic Location and Local Economic Factors

Where you live affects loan approval and terms.

Lenders consider local unemployment rates. High-unemployment areas face stricter scrutiny. Lenders worry about job loss risk.

Property values in your area matter. Declining markets make lenders nervous. They might require larger down payments or charge higher rates.

Some neighborhoods face lending discrimination through redlining. While illegal, it still happens. Certain areas get denied more often or receive worse terms.

Rural properties face stricter appraisal requirements. Lenders need comparable sales, which can be scarce in rural areas.

Condos in buildings with high investor ownership may not qualify for conventional financing. Lenders want owner-occupied buildings.

I've seen identical applicants get different terms based solely on property location. The same buyer qualified for better rates in one neighborhood versus another.

Research your area's lending environment. If you're in a challenging market, prepare for extra documentation or requirements.

The Type of Loan You're Seeking

Different loan types have different requirements beyond credit scores.

- Conventional mortgages are the strictest. They require strong credit, low DTI, stable employment, and solid down payments.

- FHA loans are more forgiving. They accept lower credit scores and higher DTI. But they require mortgage insurance for the life of the loan in many cases.

- VA loans offer zero down payment for veterans. Credit requirements are flexible, but income and residency requirements apply.

- USDA loans help rural homebuyers. Income limits apply based on area median income. Properties must be in eligible rural zones.

- Jumbo loans exceed conventional loan limits. They require excellent credit, low DTI, significant reserves, and large down payments.

- Personal loans are unsecured. Lenders focus heavily on credit score, income, and DTI since there's no collateral.

- Auto loans are secured by the vehicle. The car's value and your ability to repay both matter.

Choose the right loan type for your situation. Don't apply for conventional loans if FHA better matches your profile. You'll waste time and harm your credit with unnecessary inquiries.

Final Thoughts From a Credit Repair Professional

Your credit score opens doors, but it doesn't guarantee approval. Lenders evaluate your entire financial life.

In my over 15 years of helping consumers, I've learned that preparation makes the difference. Clients who understand these hidden factors get approved more often and receive better terms.

Start preparing months before you need financing. Build employment stability. Lower your DTI. Clean up your bank accounts. Resolve public records issues.

Don't just focus on credit score improvement. That's important, but incomplete. Address all the factors lenders check.

If you're denied, ask why. Lenders must provide specific reasons. Understanding the denial helps you fix problems before reapplying.

Work with professionals when needed. Mortgage brokers, credit counselors, and credit repair specialists can guide you through complex situations.

Remember that lenders want to approve loans. They make money when they lend. But they need to minimize risk. Show them you're a safe bet across all factors, not just credit score.

Document everything. Keep organized files of pay stubs, tax returns, bank statements, and explanations for anything unusual. Preparation prevents delays and increases approval odds.

Be honest on applications. Lies get discovered during verification. Fraud charges can result from intentional misrepresentation.

Your financial health is multifaceted. Treat it that way. Address weaknesses before they derail your loan applications.