A frozen bank account can happen even if you were never personally served, depending on how the creditor obtained a court judgment and how the bank processes legal orders.

In one case I reviewed, a client found their account frozen after a judgment had already been entered. They were unaware of the lawsuit because the service was sent to an old address. Once the creditor secured the judgment, they were able to request a bank levy, which led to the account freeze without any direct warning from the bank. Situations like this are not uncommon when service procedures are completed but not actually received.

When a creditor wins a lawsuit, they can use enforcement actions such as a bank levy, which allows funds to be frozen or seized. Banks are required to comply with these legal orders once issued. Laws such as the Fair Debt Collection Practices Act regulate collection behavior, but enforcement of a valid judgment follows court procedures rather than notification preferences. Learn more.

Frozen Bank Account · Bank Account Frozen · Default Judgment · Creditor Levy · Bank Account Frozen Due to Suspicious Activity · How to Unfreeze Account

Updated April 2026 · Sources: Nolo.com frozen bank accounts guide, Texas Law Help bank freeze article (Nov. 2025), FDCPA 15 U.S.C. § 1692g, myFICO Forums judgment and garnishment threads, NerdWallet default judgment guide, Consumer Financial Protection Bureau debt collection data

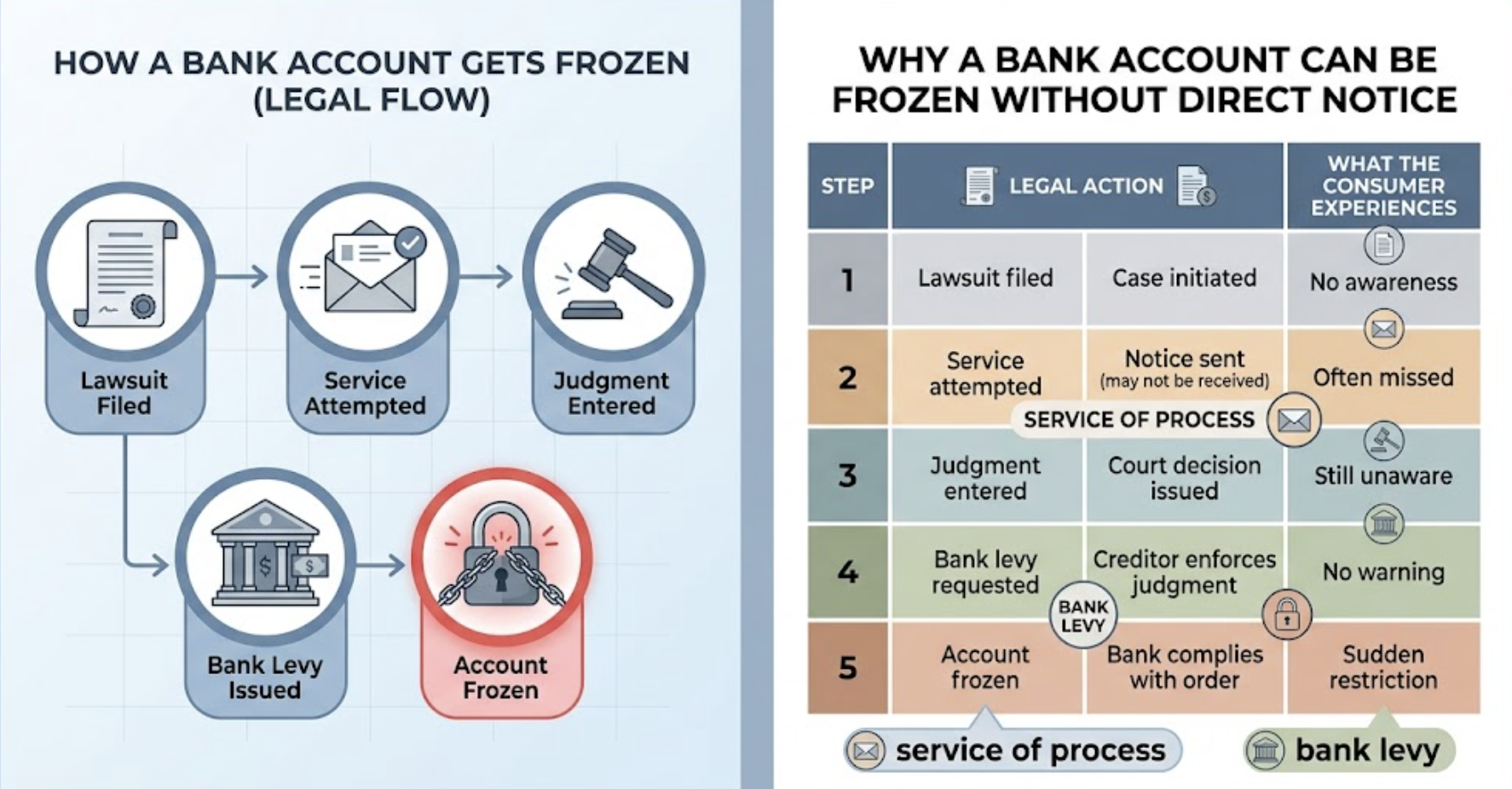

Most people discover their account is frozen at the worst possible moment: a declined card at a grocery store, a bounced automatic payment, or a zero balance when they know money was deposited. Nobody called. Nobody wrote. The debit card just stopped working.

This is not an accident. Banks are legally required to execute a freeze order the moment they receive it, before contacting you. The sequence is intentional. Understanding how the sequence works is the first step to knowing whether you have grounds to fight it.

Why Would a Bank Account Be Frozen?

The cause determines your rights and your timeline. If the freeze comes from a creditor levy, your path runs through the courts. If it comes from a bank fraud investigation, your path runs through your bank's compliance department. If it comes from the IRS or a state tax authority, those agencies have their own administrative processes. The chart below shows which causes are most common and which require a court judgment first.

The fourth category on the chart, default judgments entered without actual service, is smaller in absolute frequency but the most damaging in terms of consumer outcomes. When a collector files suit at an old address and gets a default judgment, the account holder typically learns about it only when the freeze hits. At that point, the legal window to challenge the judgment is already running. That window is one year in most states, and it starts from the date the judgment was entered, not the date you discovered the freeze.

Bank Account Frozen Due to Suspicious Activity: What This Means

Banks are required by federal law to monitor accounts for activity that could indicate fraud, money laundering, or terrorist financing. The triggers include: large cash deposits or withdrawals inconsistent with your account history, sudden international wire transfers, a pattern of structured deposits just below $10,000 (which banks flag as potential structuring), and transactions from accounts flagged as high-risk. As explained in Nolo's frozen bank account guide, the bank has no obligation to warn you before initiating a freeze for suspected illegal activity.

The most important distinction: if your account is frozen for suspicious activity, no creditor is involved and no judgment exists. The bank is not taking money from you. It is restricting your access temporarily while it reviews the account. Contact your bank directly, ask what specific activity triggered the review, and provide whatever documentation they request. An invoice for a large payment, an explanation of an unusual transfer, or identity verification documents are the most common resolution tools.

That scenario is common. The FTC and CFPB have both documented the practice known as "sewer service," where process servers file affidavits claiming they served the defendant when they did not. The summons gets mailed to an old address or simply never delivered, a default judgment enters, and the first the account holder knows about it is either a frozen account or a negative mark on their credit report.

Is It Legal for a Creditor to Freeze a Bank Account Without Serving You?

This is the distinction most people miss. No law says the creditor must call you before instructing the bank to freeze your account. What the law does require is that the creditor notified you of the lawsuit and that you had a chance to appear in court. If you never received the lawsuit, you never had that chance. The default judgment was entered without a valid opportunity to contest. Under the FDCPA and most state rules of civil procedure, that is grounds to vacate.

The myFICO community has multiple documented cases of this pattern. One member described finding a judgment from a New Jersey law firm on their credit report: "Not only did they neglect to notify me that they were suing me for this debt, but they also never even sent me a dunning letter. I literally never had any contact whatsoever from the law firm until they sent me the judgment notice. They sent it to my ex-wife. I haven't lived at that address since 2008. This all seems very illegal." The community response was consistent: "File a Motion to Vacate for improper service. Let your attorney deal with them directly."

For Houston and Phoenix residents: debt collection law firms file a significant number of default judgment cases in Texas and Arizona. Firms like Gurstel Law Firm operate in multiple states and pursue bank levies after obtaining judgments that were often entered by default. Knowing the firm behind the judgment is the first step in understanding your options, since different firms respond differently to settlement offers and Motion to Vacate filings.

How Do You Know If Your Bank Account Is Frozen?

The sequence is: court issues writ of garnishment, writ is served on your bank, bank freezes the account, bank sends you written notice of the freeze, you receive the notice in the mail while the funds are already locked. In some cases, the bank holds funds up to double the judgment amount as a precaution. If your account shows a balance of $2,000 and the judgment is for $1,200, the bank may place a hold on $2,400 as a precautionary reserve.

Once you confirm the account is frozen from a creditor levy, stop direct deposits into that account immediately. New deposits made after the freeze order may also be seized before you can access them. Contact your employer or any recurring income sources and redirect deposits to a new account at a different bank, one you have no existing loan or credit relationship with.

That experience captures what the data shows: people who do not know their rights pay immediately under financial pressure, often without realizing the judgment itself may be challengeable. Paying under duress does not waive your right to challenge the judgment's validity if it was entered on improper service, but it does make the vacate motion more complex and may reduce how much you can recover.

How Can You Unfreeze a Bank Account?

- Call your bank and identify the specific cause of the freeze. Ask whether it is a court-ordered garnishment or an internal bank hold. If it is a garnishment, ask for the name and contact information of the judgment creditor's attorney. If it is a bank hold for suspicious activity, ask what specific transactions triggered the review and what documentation they need.

- Search your county's online court records for your name. Most county courts have case search portals at no cost. Search your full name and any prior names or addresses. If a judgment appears, note the case number, filing date, and the law firm that filed. This is the judgment you need to respond to.

- File a Claim of Exemption within 10 days if exempt funds are in the account. Social Security, SSDI, SSI, VA benefits, and federal pension payments are protected from private creditor levies under federal law. Texas also protects wages under Texas Property Code Section 42.001. File the form immediately. Missing this window means those funds may be permanently released to the creditor.

- File a Motion to Vacate the default judgment if you were never served. You generally have one year from the judgment entry date to file this motion based on excusable neglect. If you can prove you were never served (improper service or sewer service), courts often extend that window. Include a meritorious defense in the motion: a reason you would have contested the debt if you had known about the lawsuit. This could be a statute of limitations defense, a dispute of the amount, or a challenge to the collector's standing to sue.

- Open a new account at a different bank for all future deposits. Any bank where you also have a loan can use the "right of setoff" to apply funds in your account toward your loan balance without a court order. Use a bank you have no credit relationship with for any new deposits while the levy is active.

For residents in Arizona and Texas, where wage garnishment for consumer debt is restricted or prohibited, the bank account levy is often the creditor's only enforcement tool. This makes the 10-day exemption window even more critical for Texas residents, since the creditor cannot reach wages directly. The full breakdown of what assets can be taken after a debt lawsuit covers the state-specific exemptions that apply in Texas and Arizona and how to claim each one within the required timeframe.

How Long Can a Bank Freeze an Account?

For creditor levies specifically, the account often stays frozen for several weeks while the legal process unfolds. During that period, the bank holds the funds, the creditor files the paperwork to have the funds formally transferred, and the account holder has the opportunity to file exemption claims or challenge the underlying judgment. Texas Law Help's bank freeze guide notes that the garnishment process "can last several months" because the bank must respond to the court, confirm the accounts belong to the debtor, and then turn over nonexempt funds through a separate court proceeding.

For fraud investigation freezes, the 2025 federal case Mohamed v. Bank of America confirmed that a 29-day freeze was within the contractual timeframe for an investigation. If the bank's investigation finds no wrongdoing, the freeze is lifted. If it finds evidence of fraud or illegal activity, the account may be closed permanently and any remaining funds seized.

Can Your Bank Account Stay Frozen Indefinitely?

In practice, yes. A freeze from a creditor levy has no expiration date. As long as the judgment is valid and the debt is unpaid, the levy remains enforceable. In Texas, a judgment is valid for 10 years and renewable. That means a freeze could theoretically be reinstated at any point within the judgment's life, any time you have nonexempt funds in an account the creditor has located. The only way to permanently end the risk is to pay the debt, negotiate a settlement, or successfully vacate the judgment.

For Phoenix residents dealing with collection firms and potential wage garnishment orders alongside bank levies, the specifics of Arizona's garnishment rules matter. Our article on wage garnishment in Phoenix covers how Arizona's garnishment limits interact with bank levies, what the exempt amount thresholds are, and how to respond to both simultaneously if a creditor pursues multiple enforcement methods at once.

Can a Creditor Freeze Your Bank Account Multiple Times?

This is why vacating the judgment is the most effective long-term resolution when the freeze resulted from a default entered without proper service. Paying the debt satisfies the judgment but does not remove it from court records immediately, and it does not protect against future levies on the interest and fees that may still be owed. Vacating the judgment if it was improperly obtained is cleaner and produces no payment.

The myFICO community consistently makes the same point: the default judgment is not permanent if you were not properly served. The legal term is "vacating" the judgment, and the process returns the case to its pre-judgment state so you can actually contest the debt. After vacating, the creditor has to prove in court that the debt is valid, that the amount is correct, and that they have the legal standing to collect it. Many debt buyers, who purchase old debts for pennies on the dollar, cannot produce this documentation and the case gets dismissed.

Understanding the statute of limitations on the original debt is critical here. If the debt is time-barred in your state, that is a complete defense. The date the limitations clock started, and whether any action by you restarted it, is a key factual question. Our article on how debt statute of limitations gets restarted covers exactly which actions reset the clock and which ones do not, since making a partial payment or acknowledging the debt in writing can extend the collector's ability to sue by years.

A Frozen Account Often Starts With an Error on Your Credit Report

Judgments that appear on your credit report can trigger collectors to locate your bank and enforce a levy. A free 3-bureau audit shows every judgment entry, collection account, and reporting inaccuracy across Experian, TransUnion, and Equifax. Items that are disputable under the FCRA or unverifiable under the FDCPA may be removable before they lead to enforcement action.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions: Frozen Bank Account

Can a creditor freeze your bank account?

Yes, but only after winning a court judgment. A private creditor cannot freeze your bank account just because you owe money. They must file a lawsuit, obtain a judgment, and then get the court to issue a separate writ of garnishment directed at your bank. The government is the exception: the IRS, state tax agencies, student loan servicers, and child support enforcement agencies can levy your account without a court judgment, though they must give you notice of their intent to levy before doing so.

How can you unfreeze a bank account?

The method depends on the cause. For a creditor levy: file a Claim of Exemption within 10 days to protect exempt funds like Social Security and VA benefits, then challenge the underlying judgment if you were never properly served. For a bank suspicious activity freeze: contact your bank, explain the flagged transactions, and provide documentation. For a government levy: contact the agency directly and establish a payment plan. The fastest path when you were never served is an emergency Motion to Vacate the default judgment filed in the originating court.

How long can a bank freeze an account?

There is no legal maximum for most types of freezes. A creditor levy stays active until the debt is paid, an exemption is granted, or the judgment is vacated. Bank fraud investigation freezes typically resolve in 7 to 21 business days. Government levies continue until the underlying debt is resolved. Court-ordered freezes tied to criminal investigations or civil litigation have no fixed end date and can last months or years.

How long can a bank freeze your account for an investigation?

Federal law does not specify a maximum duration for a bank's fraud investigation freeze. A 2025 federal court case confirmed that a 29-day freeze was within the reasonable contractual timeframe. For routine fraud flags or identity verification issues, most banks resolve the hold in 7 to 10 business days once you provide documentation. If the bank reports the account to law enforcement, the freeze can extend indefinitely while the investigation is active.

Why would a bank account be frozen?

The three main causes are: a creditor levy following a court judgment, a bank-initiated hold for suspicious activity such as fraud or money laundering patterns, or a government agency action for unpaid taxes, student loans, or child support. Each cause requires a different response. Creditor levies involve the courts. Bank holds involve your bank's compliance team. Government actions involve the specific agency.

Can I withdraw money from a frozen bank account?

No. A frozen account blocks all outgoing transactions: withdrawals, debit card purchases, ACH payments, and transfers. You can typically still receive deposits into the account, but those deposits may also be seized if the creditor's levy is active. Do not deposit additional funds into a frozen account. Redirect all income to a new account at a different bank while you resolve the freeze. The exempt funds you already have in the account may be recoverable through a Claim of Exemption filed within 10 days.

-

What Is Credit Gardening? How to Grow Your Score the Smart Way Once the freeze is resolved and the judgment is addressed, credit gardening is the method for rebuilding your score by letting existing accounts age and accumulate positive history without new hard inquiries or new accounts.

-

Can a Company Send You to Collections Without Notice? Covers the legal distinction between original creditors and debt collectors on notice requirements, the FDCPA validation notice window, and what to do when a collection appears on your report from a creditor you never heard from.

-

How to Avoid Restarting the Debt Statute of Limitations Paying even one dollar on a time-barred debt can restart the statute of limitations in some states, giving collectors fresh legal standing to sue. This covers which actions reset the clock, which do not, and how to negotiate without giving collectors that advantage.

Takeaway From Frozen Bank Accounts

A frozen bank account without personal service can occur if a judgment was entered through legally accepted service methods. However, you may still have the right to challenge the judgment, claim exemptions, or dispute improper service depending on your jurisdiction and case details.