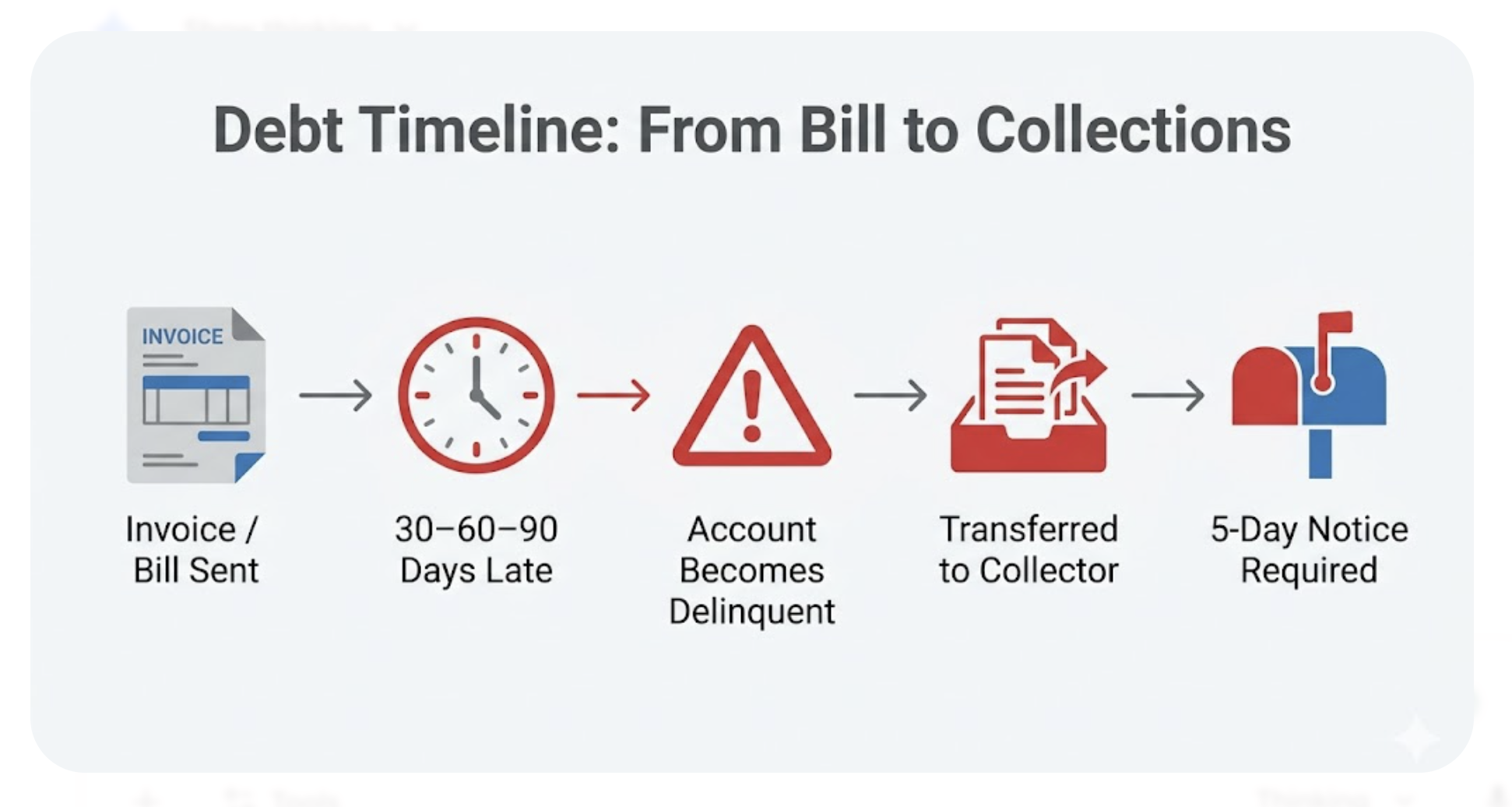

In some cases, a company can send a debt to collections without prior notice, depending on the billing process and creditor policies, but debt collectors must follow specific legal requirements once they begin collection activity.

In one case I handled, a client discovered a collections account on their credit report without receiving any prior communication from the original creditor. The account had already been transferred to a third-party collector, which triggered a drop in their credit score. Situations like this occur when billing notices are missed, sent to outdated addresses, or not acknowledged, but the transfer itself is not always a violation.

Under the Fair Debt Collection Practices Act, once a debt collector contacts you, they are required to send a written validation notice within five days. This notice must include the amount owed, the creditor’s name, and your right to dispute the debt. The law regulates how debts are collected, not whether a creditor must notify you before sending the account to collections.

Debt Collections · FDCPA Rights · Credit Report Disputes · Consumer Law · Debt Validation

Updated April 2026 · Sources: CFPB Consumer Response Annual Reports 2019-2024, FTC Fair Debt Collection Practices Act text, 15 U.S.C. § 1692g, Upsolve FDCPA analysis, myFICO Forums debt collection threads

The question comes up every day. Someone checks their credit report, finds a collection they never knew about, and asks: how is this legal? The short answer is that two different laws apply here, and they cover two different parties. The original creditor operates under one set of rules. The debt collector operates under another. The gap between those two sets of rules is where most people get blindsided.

In 2024, the CFPB received 207,800 debt collection complaints — nearly double the 109,900 received in 2023. The single most common complaint, year after year since 2013, is attempts to collect a debt the consumer never owed. Second on that list is collectors failing to provide proper notice. These are not rare edge cases. They happen at scale.

Can a Company Send You to Collections Without Notice?

This distinction matters. The original creditor — the credit card company, the hospital, the landlord, the utility — is governed by the Fair Credit Reporting Act when it comes to credit reporting. The FCRA gives financial institutions up to 30 days after reporting negative information to notify you. By then, the damage to your credit is already done.

The debt collector is governed by the FDCPA. Under that law, as the FTC's full FDCPA text confirms, the validation notice requirement under Section 1692g(a) is triggered by the collector's first communication with you. That communication can be a phone call, a letter, or — according to both FTC advisory opinions and established federal case law — a report to a credit bureau. Reporting your collection account to Experian, TransUnion, or Equifax counts as an initial communication for purposes of the five-day clock.

The myFICO community response to that post was direct: "Unfortunately, a creditor doesn't have to notify you prior to sending a debt to collections. However, the collection agency is required by law to validate the debt and notify you in writing of the debt within 30 days of contacting you." That is the legal reality. The original creditor can act without warning. The collector cannot collect without notifying you first.

What Are Your Legal Rights Under the FDCPA?

The validation notice is your most important tool. It starts a 30-day window that is only open once. If you let it close without disputing, the collector assumes the debt is valid. That assumption does not mean you owe the debt — courts have been clear that silence is not an admission of liability under Section 1692g(c). But it does mean you lose the leverage that comes from forcing the collector to verify the debt before continuing collection activity.

In practice, many collectors exploit the confusion around this window. A 2023 analysis of FDCPA complaints found that 25% of consumers who filed complaints said they never received information about their right to dispute the debt, and 75% said the validation notice they received was vague and did not include enough detail to verify the debt. Collectors who send vague notices are not necessarily violating the law, but they are using the letter of the law while ignoring its intent.

The CFPB's debt collection FAQ is clear on this: a collector "has to give you validation information about the debt either when they first communicate with you or within five days of the first contact." If you never received that notice — not because you moved without a forwarding address, but because the collector never sent it — that is a violation.

How Often Does This Happen? CFPB Complaint Data

The 2024 spike to 207,800 complaints is not random. 45% of those complaints cited debts consumers said they did not owe. These include debts from identity theft, debts that were already paid, and debts mistakenly attributed to the wrong person. Collectors reported to bureaus and began collection on accounts where they had insufficient documentation to prove the debt was valid. The CFPB noted in its 2024 FDCPA report that several examined entities — particularly student loan debt collectors — failed to provide validation notices as required when the initial communication with consumers occurred in writing.

What does this mean for you? If a collection shows up on your report, there is a non-trivial chance it was reported without full documentation in place. That is why the debt validation process exists — and why using it immediately is the correct first move.

Do Debt Collectors Have to Notify You Before Reporting to the Credit Bureaus?

This is where many people have a legitimate claim and do not know it. The sequence usually goes like this: you check your credit report, find a collection from a company you have never heard of, call the collector, and they say they sent a letter to your old address. What they often do not tell you is that the five-day clock started when they reported to the bureau — not when the letter was sent. If a letter was sent to an address they knew was outdated, and reporting to the bureau constituted the initial communication, the notice requirement was triggered before they mailed anything.

The community response in that thread was from someone who clearly understood the law: "The requirement for debt collector notification of their collection activity is FDCPA 809(a), and is within 5 days of any initial communication with the consumer. The FTC and courts have interpreted reporting to a credit reporting agency as triggering the requirement for a dunning notice within 5 days after that reporting. So you most likely have a violation of FDCPA 809(a) on their part."

The follow-up matters: a violation of the notice requirement does not automatically delete the collection from your report. But it gives you leverage. You can file a complaint with the CFPB, dispute under the FCRA, and potentially negotiate removal as part of a settlement. You may also have standing to sue in federal court.

What Should You Do If You Were Sent to Collections Without Notice?

The most common mistake people make in this situation is calling the collector and trying to negotiate without first understanding what the debt is. Once you acknowledge the debt verbally, you give the collector information. Once you make a partial payment, you may restart the statute of limitations for them to sue you in some states. The correct sequence is to get the facts first and act second.

Here is the order that produces the best results:

- Pull all three credit reports at AnnualCreditReport.com. Note the collector's name, the original creditor, the amount, and the date of first delinquency. The date of first delinquency determines when the seven-year reporting clock started, not the date the debt was sold to the collector.

- Send a debt validation letter via certified mail within 30 days of any contact. If you received a notice from the collector, the clock is running. If the collection appeared on your report and you received nothing, send the letter anyway. Under FDCPA Section 1692g, your written dispute must be responded to before the collector can continue collecting. State clearly that you dispute the debt and request verification of the amount, the original creditor's name, and proof of their authority to collect.

- Dispute with each bureau that shows the collection. Under the Fair Credit Reporting Act, you can dispute any entry you believe is inaccurate or unverifiable. State in the dispute that you were never provided a validation notice as required under the FDCPA. The bureau must investigate within 30 days. If the collector cannot verify within that window, the bureau must remove the entry.

- File a complaint with the CFPB at consumerfinance.gov/complaint. Include the collector's name, dates, and a description of the violation. This creates an official record and puts the company on notice that their handling of your account is under regulatory review.

- Consult a consumer attorney if violations are clear. Under 15 U.S.C. § 1692k, you can recover up to $1,000 in statutory damages plus attorney fees for FDCPA violations. Many consumer attorneys take these cases on contingency, meaning you pay nothing unless they recover damages. The threat of a lawsuit is also effective leverage for negotiating removal of a collection entry.

If the collection is valid and you owe the debt, the next question is whether to pay or dispute. The impact on your credit depends on whether the collection is paid or unpaid, and the full analysis of removing paid vs unpaid collections from your report covers how each scenario affects your score and which removal strategies are available in each case.

Can You Go to Jail for Not Paying a Collection?

The arrest threat is one of the most common FDCPA violations, and it works because most people do not know the law. Debt is not a crime. The court system for unpaid consumer debt is the civil court, not the criminal court. The collection agency cannot call the police. The original creditor cannot have you arrested. A civil judgment against you has real consequences — wage garnishment, liens on property, bank levies — but none of those consequences include incarceration.

The detailed breakdown of what collectors can and cannot legally do after a judgment is covered in our article on whether you can go to jail for not paying collections, including the distinction between civil and criminal debt, what happens if a collector misrepresents your legal risk, and the steps to take when you receive a lawsuit summons.

How Does a Collection Account Affect Your Credit Score?

The score impact is front-loaded. A new collection on a 700-range credit score can drop it into the 600s within one reporting cycle. An old collection from four or five years ago has already done most of its damage, and paying it may not move the score much under older scoring models. This is why timing matters. A collection that appeared last month is a different problem than one that has been on your report for six years.

FICO Score 9 treats paid collections the same as no collection. VantageScore 4.0 ignores all medical collections. These newer models are not yet used by most mortgage lenders, who still rely on FICO 2, 4, and 5. But the gap between old and new scoring models explains why the same collection can have different impacts depending on what a lender pulls. The full breakdown of rebuilding your credit after collections covers which actions move the needle on which scoring models, and the fastest path back to a bankable score after collection damage.

That thread captures a real distinction that matters in credit repair: verification and validation are not the same thing. When you dispute through the bureaus, the bureau contacts the collector and asks if the debt is accurate. The collector responds yes. That is verification — a confirmation that the data matches their records. Validation is different: it is the documentary proof that the debt is yours, the amount is correct, and the collector has the right to collect. Collectors can pass verification without providing actual validation, which is why FDCPA-level debt validation letters sent directly to the collector carry more weight than bureau disputes alone.

A Collection You Never Knew About May Be Removable

If a collection appeared on your report and you were never properly notified, you may have grounds for removal under the FDCPA or FCRA. A free 3-bureau audit shows every collection entry across Experian, TransUnion, and Equifax, identifies which ones are disputable, and outlines the correct step sequence for each.

Get My Free Credit Audit → Secure · 2 minutes · No credit card requiredFrequently Asked Questions

Can a company send you to collections without notice?

Yes. Original creditors are not required to notify you before transferring or selling your account to a debt collection agency. The FDCPA's notice requirements apply to third-party collectors, not to the original creditor. Once the account is in a collector's hands, they must send you a written validation notice within five days of their first communication, which includes reporting the debt to a credit bureau.

Do debt collectors have to notify you before reporting to credit bureaus?

No prior notification is required, but reporting to a credit bureau counts as an initial communication under FDCPA Section 809(a) according to both FTC advisory opinions and federal court case law. This means the five-day clock to send a validation notice starts the moment they report to Experian, TransUnion, or Equifax. If they reported and never sent a validation notice, that is a violation of the FDCPA.

What is a debt validation notice and when must I receive it?

A validation notice is a written disclosure required under FDCPA Section 1692g. It must be sent during or within five days of a collector's first communication with you. It must include the amount of the debt, the creditor's name, a statement that you have 30 days to dispute, and information about how to request the original creditor's information. If you do not dispute in writing within 30 days, the collector may assume the debt is valid.

What can I do if I was sent to collections without notice?

Send a debt validation letter to the collector via certified mail within 30 days of any contact. Dispute with each credit bureau showing the collection under the FCRA. File a complaint with the CFPB at consumerfinance.gov/complaint. If the collector failed to send a validation notice or continued collecting after your written dispute, consult a consumer attorney. Under 15 U.S.C. § 1692k, you may be entitled to up to $1,000 in statutory damages plus attorney fees for FDCPA violations.

How long does a collection stay on your credit report?

Seven years from the date of first delinquency. The date the debt was transferred to a collector does not reset the clock. Paying the collection does not remove it — it updates the status from unpaid to paid. The entry stays on your report for the full seven-year period unless it is successfully disputed and removed under the FCRA or FDCPA.

Can I go to jail for not paying a collection?

No. Consumer debt is a civil matter, not a criminal one. You cannot be arrested for unpaid credit card debt, medical bills, or utility balances. A collector who threatens arrest is violating FDCPA Section 1692e. What creditors can do through civil court — after obtaining a judgment — includes wage garnishment and bank levies, but not incarceration.

-

Is 686 a Good Credit Score? What You Can Actually Get Approved For If a collection dropped your score into the 680 range, this explains what lenders actually approve at that level, what rates you pay versus someone at 720, and the fastest path to the next score tier.

-

Credit Corp Solutions: Scam or Legit? A full breakdown of one of the most commonly questioned debt buyers — what they buy, how they collect, what their validation letters typically look like, and how to respond if they appear on your credit report.

-

How to Settle Midland Credit Without Resetting the Clock Midland Credit Management is one of the country's largest debt buyers. This covers the specific settlement strategy that avoids restarting the statute of limitations or creating a new derogatory event on your report.

Closing

A company can send a debt to collections without prior notice, but debt collectors must follow validation and disclosure requirements once collection begins. Understanding the difference between creditor actions and collector obligations helps you respond correctly, protect your rights, and prevent further credit damage.