When it comes to removing collections from your credit report, unpaid collections are often easier to remove than paid ones, because once a collection is paid, the account is usually marked as verified and closed, making it harder to challenge. Paying a collection does not automatically remove it, and in many cases, it actually reduces your leverage in the dispute process.

Hey there, my name is Joe Mahlow with ASAP Credit Repair. I work directly with consumers every day who are dealing with collection accounts, and I’ve seen firsthand how paid and unpaid collections are handled differently by credit bureaus and collection agencies. Understanding how these accounts are reported, and why some stick while others don’t, is critical if you want real results.

If you’ve got collections sitting on your credit report and you’re stressing about whether to pay them, settle them, or leave them alone, you’re not alone. That confusion is common, and making the wrong move can cost you money without improving your credit.

Stick with me, because breaking down the truth about paid versus unpaid collections can save you a lot of frustration, and help you choose the option that actually works.

Understanding What Happens When You Pay a Collection

Here's the thing most people don't understand about collections and credit reporting. When you have an unpaid collection on your credit report, it shows up as a negative item that's hurting your credit score. And a lot of people think, "Okay, if I just pay this thing off, it'll go away and my credit will get better." But that's not how it works.

When you pay a collection account, the status changes from "unpaid" to "paid," but the collection itself stays on your credit report. It doesn't disappear. It doesn't trigger any automatic removal. That collection account will sit there for up to seven years from the date of your original delinquency, whether you paid it or not.

And here's what really gets people frustrated: a paid collection damages your credit score almost as much as an unpaid collection. The fact that there was a collection in the first place is what matters to the credit scoring models.

So you might pay off that debt thinking you're doing the right thing for your credit, and then you see your score barely move at all.

The Reality of Removing Paid Collections

So now let's dissect the part about which is easier to remove: paid or unpaid collections. And the answer might surprise you. Unpaid collections are generally easier to remove than paid collections, and I'm going to tell you exactly why.

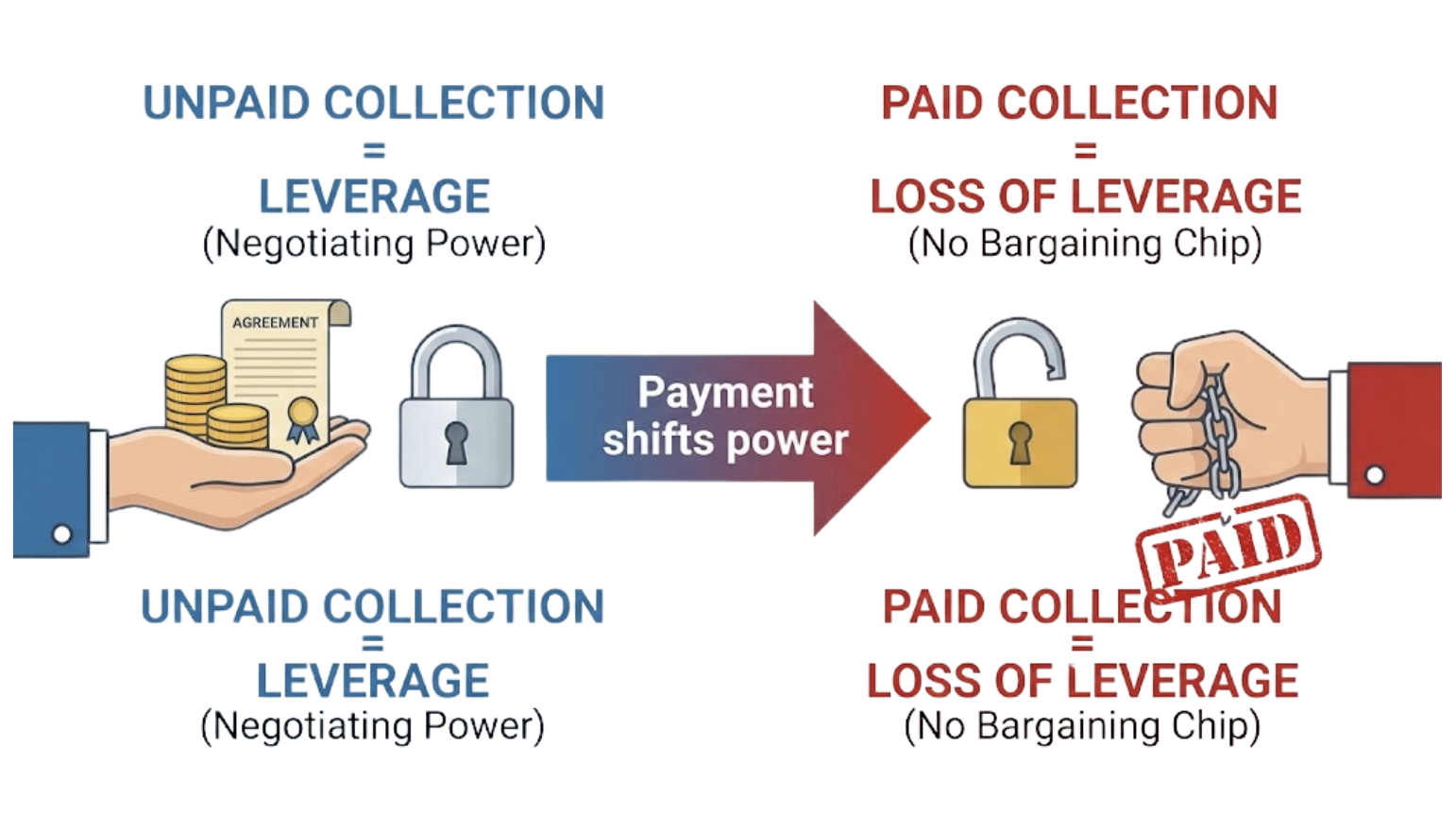

When a collection is unpaid, you have leverage. You have something the debt collector wants, which is your money. And that gives you negotiating power. You can approach that debt collector and negotiate what's called a pay-for-delete agreement. That's an agreement where you pay some amount of money, and in exchange, they agree to remove the collection from your credit report entirely.

Now, I want to be clear about something. Get that agreement in writing before you send them a single penny. Don't give them your payment information, don't give them access to your bank account, don't do anything until you have a written agreement that expressly states they will delete the collection from all three credit bureaus after you make the payment. And make sure that the agreement is signed by someone with authority at the collection agency.

But here's where it gets tricky with paid collections. Once you've already paid a collection account, you've lost your leverage. You don't have anything left to negotiate with. The debt collector already got their money, so why would they go through the extra work of removing it from your credit report? There's nothing in it for them.

That doesn't mean it's impossible to remove a paid collection, but it does mean it's significantly harder and you're going to need a different strategy.

Strategies for Removing Unpaid Collections

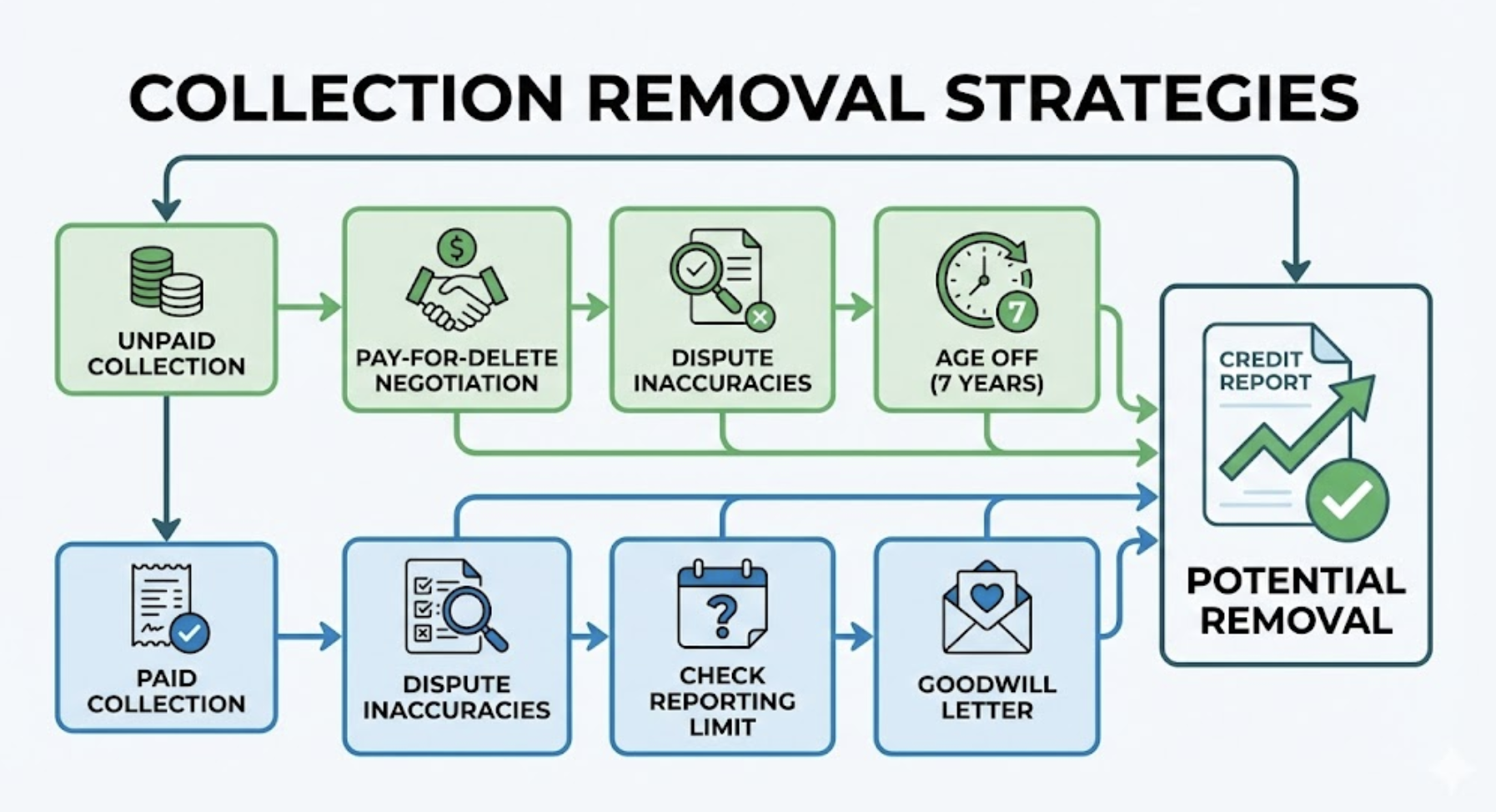

If you're dealing with an unpaid collection and your goal is to get it off your credit report, you've got a couple of options. Option number one is the pay-for-delete negotiation I just mentioned. You reach out to the collection agency, you negotiate a settlement amount, and you get them to agree in writing to delete the tradeline after you pay.

Now, some collection agencies will tell you they don't do pay-for-deletes, that it's against their policy. And you know what? Some of them really won't. But others will, especially if you're dealing with a smaller collection agency or if the debt has been sitting there for a while and they're motivated to close it out.

Your other option is to dispute the collection with the credit bureaus. If the information on your credit report is inaccurate, incomplete, or unverifiable, you have a right under the Fair Credit Reporting Act to dispute it. The credit bureaus have to investigate your dispute, and if they can't verify the information with the debt collector, they have to remove it.

And here's something important: debt collectors don't always have complete documentation. Sometimes they don't have the original contract, sometimes they can't prove the amount they're claiming is accurate, and sometimes they just don't respond to the credit bureau's investigation request because they're dealing with thousands of accounts, and yours falls through the cracks.

Strategies for Removing Paid Collections

Now, what if you've already paid the collection? You've still got options, but they require more effort and persistence. Your primary strategy here is going to be disputing the accuracy of the information on your credit report.

Look at that collection account carefully. Check the dates, check the amounts, check the account numbers, check everything. If anything is inaccurate or incomplete, you can dispute it. And sometimes paid collections have errors because when the status changes from unpaid to paid, things get updated incorrectly, or information gets lost in the shuffle.

You can also check whether the collection is beyond the seven-year reporting limit. Collections can be reported for seven years from the date of your original delinquency with the original creditor, not from when the collection agency bought the debt. If it's been more than seven years, it needs to come off your credit report regardless of whether it's been paid.

Another strategy is what's called a goodwill letter. You write to the collection agency explaining your situation, explaining why you fell behind in the first place, and asking them to remove the collection as a gesture of goodwill now that you've paid it. Does this work all the time? No. But it costs you nothing but a stamp and a little bit of time, and sometimes collection agencies will remove paid collections if you ask nicely and you have a legitimate reason for why you fell behind.

What About Settling Collections?

Now, some people want to know about settling collections for less than the full amount. And here's what you need to understand about settlements. If you settle a collection for less than what they claim you owe, that's going to show up on your credit report as "settled" rather than "paid in full."

And a settled collection is actually worse for your credit score than a paid collection. It tells future lenders that you didn't pay your full obligation, that you negotiated your way out of part of the debt. So if you're going to pay anything toward a collection, you want it either removed entirely through a pay-for-delete, or you want to pay it in full so it at least shows as paid rather than settled.

The Bottom Line on Paid vs Unpaid Collections

So here's the bottom line. If you have an unpaid collection and your goal is to get it off your credit report, you have more options and more leverage. You can negotiate a pay-for-delete, you can dispute the accuracy of the information, or you can simply let it age off your report after seven years while you focus on building positive credit history.

If you've already paid a collection, removal is harder but not impossible. You'll need to focus on disputing any inaccuracies, checking whether it's beyond the reporting limit, and potentially writing goodwill letters to see if they'll remove it voluntarily.

And here's something really important that I want you to understand: your credit score starts to recover over time even if the collection stays on your report. The impact of a collection account decreases as it ages. A three-year-old collection hurts you less than a three-month-old collection, whether it's paid or unpaid.

So if you've got collections on your credit report and you're trying to figure out the best strategy for your specific situation, that's exactly what we help people with at ASAP Credit Repair. We analyze your credit report, we identify which items are most likely to be removed, and we handle the dispute process for you so you don't have to spend your time writing letters and following up with credit bureaus and collection agencies.

If you're dealing with collections and you want professional help getting them removed, reach out to us at ASAP Credit Repair. We work with clients all across Texas and throughout the United States, and we'd be happy to review your situation and let you know exactly what we can do to help you clean up your credit report.

So go ahead and let me know in the comments: are you dealing with paid collections or unpaid collections? What state are you in? What's your goal with your credit right now? Are you trying to buy a house, get better interest rates, or just clean up your credit report? Tell me in the comments and I'll do my best to point you in the right direction.

And if this information helped you understand the difference between paid and unpaid collections, hit that like button so I know you want more content just like this. I'm Joe Mahlow with ASAP Credit Repair, and I'll see you on the next one.