guarantor definition? A guarantor is a person who agrees to pay someone else's debt if that person stops making payments. Lenders ask for a guarantor when a borrower is too risky on their own. The guarantor acts as a financial backup for the lender. Guarantors appear in personal loans, business loans, student loans, and rental leases.

Running a credit repair company, I see this go wrong all the time. One of the most unforgettable cases I handled was a retired teacher who guaranteed her nephew's car loan. She never expected to pay a cent. Eighteen months later, the car was repossessed. Her credit score dropped 87 points overnight.

The Federal Trade Commission reports that 75% of finance company loans end up paid by the guarantor or co-signer, not the borrower (FTC co-signer guide). That number alone should make anyone pause before signing. Members of r/personalfinance share similar stories every week. Many users discover the debt only after the borrower has already defaulted.

Guarantor Definition?

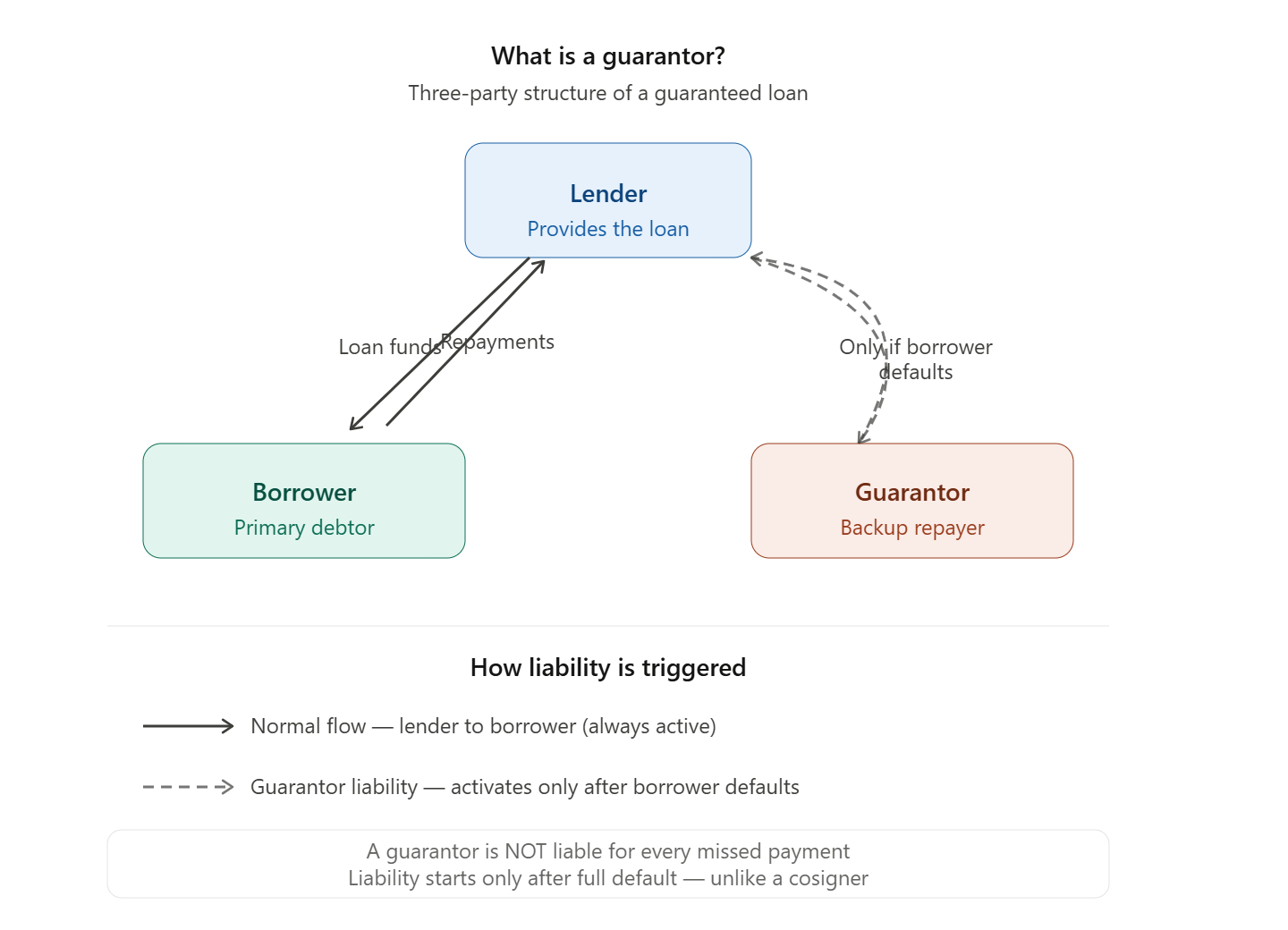

A guarantor is a third party in a loan or lease deal. The three parties are: the lender, the borrower, and the guarantor. The lender gives the money. The borrower receives it. The guarantor backs it up.

Guarantors step in only after a borrower fully defaults. The lender must first try to collect from the borrower. If that fails, the lender turns to the guarantor.

Guarantors appear across many products. These include personal loans, student loans, car loans, business loans, and apartment leases. In every case, the role is the same: cover the debt if the borrower cannot.

What Is a Guarantor in Finance?

In finance, a guarantor gives a lender a second source of repayment. If the borrower defaults, the lender can pursue the guarantor instead.

Borrowers need guarantors for several reasons. A low credit score is the most common trigger. A short credit history or low income can also create the requirement. A guarantor with strong credit fills that gap.

Guarantors appear in both personal and business finance. Parents often guarantee student loans or apartment leases for their children. Business owners often guarantee small business loans with their personal assets.

Can a Guarantor Guarantee a Loan?

Yes, a guarantor can back almost any type of loan. The guarantee is a separate legal contract. The borrower signs the loan agreement. The guarantor signs the guarantee agreement. These are two different documents.

The guarantor's liability is conditional. It only starts after the borrower defaults. This is the key difference from a co-signer, whose liability starts on day one.

The Small Business Administration (SBA) requires a personal guarantee from any business owner with 20% or more equity in a company applying for an SBA loan. This is one of the most well-known examples of a formal loan guarantee in the United States.

What Are the Different Types of Guarantors?

Guarantors fall into different categories based on their liability and context.

1. Limited guarantor. A limited guarantor covers only part of the debt. The limit can be a set dollar amount or a percentage of the loan balance. This type is common when several business partners each guarantee part of a loan.

2. Unlimited guarantor. An unlimited guarantor covers the full loan amount, including interest, fees, and collection costs. The Federal Reserve's Small Business Credit Survey found that 59% of small businesses used a personal guarantee to get funded. Most of those guarantees were unlimited.

3. Rental or lease guarantor. A rental guarantor backs an apartment lease instead of a loan. Landlords ask for one when a tenant has a low income or a poor credit score. The guarantor pays the unpaid rent or fees if the tenant fails.

4. Corporate guarantor. A corporate guarantor is a business, not a person. Companies use corporate guarantors in commercial leases and large-scale business deals.

5. Certifying guarantor. Some guarantors only confirm a person's identity. Passport applications and certain job references use this type. There is no financial liability attached.

Signing as an unlimited guarantor on a $200,000 loan is very different from confirming someone's identity on a form. The type of guarantee defines your entire exposure.

Guarantors cover a wide range of situations. They can verify an identity or take on full financial responsibility for a large loan. Knowing which type applies to your situation is the first step in protecting yourself.

Guarantor vs. Cosigner: What Is the Difference?

People often mix up guarantors and co-signers. Both back a borrower's debt, but they work in different ways.

A cosigner is liable from day one. Their name goes on the primary loan contract. The lender can pursue a cosigner for any missed payment, even the first one. Every payment, made or missed, appears on the cosigner's credit report right away.

A guarantor is liable only after the borrower fully defaults. The guarantor's credit report usually shows nothing while payments are current. Credit damage happens only if the lender pursues the guarantor after default.

Equifax confirms that cosigners are responsible for every missed payment, while guarantors only step in after full default. That is a key legal difference. But many guarantee contracts include waiver clauses that remove this protection. Always read the full agreement before you sign.

Who Qualifies as a Guarantor?

Lenders set their own rules, but most follow a similar standard. They want guarantors who can realistically cover the debt if the borrower fails.

Common requirements in the United States:

Age 21 or older.

Proof of U.S. citizenship or legal residency.

A credit score of 670 or higher.

Steady employment or a verified income source.

No history of personal loan defaults or recent bankruptcies.

Assets that could cover the guaranteed amount if needed.

A guarantor with poor credit or no income gives the lender no real protection. Most lenders reject that application outright.

In practice, most guarantors are family members or close friends. Business partners often serve as guarantors in commercial deals. Third-party guarantor services also exist for renters who cannot find a personal guarantor.

Qualifying as a guarantor requires real financial standing. Lenders run a full credit check. A weak guarantor can cost the borrower the loan, even if the borrower's own application looks solid.

Does Being a Guarantor Affect Your Credit Score?

Being a guarantor does not hurt your credit score right away. But the risk is real.

While the borrower pays on time, the debt usually does not appear on the guarantor's credit report. Payments are current, so the lender has no reason to report to the credit bureaus.

The problem starts at default. If the borrower stops paying and the lender comes after the guarantor, the debt becomes part of the guarantor's credit file. Collections and court judgments can stay on a credit report for up to seven years.

In our credit repair practice, guarantor-related credit damage is among the hardest cases we handle. The balances are usually large. The guarantor often gets no warning. The debt arrives as a collection account, which limits dispute options. Watching the borrower's payment behavior throughout the loan term is the only real way to catch a problem early.

What Happens If a Guarantor Cannot Pay?

A guarantor who cannot pay faces the same collection process as any other debtor. The lender will try to collect the full guaranteed amount. If the guarantor does not respond, the lender may go to court.

Possible outcomes include:

A civil lawsuit was filed against the guarantor.

A court judgment ordering the guarantor to pay.

Wage garnishment based on the judgment, depending on state law.

A bank account levy to recover funds directly.

A lien is placed on real property that the guarantor owns.

The Consumer Financial Protection Bureau (CFPB) notes that debt collectors must follow the Fair Debt Collection Practices Act when pursuing guarantors (CFPB debt collection overview). Guarantors have the right to request debt validation and dispute the amount if it is wrong.

Bankruptcy may discharge a guarantor's personal liability in some cases. But this depends on the loan type and the exact terms of the guarantee agreement.

When Do Lenders Require a Guarantor?

Lenders and landlords ask for a guarantor when the primary applicant does not meet their credit or income standards. These are the most common situations:

First-time borrowers with no credit history.

Students applying for private loans without income.

Borrowers with past defaults, late payments, or low credit scores.

Small business owners with limited financial history.

Renters who earn less than the landlord's income threshold.

Some lenders require a guarantor even when the borrower looks qualified on paper. The SBA's unlimited personal guarantee policy for loans with 20%+ ownership is one formal example.

If you are unsure whether a guarantor is standard for your loan type, the CFPB's consumer tools at consumerfinance.gov offer plain-language guidance on loan terms and borrower rights.

Guarantors carry real legal weight. Whether you are signing as one or asking someone to sign for you, treat the guarantee agreement the same way you treat the loan itself. Read every line. Know the liability type. Understand the default trigger. Be honest about your ability to cover the debt if things go wrong.

Credit damage from a surprise guarantee is preventable. The decision to sign is yours. Make it with full information.