805 637 7243 or 805-637-7243 is a legitimate phone number used by T-Mobile USA, Inc. and it's usually an affiliated collection related to debt. If this number shows up frequently, it likely means there is an outstanding T-Mobile account or charge associated with your name that hasn’t been paid.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered legal, financial, or professional advice. While we strive to provide accurate and up-to-date content, laws and regulations surrounding debt collection and consumer rights may vary by state and are subject to change. Always consult with a licensed attorney or financial advisor if you are dealing with a debt collection issue or legal matter. We are not affiliated with T-Mobile, or any debt collection agency.

Getting repeated calls from 805-637-7243 can be stressful and confusing. If you're dealing with these calls, we understand why you are searching more information for this number. Many people receive calls from this number without knowing who's calling or why.

This guide will help you understand exactly what's happening when you get calls from 805 637 7243 and give you the tools to protect your credit score and financial future.

Who Is Calling From 805-637-7243?

805-637-7243 belongs to T-Mobile USA, Inc. Collections Department. This is not a third-party debt collector. It's T-Mobile's internal collections team trying to collect unpaid debts directly.

T-Mobile USA, Inc. Complete Contact Information:

- Collections Phone: 805-637-7243

- Customer Service: 1-800-937-8997

- Corporate Address: 12920 SE 38th St, Bellevue, WA 98006

- Global Headquarters: Bonn, Germany

- Better Business Bureau Rating: F rating with over 24,000 complaints in 3 years

What Types of Debts Does 805-637-7243 Collect?

When T-Mobile calls from 805-637-7243, they're typically collecting:

- Unpaid monthly wireless service bills

- Early termination fees (ETF)

- Equipment financing (phones, tablets, accessories)

- Overage charges for data, minutes, or texts

- International roaming charges

- Returned payment fees

Recommended Read: 2105201454 on Caller ID: Who Are They and Why Are They Calling Me?

Why Is 805-637-7243 Calling You? (Top 5 Reasons)

1. Past Due T-Mobile Account

Your T-Mobile wireless account is 30+ days past due and has been transferred to their collections department.

2. Cancelled Service with Outstanding Balance

You cancelled your T-Mobile service but still owe money for your final bill, early termination fees, or equipment.

3. Unpaid Equipment Financing

You're financing a phone or device through T-Mobile and have missed payments on the equipment installment plan.

4. Billing Dispute Resolution

There's a billing dispute that T-Mobile's collections department is trying to resolve with you.

5. Account Closed with Negative Balance

Your account was closed due to non-payment and the remaining balance was sent to internal collections.

Good Story: 800-955-6600 Calling? Know Your FDCPA Rights Against The Northland Group

Your Rights Under Federal Law

The Fair Debt Collection Practices Act (FDCPA) protects you from abusive collection practices, even when dealing with T-Mobile's internal collections. Here's what they cannot do:

Prohibited Practices:

- Call before 8 AM or after 9 PM in your time zone

- Use abusive, threatening, or profane language

- Call your workplace if you tell them not to

- Discuss your debt with family, friends, or neighbors

- Make false statements about the debt amount or consequences

- Threaten legal action they don't intend to take

Your Rights Include:

- Right to request debt validation within 30 days

- Right to dispute the debt in writing

- Right to request all communication in writing only

- Right to have calls stop to your workplace

- Right to know the original creditor and debt amount

Investopedia explains that under the Fair Debt Collection Practices Act (FDCPA), debt collectors are prohibited from using abusive or deceptive tactics to collect a debt.

Must Read: Top 9 Consumer Rights Against Debt Collectors

How to Stop Calls from 805-637-7243

Method 1: Send a Cease and Desist Letter

Most Effective Approach: Send a written letter requesting all communication stop by phone.

Sample Letter:

[Date]

T-Mobile Collections Department

12920 SE 38th St

Bellevue, WA 98006

Re: Account Number: [Your Account Number]

Cease and Desist Phone Communications

This letter is to formally request that you cease all telephone communications regarding the above-referenced account. Under the Fair Debt Collection Practices Act, I am requesting that all future communications be in writing only and sent to the address below.

I am not acknowledging this debt or waiving any rights. If you wish to pursue collection of this alleged debt, please do so in writing only.

Sincerely,

[Your Name]

[Your Address]

Method 2: Debt Validation Request

Within 30 days of first contact, request complete debt validation:

What to Request:

- Original signed T-Mobile service agreement

- Complete payment history from account opening

- Detailed breakdown of all charges and fees

- Proof of T-Mobile's authority to collect

- License information for collectors contacting you

Method 3: Negotiate a Settlement

Before sending cease and desist, consider negotiating:

- Payment plan (often 0% interest)

- Lump-sum settlement (typically 40-70% of balance)

- Pay-for-delete agreement (removal from credit reports)

Advanced Debt Validation Strategies

Most people don't use debt validation effectively. Here's how to maximize this powerful tool:

The 30-Day Validation Window

T-Mobile must send written notice within 5 days of first contact including:

- Amount of debt

- Name of original creditor (T-Mobile)

- Your right to dispute the debt

- What happens if you don't dispute

Specific Validation Requests

Don't just ask for "proof." Request specific documentation:

- Original Contract: Signed service agreement or equipment financing contract

- Payment History: Complete account history from opening to charge-off

- Charge Breakdown: Itemized list of all fees, charges, and interest

- Authorization: Proof of T-Mobile's authority to collect this specific debt

- Licensing: Collection agent licensing information for your state

Sample Validation Letter

[Date]

T-Mobile Collections Department

12920 SE 38th St

Bellevue, WA 98006

Re: Account Number: [Your Account Number]

Debt Validation Request

I am exercising my right under the Fair Debt Collection Practices Act to request validation of the alleged debt referenced above. Please provide:

1. Original signed service agreement or equipment contract

2. Complete payment history from account opening to present

3. Detailed breakdown of all charges, fees, and interest

4. Documentation showing T-Mobile's legal authority to collect this debt

5. Copies of all license information for collectors contacting me

I dispute this debt and request validation before any further collection activity. This is not an acknowledgment of the debt.

Sincerely,

[Your Name]

[Your Address]

This validation letter can help you take control. According to personal finance experts at NerdWallet, ignoring debt collection calls can harm your credit score and may even escalate to legal consequences. They strongly advise responding in writing and requesting a debt validation letter before making any payments.

Settlement and Negotiation Tactics

If the debt is valid, you can still minimize damage to your credit and finances:

T-Mobile Settlement Statistics

Based on consumer reports, T-Mobile collections typically accepts:

- Recent debts (under 1 year): 50-70% settlements

- Older debts (1-2 years): 30-50% settlements

- Very old debts (3+ years): 10-30% settlements

Pay-for-Delete Negotiations

Most Valuable Strategy: Negotiate complete removal from credit reports in exchange for payment.

Negotiation Script: "I'm willing to settle this account for $[amount], but only if T-Mobile agrees to remove all negative reporting from my credit reports within 30 days of payment. I need this agreement in writing before making any payment."

Best Times to Negotiate

- End of month: Collectors need to meet quotas

- End of quarter: Higher settlement authority

- Before 180 days: Before potential charge-off

How T-Mobile Collections Affect Your Credit Score

Immediate Impact

When T-Mobile reports your account to credit bureaus:

- Credit score drop: 50-100+ points

- Account status: Shows as "Collection"

- Timeline: Usually 30-60 days after first missed payment

Long-Term Consequences

Collections on your credit report can:

- Block loan approvals for 2-3 years

- Increase interest rates on approved credit

- Affect rental applications and job opportunities

- Raise insurance premiums

- Remain on credit reports for 7 years

The Collection Timeline

- 30 days past due: Account marked late

- 60 days past due: Second late payment reported

- 90 days past due: Account may go to collections

- 120+ days past due: Collection account appears on credit report

- 180 days past due: Account typically charged off

Common Mistakes to Avoid

Mistake 1: Making Partial Payments Without Agreement

Why it's harmful:

- Resets statute of limitations

- Acknowledges debt validity

- Doesn't improve credit score

- Wastes money without resolution

Mistake 2: Providing Bank Account Information

Never give T-Mobile:

- Bank account numbers

- Routing numbers

- Debit card information

- Authorization for automatic withdrawals

Mistake 3: Verbal Payment Agreements

Always get in writing:

- Payment amounts and dates

- Settlement terms

- Credit reporting agreements

- Account closure confirmation

Mistake 4: Ignoring Legal Notices

Don't ignore:

- Court summons

- Judgment notices

- Wage garnishment orders

- Bank levy notifications

Forbes highlights in one of its articles that ignoring debt collection calls can lead to legal consequences, including wage garnishment or court judgments, especially if the debt is valid.

When T-Mobile Violations Occur

T-Mobile collections must follow federal law. Common violations include:

Frequent FDCPA Violations:

- Calling outside permitted hours (8 AM - 9 PM)

- Continuing to call after cease and desist request

- Misrepresenting debt amount or consequences

- Failing to provide written validation

- Discussing debt with unauthorized parties

How to Document Violations:

- Record call dates, times, and duration

- Save voicemails and transcribe content

- Document threats or abusive language

- Keep records of written communications

- Note any false statements made

Legal Remedies:

You can sue T-Mobile for FDCPA violations and recover:

- Up to $1,000 in statutory damages

- Attorney fees and court costs

- Actual damages (lost wages, medical bills)

- Injunctive relief to stop violations

Recommended Read: Stop 800-823-2318 Harassment: Your Rights and How to Fight Back

Credit Repair After T-Mobile Collections

Immediate Actions (First 30 Days)

- Pull credit reports from all three bureaus

- Dispute inaccurate information with credit bureaus

- Request debt validation from T-Mobile

- Document all communications

- Stop using credit cards to prevent further damage

Short-Term Strategy (1-6 Months)

- Negotiate settlement or payment plan

- Build emergency fund to avoid future collections

- Apply for secured credit card to rebuild credit

- Monitor credit reports monthly for changes

- Pay all other bills on time

Long-Term Recovery (6+ Months)

- Focus on positive payment history

- Keep credit utilization below 30%

- Don't close old credit accounts

- Consider credit limit increases

- Diversify credit types (installment + revolving)

Professional Help Options

When to Seek Help

Consider professional assistance if:

- Debt exceeds $5,000

- You're facing multiple collections

- T-Mobile is violating federal laws

- You're threatened with legal action

- Your credit score has dropped significantly

Types of Professional Help

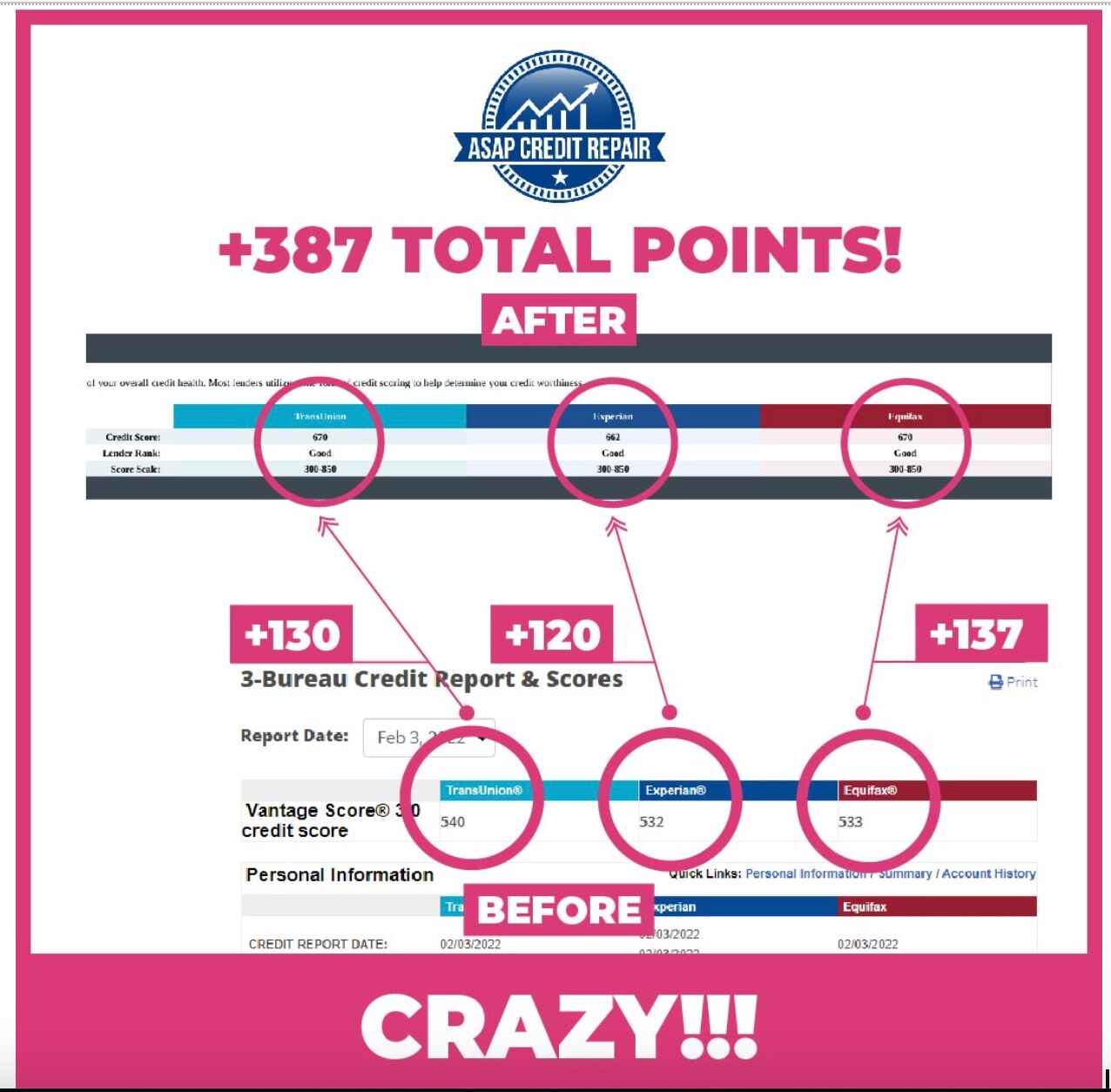

Credit Repair Companies like ASAP Credit Repair:

- Dispute inaccurate information

- Negotiate with creditors

- Average 40+ point credit score improvement in 3-6 months

- Cost: $50-350/month

See real results below:

Consumer Law Attorneys:

- Specialize in FDCPA violations

- Often work on contingency basis

- Can sue for violations and damages

- Handle complex legal issues

Credit Counseling Services:

- Non-profit debt management

- Financial education and budgeting

- Debt management plans

- Usually free or low-cost

Red Flags: Legitimate vs. Scam Calls

Legitimate T-Mobile Collections (805-637-7243):

✅ Can provide your account number and service address

✅ Know your payment history and service details

✅ Send written validation notices within 5 days

✅ Allow you to dispute the debt

✅ Stop calling if requested in writing

✅ Follow FDCPA guidelines

Scam Collectors Pretending to Be T-Mobile:

❌ Demand immediate payment by wire transfer or gift cards

❌ Threaten arrest or jail time

❌ Cannot provide specific account details

❌ Refuse to send written validation

❌ Call from spoofed numbers

❌ Ask for Social Security numbers immediately

Verification Method: Hang up and call T-Mobile customer service at 1-800-937-8997 to verify any outstanding balance.

Real Customer Experiences

Common T-Mobile Collections Complaints:

Billing Dispute Example: "T-Mobile collections called about a $2,100 debt that isn't mine. I've requested validation multiple times but never received proper documentation. They've added and removed it from my credit report twice without resolution."

Equipment Financing Issue: "After my phone was stolen, T-Mobile continued charging me for equipment financing. When I couldn't pay, they sent it to collections even though I filed a police report and insurance claim."

T-Mobile Collections Statistics:

- BBB Rating: F with 24,000+ complaints in 3 years

- Common Issues: Billing disputes, validation problems, credit reporting errors

- Resolution Rate: Approximately 60% of complaints resolved

- Average Complaint Response Time: 14 days

State-Specific Considerations

Debt collection laws vary significantly by state. Key factors include:

Statute of Limitations by State:

- 3 years: Delaware, Louisiana, North Carolina, Tennessee

- 4 years: Arkansas, Colorado, Kansas, Maryland, Minnesota, Missouri, Montana, New Hampshire, Ohio, Oklahoma, Rhode Island, Texas, Utah

- 5 years: Georgia, Hawaii, Nevada, New York, Oregon, South Carolina, Vermont, Washington, Wisconsin

- 6 years: Alabama, Alaska, Arizona, California, Connecticut, Florida, Idaho, Illinois, Indiana, Iowa, Maine, Massachusetts, Michigan, Mississippi, Nebraska, New Jersey, New Mexico, North Dakota, Pennsylvania, South Dakota, Virginia, West Virginia, Wyoming

- 10 years: Kentucky

- 15 years: Wyoming (written contracts)

Wage Garnishment Rules:

- Prohibited: North Carolina, Pennsylvania, South Carolina, Texas

- Limited: Varies by state (typically 10-25% of disposable income)

- Court order required: Most states require judgment before garnishment

Taking Action: Your Step-by-Step Plan

Week 1: Assessment and Documentation

- Verify the debt - Check credit reports for T-Mobile accounts

- Gather documentation - Old bills, contracts, payment records

- Document calls - Dates, times, what was discussed

- Check state laws - Statute of limitations and garnishment rules

Week 2: Formal Response

- Send validation letter (if within 30 days of first contact)

- Dispute credit report entries (if inaccurate)

- File complaints (if FDCPA violations occurred)

- Cease phone calls (if you prefer written communication)

Week 3-4: Negotiation or Resolution

- Review validation response (if T-Mobile provides one)

- Negotiate settlement (if debt is valid)

- Get agreements in writing before making payment

- Monitor credit reports for updates

Frequently Asked Questions About 805-637-7243

Why do I keep getting voicemails from 805-637-7243?

T-Mobile's automated dialing system leaves voicemails when you don't answer. They're required to attempt contact multiple times before taking further collection action. The persistent calling is designed to encourage payment and avoid escalation to legal action.

Is 805-637-7243 a scam or legitimate?

805-637-7243 is a legitimate T-Mobile collections number. However, scammers sometimes spoof this number.

Verification tip: Ask for your account number, service address, and recent payment history. Legitimate T-Mobile representatives will have this information.

Can I stop calls from 805-637-7243?

Yes, you can request that T-Mobile stop calling you. Send a written "cease and desist" letter requesting all communication be in writing only. However, this doesn't eliminate the debt - it only stops the phone calls.

What happens if I ignore calls from 805-637-7243?

Ignoring T-Mobile collections calls can lead to:

- Credit reporting (30-60 days after first missed payment)

- Account sent to third-party collections

- Potential lawsuit for debts over $500

- Wage garnishment (in some states)

- Bank account levies

Both NerdWallet and Forbes emphasize the importance of taking proactive steps when dealing with debt collectors. They advise consumers not to panic but to instead verify the debt, understand their rights, and avoid common mistakes like ignoring calls or making payments without proper documentation.

Can T-Mobile sue me for unpaid bills?

Yes, T-Mobile can sue for unpaid bills, typically when the debt exceeds $500-1,000. They usually prefer internal collections and settlements before pursuing legal action.

How long will T-Mobile try to collect the debt?

T-Mobile typically tries internal collections for 6-12 months before writing off the debt or selling it to a third-party agency. The statute of limitations varies by state but is typically 3-6 years.

Can I negotiate with T-Mobile collections?

Yes, T-Mobile often accepts settlement offers. Many customers successfully negotiate:

- Payment plans with 0% interest

- Lump-sum settlements for 40-70% of the balance

- Removal from credit reports (pay-for-delete agreements)

Conclusion: Protecting Your Financial Future

Dealing with calls from 805-637-7243 doesn't have to destroy your credit or financial future. By understanding your rights, using proper validation techniques, and taking strategic action, you can minimize damage and start rebuilding your credit.

Key Takeaways:

- 805-637-7243 is T-Mobile's legitimate internal collections number

- You have specific rights under federal debt collection laws

- Debt validation is your most powerful tool within the first 30 days

- Settlement negotiations can save you 30-60% on the debt amount

- Professional help is available for complex situations

Remember:

- Act quickly - You have more options early in the process

- Document everything - Keep records of all communications

- Get agreements in writing - Verbal promises aren't enforceable

- Monitor your credit - Ensure agreements are honored

- Stay informed - Know your state's specific debt collection laws

Collection accounts are temporary problems with permanent solutions. Whether you choose to validate the debt, negotiate a settlement, or work with professionals, taking action is always better than ignoring the problem.

Your credit score is important, but it's not permanent. With the right approach, patience, and persistence, you can overcome these challenges and build a stronger financial future. Don't let a collection account define your financial destiny. Fight them now!