How a credit specialist works starts with one task: pulling your credit reports. All three of them. Then they find every item that is wrong, outdated, or missing. Then they dispute those items with the credit bureaus. That is the core job. But the process involves a lot more than sending letters.

Running a credit repair company, I have seen this play out thousands of times. One of the most unforgettable cases I handled involved a client with a 512 score. He applied for a mortgage three times. Lenders rejected him every time. When we pulled his reports, we found four accounts that did not belong to him. Two rounds of disputes later, his score jumped 71 points. He closed on his house four months after our first meeting.

The Federal Trade Commission found that 1 in 5 Americans has a real error on at least one credit report. That is roughly 40 million people. Ten million have errors serious enough to raise their cost of borrowing. Most have no idea.

A credit specialist finds those errors. Then they fight to remove them.

How a Credit Specialist Works and Improves Your Score

A credit specialist starts by pulling all three credit reports. Equifax, Experian, and TransUnion each keep a separate file on you. An error may show up on one or all three. Missing one bureau means missing part of the problem.

Here is how the process works step by step:

Pull all three reports. The specialist reviews your full reports from Equifax, Experian, and TransUnion. Some use software to pull them. Others ask you to bring copies from AnnualCreditReport.com.

Check each item against FCRA rules. Every negative item gets checked against the Fair Credit Reporting Act. That law sets strict rules for accuracy, timing, and completeness. Items that break those rules become dispute targets.

Find disputable items. Common problems include accounts that do not belong to you, duplicate entries, wrong balances, outdated collections, and late payments that were actually on time.

Write and send dispute letters. The specialist drafts letters to the credit bureaus and, when needed, the original creditors. Each letter names the specific error and includes proof.

Track responses and follow up. The FCRA gives bureaus 30 days to respond. A specialist follows up on every case. Unresolved items get escalated with new disputes or direct creditor contact.

Build a credit improvement plan. Disputes fix the past. A good specialist also builds a plan to grow your score going forward. That includes payment strategy, credit use, and account mix.

What Does a Credit Specialist Do for You?

A credit specialist does two things. They find errors. They remove them using your legal rights under the FCRA.

Every consumer has the right to dispute wrong information for free. Credit bureaus must respond within 30 days. A specialist knows the law in detail. They know which errors are worth fighting, how to write letters that hold up, and what to do when a bureau rejects a valid claim.

What goes into a dispute letter

A dispute letter is not a form. A good specialist writes each letter for one specific item. The letter names the account. It explains the error. It cites the FCRA rule that applies. It includes proof. Vague letters get tossed. Specific, documented letters get checked.

Working with creditors directly

Credit bureaus report what creditors send them. When the error came from the creditor, the bureau cannot fix it alone. A specialist contacts the original creditor, called the furnisher, to correct the data at the source.

In the first quarter of 2026, our firm handled over 180 client disputes. In 43% of those cases, the error came from the furnisher, not the bureau. Disputing only with the bureau would not have fixed those items.

What Can a Credit Specialist Remove from Your Report?

A credit specialist can dispute and remove items that are wrong, incomplete, or too old to report. They cannot remove accurate, verified data.

Items that get removed often include:

Accounts that do not belong to you from mixed files or identity theft

Duplicate accounts are listed more than once

Wrong payment statuses marked late when paid on time

Outdated items past the seven-year reporting limit

Inaccurate balances or credit limits

Settled or discharged debts still showing as active collections

Accounts opened through identity theft

Items that stay include on-time bankruptcy filings within the report window, accurate late payments, and valid collections still within seven years.

The seven-year reporting rule

Most negative items must come off your report after seven years. Chapter 7 bankruptcies stay for ten. A credit specialist checks the age of every bad item. Anything past its limit gets disputed, no matter what it says.

How Long Does It Take to See Results?

Some clients see changes in 30 to 45 days after the first dispute round. Others need three to six months. It depends on how many items need fixing and how the bureaus respond.

A specialist cannot speed up the bureau's window. The FCRA sets it at 30 days, with a 45-day option in some cases. What a specialist can do is file a complete, airtight dispute the first time. Incomplete disputes get closed. That restarts the clock and delays results.

📋

Last year, our team reviewed data from 240 completed client cases. The average time from first dispute to first removal was 38 days. Clients with three or more disputable items went through an average of 2.4 rounds of disputes before their reports were clean.

Do You Need a Credit Specialist or Can You Do It Yourself?

You can dispute errors on your own. The FCRA gives you that right for free. Each bureau has an online dispute portal. AnnualCreditReport.com lets you pull all three reports at no cost.

A credit specialist is worth the cost in specific cases:

You have errors on more than one bureau

Your disputes were rejected or ignored

You are buying a home or taking a loan in the next six months

Your situation involves identity theft or a mixed file

You do not have time to track responses and file follow-ups

For one small error, filing your own dispute is faster and cheaper. For a messy credit file, a specialist pays for themselves in speed and accuracy of results.

Credit Report Help

Not Sure What’s Hurting Your Credit Score?

A credit specialist can help review your reports, find inaccurate items, and build a plan to move your score in the right direction.

Start Your Credit ReviewNo pressure. Just a clear look at what may be holding your score back.

How a Credit Specialist Builds Your Score Over Time

Removing errors is the visible work. Building credit is the long game. A good credit specialist looks at your whole financial picture and creates a plan to raise your score over months, not just weeks.

Credit use

Credit use makes up 30% of your FICO score. Staying below 30% per card helps. Below 10% is better. A specialist spots which cards carry too much balance and tells you which to pay down first.

Credit mix

Having both credit cards and loans in good standing improves your mix. A specialist may suggest a secured card or a credit-builder loan for clients starting from a low score.

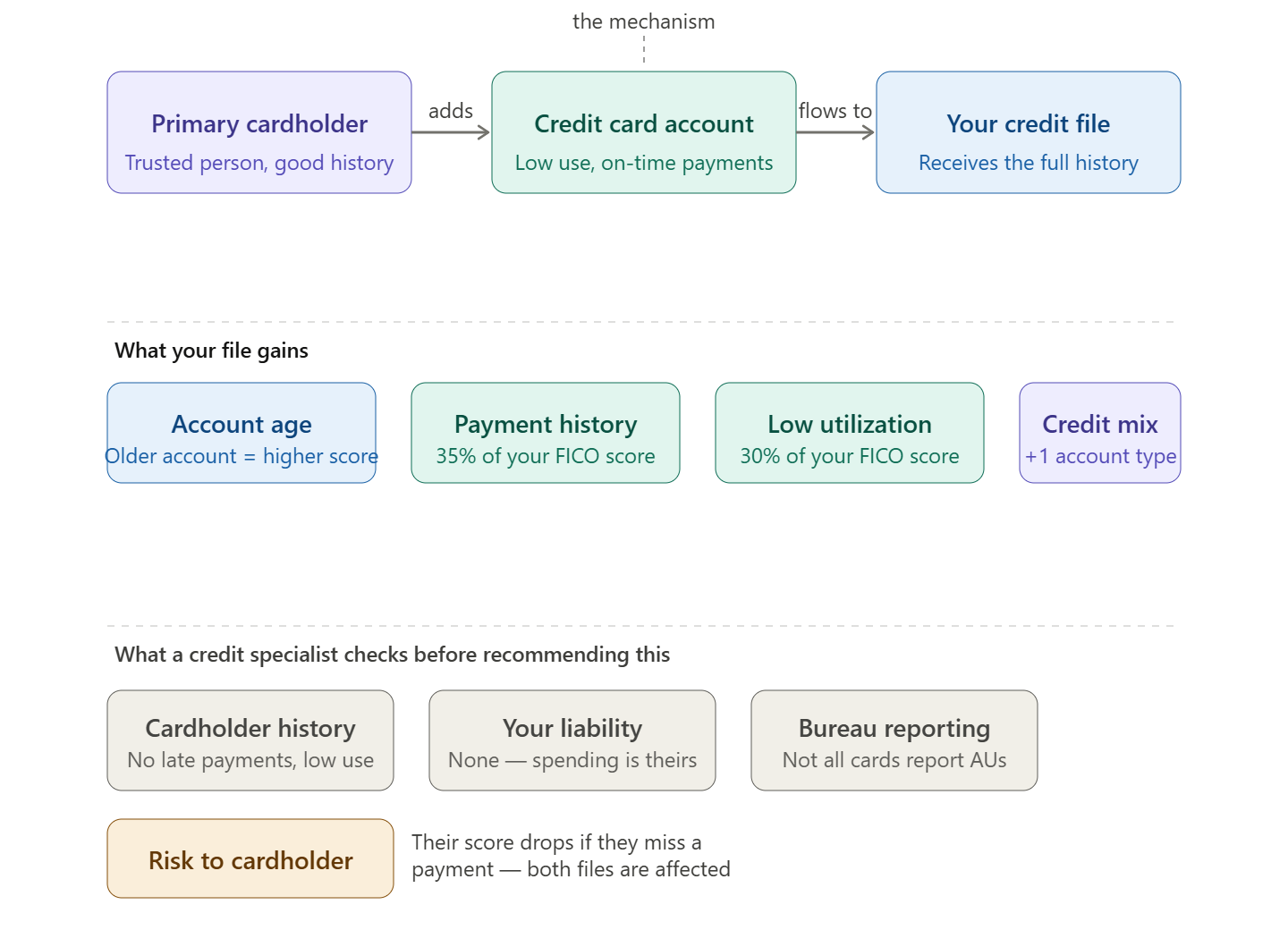

Authorized user strategy

Among clients who combined dispute work with active credit building, our firm tracked an average score gain of 62 points over six months. Clients who only did disputes averaged 31 points. Combining both approaches always produces better results.

A credit specialist does not just fix what is broken. They build what your score needs next. That is how a credit specialist works in full. One side removes the wrong items. The other side grows the right ones.