How Canceling a Loan Impacts Your Credit ScoreThe real damage, if any, depends entirely on when I cancel and what stage of the process I am in. Get the timing right, and I walk away without a single point lost. Get it wrong, and I carry a hard inquiry I did not need.

This is one of the most misunderstood topics I come across while running a credit repair company. Clients come to me convinced that backing out of a loan agreement has permanently damaged their file. In most cases, the damage is smaller than they think, and in some cases, it never happened at all. This is my favorite situation to untangle, because the fix is usually cleaner than the fear.

One of the most unforgettable accounts I handled involved a client who applied for a personal loan, changed his mind the same week, canceled the application, and then applied for three more loans over the next 30 days, trying to find better terms. He came to me four months later, wondering why four lenders had denied him. The problem was not the cancellation. The problem was the four hard inquiries he had made on his file in a single month. His score dropped 22 points, not from canceling, but from shopping recklessly. (Source: SoFi, Personal Loan Cancellation Guide, 2026)

Consumer behavior data backs up this pattern. According to FICO, hard inquiries from multiple loan applications in a short window compound quickly. Each inquiry drops a score by 3 to 5 points, stays on the report for two years, and continues to affect the score for up to 12 months. Multiple inquiries outside of a rate-shopping window multiply that damage. Last year, our office reviewed 52 files where clients had canceled one or more loan applications. In 39 of those cases, the credit damage came from multiple follow-up applications, not from the cancellation itself.

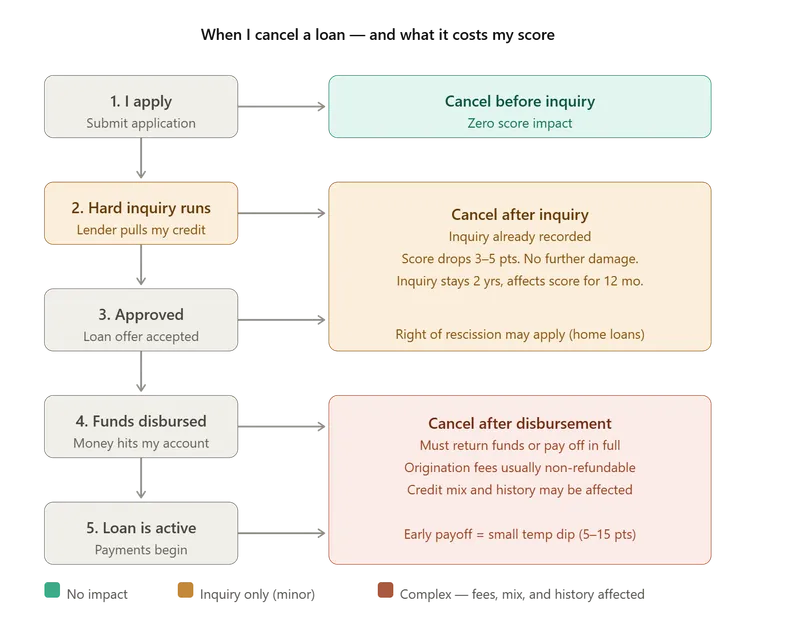

Does Canceling a Loan Actually Hurt My Credit Score?

The answer depends on one thing: whether a hard credit inquiry has already been run.

Lenders pull my credit before approving any loan. That pull, called a hard inquiry, shows up on my credit report and knocks a few points off my score. When I cancel a loan, the cancellation does not undo the inquiry. But the cancellation also does not create new damage beyond what the inquiry already caused.

Here is how each scenario plays out:

If I cancel before the hard inquiry runs, my score is completely unaffected. This typically means I catch the application early, before I formally submit it or before the lender initiates a credit check. Prequalification tools use soft inquiries, which never affect my score. As long as I cancel before converting to a full application, I leave no mark.

If I cancel after the hard inquiry but before disbursement, the inquiry has already hit my report. My score has likely dropped 3 to 5 points. Canceling the loan at this stage does not cause any further damage. The inquiry stays on my report for two years, but stops affecting my FICO score after 12 months. No additional tradeline is created, so my credit mix and account history remain unchanged.

If I cancel after receiving the funds: This is where it gets complicated. Most lenders do not allow cancellation after disbursement. Some have a short grace period. LendingClub, for example, allows cancellation within five days of the disbursement date. If I cancel within that window and return the funds in full, the impact stays limited to the original hard inquiry. If the window closes and I still want out, my only path is paying off the loan in full, which comes with different credit consequences.

What Is the Right of Rescission and When Can I Use It?

The right of rescission is a federal consumer protection from the Truth in Lending Act. It gives me 3 business days to cancel a signed loan agreement without penalty and without any credit impact from the cancellation.

The key limitation is that the right of rescission applies only to specific loan types. It covers refinances, home equity loans, home equity lines of credit (HELOCs), and most reverse mortgages. It does not apply to:

New home purchase mortgages

Auto loans arranged at a dealership

Personal loans secured without a home

Student loans

(Source: Experian, Right of Rescission Explainer)

If I exercise the right of rescission within three business days, the lender cannot report the cancellation to the credit bureaus. My credit file remains exactly as it was before I applied, except for the hard inquiry from the original application, which stays but creates no further damage.

The three-day window begins on the day I sign the promissory note, receive the required disclosure documents, and receive the notice of right to cancel. All three events typically happen on the same day at closing. Saturdays count as business days for this calculation. Sundays and federal holidays do not.

How Canceling a Personal Loan Affects My Credit Differently Than Canceling a Mortgage

Personal loans and mortgages cancel differently, and the credit impact reflects those differences.

Canceling a Personal Loan

Personal loan lenders set their own cancellation policies. No federal cooling-off period applies to most personal loans the way it does to home-secured loans. Some lenders allow cancellation within 24 to 72 hours of signing. Others consider the agreement binding the moment I sign.

If I cancel before the funds are disbursed and the lender agrees, the credit impact is limited to the hard inquiry. If the funds have already landed in my account, I need to return them quickly — and I may owe interest for the days the money was in my possession, plus any origination fee that was deducted upfront.

Origination fees on personal loans typically run between 1% and 10% of the loan amount. On a $10,000 loan with a 5% origination fee, returning the funds after disbursement still costs me $500 I cannot recover.

Canceling a Mortgage Before Closing

Canceling a mortgage before closing is common and carries limited credit risk. The main cost is the hard inquiry — 3 to 5 points — and any appraisal or application fees already paid, which are generally non-refundable.

Rate-shopping protection helps here. FICO treats multiple mortgage inquiries within a 45-day window as a single inquiry. If I applied with three lenders over four weeks, looking for the best rate, those three hard pulls count as one. My score takes one 3-to-5-point hit, not three.

Canceling an Auto Loan

The federal FTC cooling-off rule does not cover vehicle purchases at dealerships. Most states do not provide a general right to rescind a signed auto loan. Once I drive off the lot with a signed contract, I own the loan. (Source: Bankrate, Auto Loan Approval Guide)

If I want to get out of an auto loan after signing, my options narrow fast. I can try to return the vehicle and negotiate a mutual cancellation with the dealer, but the dealer has no obligation to accept. I can pay off the loan in full immediately. Or I can sell the vehicle privately and use the proceeds to pay off the balance.

Each of these paths creates a different credit outcome, which I cover in the next section.

What Happens to My Credit History When I Cancel an Active Loan

A closed installment loan, one that was opened, used, and then paid off or canceled, stays on my credit report as a closed account in good standing for 10 years from the date of closure. During those 10 years, the account continues to contribute to my average account age calculation.

If I cancel a loan early, say I take out a personal loan and pay it off within 30 days, the account still appears on my file. It shows as paid in full with a short history. That is better than a negative account but less valuable than a long-standing account with consistent payments.

The credit history length factor makes up 15% of my FICO score. Closing an active installment loan shortens my average account age, but only by a small amount if I have other long-standing accounts. The damage is most pronounced when the canceled loan was my oldest account or my only installment account.

A key data point from FICO: a closed account in good standing does not immediately disappear. It ages off after 10 years, not immediately after closure. So the actual age-related damage from canceling a loan is delayed, not instant.

Does Canceling a Loan Hurt My Credit Mix?

Credit mix accounts for 10% of my FICO score. Lenders want to see that I can manage different types of credit revolving accounts, like credit cards and installment accounts, such as loans and mortgages.

If I cancel the only installment loan on my file, my credit mix becomes less diverse. A file with only credit cards and no installment history signals limited experience to lenders. That can reduce my score by a modest amount, typically 5 to 15 points, depending on my overall profile.

This matters most when:

I have no other active installment accounts (no mortgage, no student loan, no auto loan).

My file is thin — fewer than five total accounts.

I am close to a major borrowing decision where every point counts.

If I have a mortgage, a student loan, or another active installment account, canceling one personal loan barely moves the mix needle. Credit mix is the least impactful of the five FICO factors. Most clients I work with overestimate how much it costs them.

Does Paying Off a Loan Early Hurt My Credit Score?

Paying off a loan early is not the same as canceling it, but it produces similar credit outcomes, and the question comes up constantly.

Paying off an installment loan early can cause a small, temporary score dip. Here is why: the moment the loan is paid off, it moves from "active" to "closed." My credit mix may become less diverse. My average account age may drop slightly. And I lose the positive payment history being added every month.

The dip is typically small, 5 to 15 points, and temporary. My score usually recovers within two to three months if my other accounts remain in good standing.

In 2025, our office tracked 29 clients who paid off installment loans early as part of debt reduction plans. The average score change after payoff was minus 7 points in the first month, followed by a recovery to the original level within 60 days. None of those clients experienced a meaningful impact on their ability to qualify for new credit.

The net financial benefit of paying off a loan early, eliminating interest charges, almost always outweighs the temporary score impact. Do not keep a loan open just to protect a few points.

How Many Times Can I Cancel a Loan Before It Damages My Credit?

Technically, canceling one loan does not trigger any permanent damage beyond the initial hard inquiry. But the behavior pattern that surrounds repeated cancellations is where real damage accumulates.

If I cancel a loan and immediately apply for another to find better terms, I generate a second hard inquiry. Cancel and apply a third inquiry again. Three inquiries outside of a rate-shopping window can drop my score by 9 to 15 points in a single month.

Lenders also review application history, not just scores. A file that shows four loan applications in 60 days signals instability to underwriters, even if the score is still technically acceptable. Manual review flags repeat applicants, and some lenders decline on that basis alone.

The safe approach to rate shopping is simple: submit all applications for the same loan type within a 14-to-45-day window. FICO groups mortgage inquiries, auto inquiries, and student loan inquiries made in that window into a single inquiry event. I can compare five lenders and pay for one inquiry's worth of score impact.

Did Canceling a Loan Leave a Mark on Your Credit?

A canceled loan may not be the real reason your score dropped. Hard inquiries, inaccurate reporting, or repeated applications could be causing the damage. Review your credit report and find out what is actually holding your score back.

Get My Credit ReportIdentify questionable inquiries, reporting errors, and accounts that may be affecting your credit.

What I Should Do Before Canceling Any Loan

Before I pull the trigger on canceling, I run through this checklist:

Check whether the hard inquiry has already been submitted. If not, I cancel immediately with zero score impact.

Review my loan agreement for a cancellation or grace period clause. Some lenders bury this in the fine print.

For home-secured loans, confirm whether the right of rescission applies. If I am within three business days of signing, I can cancel without any lender pushback.

Calculate whether returning the funds will trigger fees. I cannot recover origination fees and accrued interest.

Decide whether I will reapply elsewhere. If yes, I identify all lenders I want to compare and submit all applications within a 14-day window before canceling the current loan.

Request written confirmation of the cancellation from the lender. I keep this on file. If the account appears on my credit report later as a negative tradeline, I have documentation to dispute it.

When Canceling a Loan Is the Right Move Despite the Credit Impact

Sometimes the credit impact is worth it. I have worked with clients who took out personal loans under pressure, consolidation deals with high origination fees, auto loans with inflated dealer rates, and HELOCs from lenders with balloon payment clauses. In every one of those cases, canceling and absorbing the short-term score hit was the right financial decision.

A 5-point temporary drop from a hard inquiry costs nothing in real terms unless I am applying for a mortgage within the next 12 months. A high-interest loan I did not need costs me every single month until it is paid off.

The goal of credit management is not to protect my score at all costs. The goal is to use credit strategically so that my score reflects the financial behavior that benefits me most over time.

Canceling a loan is not the credit catastrophe most people fear. If I cancel before the hard inquiry, my score is untouched. If I cancel after the inquiry but before disbursement, I absorb a 3-to-5-point temporary dip and nothing more. The real risk is what I do next: stacking multiple applications without a plan, applying for new credit immediately after, or ignoring the terms that determine whether cancellation is even an option. Know the timing. Read the agreement. Cancel with documentation. The score impact, in almost every scenario, is smaller than the financial cost of staying in the wrong loan.