If you are wondering how long credit repair takes, here is the direct answer: anywhere from 30 days to 12 months or more. Simple errors in your report can be cleared in a single dispute cycle. Serious issues like collections, charge-offs, or missed payments take much longer. The sooner you understand your specific timeline, the faster you can plan around it.

I run a credit repair company. One of the most unforgettable cases I ever handled involved a client who had waited seven months with another company that promised fast fixes. When she came to us, her file had four disputable errors that no one had caught. We cleared three of them within 60 days. Her score jumped 74 points. She had been paying for promises, not results. That case is why I believe understanding this process yourself changes everything.

The numbers confirm how widespread this problem is. According to a Federal Trade Commission study, one in five Americans has an error on at least one of their three credit reports, and one in ten has an error serious enough to lower their score. A 2024 joint investigation by Consumer Reports and WorkMoney found that nearly half of the 4,000+ people who checked their credit reports discovered at least one mistake, and more than a quarter found serious errors tied to debts that could affect their financial opportunities. Complaints to the CFPB about credit report errors more than doubled between 2021 and 2023, according to Consumer Reports.

You may have one of those errors right now and not know it.

What Decides How Long Your Credit Repair Will Take?

Your timeline is not the same as anyone else's. Before you can estimate it, you need to understand what actually drives it.

Three things matter most:

The type of negative item on your report. Errors clear faster than legitimate derogatory marks like collections or late payments.

How fast the credit bureaus and creditors respond to your disputes.

Whether you are only correcting errors or also rebuilding positive history from the ground up.

One thing most people miss: credit bureaus update their data roughly once per month. Even after a dispute is resolved in your favor, the correction may not show on your report until the next reporting cycle. Build that delay into your expectations from the start.

Step 1: Pull Your Credit Reports and Find the Errors

Your first move is to pull your reports from all three bureaus — Equifax, Experian, and TransUnion. You can access all three for free at AnnualCreditReport.com. Weekly free access is currently available, not just once per year.

Go through each report carefully. Look for these specific problems:

Accounts you do not recognize or never opened.

Late payments recorded on payments you know you made on time.

Balances listed higher than what you actually owe.

Accounts that are closed but still show as open.

The same debt is listed more than once.

If your records are organized, this review takes a few hours. If you need to dig up old bank statements and payment confirmations, give yourself two to three days. Do not rush this step. The strength of every dispute you file depends on what you find here.

How Long Does This Step Take?

Plan for one to three days. Review all three reports fully before you file a single dispute. Disputing errors one at a time stretches your timeline. A complete, well-documented batch submission moves faster.

Step 2: File Your Disputes with the Credit Bureaus

Once you spot errors, you dispute them directly with the bureau reporting the wrong information. Write a dispute letter and include supporting documents, such as bank statements, payment records, or anything that proves the error. Send everything by certified mail with a return receipt so you have a timestamped paper trail.

Under the Fair Credit Reporting Act, a credit bureau must investigate your dispute within 30 days of receiving it. After finishing the investigation, they have five business days to notify you of the result. That is the legal minimum. In reality, the full cycle tends to run longer. When you factor in mail delivery time, bureau processing delays, and database update schedules, a single dispute round typically takes 30 to 45 days from start to finish. Each bureau operates independently, so disputes across all three can be resolved on different schedules.

What If the Bureau Sides Against You?

You still have options. Resubmit with stronger documentation. File a complaint with the Consumer Financial Protection Bureau at consumerfinance.gov. If you believe the bureau violated the Fair Credit Reporting Act, a consumer protection attorney can take the matter further.

How Long Does This Step Take?

Budget 30 to 45 days per dispute round. Complex cases with errors reported by multiple furnishers may need two or three rounds. Plan four to six weeks per round, not four to six days.

Step 3: Negotiate Directly with Creditors

Some negative marks on your report are accurate. A real late payment, an unpaid balance, or a collection account will not disappear through a bureau dispute. You need to go directly to the creditor.

Three approaches work here:

Pay-for-delete. You offer to settle the balance in exchange for the creditor removing the account from your report entirely.

Goodwill deletion. You write a letter asking the creditor to remove the negative mark as a courtesy, pointing to your otherwise strong payment history.

Payment plan negotiation. You set up a structured repayment agreement to resolve the balance and stop further damage to your score.

In our office last year, we tracked 38 successful goodwill deletion requests across client accounts. Most came from clients who had one or two isolated late payments on otherwise clean files. Creditors respond better when your overall history gives them a reason to work with you.

How Long Does This Step Take?

A quick creditor response with an agreement can resolve some items in two to four weeks. Larger debt settlements and formal repayment agreements typically take one to two months to finalize and show up on your report.

Step 4: Build New Positive Payment History

Removing errors and clearing negative marks handles the past. You also need to replace that damage with a record of responsible behavior going forward. This is the step most people underestimate, and it is where patience matters most.

It generally takes at least one year to rebuild bad credit typically defined as a score below 640 according to WalletHub research. Exactly how long depends on how low your score is and how far you need it to go.

The two factors that move your score the most are:

Payment history — 35% of your FICO score, the single largest factor.

Credit utilization — 30% of your FICO score.

Pay every bill on time, every month, without exception. Keep your credit card balances below 10% of your available limit. Both habits start producing visible results within three to six months when applied consistently.

Should You Use a Secured Card While Repairing Credit?

Yes. A secured credit card is one of the most effective tools for building a positive history during this phase. Charge one small, recurring expense each month, pay the full balance before your statement closes, and ask about an upgrade at six months. In our office, clients who follow this approach alongside active dispute work see score increases of 40 to 80 points within six months.

How Long Does Credit Repair Take for Each Type of Negative Mark?

Your timeline depends heavily on what specific items are dragging your score down. Here is what to expect for each one.

Late Payments

A single late payment can drop your score by 50 to 100 points. Recovery starts the moment you resume paying on time, but full recovery can take up to 18 months. Late payments stay on your report for seven years from the date of the first missed payment. Their weight on your score decreases as they age.

Collection Accounts

Collections stay on your report for seven years from the original delinquency date. A paid collection is better than an unpaid one, but paying it alone does not remove it. A successful pay-for-delete agreement is the fastest way to clear a collection before the seven-year mark.

Charge-Offs

Charge-offs remain for seven years. The balance still counts against you even after the charge-off date. Settling the balance even for less than the full amount stops further damage and shows the account as resolved.

Bankruptcy

Chapter 13 bankruptcy stays on your report for seven years from the filing date. Chapter 7 lasts for ten years. Both carry a severe initial score impact. Active rebuilding behavior after your discharge date speeds up recovery significantly.

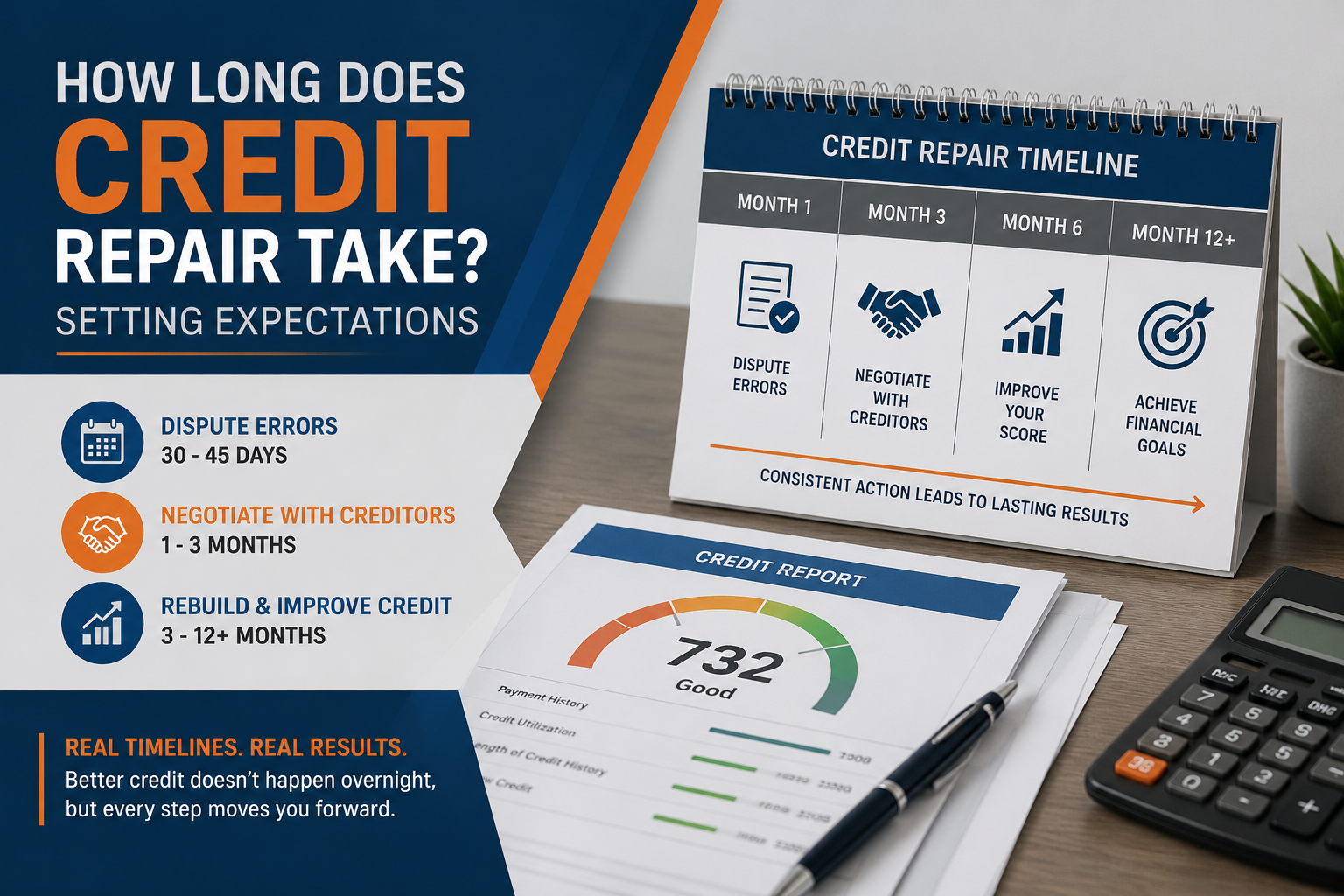

Your Full Credit Repair Timeline at a Glance

Here is what the complete process looks like from start to finish:

Pulling and reviewing all three credit reports: 1 to 3 days.

Filing disputes for errors: 30 to 45 days per round.

Negotiating with creditors for accurate negative marks: 2 to 8 weeks.

Building positive payment history: 6 to 12 months for meaningful improvement.

Full recovery after serious damage: 12 to 24 months or longer.

On average, credit repair takes 3 to 6 months to produce meaningful score improvements. That timeline gets shorter when you dispute errors quickly, remove collections, and commit to consistent financial habits from day one.

Three Things You Can Do Today to Move Faster

You do not have to wait to start. These three actions produce results faster than anything else.

Start with Your Credit Reports Before Anything Else

Errors are your fastest wins. A single corrected error can lift your score without months of waiting. Pull all three reports today at AnnualCreditReport.com. Dispute every inaccuracy you find in the same batch. Use certified mail with a return receipt so the bureaus cannot dispute when they received your dispute.

Set Up Autopay on Every Account You Have

One missed payment can undo months of progress. Set autopay for the minimum on every account right now. Then, pay the full balance on top of that manually each month. Autopay prevents timing mistakes. Full manual payments prevent interest from adding to your balance.

Stop Applying for New Credit While You Are in Active Disputes

Every new application triggers a hard inquiry, which drops your score slightly. Multiple inquiries in a short window signal risk to lenders. Hold off on any new applications until your score reaches a level where you qualify for terms that are actually worth taking.

Credit repair is not a product you buy. It is a process you work through. The clients in our office who see the fastest results are not the ones with the smallest problems. They are the ones who stay organized, act on every step without delay, and do not stop at the first pushback from a bureau or creditor.

Your first step is free. Pull your reports at AnnualCreditReport.com right now. Every day you wait is another day added to your timeline.