Are you eager to learn the key factors to boost your credit score? Whether you're aiming to improve your credit score or maintain its strength, understanding these five key factors is necessary.

Did you know that over 30% of Americans have credit scores below 601, which is considered poor or bad?

Your credit score plays a crucial role in your financial life, affecting your ability to secure loans, mortgages, and even rent an apartment. Looking at today's competitive economic landscape, knowing how to enhance your credit score is more important than ever.

This guide will explore five key factors that significantly impact your credit score. I’m also excited to share actionable tips on how to increase credit score quickly. From payment history to credit utilization, let’s explore the secrets to achieving a healthier credit score and securing a brighter financial future.

Understanding Credit Scores

Before diving into the key factors, let's first understand what a credit score is and why it matters.

What is a Credit Score and Why Does it Matter?

Your credit score is a three-digit number that represents your creditworthiness, based on your credit history and financial behavior. Lenders use this score to assess the risk of lending you money and determine the terms of your loans.

Think of it as your financial grading system. The higher your credit score, the more trustworthy you appear to lenders. Making it easier to qualify for loans, mortgages, and credit cards. A lower score may indicate higher risk to lenders, potentially leading to higher interest rates or even denial of credit.

How are Credit Scores Calculated?

Credit scores are calculated using complex algorithms that analyze various factors from your credit report. While the exact formulas used by credit scoring models are proprietary, they generally consider several key factors.

So what are the 5 factors that affect your credit score?

1. Payment History: This is the most critical factor. This represents whether you've paid your bills on time. Late payments, defaults, and bankruptcies can significantly lower your score.

2. Credit Utilization: This measures how much of your available credit you're using. Keeping your credit card balances low relative to your credit limits can positively impact your score.

3. Length of Credit History: The longer your credit history, the more data lenders have to assess your creditworthiness. It includes the age of your oldest account, the average age of all your accounts, and the age of your newest account.

4. Types of Credit: Another key factor in boosting your credit score is your credit mix. Lenders like to see a mix of different types of credit, such as credit cards, installment loans, and mortgages. Having a diverse credit portfolio can demonstrate your ability to manage various financial obligations responsibly.

5. New Credit Inquiries: Opening several new credit accounts or applying for multiple loans within a short period of time can indicate financial instability and may lower your score.

Throughout this article, we will be touching base on each of these so you can understand better.

Finding Your Credit Score

Now that you understand what a credit score is and how it's calculated, you might be wondering where to find yours. Thankfully, there are several ways to access your credit score:

1. Credit Monitoring Services: Many financial institutions and credit card companies offer free access to your credit score as part of their services. Check your bank's website or mobile app to see if this feature is available to you.

2. Credit Reporting Agencies: You can also obtain your credit score directly from the major credit reporting agencies, such as Equifax, Experian, and TransUnion. They typically offer credit monitoring services or one-time credit reports for a fee.

3. Third-Party Websites: Numerous websites and apps provide free credit scores and credit monitoring services. Just be cautious and ensure to use reputable sources to avoid scams or identity theft.

Now, time to expand on those key factors to boost your credit score fast.

Key Factors To Boost Your Credit Score

Key Factor 1: Payment History

The Importance of Payment History

Your payment history is a record of how consistently you've made on-time payments on your credit accounts, such as credit cards, loans, and mortgages. It's one of those key factors to boost your credit score because it gives lenders insight into your reliability as a borrower.

The way you make payments is also one key factor to increase your credit score for a loan.

Simply put, your payment history reflects your track record of meeting your financial obligations. When you make payments on time, it demonstrates to lenders that you're responsible and likely to repay any future debts as agreed upon. Missed or late payments can signal financial instability and may raise concerns for lenders.

How Late Payments Can Negatively Impact Credit Scores

Late payments can have significant consequences on your credit score. When you fail to make a payment on time, it's typically reported to the credit bureaus, which then include it in your credit report. This negative information can stay on your credit report for up to seven years, depending on the type of account and the severity of the delinquency.

Each late payment can cause your credit score to drop, potentially by as much as 100 points or more, depending on factors such as the length of the delinquency and your overall credit history. The more recent and frequent the late payments, the greater the impact on your score.

Let's say you have a credit card with a $1,000 balance and a minimum payment of $50 due each month. If you miss the payment deadline by just one day, you could incur a late fee of $25 from the credit card issuer. Additionally, the late payment could be reported to the credit bureaus, tarnishing your payment history.

Imagine this scenario repeated over several months. Each late payment not only incurs additional fees but also chips away at your credit score. Eventually, your credit score could plummet, making it harder to qualify for new credit or obtain favorable interest rates on loans.

Tips for Maintaining a Positive Payment History

So how can we keep up with maintaining a good payment history? I have some handy tips to keep your financial obligations on track:

1. Set up automatic payments: Schedule automatic payments for recurring bills to ensure they're paid on time every month, without the risk of forgetting.

2. Use reminders: Set up calendar reminders or notifications from your banking app to stay on top of due dates.

3. Create a budget: Establish a budget to track your income and expenses, prioritizing bill payments to avoid late fees.

4. Negotiate with creditors: If you're facing financial difficulties, reach out to creditors to discuss payment options and avoid late payments.

By following these tips and making timely payments a priority, you can maintain a positive payment history and protect your credit score.

So you see, maintaining a pristine payment history is essential for preserving and improving your credit score. By consistently making on-time payments, you can demonstrate your creditworthiness to lenders and enjoy better access to credit opportunities in the future.

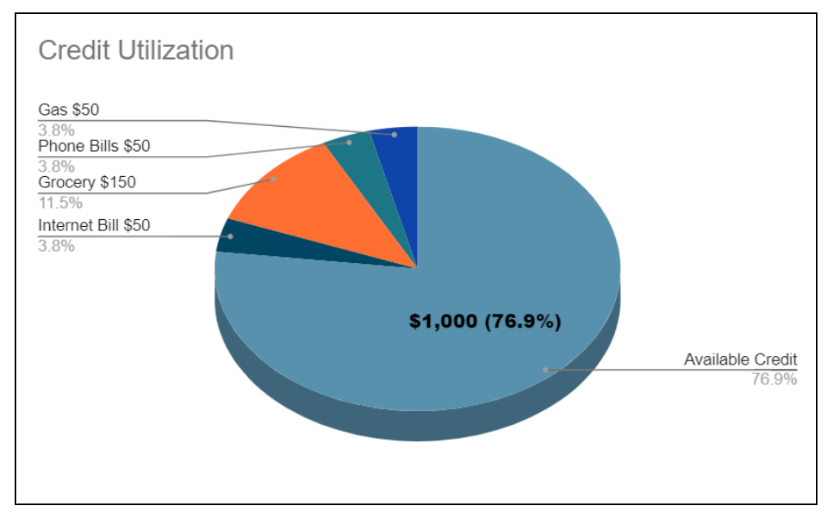

Key Factor 2: Credit Utilization

Credit Utilization and Its Significance in Credit Scoring

Credit utilization refers to the ratio of your credit card balances to your credit limits. It's a measure of how much of your available credit you're using at any given time. This factor is significant in credit scoring because it reflects your borrowing habits and financial management skills.

Simply put, a low credit utilization ratio indicates that you're using only a small portion of the credit available to you, which can be viewed positively by lenders. Conversely, a high credit utilization ratio suggests that you're heavily reliant on credit and may be at risk of overextending yourself financially.

The Ideal Credit Utilization Ratio and Its Impact on Credit Score

The ideal credit utilization ratio is generally considered to be below 30%. This means that you're using less than 30% of your available credit at any given time. Maintaining a low credit utilization ratio demonstrates to lenders that you're managing your credit responsibly and not maxing out your available credit.

Your credit utilization ratio has a direct impact on your credit score. High utilization ratios can negatively affect your score. Low ratios, on the other hand, help you turned bad credit history around. Lenders prefer to see borrowers with low credit utilization ratios because they pose less risk of defaulting on their debts.

Strategies for Reducing Credit Utilization and Improving Scores

1. Pay down balances: The most effective way to lower your credit utilization ratio is to pay down your credit card balances. Aim to keep your balances well below your credit limits to demonstrate responsible credit usage.

2. Request a credit limit increase: Another strategy is to request a credit limit increase on your existing credit cards. This can help decrease your credit utilization ratio by increasing the amount of available credit you have.

3. Use multiple credit cards: Instead of relying heavily on one credit card, consider spreading out your balances across multiple cards. This can help lower your overall credit utilization ratio.

4. Avoid closing unused accounts: Closing unused credit accounts can actually harm your credit utilization ratio by reducing the amount of available credit you have. Instead, keep these accounts open to maintain a healthy credit mix and lower overall utilization.

Key Factor 3: Credit History

Explanation of How Credit History Length Affects Credit Scores

If your goal is to know how to increase credit score to 800, the answer is patience. Let your credit history do its part. It's important to know that while there are strategies to improve credit scores, to boost credit score overnight is just an overstatement.

Your credit history length refers to the length of time your credit accounts have been open and active. It plays a significant role in determining your credit score as it provides lenders with insight into your credit management behavior over time. Essentially, the longer your credit history, the more data lenders have to assess your creditworthiness.

Credit scoring models consider the age of your oldest credit account, the age of your newest credit account, and the average age of all your accounts when calculating your credit score. A longer credit history is generally viewed positively by lenders because it demonstrates a track record of responsible credit management and financial stability.

In contrast, a short credit history may indicate limited experience with credit or a lack of established credit relationships. This can make it more difficult for lenders to assess your risk as a borrower. As a result, individuals with shorter credit histories may have lower credit scores or face challenges in qualifying for certain types of credit.

The Components of Credit History Length

Age of Oldest Credit Account: This component refers to the length of time since you opened your oldest credit account. The longer this account has been open and active, the more positive impact it can have on your credit score. Lenders often view a lengthy credit history as a sign of financial responsibility and stability.

Age of Newest Credit Account: The age of your newest credit account reflects how recently you've established new credit relationships. While opening new credit accounts can add to the diversity of your credit profile, a short credit history may initially have a minimal impact on your credit score until those accounts have been open and active for a significant period.

Average Age of All Accounts: This component calculates the average age of all your credit accounts, taking into account both old and new accounts. A higher average age indicates a longer-established credit history, which can positively influence your credit score. However, opening new accounts can lower the average age of your accounts, potentially impacting your score in the short term.

This simple explanation should help us understand why sometimes the credit repair timeline is not what we expect. As you can see, your credit history length is also a key factor in determining your creditworthiness.

Key Factor 4: Credit Mix

What's Credit Mix and Why Does It Matter?

Credit mix is simply the different types of credit accounts you have. This includes things like credit cards, loans for cars or homes, and other types of credit. Lenders like to see a mix because it shows you can handle different kinds of financial responsibilities.

Overlooking Credit Mix

Did you know that having a credit mix is the simplest factor that contributes to a rising credit standing? As an expert in credit repair, I've seen firsthand why many people aren't using the power of credit mix to their advantage. One of the main reasons is fear. The fear of taking on debt and fear of not being able to manage it effectively. Many individuals have a misconception that having more types of credit means taking on more debt, which can be intimidating.

Additionally, there's a lack of awareness about how credit mix can positively impact credit scores. Some people simply aren't aware that having a diverse mix of credit accounts, even if they're not using them all the time, can actually improve their creditworthiness in the eyes of lenders.

Moreover, there's a tendency to focus solely on short-term goals or immediate financial needs, rather than considering the long-term benefits of a balanced credit portfolio.

What Counts as Different Types of Credit?

Since we just learned that a good credit mix is another key factors to boost your credit score, let’s understand the different types of credit.

1. Revolving Credit: Credit cards. You can spend up to a certain limit and pay it back monthly.

2. Installment Credit: This is when you borrow a fixed amount and pay it back over time in regular installments. It's common with things like car loans, student loans, and mortgages.

3. Open Credit: These are accounts like lines of credit, where you have access to a set amount of credit that you can borrow against as needed.

Having a mix of these types of credit shows lenders you're responsible for different kinds of financial commitments.

How to Mix It Up and Raise Your Score

It's easier than you think to diversify your credit mix:

Check Your Mix: Look at your current credit accounts. Do you mostly have credit cards? Maybe it's time to consider adding an installment loan, like a small personal loan or a car loan. If you only have installment loans, think about adding a credit card or two.

Borrow Responsibly: Only take on debt that you're comfortable managing. Make sure you can afford the payments before you borrow.

Stay Balanced: Keep an eye on your overall debt level and make sure it doesn't get too high. Aim for a mix that's diverse but manageable.

By mixing up your credit types, you're not only improving your credit score but also showing lenders that you're a responsible borrower - and that can open up more financial opportunities for you in the long run.

Key Factor 5: New Credit Accounts

Finally, we reached the topic of new credit accounts and their impact on your credit scores. Actually, It's an important aspect of managing your credit health that often goes unnoticed.

When we talk about new credit accounts, we're referring to the number of credit accounts you've opened recently and the inquiries made by lenders when you apply for credit. This factor alone contributes 10% to your FICO score, which is a significant portion. However, here's the binding point: too many new accounts or frequent credit inquiries can actually work against you, leading to a drop in your credit score. It's like walking a tightrope – one wrong step, and you could find yourself in financial trouble.

So, while it might be tempting to jump at every new credit opportunity, it's essential to proceed cautiously. Stick to your financial plan, make timely payments, and avoid opening too many accounts or applying for credit too often. By taking a prudent approach, you can ensure that new credit accounts work in your favor, contributing positively to your credit health and overall financial well-being.

Final Thoughts

As we wrap up our topic about the five key factors for boosting credit scores, let's recap the essential points you need to remember. Payment history, credit utilization, credit history length, credit mix, and new credit account. These are the pillars that uphold your credit health. By understanding and managing these factors effectively, you’ll know the secrets to how to raise your credit score 200 points in 30 days.

Now, it's time to take action. Don't let fear or uncertainty hold you back from improving your credit score. Work with ASAP Credit Repair now! Whether it's making timely payments, diversifying your credit mix, or being cautious with new credit accounts, every small step you take can make a significant difference. Remember, your credit score is not set in stone – it's a dynamic reflection of your financial habits and decisions.

So, I encourage you to take charge of your financial future today. Start by checking your credit report regularly to monitor your progress and identify areas for improvement. And if you ever feel overwhelmed or unsure, don't hesitate to work with ASAP Credit Repair. Whether it's a credit counselor or a financial advisor, there are resources available to support you on your journey towards better credit health.

Together, let's empower ourselves to build stronger credit scores and unlock greater financial opportunities for the future. Your journey to better credit starts now.