So, your credit score isn't where you want it to be, and you're ready to take action. Feeling overwhelmed by where to start? Don't worry, because ASAP Credit Repair is here to guide you through the process.

If you're reading this, chances are you're all too familiar with the frustration of having a less-than-ideal credit score. Whether it's due to missed payments, high credit card balances, or other financial missteps, the impact of bad credit can weigh heavily on your financial future. But just like with any problem, there's a solution – and that's where we come in.

Introducing "Easy Steps To Clear Out Your Bad Credit History." With over two decades of tackling the financial landscape, I discovered the most effective way to fix bad credit.

This step-by-step guide will help you conduct a thorough examination of your credit history and take actionable steps towards improving your credit score. We believe everyone should have access to the tools they need to repair their credit and boost their score.

If you're ready to take control of your financial health and pave the way for a brighter financial future, let's dive in!

How bad credit history happens.

Understanding what forms a bad credit history is crucial for anyone looking to improve their financial standing.

Put simply, bad credit history refers to a track record of financial missteps that have negatively impacted one's credit score. These missteps can include late or missed payments, high credit card balances, bankruptcy, foreclosure, and accounts in collections, such as Charter Communications collections. While this may seem like a complex issue to attack, it's essential to break it down into manageable components.

One common reason is missed or late payments. Did you know that your payment history makes up a whopping 35% of your credit score? It's true! Every time you miss a payment or pay late, it gets recorded on your credit report and can lower your score.

Another factor that contributes to bad credit history is high credit card balances. Your credit utilization ratio, which measures how much of your available credit you're using, plays a significant role in your credit score. Ideally, you want to keep this ratio below 30%. So, if you're maxing out your credit cards or carrying high balances, it can negatively impact your score. It's like trying to balance too many plates at once – eventually, something's bound to fall.

However, bad credit history is often overlooked or misunderstood. Bad credit history encompasses more than just missed payments or high credit card balances; it's about understanding the underlying factors that contribute to a poor credit score.

Reasons for bad credit history may include:

- Missed or late payments

- High credit card balances

- Opening too many new credit accounts

- Financial mismanagement

- Identity theft or fraud

Overall, a bad credit history happens when you don't manage your finances responsibly. But the good news is that it's never too late to turn things around. By taking proactive steps to improve your credit habits and address any past mistakes, you can set yourself on the path to a brighter financial future.

Why should you worry about a bad credit history?

As we said, you can't just set and forget when it comes to credit reports, and bad credit is no exception. The financial landscape moves swiftly, much like the ever-changing world of finance. If you think that past financial decisions are enough to secure your future, think again. Ignoring the importance of your credit history could leave you lagging in the race towards financial stability.

Your credit history isn't something you can afford to neglect. It's a reflection of your financial health, much like a mirror that reveals your past mistakes and successes. Lenders, landlords, and even potential employers use this mirror to gauge your trustworthiness.

A bad credit history will be their warning sign. This will alert them that lending you money is a potential risk ahead. So what does that mean for you? It could mean higher interest rates, limited housing options, or even missed opportunities altogether.

So again, to answer the question: why worry about a bad credit history? Because it's not just a number – it's your financial reputation on the line. By taking proactive steps to address any issues and improve your credit standing, you're not just safeguarding your future; you're opening doors to a world of financial possibilities.

So, don't underestimate the importance of your credit history. Embrace it, learn from it, and watch as it propels you towards a brighter financial future.

Tools and services you need to check your credit score and history.

To kickstart your journey towards better credit, you'll need the right tools at your fingertips. You might need to sign up for some services or subscriptions, just like from ASAP Credit Repair. This all depends on how detailed you want your report to be. We have compiled this handy list to get you running. But we’ll list more as we proceed.

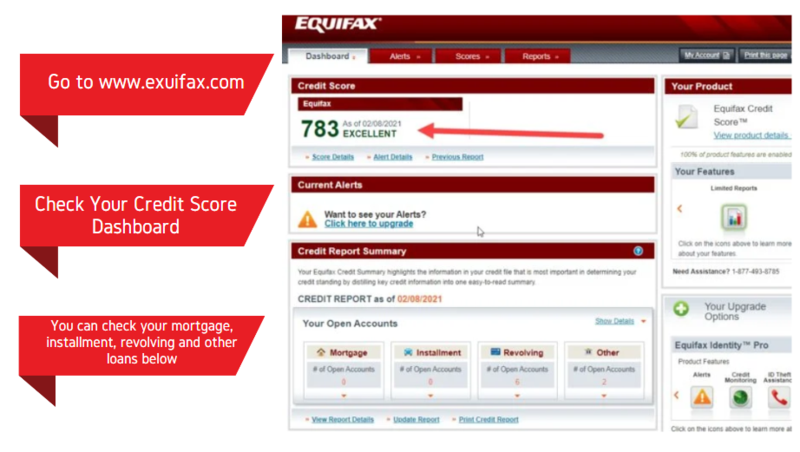

Credit Reporting Agencies: Obtain your credit reports from Equifax, Experian, and TransUnion. These agencies compile crucial information about your credit history, including payment records and account activity.

Credit Score Monitoring Services: Sign up for platforms offering credit score monitoring. These services provide regular updates on your score, alerting you to any changes or discrepancies.

Credit Score Calculators: Use online calculators to estimate your credit score based on factors like payment history and credit utilization. While not precise, they offer insights into areas for improvement.

Financial Management Apps: Explore apps with credit monitoring features. These sync with your accounts, allowing real-time tracking and personalized recommendations.

Credit Counseling Services: Consider seeking guidance from credit counseling services for tailored advice on managing and repairing your credit.

With these tools in hand, you'll gain a comprehensive understanding of your credit profile, empowering you to take proactive steps towards financial health.

How to clear out your bad credit history with 7 easy steps.

Alright, let’s skip to the good part. As your go-to guy when it comes to everything about finance and credit, I am excited to share what I know. I wrote this comprehensive guide about how to wipe away those pesky bad credit histories. Your credit score may change in the future, as not everything listed here needs to be checked every time. I recommend you weigh what works for you and eventually come up with your own credit repair strategy as you move forward.

Step 1: Check Your Credit Score and Reports

Start by getting a clear picture of your current credit situation. You can access your credit reports for free from each of the three major credit bureaus – Equifax, Experian, and TransUnion – once a year.

Reviewing these reports allows you to spot any errors or discrepancies that may be dragging down your score. Additionally, don't forget to check your credit score, which you can do for free through various online platforms or your credit card provider.

Credit reports, on the other hand, contain detailed information about your credit accounts, payment history, outstanding debts, and other financial activities. They serve as a comprehensive record of your financial behavior and are used by lenders to evaluate your creditworthiness.

By checking your credit score and reports regularly, you can:

Monitor changes: Keeping an eye on your credit score and reports allows you to spot any sudden changes or discrepancies, such as unauthorized accounts or errors, which could indicate potential fraud or identity theft.

Understand your financial standing: Reviewing your credit reports helps you understand your current financial situation, including your outstanding debts, payment history, and credit utilization. This information can help you make informed decisions about managing your finances and improving your credit score.

Identify areas for improvement: If your credit score is lower than you'd like, reviewing your credit reports can help you identify areas for improvement. For example, you may discover missed payments or high credit card balances that are negatively impacting your score. By addressing these issues, you can take steps to improve your creditworthiness over time.

Overall, checking your credit score and reports is an essential part of managing your finances responsibly and maintaining good credit health. It allows you to stay informed about your credit standing, detect any errors or fraudulent activity, and take proactive steps to improve your financial situation.

Step 2: Fix or Dispute Errors

Now after reviewing your credit score, you might want to take steps to fix it. If you come across any inaccuracies or discrepancies in your credit reports, it's essential to take swift action by disputing them with the credit bureaus.

Fixing or disputing errors on your credit reports is a crucial step in maintaining accurate financial records and ensuring your creditworthiness is correctly represented. Despite being diligent with your finances, mistakes on credit reports are more common than you might realize, affecting many consumers' ability to secure loans or credit.

This process involves notifying the credit reporting agencies of the errors and providing evidence to support your claim. By addressing these mistakes promptly, you can prevent them from negatively impacting your credit journey and potentially affecting your ability to access credit in the future.

Here’s a guide to fixing and disputing credit report errors:

1.Review Your Credit Reports: Obtain copies of your credit reports from all three major credit bureaus: Equifax, Experian, and TransUnion. Review each report carefully to identify any errors or inaccuracies in your personal information, account details, or payment history.

2.Document Errors: Keep detailed records of any errors you find, including the specific information that is incorrect and any supporting documentation you have to verify the correct information.

3.Initiate Dispute Process: Contact the credit bureau(s) reporting the errors to initiate the dispute process. You can typically file a dispute online, by mail, or over the phone, depending on the bureau's procedures.

4.Provide Supporting Evidence: When filing your dispute, provide copies of any documentation that supports your claim. This may include bank statements, payment records, or correspondence with creditors.

5.Wait for Investigation: After receiving your dispute, the credit bureau will investigate the disputed items. They will contact the creditor(s) responsible for the information and request verification of the accuracy of the data.

6.Review Investigation Results: Once the investigation is complete, the credit bureau will provide you with the results. If the disputed information is found to be inaccurate, the bureau will update your credit report accordingly.

7.Request Correction: If the investigation results in a correction to your credit report, request a copy of the updated report from the credit bureau to ensure the changes have been made accurately.

8.Follow Up as Needed: If any disputed items are not resolved to your satisfaction, follow up with the credit bureau and provide additional evidence if necessary. You may also consider contacting the creditor directly to address the issue.

9.Monitor Your Credit: After resolving any errors on your credit report, continue to monitor your credit regularly to ensure that the corrections have been made and that no new errors appear. You can request free credit reports from each bureau once a year through AnnualCreditReport.com.

10. Maintain Documentation: Keep copies of all correspondence, dispute forms, and supporting documentation related to the dispute process for your records. This documentation may be helpful in case you need to dispute errors in the future.

Good Read: how to remove an eviction from your credit report

So It’s just not about identifying problems, you need to take action and be consistent about it.

Step 3: Prioritize Timely Payments

Your payment history carries significant weight in determining your credit score, accounting for a whopping 35%. Make it a priority to pay your bills on time, every time. Consider setting up automatic payments or reminders to ensure you never miss a due date. Timely payments demonstrate financial responsibility and can have a positive impact on your credit standing.

Step 4: Manage Your Credit Utilization

Your credit utilization ratio, which compares your credit card balances to your credit limits, is another important factor in your credit score calculation. Aim to keep this ratio below 30% to show lenders that you're responsible for your credit. Paying down debts and avoiding maxing out your credit cards can help you achieve and maintain a healthy utilization ratio.

Step 5: Pay Off Debts Strategically

I know this might be everybody’s least favorite subject when it comes to finance. But we cannot skip this part since this is critical. If you want to fix that bad credit history, you've got to tackle those debts head-on. No beating around the bush here. Outstanding debts can weigh you down and hinder your efforts to improve your credit score.

You need a plan—a clear strategy to show those debts who's boss. Think of it as drawing up battle lines against your financial foes. There are a couple of ways to approach this:

Option one: the debt avalanche. This is all about prioritizing your debts based on interest rates. Attack the ones with the highest rates first, then work your way down the list. It's like taking out the enemy's heavy artillery before going after the smaller targets.

Option two: the debt snowball. With this approach, you start by paying off your smallest debts first, then move on to the bigger ones. It's all about building momentum and keeping your motivation up. Knock out those small debts one by one, and pretty soon, you'll be on a roll.

Now, which method should you choose? Well, it depends on your style. If you're all about saving money on interest and sticking to a strict plan, go with the debt avalanche. But if you need some quick wins to keep you motivated, the debt snowball might be more your speed.

But the bottom line here is you need to pick a strategy and stick with it. Consistency is key when it comes to paying down debt. Keep making those payments month after month, and you'll start to see those balances shrink and your credit score rise. It's not gonna be easy, but trust me, it'll be worth it in the end.

Good read: What is the relationship between an emergency fund and credit/loans

Step 6: Keep Old Credit Accounts Open

Closing old credit accounts may seem like a good idea after paying them off, but it can actually harm your credit score. Why? Because keeping these accounts open helps establish a longer credit history. A long credit history can positively impact your score. It means that you have been a long-time lender and you have money to pay debts. However, one thing to keep in mind is added expense. Check for any fees or conditions associated with keeping the accounts open.

Step 7: Use Credit Wisely

While it may be tempting to apply for new credit, especially as you work towards improving your score, it's essential to exercise caution. Each new credit application triggers a hard inquiry on your credit report, which can temporarily lower your score. Only apply for credit when necessary and avoid taking on more debt than you can comfortably manage.

Bonus Tip: Regularly Monitor Your Credit

Once you've initiated the steps to fix your credit, there's no turning back!

It's important to monitor your progress regularly. Check your credit score monthly to track improvements and catch any errors early on. Remember, improving your credit score is a gradual process that requires patience and persistence.

Ready to start your credit repair journey?

To be honest, there's much more to effective credit repair than what we've covered here. Each of these steps could merit a detailed guide and more. Addressing these issues found in your credit history can set you on the path to financial improvement, potentially leading to better loan approvals and lower interest rates.

If you're eager to enhance your overall credit repair strategy, be sure to explore our comprehensive guide to improving your credit score.

But if this seems overwhelming or if you desire a deeper examination of your credit situation, don't hesitate to reach out! Our team at ASAP Credit Repair specializes in credit repair solutions and conducts audits for our clients regularly. We're here to assist you every step of the way, whether you need guidance through the process or someone to handle the audit for you.

So, what are you waiting for? Take the first step towards improving your credit today and contact us to schedule a consultation. Your journey to better credit starts now!