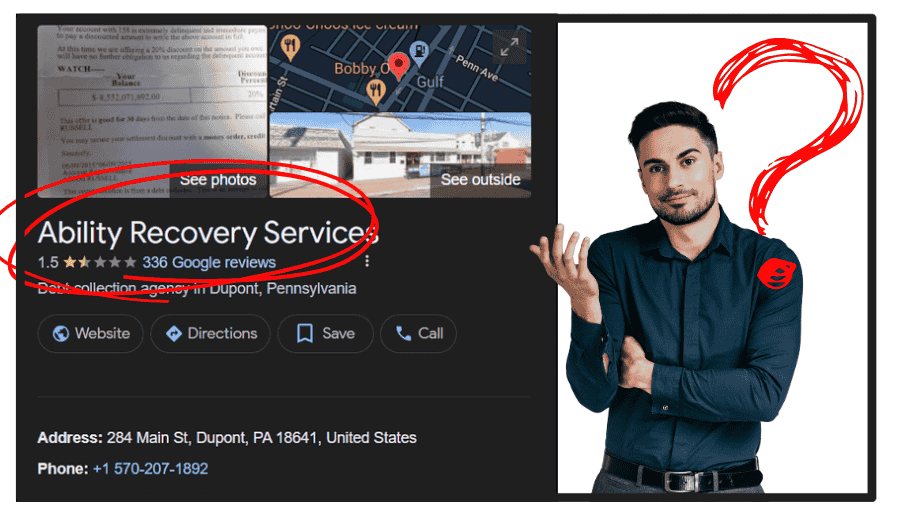

Have you ever got a call from ability recovery service asking you to pay for a debt you had a few years back?

As someone who helps people with poor credit, I know dealing with collection accounts on your credit report is a nightmare. One agency I've had to contend with is Ability Recovery Service.

Debt collection is a common practice in the United States, and millions of Americans likely receive debt collection calls daily from various agencies. (One in which is Ability Recovery Service).

According to the Consumer Financial Protection Bureau (CFPB), debt collection is one of the most complained-about financial products or services, indicating a significant volume of interactions between debt collectors and consumers.

If you find yourself in a similar situation, you may be wondering if there's anything you can do to get Ability Recovery Service deleted from your credit report.

With the right approach, you may be able to improve your credit score by ridding your report of this collection agency. I'll share what I learned from my own experience disputing Ability Recovery Service so you can determine if it's worth pursuing the removal of their account(s) from your credit history.

What is Ability Recovery Service?

Ability Recovery Service is a Debt Collection Agency.

Ability Recovery Service is a legitimate debt collection agency that has operated since 2011. They buy unpaid debts from creditors and tries to collect payments from consumers. As a debt collector, Ability Recovery Service will report debts they are trying to collect to the credit bureaus, which can hurt your credit score.

Headquartered in Scranton, Pennsylvania, ARS collects consumer debt nationwide. ARS acts as a third-party collection agency, recovering outstanding debts for:

- Telecommunications services

- Student loans

- Utility bills

- Medical bills

- Financial institution debts

You can contact ARS at: 284 Main St, Dupont, Pennsylvania 18641

Website: https://abilityrecoveryservices.com/

In the latest financial quarter, many consumers found themselves facing a familiar name on their credit reports: Ability Recovery Service. This company, known for its debt collection activities, has become a significant player in the financial landscape, impacting individuals' credit scores across the nation.

During the period, Ability Recovery Service made its mark by reporting robust financial figures. Adjusted earnings stood at 8 cents per share, aligning perfectly with market expectations. Meanwhile, the company's sales surged to $634 million, marking an impressive 21% growth compared to the previous year. Analysts had forecasted sales to hit $625 million, but Ability Recovery Service surpassed those expectations.

One standout performer in Ability Recovery Service' portfolio was its U.S. commercial business, which experienced a staggering 40% year-over-year growth. This segment emerged as a primary driver of the company's top-line growth, contributing significantly to its overall revenue stream.

They focus on medical debt collection.

Ability Recovery Service is known to specialize in collecting medical debts, often working on behalf of healthcare providers like hospitals and physicians.

While collection agencies typically report unpaid debts to the major credit bureaus (Experian, Equifax, TransUnion) – an action that usually damages your credit score – there are specific, important rules for how medical collection debt is treated on credit reports as of 2025:

- Under $500 Threshold: Medical collection accounts with an initial balance under $500 should not appear on your credit reports at all.

- Paid Collections Removed: If you fully pay off a medical collection debt, it must be removed from your credit reports.

- Waiting Period for Unpaid Debts ($500+): For unpaid medical debts of $500 or more, there has been a standard one-year waiting period before they appear on your credit report. This allows time to resolve billing or insurance issues before your credit is impacted.

Therefore, if Ability Recovery Service is handling your unpaid medical bill:

- If it's under $500, it shouldn't affect your credit report.

- If it's $500 or more and unpaid, it will likely be reported and negatively impact your credit score, but only after the waiting period.

- If you pay the debt (regardless of the amount, assuming it was reportable), it should be deleted from your reports.

Recommended: Debt Restructuring

Why Ability Recovery Services Appear on Your Credit Report?

If you've recently discovered Ability Recovery Service listed on your credit report, you're likely wondering how they landed there and what it means for your financial standing. Most likely, you have an unsettled debt.

When a debt remains unpaid for an extended period, the original creditor may deem it uncollectible and decide to sell the debt to a third-party collection agency like Ability Recovery Service. These agencies, in turn, acquire these debts at discounted rates, hoping to recoup as much of the outstanding balance as possible.

Once Ability Recovery Service takes ownership of the debt, they're entitled to report it to the major credit bureaus—Equifax, Experian, and TransUnion. This reporting serves several purposes: it alerts other creditors and lenders to the existence of the delinquent account, potentially impacting your ability to secure credit in the future.

While this may seem unfair, it is perfectly legal. However, there are steps you can take to remove Ability Recovery Service from your credit report. We will be learning more about this as we go along.

How to Remove Ability Recovery Service From Your Credit Report.

Ability Recovery Service collection accounts can drastically pull down and damage your credit score. Now, let me tell you, I've seen my fair share of clients struggling with this issue. The good thing is that, over the years, we have discovered some proven methods to tackle it head-on.

Here are some options to consider if you want to remove their entry:

Check your credit reports.

The first step is to obtain copies of your credit reports to review what exactly Ability Recovery Service is reporting. Look for any errors in the reports, like debts that do not belong to you or incorrect account information.

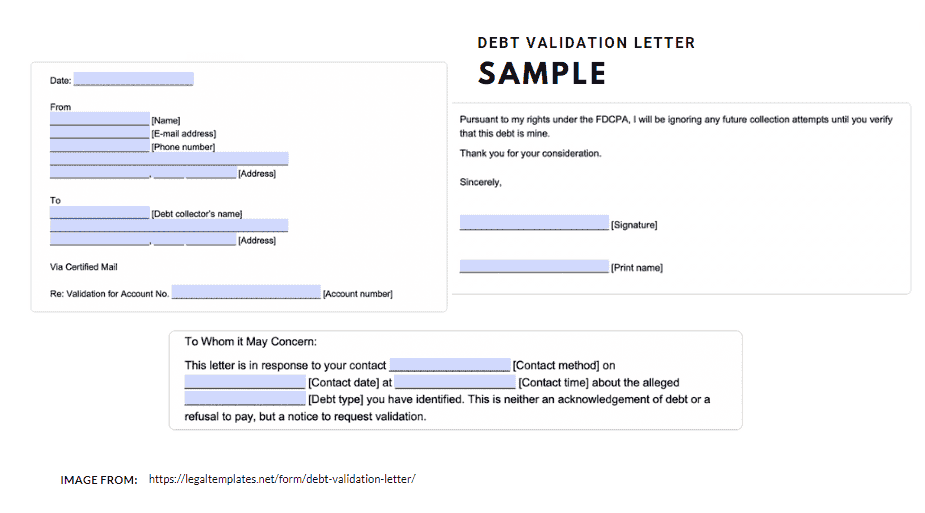

Dispute the debts with credit bureaus by sending a debt validation letter.

If you find any errors or unauthorized debts, dispute them with the credit bureaus that are reporting them. You should dispute the collection account with the credit bureaus, Experian, Equifax, and TransUnion. Provide a letter stating that you do not recognize the debt and request an investigation. The collection agency must provide verification of the debt within 30 days. If they cannot do so, the account must be removed.

You can also send a cease and desist letter to Ability Recovery Service, demanding that they stop contacting you and remove the account from your credit reports. Explain that you do not recognize the debt and wish to deal with the original creditor directly. Send this letter via certified mail with the return receipt requested so you have proof they received it.

Negotiate a pay-for-delete agreement.

If the debt is verified as valid, you may need to negotiate a settlement to have the account removed. Offer to pay a portion of the balance, such as 50-70%, in exchange for Ability Recovery Service marking the debt as “settled” and requesting deletion of the account from your credit reports. Get any agreement in writing before making a payment.

Hire a credit repair company.

A credit repair company like ASAP Credit Repair knows what should and shouldn't appear on your credit report, and we understand exactly what to dispute and the proper procedures for doing so. Our team at ASAP specializes in advocating for consumers and handling communications with debt collectors. Plus, we offer the advantage of expertise, often leading to more favorable resolutions.

Remember, if Ability Recovery Service cannot provide proper validation, the debt is inaccurate, or you successfully negotiate a pay-for-delete agreement, the collection should be removed from your credit reports. This can help boost your credit scores and make it easier to get approved for loans and credit cards.

You can also check: Understanding Debt Relief: Your Options and Outcomes!

How to Send Validation Letters to Ability Recovery Service.

As a first step to removing Ability Recovery Service from your credit report, you should send them a debt validation letter. This is a formal request for them to provide evidence that you actually owe the debt they are reporting. Many collection agencies do not have sufficient documentation to validate debts, especially older ones. Below is a step by step on how to do it:

Step 1: Request details about the debt.

In your letter, ask Ability Recovery Service to provide details about the debt including the name of the original creditor, the date you allegedly incurred the debt, the amount owed, and a copy of the original signed contract or billing statements. Explain that you are disputing the validity of this debt under the Fair Debt Collection Practices Act and will not make any payments until they provide this information.

Step 2: Send the letter certified mail, return receipt requested.

It is important to send this letter certified mail, return receipt requested. This provides proof that Ability Recovery Service received your letter. Keep copies of the letter and the receipt for your records.

Step 3: Review the information they provide.

Once you receive a response from Ability Recovery Service, review the information carefully. Look for any inaccuracies or lack of sufficient documentation. If they do not respond within 30 days or do not provide the necessary details to validate the debt, you can file a dispute with the credit bureaus to have the collection account removed from your credit reports.

Step 4: Dispute the debt with the credit bureaus.

File a dispute with Equifax, Experian, and TransUnion stating that Ability Recovery Service did not validate the debt. Provide copies of your debt validation letter and any response you received. The credit bureaus will then conduct an investigation. If Ability Recovery Service cannot provide validation, the collection account should be removed from your credit reports. This will help improve your credit scores and prevent further collections activity on this invalid debt.

Staying persistent and following proper procedures can effectively help you remove Ability Recovery Service from your credit report. Don't let invalid debts weigh down your credit and financial well-being. Take action today to clear up errors and repair your credit.

Challenging Debt Collectors like Ability Recovery Service

Understand the Fair Debt Collection Practices Act

Debt collectors can be a source of stress and anxiety for anyone facing financial difficulties. But did you know that there are laws in place to protect consumers from unfair and aggressive collection tactics? One such law is the Fair Debt Collection Practices Act (FDCPA), and knowing your rights under this legislation can make a world of difference when dealing with agencies like Ability Recovery Service.

What is the Fair Debt Collection Practices Act (FDCPA)?

The FDCPA is your shield against shady debt collection practices. Enacted back in 1977, this law sets the ground rules for how debt collectors can interact with you. Here's a snapshot of what it covers:

No Harassment: Debt collectors can't pester you endlessly or threaten you with violence. They also can't call you at crazy hours or make your phone ring off the hook.

Validation of Debts: Ever received a call about a debt you don't recognize? You have the right to ask for proof that the debt is actually yours. It's like saying, "Show me the receipts!"

Cease Communication: If the constant calls and letters are driving you nuts, you can tell debt collectors to back off with a cease and desist letter. They have to respect your wishes, except when it comes to important stuff like legal notices.

No Deceptive Tactics: Debt collectors can't trick you into paying more than you owe. They can't pretend to be lawyers or threaten to throw you in jail. Basically, they have to play fair.

Want to learn more about how to deal with debts? Check this out!

How Does This Affect Ability Recovery Service?

The Fair Debt Collection Practices Act (FDCPA) regulates the behavior of debt collection agencies like Ability Recovery Service, ensuring they adhere to fair and ethical practices when attempting to collect debts.

Under the FDCPA, Ability Recovery Service is prohibited from engaging in tactics such as harassment, making false statements, or using deceptive means to collect debts. Additionally, the FDCPA grants consumers rights, such as the ability to request validation of the debt and to dispute inaccuracies on their credit report.

Failure to comply with the FDCPA can result in penalties and legal action against Ability Recovery Service. Therefore, the FDCPA serves as a critical safeguard for consumers, providing recourse against abusive or unfair debt collection practices..So, if you find yourself on the receiving end of their calls or letters, remember that you have rights.

What You Can Do:

If Ability Recovery Service or any other debt collector comes knocking, here's what you can do:

- Know Your Rights: Familiarize yourself with the FDCPA so you can spot any violations.

- Ask for Validation: If you're not sure about a debt, request validation. They have to prove it's legit.

- Settle Smart: If you owe money, negotiate a settlement, but make sure you get everything in writing.

- Dispute Errors: If there are mistakes on your credit report, dispute them with the credit bureaus. It's your right.

Whether it's Ability Recovery Service or any other agency, remember that you have the power to stand up for yourself.

How to Prevent Ability Recovery Service from Reappearing.

To prevent Ability Recovery Service from reappearing on your credit report, you must take proactive steps.

We have learned to dispute the collection account with the credit bureaus and provide evidence that it does not belong to you. For my clients, I sent dispute letters to Equifax, Experian, and TransUnion stating that they did not owe the debt, and included proof of payment for the account in question.

Within 30 days, the collection was removed from their credit reports. However, collection agencies can re-report information, so continue monitoring your credit reports regularly. If the collection reappears, dispute it again immediately. Repeat this process each time it shows up.

You should also contact Ability Recovery Service directly and request validation of the debt in writing. Send a letter via certified mail demanding evidence that you owe the amount listed. Collection agencies must have reasonable evidence before pursuing collections, and if they cannot validate the debt, they must stop collection activity.

In many cases, they will not respond or will drop their claim against you. If they do provide evidence, review it carefully to determine if it proves you owe the debt. If it does not seem valid or accurate, send another letter disputing their claim. Continue disputing until they stop contacting you regarding this collection.

As a final precaution, you may want to place a fraud alert or freeze your credit reports. A fraud alert warns creditors that you may have been a victim of identity theft, and asks them to verify your identity before opening new accounts. A credit freeze locks access to your credit reports, preventing accounts from being opened in your name. Either of these options can help prevent Ability Recovery Service or another agency from re-reporting the disputed collection.

By taking a proactive stance, sending dispute and validation letters, and monitoring your credit regularly, you can successfully prevent Ability Recovery Service and other collection accounts from reappearing on your credit reports. Staying vigilant about inaccuracies and unwanted collections is key to keeping your credit reports clean and your scores high.

Demonstrating Successful Resolution: Removal of Ability Recovery Service

In our commitment to assisting individuals with credit challenges, we have observed tangible improvements through strategic dispute processes. Addressing collection accounts, such as those reported by Ability Recovery Service, is a key aspect of credit repair.

To show you how this can help, here's a picture that shows how one of our client's credit score changed. After we helped them get an Ability Recovery Service account removed, their credit score went up!

This shows that when you take steps to fix problems like collections from Ability Recovery Service, it can really make your credit score better. It means you might have a better chance of getting loans or credit cards in the future.

This example is indicative of the results that can be attained through informed and persistent action. By leveraging consumer rights and employing effective dispute strategies, the removal of collection agencies like Ability Recovery Service from credit reports is a demonstrable possibility, contributing to improved credit profiles and enhanced financial standing.

FAQs on Getting Rid of Ability Recovery Service

As someone looking to improve their credit, Ability Recovery Service can be frustrating to deal with. Here are some common questions I had when disputing them from my credit report:

How do I know if Ability Recovery Service is on my credit report?

To check if Ability Recovery Service is listed on your credit report, request free copies of your reports from AnnualCreditReport.com. Look for any accounts under “Collections” or “Public Records” that show Ability Recovery Service as the creditor.

Why is Ability Recovery Service contacting me?

Ability Recovery Service is a debt collection agency. If they are contacting you, it means a creditor has hired them to collect on a debt you allegedly owe. It could be for medical bills, credit cards, personal loans, etc. They will continue to contact you until the debt is resolved or disputed.

How do I dispute Ability Recovery Service?

You have the right to dispute any inaccurate information on your credit reports under the Fair Credit Reporting Act. To dispute Ability Recovery Service, contact each of the three credit bureaus – Equifax, Experian and TransUnion – and file a formal dispute in writing. Explain that you do not recognize the debt or Ability Recovery Service lacks sufficient documentation to substantiate it. The credit bureaus have 30 days to investigate and remove the collection if found to be erroneous.

What if Ability Recovery Service won’t remove my dispute?

If Ability Recovery Service refuses to remove the dispute, you may need to take further action. You can contact a consumer lawyer regarding your legal rights. You may also file a complaint against Ability Recovery Service with your state consumer protection agency and the FTC for violating consumer protection laws. As a last resort, you may need to negotiate a settlement to pay less than the full amount just to resolve the matter in exchange for deleting the entry from your credit reports.

Disputing Ability Recovery Service and removing them from your credit reports can be challenging. But by understanding your rights and taking proactive steps, you can successfully eliminate this collection agency from your financial life. Let me know if you have any other questions!

Conclusion

Ultimately, removing collections from your credit report can be a lengthy process. But staying persistent and following the proper dispute procedures can help you make progress. Don't let intimidating collection agencies like Ability Recovery Service stop you from exercising your rights under the law.

Keep all your documentation organized and continue disputing inaccurate information. With time and effort, you can repair the damage to your credit and move forward. Staying focused on your financial goals will keep you motivated. A clean credit report is possible with diligence.

If you're feeling overwhelmed or unsure of where to start, consider seeking assistance from a reputable credit repair company like ASAP Credit Repair. Their expertise and commitment to client satisfaction can provide invaluable support as you navigate the complexities of credit repair. With their help and your determination, a clean credit report is within reach.

Take the first step towards repairing your credit today and explore how ASAP Credit Repair can assist you on your journey to financial wellness.