Have you ever checked your credit score and seen a sudden drop, leaving you wondering, "what happened?"

If you suspect there might be inaccurate information on your credit report, a 609 letter can be a powerful tool to fight back. This method is grounded in the provisions of the Fair Credit Reporting Act (FCRA). Which empowers consumers to dispute inaccuracies and challenge these sudden score drops that could be caused by errors on your report.

Learning to draft a 609 letter empowers you to fix errors on your credit report. This protects your financial reputation. It also ensures accurate information for lenders.

Interested in learning more about 609 letters? Stay with me, since I’ll go in details as we go on.

Recommended: Your Guide To Navigating Credit Disputes to Avoid Denied Loan Applications

![]()

What is the FCRA?

The Fair Credit Reporting Act, or FCRA, enacted in 1970, is a federal law that regulates credit reporting agencies (CRAs) like Equifax, Experian, and TransUnion. Its core purpose is to ensure the accuracy, fairness, and privacy of the information they collect, compile, and distribute about consumers.

Section 609: Your Right to Access Credit Report Information

Within the FCRA, Section 609 holds importance for consumers. It grants you the right to access all the information CRAs have on file about you, essentially giving you a complete picture of your credit report.

Here's what Section 609 empowers you to do:

Review Everything: You can see all the details that contribute to your credit score, including account information (balances, dates), credit inquiries, public records, and late payments.

Identify Errors: By reviewing your report, you can identify any potential inaccuracies like incorrect account details, late payments you didn't make, or even debts that belong to someone else (a sign of identity theft).

Take Action: Once you find errors, Section 609 empowers you to leverage other sections of the FCRA, like Section 611, to initiate a dispute process with the CRAs.

Why is Section 609 Important?

A clean credit report is crucial for securing loans, renting an apartment, and even getting the best insurance rates. If your report contains mistakes, like incorrect account information, late payments you didn't make, or even debts that don't belong to you, it can significantly impact your financial opportunities.

By regularly accessing your credit report, you can:

Maintain Credit Health: Early detection of errors allows you to address them promptly, preventing them from negatively impacting your score.

Monitor Progress: If you're actively working on improving your credit score, you can track your progress by seeing if positive changes (like on-time payments) are reflected in your report.

Verify New Information: Section 609 empowers you to ensure any recently added information, like a new loan or credit card, is accurate and reflects the terms you agreed upon.

The FCRA and Section 609: Working Together for You

Understanding your rights under the FCRA, particularly Section 609, allows you to take control of your credit health. This ensures your credit score accurately reflects your financial responsibility, opening doors to better financial opportunities.

![]()

What is a 609 Letter?

Now that you understand the power of Section 609 and your right to access your credit report, let's delve deeper into how to leverage this knowledge. When you identify errors on your report, the next step is to dispute them effectively. Here's where a 609 letter comes in.

A 609 letter is a formal request you send to a credit bureau (Equifax, Experian, or TransUnion) to dispute errors on your credit report. It leverages your rights under the Fair Credit Reporting Act (FCRA) to challenge inaccurate or unverifiable information that could be dragging down your credit score.

If you are suffering from poor credit because of a debt you can't trace, sending a 609 letter to the credit bureaus can save your score.

How Does a 609 Letter Work?

Using a 609 letter, you're essentially forcing the credit bureau to investigate the disputed information. They are legally obligated to respond within 30-45 days and either remove the error or provide proof that it's accurate.

Here's What You Need to Do:

Pull Your Credit Report: First, obtain a free copy of your credit report from AnnualCreditReport.com. This allows you to identify any discrepancies.

Gather Information: Make copies of documents like your ID, Social Security card, and proof of address to support your dispute.

Supporting Documentation (Optional): If you have evidence to back up your claim (e.g., receipts, cancellation notices), include copies with your letter.

Write Your 609 Letter: Clearly state the errors you're contesting and why you believe they're inaccurate. You can find free 609 letter templates online, but consider seeking professional help if needed.

Send Your Letter (Certified Mail): Send your letter with a return receipt to ensure delivery to the appropriate credit bureau (addresses provided below).

Important Tips:

- Focus on verifiable errors: A 609 letter is most effective for challenging mistakes, not legitimate debts.

- Be clear and concise: Clearly state the disputed information and provide supporting documentation.

- Follow Up: If you don't hear back within 30-45 days, follow up with the credit bureau.

![]()

How to Write and Send a 609 Letter to Dispute Credit Report Errors

Crafting Your 609 Letter

1. Start with the Basics: Include your name, address, and contact information at the top.

2. Identify the Credit Bureau: Address the letter to the specific credit bureau where you found the error (Equifax, Experian, or TransUnion). You'll find their mailing addresses at the end of this guide.

3. State Your Purpose: Clearly state that you're writing to dispute errors on your credit report under Section 609 of the Fair Credit Reporting Act (FCRA).

4. Highlight the Errors: Clearly identify the specific information you're disputing. Include details like account number, date opened (if applicable), and the reason you believe it's inaccurate.

5. Request Verification (Optional): You can request the credit bureau to verify the information with the creditor who reported it.

6. Include Supporting Documents: Attach copies of any documents that support your claim, like receipts or cancellation notices.

7, Close with a Call to Action: Request the credit bureau to investigate the disputed information and remove it if found to be inaccurate. Mention the desired outcome, like having the error corrected or completely deleted from your report.

8. Sign and Date: Don't forget to sign and date the letter.

Recommended: How to Use a Pay for Delete Letter to Improve Your Credit Score: A Step-by-Step Guide

Sending Your 609 Letter

Certified Mail: It's crucial to send your letter via certified mail with a return receipt. This provides tracking and confirmation of delivery.

Keep a Copy for Your Records: Always make a copy of the letter and all the documents you send for your own records.

Can You Do It Yourself?

Yes, you can! While there are credit repair services available, writing a 609 letter is a manageable process. Many resources online offer a free 609 letter template for reference. However, if the dispute is complex or you need extra guidance, consider seeking professional help.

Remember:

- Be clear, concise, and factual in your letter.

- Focus on the disputed information and provide supporting evidence if possible.

- Keep a copy of everything you send for your records.

By following these steps and understanding your rights under the FCRA, you can effectively dispute errors on your credit report and ensure a fair and accurate representation of your financial health.

Source: www.thebalancemoney.com/dispute-credit-report-errors-960452

![]()

What should be on your 601 letter?

1. Addressing the Inaccuracy

Account Information: [Name of the account, e.g., "ABC Department Store Credit Card"] (if applicable)

Account Number: [Account Number] (if applicable)

2. Dispute Details

Please be advised that I am writing to dispute the following information on my credit report: [Clearly describe the error. Be specific. Examples include:]

- This account reflects a late payment. However, I have consistently made my payments on time. (Attach copies of bank statements as verification)

- The report shows the account in collections, despite being paid in full. (Attach a copy of the written confirmation from the creditor stating the account is paid)

- This account does not belong to me. I believe this may be a case of identity theft. (Attach any documentation supporting your claim)

3. Request for Investigation and Correction

I kindly request a thorough investigation into this dispute. I believe the aforementioned information is inaccurate and should be removed from my credit report.

To achieve an accurate reflection of my creditworthiness, I request that my report be updated as follows: [State the desired outcome. Examples include:]

- Remove the late payment notation.

- Mark the account as "paid in full."

- Delete the entire account from my report.

4. Thank You and Closing

Thank you for your prompt attention to this matter. I look forward to your response and a swift resolution to this dispute.

Sincerely,

[Your Signature] [Your Printed Name]

Important Reminders:

- Personalize this template to reflect your specific error.

- Include copies of any supporting documents you may have (e.g., bank statements, receipts, confirmation letters).

- Always keep a copy of the letter and its attachments for your records.

![]()

Ready, Aim, Dispute! Now, let's craft your letter.

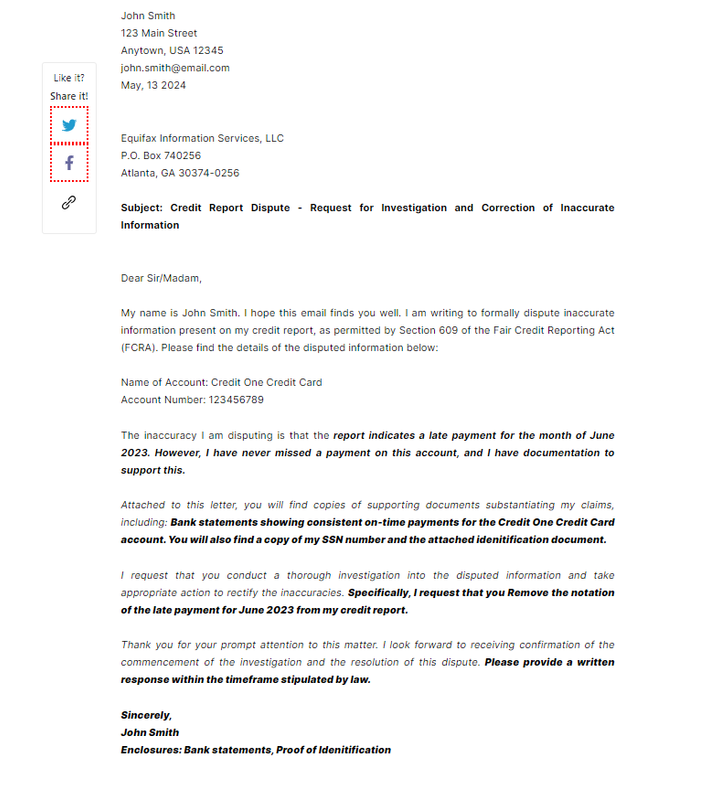

[Your Name]

[Your Address]

[City, State, Zip Code]

[Your Phone Number]

[Your Email Address]

[Date]

[Credit Bureau Name]

[Credit Bureau Address]

[City, State, Zip Code]

Subject: Credit Report Dispute - Request for Investigation and Correction of Inaccurate Information

Dear Sir/Madam,

I am writing to formally dispute inaccurate information present on my credit report, as permitted by Section 609 of the Fair Credit Reporting Act (FCRA). Please find the details of the disputed information below:

Account Information:

Name of Account: [Name of the account, e.g., "ABC Department Store Credit Card"]

Account Number: [Account Number] (if applicable)

Description of Error:

The inaccuracies I am disputing are as follows:

[Describe each inaccuracy concisely and clearly]

Supporting Evidence:

Attached to this letter, you will find copies of supporting documents substantiating my claims, including:

[List any documents or evidence provided]

Request for Investigation and Correction:

I request that you conduct a thorough investigation into the disputed information and take appropriate action to rectify the inaccuracies. Specifically, I request that you:

[State the desired action, such as removal of the erroneous information, correction of inaccuracies, etc.]

Conclusion:

Thank you for your prompt attention to this matter. I look forward to receiving confirmation of the commencement of the investigation and the resolution of this dispute. Please provide a written response within the timeframe stipulated by law.

Sincerely,

[Your Name]

Enclosures: [List any documents or evidence attached]

With this template and your determination, you're well-equipped to challenge credit report errors and pave the way for a more accurate and healthy credit score.

What if My Dispute is Denied?

If the credit bureau verifies the information, you can still fight back. You can submit additional documentation or request a reinvestigation. For complex disputes, consider seeking help from a credit repair specialist.

Conclusion: Take Charge of Your Credit Health

Don't let errors on your credit report hold you back. By understanding the power of a 609 letter and taking action, you can clear up inaccuracies and improve your credit score.

Ready to Get Started?

Download a free 609 letter template (link to template)

Learn more about credit repair services from asapcreditrepairusa.com (link to asapcreditrepairusa.com)