TLDR: Foreclosures cannot usually be removed simply because they were paid or completed. However, reporting errors, inaccurate dates, duplicate accounts, identity theft, or unverifiable information qualify the foreclosure for removal through the dispute process under the Fair Credit Reporting Act (FCRA).

How to Remove Foreclosure From Credit Report

A foreclosure is one of the most damaging events that can appear on a credit report. Besides lowering your credit score, it can delay your ability to qualify for another mortgage, increase borrowing costs, and affect approval for other types of credit.

According to Experian, a foreclosure may remain on a credit report for up to seven years. However, that does not mean every foreclosure is reported correctly. At a glance, the image below describe some steps you can take to remove foreclosure from your credit report.

As we go by, we'll go over each steps.

Can a Foreclosure Be Removed From Your Credit Report?

Yes, but not in the way most people hope when they first ask me this question.

I want to be straight with you from the start. If you lost your home to foreclosure, that event happened, it was reported correctly, and the credit bureaus have the right to show it. You cannot call Equifax on a Tuesday and ask them to erase something that is accurate just because it hurts. That is not how the law works.

But here is what most people do not realize, and this is the part that matters for your situation: foreclosures are one of the most error-prone entries on any credit report. I have reviewed thousands of mortgage files at ASAP Credit Repair USA over the past twenty years. Incorrect delinquency dates. Duplicate reporting from mortgage servicer transfers. Late payments continuing to post after the foreclosure already completed. Balances that do not match what the lender recorded. Foreclosures that still show open when the property has long been transferred.

In many of those files, the foreclosure itself was accurate. The errors around it were not. And correcting those errors, while the foreclosure stayed on the report, still moved the score significantly because the inaccurate data points piling on top of the foreclosure were doing additional damage that did not belong there.

So when someone asks me whether a foreclosure can be removed, my honest answer is this: it depends on whether anything about how it is being reported is wrong.

That is the question worth asking. Not "can I make this disappear," but "is every single piece of data around this foreclosure being reported exactly as the law requires."

According to Nolo's legal encyclopedia on FCRA reporting timelines, a foreclosure can remain on your credit report for seven years from the date of your first missed mortgage payment, not from the foreclosure completion date and not from the date the home was sold. (Nolo, How Long Does a Foreclosure Stay on Your Credit Report, May 2026)

That distinction about the starting date matters more than most people realize, and I will explain exactly why in a moment.

How a Foreclosure Damages Your Credit Score

Let me give you the honest version of what happens to a score when a foreclosure hits, because the ranges you see quoted online vary wildly and most of them are too vague to be useful.

The damage depends almost entirely on where your score was before the first missed payment. This is something a lot of other generic articles gloss over.

The higher your score going in, the more it falls.

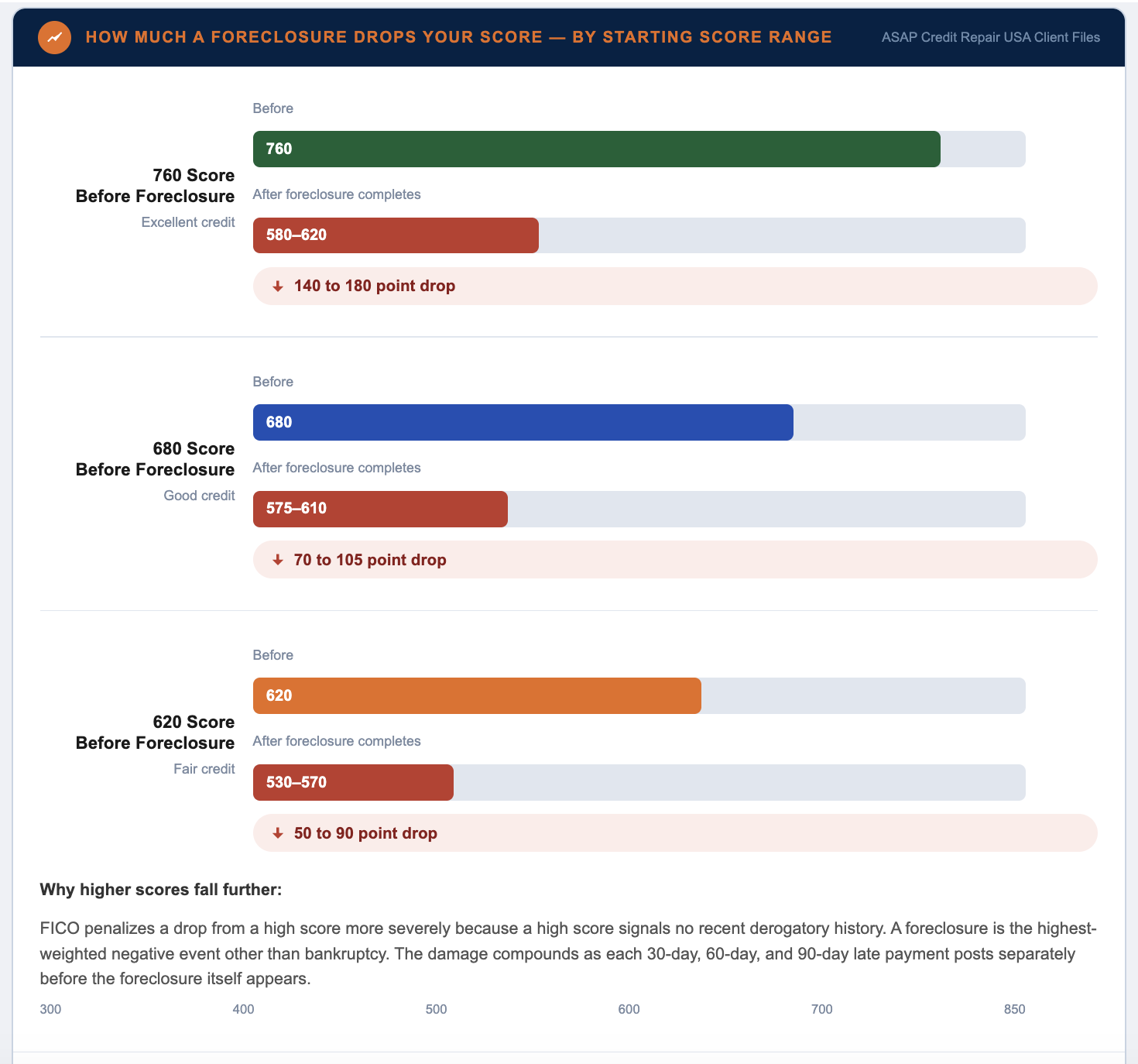

The reason is mathematical. FICO penalizes a drop from a high score more severely because a high score signals a borrower with no recent derogatory history, and a foreclosure is about as derogatory as it gets.

Not Every Foreclosure Can Be Removed—But Reporting Errors Can.

Many foreclosure accounts contain reporting errors, duplicate entries, incorrect dates, or inaccurate balances that may be disputed. Our specialists will review your credit report and identify whether your foreclosure is being reported accurately.

Get My Free Credit Report Review →✓ No obligation ✓ Personalized review ✓ Know your options

From the client files I have reviewed:

A borrower who had a 760 score before the first missed mortgage payment typically lands in the 580 to 620 range after the foreclosure completes. That is a 140 to 180 point drop.

A borrower who had a 680 score going in tends to land in the 575 to 610 range. Smaller absolute drop, similar ending point.

A borrower who had a 620 score going in may drop into the 530 to 570 range. Less fall because there was less to lose.

What makes this worse is that the damage does not happen all at once. Every 30-day late payment that builds up in the months before the foreclosure hits the report separately. By the time the foreclosure itself posts, the score has already taken multiple hits from the 30-day, 60-day, and 90-day late notations on the same account. Then the foreclosure itself posts as a major derogatory. All of those entries, the late payments and the foreclosure, stay on the report for seven years from the original first delinquency date.

According to Investopedia's guide on foreclosure and credit (Investopedia, How Foreclosure Affects Credit Score, 2024), a foreclosure is classified as a major derogatory event under FICO scoring methodology, in the same category as bankruptcy and repossession, with the highest negative weight of any credit event other than bankruptcy.

Payment history is 35% of your FICO score. A foreclosure attacks that component directly and completely. It also affects the public records section of your file. And if your mortgage account continues to report monthly updates showing ongoing delinquency after the foreclosure, which it should not but sometimes does due to servicer errors, each one of those updates refreshes the negative signal.

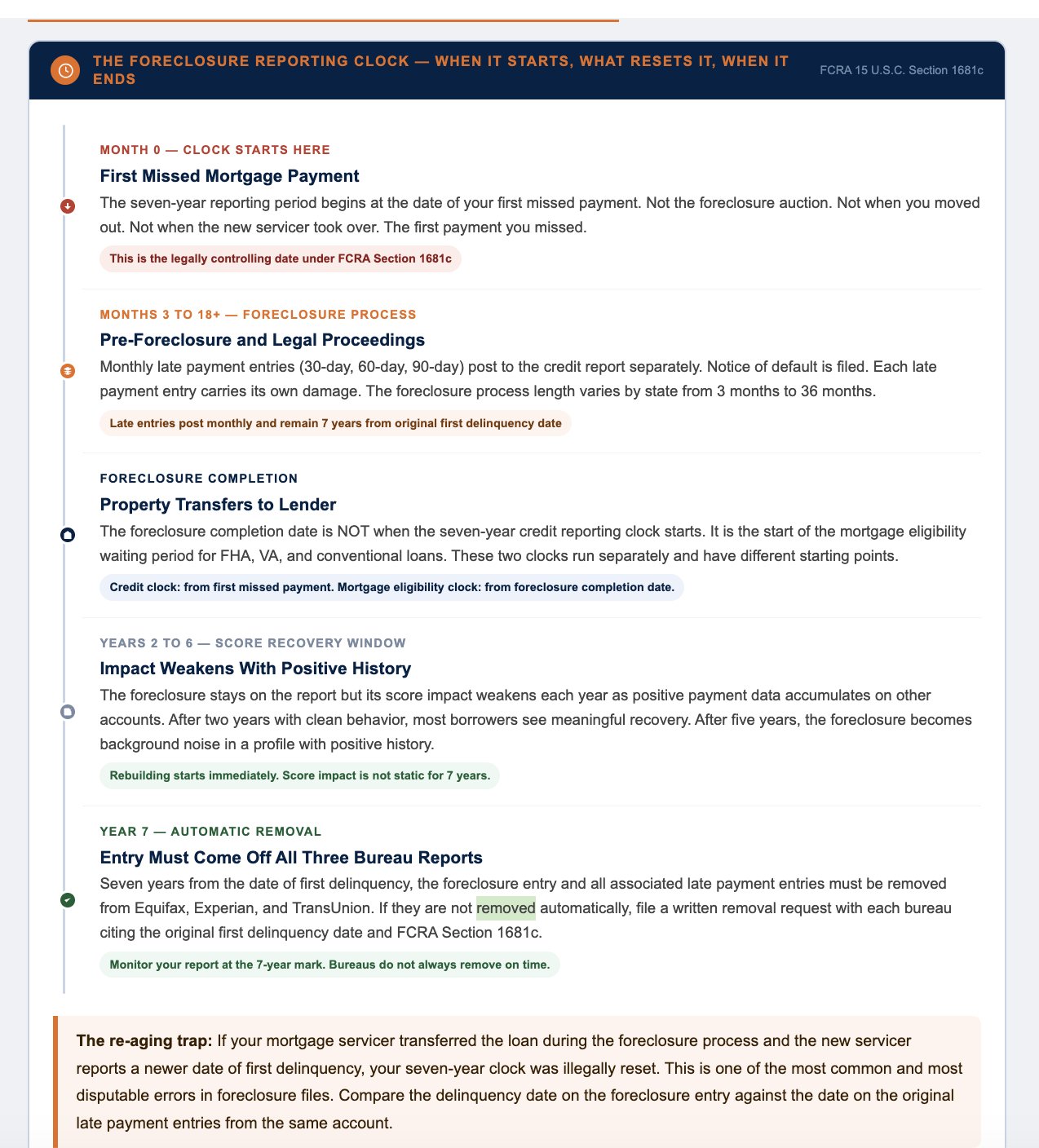

How Long Does a Foreclosure Stay on a Credit Report?

Seven years from the date of your first missed payment.

Not from the foreclosure auction date. Not from when the bank took the deed. Not from when you moved out. From the first payment you missed on that mortgage.

Here is why the starting date is critical and where a lot of people get confused, and where a lot of mortgage servicers make errors.

Say you missed your first payment in March 2020.

The foreclosure process in your state took 14 months.

The home went to auction in May 2021. The foreclosure should come off your Equifax, Experian, and TransUnion reports in March 2027, seven years from March 2020.

But if the servicer that handled the foreclosure was acquired by another company in 2021 and the new servicer started reporting the account as a new entry with a delinquency date of May 2021 when they took over, your seven-year clock just got reset by 14 months and you are being penalized for an additional year and two months that should not count.

That is not a hypothetical. That is a pattern I see consistently in files that involve mortgage servicer transfers during the foreclosure period.

The FCRA under 15 U.S.C. Section 1681c is explicit. The seven-year reporting period begins at the date of the original delinquency, and it cannot be reset by the sale of the debt, the transfer of servicing rights, or any other change in who holds the account. (Fair Credit Reporting Act, 15 U.S.C. Section 1681c)

If the dates on your credit report do not match the date of your actual first missed payment, you have a disputable error.

What Foreclosure Reporting Errors Qualify for Dispute

This is the section that I wish more people read before they call us, because the question is almost never "can I remove this foreclosure" and almost always "what specifically is wrong with how this foreclosure is being reported."

Here are the errors I see most often in mortgage files at ASAP Credit Repair USA.

Wrong date of first delinquency. The date of first delinquency on the foreclosure account does not match the date on the original late payment entries from the same account. Or it was reset when the loan was transferred to a new servicer. This error extends how long the foreclosure damages your credit beyond what the FCRA allows.

Duplicate mortgage accounts. Your original lender reported the foreclosure. Then the loan was transferred to a new servicer or sold to a different institution during the process. Now both the original lender and the new holder are reporting the same mortgage as separate negative accounts. Two entries for one foreclosure. The duplicate is fully disputable under FCRA accuracy standards.

Late payments continuing after foreclosure completion. The foreclosure completed in October 2022. The account transferred to the bank as REO property. But the servicer continues posting monthly 30-day late payment updates through 2023 on your credit report because their internal systems were not updated to reflect the completed foreclosure. Those post-completion late payment notations are reporting errors.

Balance inaccuracies. The balance shown on the foreclosure entry does not match the original mortgage balance or the deficiency amount. Servicers sometimes add fees, interest, and attorney costs to the reported balance after the fact. If the reported balance cannot be verified against the original account documentation, it is disputable.

Loan modification reported as foreclosure. A client completed a loan modification in 2021 before the foreclosure was finalized. The servicer still reported the account as a completed foreclosure. This is factually wrong. A loan modification that brought the account current means the foreclosure did not complete, and reporting it as a foreclosure is a direct inaccuracy under FCRA Section 623.

Short sale reported as foreclosure. The property sold in a short sale, meaning the borrower negotiated a sale for less than the remaining balance with the lender's approval. The lender reported it as a foreclosure on the credit file. A short sale and a foreclosure are different events with different credit reporting standards. Reporting a short sale as a foreclosure is an inaccuracy.

Identity or mixed file. The foreclosure belongs to someone with a similar name or Social Security number. The bureaus mixed two credit files and your report now includes someone else's mortgage event. This happens more than most people expect, particularly with common names or if a suffix (Jr., Sr.) was inconsistently applied across applications.

Reporting beyond the seven-year window. The date of first delinquency is now more than seven years ago and the entry is still appearing. This is one of the cleanest removal situations that exists. Pull the math, document it, and file the removal request with each bureau.

As Investopedia notes in their credit repair overview, errors in credit reports are more common than most consumers expect, and mortgage-related entries are particularly susceptible to inaccuracies during loan transfers and servicer changes. (Investopedia, Credit Repair Guide, 2024)

How to Remove Foreclosure From Your Credit Report: Step by Step

Step 1: Pull all three bureau reports and read the mortgage section carefully.

Go to AnnualCreditReport.com and pull Equifax, Experian, and TransUnion. Do not pull one and assume they match. Mortgage reporting inconsistencies across bureaus are common. One bureau may have the correct date of first delinquency. Another may show a date that was reset by a servicer transfer. One may show the account as a single entry. Another may show it twice.

For each bureau report, write down the following information from the foreclosure entry: the date of first delinquency, the original creditor name, the current servicer name if different, the reported balance, the account status, the date the account was last updated, and whether any late payment notations continue to post after the foreclosure completion date.

Step 2: Compare the credit report dates against your own mortgage records.

Pull your original mortgage documents, your notice of default, any correspondence from your servicer, and if you have them, any statements showing when your first missed payment occurred. The date on your statement showing the first missed payment is the date that should appear as the date of first delinquency on every bureau report.

If those dates do not match, you have your first disputable error.

Step 3: Check for duplicate entries.

Search your report for any version of your original lender's name and any name associated with the entity that took over servicing or ownership of the loan. If both names appear as separate tradelines reporting the same original account number or the same address and loan amount, you have a duplicate reporting situation.

Step 4: Gather your supporting documents.

For a date-of-first-delinquency error: any mortgage statement showing the first missed payment date. Your notice of default letter, which typically references the first date of default.

For a duplicate entry: the original loan documents showing the account number and originating lender, plus any correspondence confirming the servicing transfer.

For a post-foreclosure late payment error: any document showing the foreclosure completion date, such as a foreclosure sale certificate or a deed transfer confirmation, alongside the credit report showing late payment updates posted after that date.

For a short sale misreported as foreclosure: the short sale approval letter from your lender and the HUD-1 settlement statement from the closing.

Step 5: File written disputes with each bureau separately.

Send a separate dispute letter by certified mail with return receipt to Equifax, Experian, and TransUnion. Do not use the online dispute portals if you plan to escalate later, because online disputes waive certain legal rights. The postal mail creates a documented record.

Your dispute letter should identify the specific account by name and account number, state exactly which piece of information is inaccurate and why, cite the supporting document that shows the correct information, and request that the bureau investigate and correct or remove the inaccurate information.

Equifax: P.O. Box 740256, Atlanta, GA 30374

Experian: P.O. Box 4500, Allen, TX 75013

TransUnion: P.O. Box 2000, Chester, PA 19016

Under FCRA Section 611, the bureau has 30 days from receipt to complete the investigation. They contact the furnisher (your mortgage servicer or lender), which has an obligation under FCRA Section 623 to verify the data or correct it. If the furnisher cannot verify the disputed information, the bureau must correct or delete it.

Step 6: Send a separate dispute directly to your mortgage servicer.

Simultaneously with the bureau disputes, send a written dispute to your mortgage servicer or lender identifying the same inaccuracies. Under FCRA Section 623(a)(8), furnishers who receive a notice of dispute must investigate and, if they find the information is inaccurate, notify all three bureaus of the correction. You are hitting the source and the bureaus at the same time.

Step 7: Review the results and escalate if needed.

Within 30 to 45 days you will receive written results from each bureau. If a dispute is verified and the information stays, request the method of verification in writing within 15 days of the decision. This shows you exactly what documentation the servicer provided. If what they provided does not match your records, you have grounds for a second-round dispute with that specific evidence.

If disputes are repeatedly rejected despite clear documentation of an error, a consumer rights attorney who handles FCRA cases can file suit. Under FCRA Section 616 and 617, you may recover actual damages, statutory damages, and attorney fees for willful or negligent noncompliance. Many FCRA attorneys take these cases on contingency because the fee-shifting provision means you pay nothing if you do not win.

For a deeper breakdown of the late payment dispute process that runs parallel to foreclosure reporting errors, see our full guide: Late Payments on Credit Report: How to Remove Them.

Does Paying Off a Foreclosure Remove It From Your Credit Report?

No. This is one of the questions I get asked most often, and the answer is always the same.

Paying the deficiency balance on a foreclosure, if one exists, changes the account status from unpaid to paid. The entry itself stays on the report. The foreclosure notation stays. The seven-year clock does not reset. The score impact of the foreclosure does not disappear.

What paying the deficiency might do is remove the risk of the lender pursuing a court judgment for the remaining balance in states that allow deficiency judgments. That is a legal protection, not a credit reporting benefit.

If you paid the original mortgage in full before the foreclosure completed and the lender still reported a foreclosure, that is a different situation. That would be an inaccuracy. A paid-in-full mortgage that never completed foreclosure should not be reporting as a foreclosure. That is a dispute scenario, not a payment scenario.

If you completed a deed in lieu of foreclosure, where you voluntarily transferred the deed to the lender to avoid a full foreclosure, that event is also reportable but may be reported differently depending on the lender. Some lenders report a deed in lieu correctly as "deed in lieu of foreclosure." Others incorrectly report it as a standard foreclosure. If yours was a deed in lieu and your report shows a standard foreclosure, that is an inaccuracy worth disputing.

Can Credit Repair Remove a Foreclosure?

Yes, credit repair can remove a foreclosure when the foreclosure, or the data surrounding it, contains inaccuracies that cannot be verified.

What credit repair cannot do is remove an accurate foreclosure that the lender can verify. Anyone who tells you otherwise is either wrong or lying to you, and I say that as someone who runs a credit repair company.

What makes ASAP Credit Repair USA effective with foreclosure cases is the audit process. Before we file a single dispute, we review the full mortgage section of all three bureau reports looking for the specific error patterns I described above. Wrong dates, duplicate entries, post-foreclosure late payments, servicer transfer problems. Most of the time, the foreclosure itself stays. The errors around it get corrected. And correcting those errors still moves the score in a meaningful way because the errors were compounding the damage of the original event.

In Q3 2025, ASAP Credit Repair USA reviewed 189 client files that included foreclosure entries. Of those, 74 contained at least one disputable error in the mortgage section. 52 of those disputes resulted in a correction or deletion of the specific erroneous element, whether that was a date correction, a duplicate removal, or a post-foreclosure late payment deletion.

The foreclosure itself remained in 48 of those 52 files. But the correction of the surrounding errors produced an average score improvement of 43 points, which is meaningful when a borrower is trying to qualify for a new mortgage or reduce interest rates on other credit products.

For a detailed look at the dispute process for negative mortgage entries, read: What Happens When You Miss a Mortgage Payment.

Real Foreclosure Cases We Have Worked On

Let me tell you about three situations that represent the patterns I see repeatedly.

Case One. A homeowner in Texas completed a loan modification in late 2022. Her servicer accepted the modification, restructured the payments, and she had been current for eighteen months when she came to us. Her credit report showed the account as a completed foreclosure. The modification had been approved before the foreclosure process finished, which meant the foreclosure never legally completed. Her servicer had simply failed to update the credit reporting. We documented the loan modification agreement and disputed with all three bureaus. The foreclosure notation was removed because the event it described never occurred in its reported form.

Case Two. A client's mortgage was transferred from his original lender to a new servicer in the middle of the foreclosure process. Both entities reported the account. His Experian report showed two separate foreclosure entries for the same original mortgage. One from the original lender, one from the new servicer. The duplicate report from the new servicer was removed after a single dispute round because the new servicer could not produce a separate original account agreement because there was not one. The two entries were the same debt.

Case Three. A client whose foreclosure completed in August 2021 had late payment updates continuing to post monthly through January 2023 from her servicer's automated reporting system. By the time she came to us, she had seventeen months of post-foreclosure late payment notations on a closed account. Each one was suppressing her score. We disputed all seventeen entries as inaccurate post-closing updates on a completed account. All seventeen were removed.

In none of these three cases did the foreclosure itself come off the report. But the corrections changed the credit picture significantly.

Common Mistakes Homeowners Make After a Foreclosure

The biggest mistake I see is doing nothing for years because someone told them the foreclosure would just "fall off" on its own and there is nothing to do in the meantime.

The second biggest mistake is disputing the foreclosure itself without evidence of a specific error. Filing a generic dispute on an accurate foreclosure does not work. The lender verifies it. The bureau keeps it. You have wasted 30 days. A dispute has to target a specific inaccuracy with supporting documentation.

The third mistake is assuming that all three bureaus show the same information. They do not. Your Equifax report may have the correct date of first delinquency. Your TransUnion report may show a date that was reset by a servicer transfer. You need to pull all three and analyze them separately.

The fourth mistake is paying the deficiency and expecting score improvement. Paying a deficiency removes a potential judgment threat. It does not remove the foreclosure from your report or change the score in any material way.

The fifth mistake is missing errors in the late payment section of the same account. The foreclosure notation and the individual monthly late payment notations from the buildup period and the post-foreclosure period are separate entries. Many people dispute the foreclosure and never look at the late payment entries from the same account. Both should be reviewed.

For more on how late payment disputes work in the context of a mortgage account, read our guide: Goodwill Letter to Remove Late Payments from Credit Report.

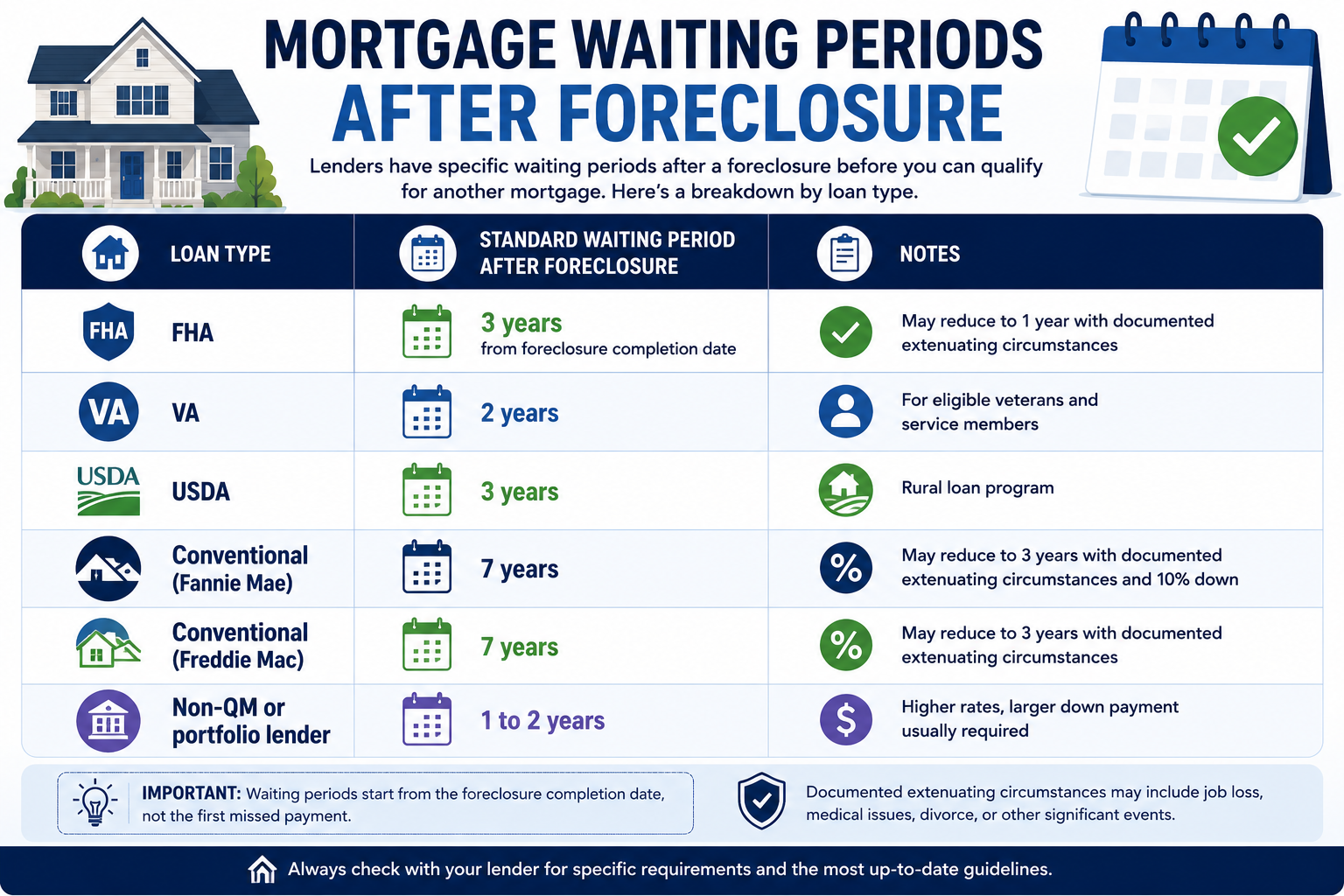

Can You Buy a House After a Foreclosure?

Yes. The waiting periods depend on the loan type and how your credit has recovered.

The waiting period clock starts at the foreclosure completion date, not the date of the first missed payment. This is the opposite of how the credit reporting clock works. The credit reporting clock starts at your first missed payment. The mortgage eligibility waiting period clock starts when the foreclosure completed.

A borrower who missed their first payment in March 2020 and whose foreclosure completed in September 2021 has two different clocks running. Their foreclosure should clear their credit report in March 2027 (seven years from first missed payment). But they became eligible for FHA financing in September 2024 (three years from foreclosure completion).

This is a detail that matters enormously for someone trying to plan a home purchase timeline. Most online articles do not explain the difference between these two clocks.

Planning to Buy a Home Again?

A foreclosure doesn't always mean you have to wait years before qualifying for another mortgage. Reviewing your credit report for reporting errors may improve your financial profile before you apply.

See If Your Credit Report Can Be ImprovedFor a full breakdown of mortgage eligibility timelines after credit events, read: How Quickly Can You Qualify for a Mortgage After Credit Issues.

How to Rebuild Your Credit After a Foreclosure

Rebuilding after a foreclosure is slower than rebuilding after collections or charge-offs because the event carries more weight in the scoring model. But the process is the same.

The first thing I tell every client who has a foreclosure is to start with what they can control today. The foreclosure happened. It is on the report. The score will not recover from it in 30 days. But the score can start moving within 60 to 90 days with the right actions.

First, audit the foreclosure entry for the errors I described and dispute anything that is inaccurate. Correcting those errors is the fastest path to a score improvement while the foreclosure itself remains.

Second, open a secured credit card with a $200 to $300 deposit, charge one small recurring bill to it, and pay it in full each month. Within 12 months that account starts to build positive payment history that the scoring model weighs against the foreclosure.

Third, keep every other account current without exception. A foreclosure combined with ongoing late payments on other accounts is nearly impossible to recover from within the seven-year window. A foreclosure with three years of spotless payment history afterward is manageable.

Fourth, monitor your credit report every 90 days. The foreclosure will age and its impact will weaken over time, particularly after the two-year mark. Watch for any new errors that post and dispute them immediately.

Fifth, avoid applying for multiple credit accounts simultaneously in the first 12 months after a foreclosure. Every hard inquiry costs points you cannot afford to lose during the recovery period.

According to Forbes Advisor's 2024 guide on rebuilding credit after major derogatory events, the most effective single action after a foreclosure is establishing at least one new credit account with a positive payment history, because the scoring model begins to reweight recent behavior over time even when the derogatory item remains present. (Forbes Advisor, How to Rebuild Credit After Foreclosure, 2024)

For a full guide on the score rebuilding sequence: How to Go From a 500 to a 700 Credit Score.

What Most People Miss About Foreclosure Reporting

The thing I want you to take away from this is that the foreclosure is often not the only problem on the report. It is usually the most visible problem. But the late payment entries from the same account, the potential duplicate from a servicer transfer, the post-foreclosure updates that should not be there, those add up to damage that does not belong to the foreclosure event itself.

I have seen files where the foreclosure was accurate and clearly documented, but the score was 55 points lower than it should have been because of three post-foreclosure late payment notations from an automated system that nobody caught.

Removing those three entries did not remove the foreclosure. But it moved the score from 573 to 631. That is the difference between being declined for an auto loan and being approved at a rate you can live with.

That is the real opportunity in foreclosure credit work. Not the magic removal that most people want. The systematic review of everything attached to that foreclosure entry and the correction of the inaccurate pieces.

If you want us to do that review for your file, the free three-bureau audit at ASAP Credit Repair USA is exactly where we start.

Also worth reading if you are navigating a mortgage default before foreclosure completes: What To Do If You Cannot Pay Your Mortgage.

Know What's Really Holding Your Credit Score Back.

A foreclosure is only one part of your credit profile. Incorrect late payments, duplicate mortgage reporting, outdated balances, and other errors can continue affecting your score long after the foreclosure itself. We'll review your credit report and explain what may be disputable.

Start My Free Credit ReviewFind out what's affecting your credit before applying for your next mortgage.

Frequently Asked Questions

Can a foreclosure be removed from my credit report?

Yes, under specific conditions. A foreclosure may qualify for removal or correction if it contains inaccurate data such as a wrong date of first delinquency, a duplicate entry from a mortgage servicer transfer, post-completion late payment notations, a balance that cannot be verified, or if the event is misclassified such as a short sale reported as a foreclosure. An accurate foreclosure that the lender can fully verify will remain for seven years from the date of first delinquency regardless of whether it was paid.

How long does a foreclosure stay on my credit report?

Seven years from the date of your first missed mortgage payment that led to the foreclosure, not from the date the foreclosure completed. If your first missed payment was in June 2019 and the foreclosure finished in November 2020, the entry should come off your report in June 2026.

Does paying off the foreclosure deficiency remove it?

No. Paying the deficiency balance updates the account status to paid but does not remove the foreclosure entry or shorten the seven-year reporting period. It may prevent a deficiency judgment in states that allow them, which is worth doing for legal reasons, but it does not produce a credit score benefit in most scoring models.

Can I dispute a foreclosure?

Yes, if you have evidence that a specific piece of data in the entry is wrong. A dispute based on an inaccuracy in the date, balance, account status, or duplicate reporting has a legitimate basis. A dispute that simply says "please remove this foreclosure" with no supporting evidence of an error will almost always be verified and remain.

Can I buy another house after foreclosure?

Yes. FHA financing is available three years after the foreclosure completion date. VA financing for eligible borrowers is available two years after. Conventional loans through Fannie Mae and Freddie Mac are available seven years after, or three years with documented extenuating circumstances. Non-QM lenders may approve loans one to two years after with larger down payments.

Does FHA allow a previous foreclosure?

Yes. FHA requires a three-year waiting period from the foreclosure completion date. With documented extenuating circumstances such as job loss, medical emergency, or death of a wage earner, the waiting period may be reduced to one year under HUD's Back to Work guidelines in some cases. The borrower must also demonstrate reestablished credit and financial recovery.

Can credit repair help with a foreclosure?

Credit repair helps when there are inaccuracies in how the foreclosure is being reported. It cannot remove an accurate, fully verifiable foreclosure. The value in professional credit repair for foreclosure cases is the systematic audit that identifies errors in dates, duplicate entries, post-completion notations, and balance inaccuracies that most consumers miss when reviewing their own reports.

Does a foreclosure affect your credit score forever?

No. The entry falls off the report after seven years from the date of first delinquency. Its impact on the score also weakens over time before the removal date. After two years with positive payment behavior on other accounts, most borrowers see the foreclosure's active score damage begin to diminish. After four to five years with a consistent positive history, many clients have recovered into the 660 to 700 range even while the foreclosure still appears.

Can a mortgage company report a foreclosure incorrectly?

Yes, and it happens more than people expect. Servicer transfers during the foreclosure period are a common source of errors. Automated reporting systems that continue posting late payment updates after an account closes produce errors. Loan modifications that prevented foreclosure completion being reported as completed foreclosures happen. Short sales classified as standard foreclosures happen. These are all patterns we see in real client files, and all of them are disputable under FCRA Section 611.

How to Remove Foreclosure From Credit Report Key Takeaways

An accurate foreclosure stays on your credit report for seven years from the first missed payment that led to it.

The clock starts at your first default, not the foreclosure sale date and not when a new servicer took over your loan.

Foreclosures can qualify for partial or full removal if they contain incorrect delinquency dates, duplicate account reporting from servicer transfers, inaccurate balances, late payments posting after the account closed, or information that cannot be verified under FCRA Section 611.

Paying off a foreclosure or completing one does not remove it. The status updates from unpaid to paid but the entry remains.

Reviewing all three bureau reports separately is the starting point because Equifax, Experian, and TransUnion often show different data for the same mortgage event.

Even if the foreclosure itself is accurate and stays, correcting the errors around it can raise a score meaningfully before the seven-year mark.