How to sign up for a credit repair service online. But choosing the right company before you sign up takes a little more thought. This guide walks you through how to sign up for a credit repair service, what to watch for in the contract, and what happens after you submit your information.

I own a credit repair company. One of the most unforgettable accounts I ever dealt with came from a client who paid two months of fees to a company that never filed a single dispute. She had no idea until she pulled her credit report herself.

The FTC enforces the Credit Repair Organizations Act (CROA), which bans companies from charging upfront fees before performing services. It also requires a written contract and gives you a 3-day right to cancel. Many people skip this step and pay the price. Knowing the law before you sign up protects you.

What Is a Credit Repair Service?

A credit repair service is a company that reviews your credit reports and disputes inaccurate or outdated items on your behalf.

Credit bureaus are required by law to investigate disputes within 30 days. Reputable services use that window to challenge errors, send goodwill letters to creditors, and flag items that should not appear on your report.

Credit repair companies cannot remove accurate negative information. Any company that promises otherwise is violating federal law. The FTC can shut them down, and you can sue them directly.

Most services charge between $60 and $150 per month, with some flat-rate options around $400, according to ConsumerAffairs credit repair statistics. Setup or first-work fees often match the monthly fee.

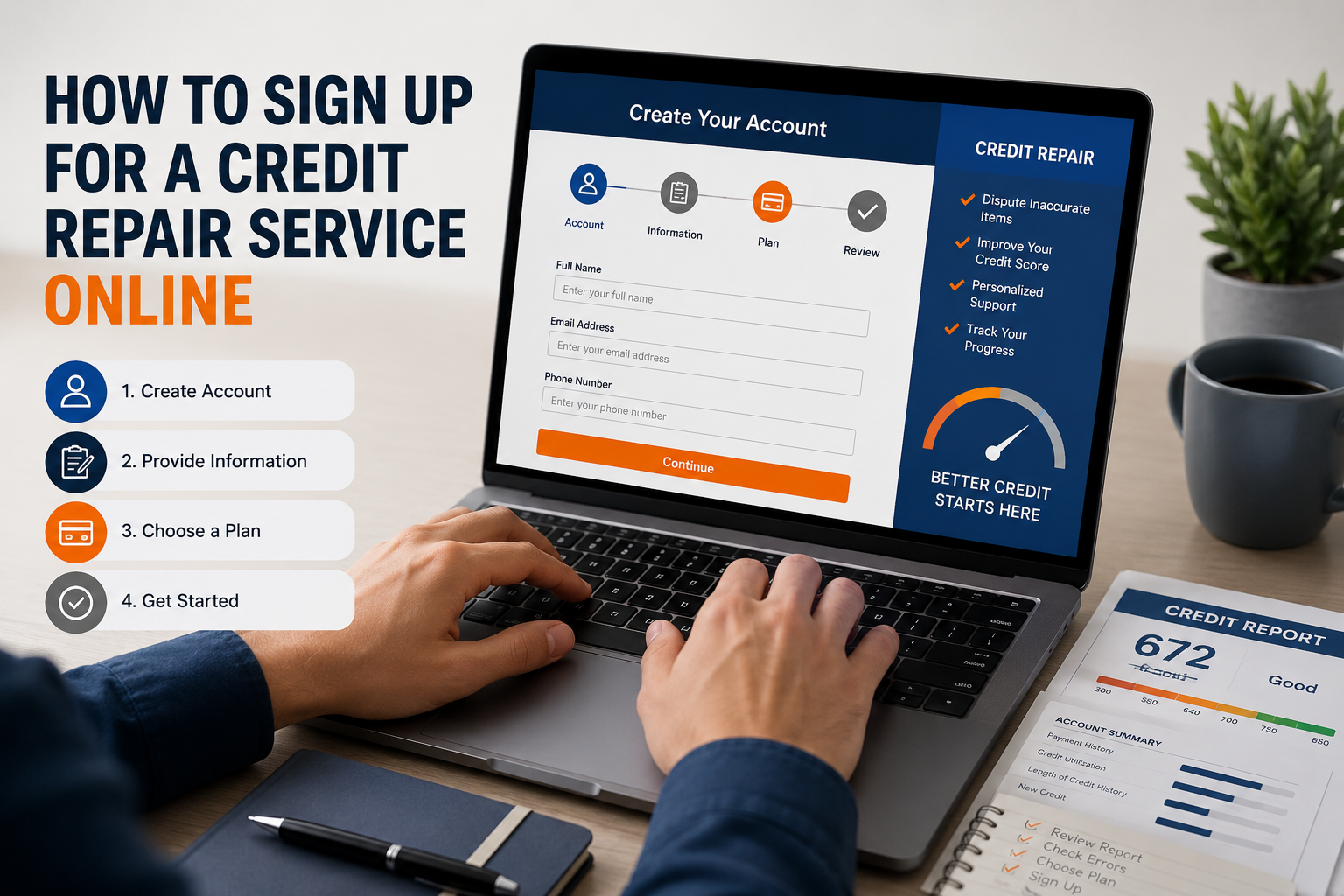

How to Sign Up for a Credit Repair Service Online

Once you choose a company, the actual signup takes a few minutes. Here is what the process looks like.

Go to the company's official website and click "Get Started" or "Sign Up."

Enter your name, email address, phone number, and basic details about your credit situation.

Select a service plan based on how much help you need.

Provide payment information. Legitimate companies do not charge until they have done work.

Submit the form and watch for a confirmation email with the next steps.

Most companies schedule a consultation within 24 to 48 hours of signup. That call is where they review your credit report and explain the specific items they will target.

You will also need to upload or provide some documents. Common requirements include a government-issued ID, proof of address, and sometimes a copy of your credit report if the company does not pull it directly.

How Do I Choose the Right Credit Repair Service?

Choosing the wrong company is the most expensive mistake you can make. Here is what to check before you sign.

Check for CROA compliance. The company must provide a written contract. It cannot charge you before doing work. It must give you a 3-day cancellation window. If any of those three things are missing, walk away.

Read recent reviews. Check Trustpilot, Google Reviews, and the Better Business Bureau. Look for patterns in complaints, not just the star rating. One bad review means nothing. Dozens of complaints about billing issues or no results are a red flag.

Look for transparent pricing. Legitimate companies list their fees clearly. The monthly fee, setup fee, and what each plan includes should all appear on their website without requiring a phone call.

Ask about their process. Find out what types of items they dispute, how they communicate updates, and whether they offer credit monitoring as part of the plan.

Avoid guaranteed results. No credit repair company can guarantee a specific score increase. Credit reporting involves three separate bureaus and multiple creditors, all with their own timelines. Any company promising 100-point jumps in 30 days is lying.

At our firm, we receive clients almost every month who signed with a company that made bold promises and delivered nothing. Last quarter alone, we saw six cases where clients paid two to four months of fees before realizing no disputes had been filed.

What Should I Look for in a Credit Repair Contract?

The contract is where most people make mistakes. Read it before you sign anything.

Here are the four things to verify in every contract:

Fees: The contract must state the exact amount you will pay and when. Monthly, flat-rate, or per-item pricing should all be spelled out. No legitimate company hides fees in fine print.

Services: The contract should list exactly what the company will do. Disputing errors, sending goodwill letters, and creditor interventions are all specific actions. Vague language like "work to improve your credit" means nothing enforceable.

Timeframe: Ask for a realistic estimate. Most clients see movement in 3 to 6 months. Complex situations with multiple collection accounts or judgments take longer.

Cancellation policy: You have the legal right to cancel within 3 days of signing. Beyond that, most reputable companies operate month to month with no long-term commitment required.

The CROA requires companies to give you a document explaining your rights before you sign. If the company skips this step, that is a federal violation.

What Happens After I Sign Up for a Credit Repair Service?

Here is what to expect once you are enrolled.

Credit report review: The company pulls your reports from all three bureaus. They look for errors, outdated items, duplicate accounts, and anything that violates the Fair Credit Reporting Act.

Dispute filing: For every item that qualifies, they send a formal dispute to the relevant bureau or creditor. Bureaus have 30 days to respond to each dispute.

Updates and reporting: Reputable companies send you progress reports. Monthly updates are standard. Some provide a dashboard where you can track disputes in real time.

Creditor outreach: For some items, the company contacts creditors directly. Goodwill letters ask creditors to remove accurate but old late payments as a gesture of goodwill. Pay-for-delete negotiations offer to settle a balance in exchange for removing the item.

You stay involved: Sign in to monitor your own credit through a free tool like Credit Karma or Experian. You will catch any new issues faster than the company will.

How Long Does a Credit Repair Service Take to Show Results?

Credit repair takes between 3 and 6 months for most cases. Some items resolve faster. Others take longer.

Credit bureaus have 30 days to investigate each dispute. If a bureau does not respond within that window, the item must be removed. If they verify the item, the company may escalate with additional documentation or a different dispute approach.

Complex files with bankruptcies, multiple collections, or judgment liens take longer. Simple errors, like a wrong account number or a payment marked late that was paid on time, often resolve in the first dispute cycle.

Patience matters. Using the service while also missing payments, maxing out cards, or applying for multiple lines of credit will slow or erase any progress the disputes create.

Can I Cancel a Credit Repair Service Anytime?

By law, you can cancel within 3 days of signing the contract with no penalty. After that, cancellation terms depend on the company.

Most reputable credit repair companies use month-to-month billing. You can stop at any time by contacting the company in writing. Check your contract for any notice requirements, such as canceling before the next billing cycle.

Companies that lock you into 6- or 12-month contracts with cancellation fees are worth avoiding. The CROA gives you the right to cancel, but only the first 3 days are federally protected; beyond that. Know your terms before you need to use them.

Do Credit Repair Services Guarantee Results?

No legitimate credit repair service guarantees a specific outcome. The CROA makes it illegal to promise results that the company cannot control.

Bureaus investigate disputes independently. Creditors respond on their own timelines. Some items come off quickly. Others get verified and stay. Reputable companies set realistic expectations and explain what they can and cannot influence.

If a company promises to raise your score by a set number of points in a set number of days, that promise is a red flag. Report it to the FTC at ftc.gov if you believe you were deceived.

Ready to Start Repairing Your Credit?

Don't wait months wondering what to do next. Get a professional review of your credit report, identify inaccurate items, and take the first step toward better credit today.

✓ Free Credit Analysis

✓ Personalized Dispute Strategy

✓ No Confusing Guesswork

See what's hurting your credit and learn your options before making any decisions.

Questions to Ask Before You Sign Up for a Credit Repair Service

These five questions will tell you most of what you need to know about any company.

What specific items will you dispute in my report?

How do you communicate progress, and how often?

What is the total monthly fee, and are there any other charges?

Do you operate month to month, or is there a minimum commitment?

What happens if a dispute comes back verified?

A company that answers these clearly and honestly is worth considering. A company that deflects, rushes you through the consultation, or avoids the cancellation question is not.

Credit repair done right takes time, proper documentation, and a company that follows the law. Take those three things seriously before you sign anything.