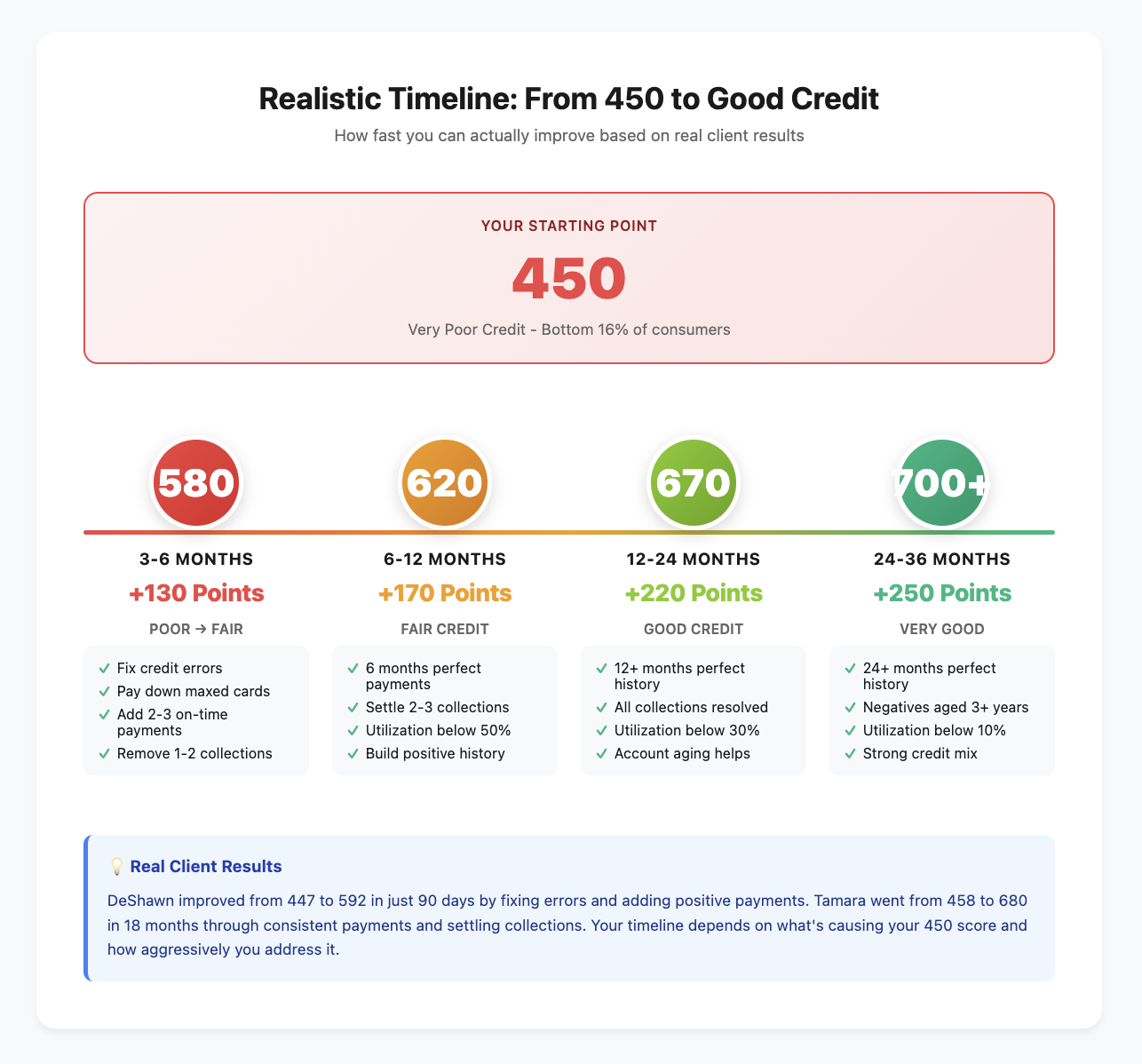

A 450 credit score can increase to 580-600 (Fair range) in 3-6 months with aggressive action, or reach 650-700 (Good range) in 12-24 months with consistent positive habits.

The timeline depends entirely on what's dragging your score down and how quickly you can fix those issues.

But here's what most people with a 450 credit score don't realize: you're not starting from scratch, you're recovering from specific problems. And different problems take different amounts of time to fix.

I'm writing this guide because I see clients with 450 credit scores every week at my credit repair company. Just last Tuesday, DeShawn walked into my office devastated. His 450 score cost him an apartment, the landlord rejected him outright. He thought he was stuck for years. Three months later, his score hit 592, and he's now in that apartment. The difference? He knew exactly what to fix and attacked it systematically.

Here's what you need to know about improving a 450 credit score:

- A 450 score puts you in the bottom 16% of all consumers

- The average person with a 450 score has past-due accounts, collections, or charge-offs

- Quick wins can boost your score 30-50 points in 30-90 days

- Getting to "Good" credit (670+) typically takes 18-36 months from 450

- The actions you take in the next 30 days determine how fast you improve

Let me show you exactly how fast you can realistically improve your 450 credit score, and what you need to do starting today.

What a 450 Credit Score Actually Means

A 450 credit score falls in the "Very Poor" range (300-579). This isn't just bad, it's in the bottom tier of credit scores. Only 16% of consumers have scores this low.

Here's what lenders see when they look at a 450 score:

You're a high-risk borrower. You've likely defaulted on debts, missed multiple payments, or had accounts sent to collections. According to data, 62% of consumers with scores under 579 will become seriously delinquent in the future.

What this costs you in real money:

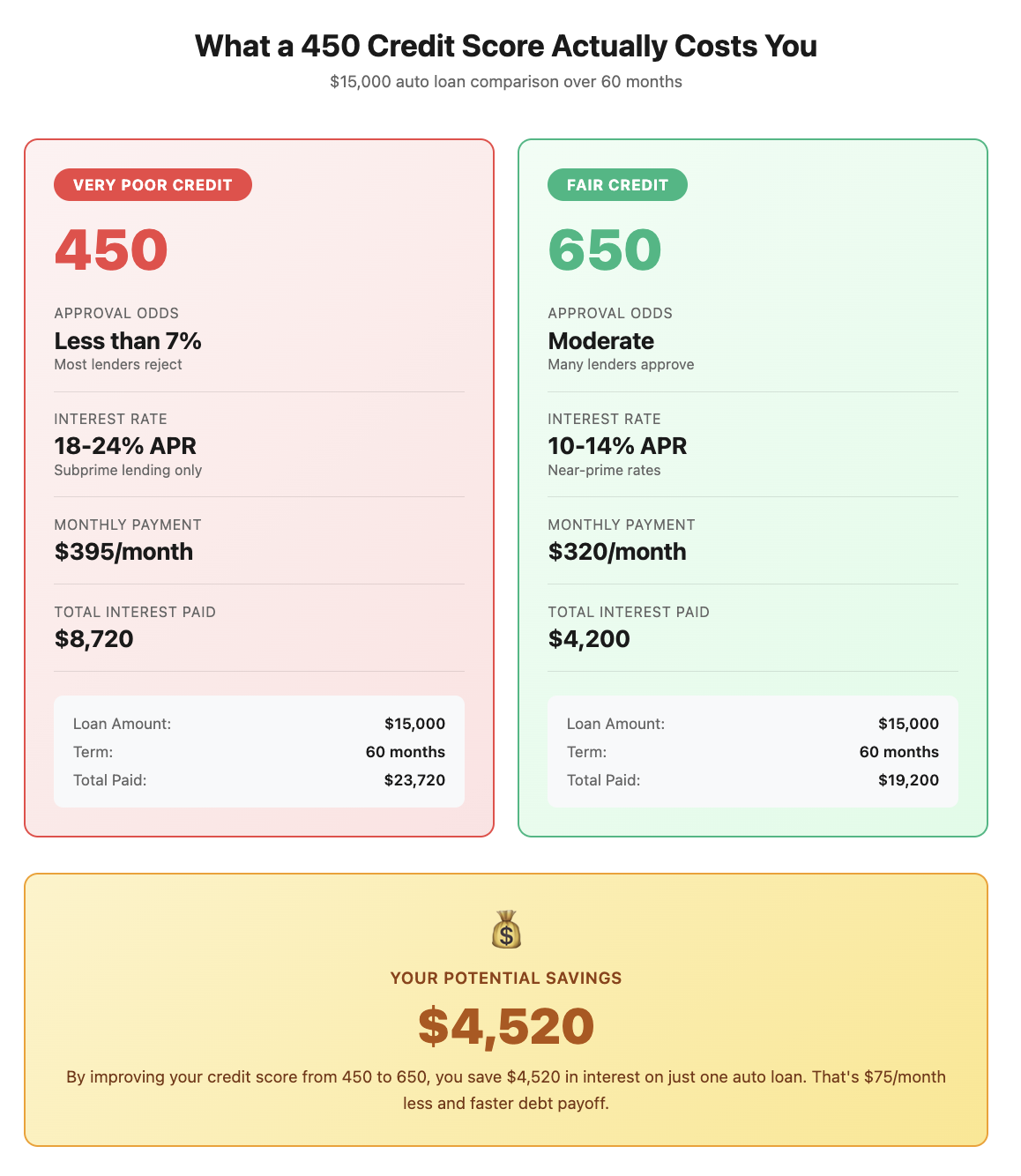

Let's say you need a $15,000 auto loan. Here's what you'd pay at different credit scores:

With 450 credit score:

- Approval odds: Less than 7% of auto loans go to this range

- Interest rate if approved: 18-24% APR

- Monthly payment: $395/month

- Total interest paid: $8,720 over 60 months

With 650 credit score:

- Approval odds: Moderate

- Interest rate: 10-14% APR

- Monthly payment: $320/month

- Total interest paid: $4,200 over 60 months

Difference: $4,520 saved by improving your score 200 points.

Why Your Score Is 450 (The Real Reasons)

Before you can improve your 450 credit score, you need to understand what caused it. I've reviewed hundreds of credit reports with scores in this range, and they almost always show these issues.

Late Payments and Delinquencies

Among consumers with a 450 credit score, 27% have gone 30+ days past due within the last 10 years. Many have multiple late payments or current past-due accounts.

What this looks like:

- Credit card payment 60 days late: -70 to -100 points

- Multiple accounts 30 days late: -50 to -90 points

- Currently, past due accounts: Ongoing damage every month

Payment history makes up 35% of your FICO score, the largest single factor.

Collections and Charge-Offs

If you stopped paying a debt entirely, the creditor eventually "charged it off" (wrote it off as a loss) or sent it to collections.

Impact on your 450 credit score:

- One collection account: -100 to -150 points

- One charge-off: -110 to -150 points

- Multiple collections: Each adds more damage

The average credit card debt for consumers with a 450 score is $1,517, often in collections.

High Credit Utilization

Among consumers with 450 scores, the average utilization rate exceeds 100%. This means they owe more than their credit limits through fees and interest.

Example:

- Credit card limit: $500

- Balance owed: $650 (130% utilization)

- Impact: Maximum negative effect on score

Credit utilization accounts for 30% of your FICO score.

Recent Credit Inquiries

Applying for multiple credit products in a short period signals financial distress.

What happens:

- Each hard inquiry: -5 to -10 points

- Multiple inquiries in 6 months: Looks desperate to lenders

- Impact lasts up to 2 years

Lack of Positive Credit History

Some 450 scores come from having almost no credit history combined with one or two negative marks.

Common scenario:

- 1-2 years of credit history total

- One charged-off account for $800

- No current positive accounts reporting

- Result: 450 score

How Fast You Can Actually Improve (Real Timelines)

Let me share real client stories that show exactly how fast, or slow, credit score improvement happens from 450.

Client Story 1: DeShawn - 450 to 592 in 90 Days

DeShawn, 28, came to me with a 447 credit score after his apartment application got rejected. He was furious and desperate.

His credit report showed:

- Three credit cards in collections (totaling $3,200)

- One charged-off personal loan ($1,800)

- Current credit card maxed out at $300 limit

- No positive payment history in 18 months

What we did:

Month 1:

- Disputed two collection accounts that had wrong balances (he proved he paid more than reported)

- Paid down his maxed-out card to $90 (30% utilization)

- Opened a secured credit card with $200 deposit

Month 2:

- One collection account removed due to inaccurate information

- Other collection updated with correct lower balance

- Made first on-time payment on secured card

- Made first on-time payment on existing card

Month 3:

- Second on-time payment on both cards

- Negotiated "pay for delete" on one collection ($800 paid, account removed)

- Utilization stayed below 30% on both cards

Results after 90 days:

- Score jumped from 447 to 592 (145-point increase)

- Got approved for the apartment

- Qualified for a secured credit card with better terms

Why it worked so fast: DeShawn had recent negatives that could be disputed or removed, and adding positive payment history immediately helped.

Client Story 2: Tamara - 458 to 680 in 18 Months

Tamara, 35, had a 458 score from a rough divorce where she stopped paying attention to bills.

Her credit report showed:

- Five accounts in collections (totaling $8,900)

- Two charge-offs (credit cards totaling $4,200)

- Mortgage current (never missed a payment)

- No revolving credit reporting positively

What we did:

Months 1-3:

- Opened two secured credit cards ($300 and $500 deposits)

- Made all payments on time

- Paid off smallest collection account ($450)

- Disputed inaccuracies on two accounts

Months 4-6:

- Continued perfect payment history on secured cards

- Negotiated settlements on two collections (paid $2,800 to settle $4,200)

- Score reached 520

Months 7-12:

- Six more months of perfect payments

- Paid off another collection account in full

- Increased credit limits on secured cards (showing positive payment pattern)

- Score reached 590

Months 13-18:

- Continued perfect payments (now 18 months of positive history)

- Graduated from secured cards to regular cards

- Old negatives aging off in impact

- Score reached 680

Results after 18 months:

- Score improved 222 points

- Qualified for a conventional mortgage refinance

- Saved $340/month on mortgage payment with better rate

Why it took longer: Tamara had more serious damage (charge-offs and multiple collections) that couldn't be quickly removed. But consistent positive behavior gradually outweighed old negatives.

Client Story 3: Marcus - 445 to 625 in 6 Months

Marcus, 41, had a 445 score from medical collections after a hospital stay without insurance.

His credit report showed:

- Six medical collections (totaling $12,400)

- Two late payments on auto loan (from 3 years ago)

- One active credit card in good standing

- Otherwise clean credit history

What we did:

Month 1:

- Requested itemized bills from hospital

- Found billing errors totaling $4,800

- Disputed all six collections with documentation

Month 2:

- Three collections removed due to errors

- Negotiated payment plan on remaining three ($7,600 total)

Month 3:

- Paid first collection in full ($2,100)

- Requested deletion (medical collections often delete after payment)

- Kept auto loan and credit card current

Month 4-6:

- Paid second collection ($2,800)

- Secured deletion agreements on both paid collections

- Maintained perfect payment history on all current accounts

- Final collection placed on payment plan

Results after 6 months:

- Score jumped from 445 to 625 (180 points)

- Five of six collections removed from report

- Qualified for apartment with no issues

Why it was moderately fast: Medical collections often contain errors and can be negotiated for deletion. Marcus's underlying credit behavior was good, his low score came from one specific problem.

The Realistic Timeline for Different Score Goals

Based on my experience with dozens of clients, here's how long it actually takes to reach different score levels from 450.

To Reach 550-580 (Poor to Fair): 3-6 Months

What you need to do:

- Fix credit report errors (immediate impact)

- Bring all current accounts current (stop being past due)

- Pay down maxed-out cards to below 75% utilization

- Add one or two on-time payments to your history

- Settle or pay one collection account if possible

Why this timeline:

- Simple errors get fixed in 30-60 days

- Payment history starts improving immediately when you go current

- Utilization drops as soon as you pay down balances

- These quick wins can boost you 50-100 points

Real example: DeShawn went from 447 to 592 in 90 days by fixing errors, paying down balances, and adding positive payments.

To Reach 600-650 (Fair Range): 6-12 Months

What you need to do:

- Everything from 550-580, plus:

- Six months of consistent on-time payments

- Settle or remove 2-3 collection accounts

- Get utilization below 50% on all cards

- Avoid new credit applications

- Build positive payment history on at least two accounts

Why this timeline:

- You need several months of positive behavior to outweigh negatives

- Settling collections takes time to negotiate and execute

- Credit bureaus need to see sustained good behavior, not just one-time fixes

Real example: Marcus went from 445 to 625 in 6 months by removing medical collections and maintaining perfect payments.

To Reach 670-700 (Good Range): 12-24 Months

What you need to do:

- Everything from 600-650, plus:

- 12-18 months of perfect payment history

- Resolve all collections and charge-offs

- Keep utilization below 30% consistently

- Age your accounts (older accounts help)

- Build credit mix (installment loan + revolving credit)

Why this timeline:

- Good credit requires sustained positive behavior over time

- Old negative marks need to age and lose impact

- You need substantial positive history to outweigh past problems

Real example: Tamara went from 458 to 680 in 18 months through consistent payments, settling collections, and letting time heal old wounds.

To Reach 700+ (Good to Very Good): 24-36 Months

What you need to do:

- Everything from 670-700, plus:

- 24+ months of perfect payment history

- All negative marks either removed or aged beyond 2-3 years

- Utilization below 10% (optimal)

- Mix of credit types with long history

- No recent hard inquiries

Why this timeline:

- Reaching "Very Good" credit from 450 requires time, there's no shortcut

- You need years of positive behavior to fully overcome a 450 starting point

- The most damaging items (charge-offs, collections) stay on reports for 7 years but lose impact over time

Your 30-Day Action Plan to Start Improving Today

You can't get to 700 overnight from 450. But you CAN make significant progress in the next 30 days that sets you up for long-term improvement.

Week 1: Get the Full Picture

Day 1-2: Pull all three credit reports

Go to AnnualCreditReport.com and get reports from Equifax, Experian, and TransUnion. Print them or save PDFs.

Day 3-4: Review every single item

Look for:

- Accounts you don't recognize (possible fraud)

- Wrong balances or payment histories

- Duplicate collections (same debt reported multiple times)

- Accounts that should have fallen off (over 7 years old)

Day 5-7: Create your hit list

Make a spreadsheet with:

- Every negative item (collections, charge-offs, late payments)

- The creditor name and amount

- Whether you recognize it

- Whether information looks inaccurate

- Priority order for addressing

Week 2: Fix Quick Wins

Day 8-10: Dispute obvious errors

File disputes with credit bureaus for:

- Accounts that aren't yours

- Wrong amounts or dates

- Duplicate entries

Send disputes online or via certified mail. The bureaus must investigate within 30 days.

Day 11-12: Check for outdated negatives

Negative items should fall off after 7 years (10 years for bankruptcy). If you have old negatives still reporting, dispute them as outdated.

Day 13-14: Request debt validation

For collections you don't recognize or seem wrong, send debt validation letters. Collectors must prove they own the debt and the amount is accurate.

Week 3: Start Building Positive History

Day 15-17: Bring current accounts current

If you have accounts currently past due, pay them current immediately. Being 30, 60, or 90 days late actively hurts your score every month.

Day 18-20: Apply for a secured credit card

If you don't have any positive accounts reporting, get a secured card:

- Requires $200-500 deposit

- Reports to all three bureaus

- Lets you build payment history

Recommended options:

- Discover it® Secured

- Capital One Platinum Secured

- OpenSky® Secured Visa®

Day 21: Make your first on-time payment

If you already have cards, pay them on time this month. Set up autopay for at least the minimum to never miss a payment.

Week 4: Address Collections Strategically

Day 22-24: Prioritize which collections to tackle first

Pay collections in this order:

- Medical collections with errors (easiest to remove)

- Small balances you can pay in full with "pay for delete"

- Recent collections (under 2 years old) hurting you most

- Old collections (over 4 years) that are aging out anyway

Day 25-27: Negotiate with collectors

Call or write to negotiate:

- Pay for delete (they remove it if you pay)

- Settlement for less than owed

- Payment plan to make it manageable

Get everything in writing before paying.

Day 28-30: Make your first payment

Pay at least one small collection account if possible. Even paying $200-500 can remove one negative item and boost your score.

Critical Mistakes That Slow Down Your Progress

After seeing hundreds of clients try to improve from 450, these mistakes keep appearing. Avoid them.

Mistake 1: Paying Collections Without Negotiating Deletion

The single biggest mistake I see: clients pay collections in full, thinking it will immediately help their score.

The reality: A paid collection still shows on your report as a collection. It changes from "unpaid collection" to "paid collection", but it's still negative.

What Marcus did wrong before finding me:

He paid a $1,200 collection in full without asking for deletion. The account updated to "paid" but stayed on his report. His score went up 8 points, not the 50+ he expected.

The right way:

Before paying ANY collection:

- Call the collector

- Say: "I can pay $X if you agree to delete this from my credit report"

- Get written confirmation of deletion agreement

- Pay only after you have the agreement in writing

- Follow up 30-60 days later to confirm deletion

Mistake 2: Closing Credit Card Accounts

Clients with 450 scores often have maxed-out or problematic cards. Their instinct: "Close it so I can't use it anymore!"

Why this hurts:

Closing cards reduces your available credit. If you have:

- Card 1: $300 balance / $500 limit

- Card 2: $0 balance / $800 limit

- Total utilization: $300 / $1,300 = 23%

Close Card 2:

- Card 1: $300 balance / $500 limit

- Total utilization: $300 / $500 = 60%

Your utilization jumps from 23% to 60%, dropping your score 20-40 points.

The right way:

Keep cards open but:

- Cut up the physical card if needed

- Remove saved payment info from online shopping

- Use it for one small recurring charge (Netflix) and set to autopay

- Keep the available credit helping your utilization

Mistake 3: Applying for Multiple Credit Products Quickly

Clients see their 450 score and think: "I need more credit to improve my score!" They apply for 3-5 cards in one month.

Why this hurts:

Each application is a hard inquiry:

- First inquiry: -5 points

- Second inquiry: -5 points

- Third inquiry: -5 points

- Plus: Looks desperate to lenders

You drop 15-20 points and look financially unstable.

The right way:

Apply for one secured card. Wait 6 months. Make perfect payments. Then consider a second card if needed.

Mistake 4: Ignoring Current Bills While Focusing on Old Debt

Clients get laser-focused on paying old collections. Meanwhile, they miss current credit card or loan payments.

Why this hurts:

A new 30-day late payment drops your score 60-100 points, more than paying off a 3-year-old collection might raise it.

The right way:

Priority order:

- Current bills (mortgage, rent, current credit cards, loans)

- Recent collections (under 2 years old)

- Old collections (over 3 years old, aging out anyway)

Never sacrifice current payments to pay old debt.

Mistake 5: Not Checking Results After Disputes

Clients file disputes and forget about them. The bureaus investigate, decide against them, and nothing changes.

Why this hurts:

If you don't follow up, errors stay on your report. You miss the chance to escalate or provide additional evidence.

The right way:

After filing disputes:

- Check your email daily for updates

- Log into credit bureau accounts weekly

- Follow up after 30 days if no response

- Re-dispute with additional documentation if denied

- Escalate to CFPB if bureaus ignore you

When to Get Professional Help

Most people with a 450 credit score can improve it themselves following this guide. But some situations need expert assistance.

Get professional help if:

- You have 5+ collection accounts: Negotiating multiple collectors gets complex. Credit repair companies can handle this for $50-150/month.

- You have bankruptcy or judgments: These require legal strategy beyond basic credit repair. Consult a consumer law attorney.

- Disputes keep getting rejected: If you've disputed errors 2-3 times and they're still not fixed, you need escalation help. Consumer attorneys work on contingency (you don't pay unless you win).

- You're facing mortgage application in 6 months: Time-sensitive situations benefit from aggressive professional help to maximize score improvement quickly.

- You suspect identity theft: If accounts on your report aren't yours, you need fraud resolution services, not basic credit repair.

The Bottom Line on Improving a 450 Credit Score

A 450 credit score can improve significantly in 3-6 months with the right actions, reaching Fair credit (580-669). Getting to Good credit (670-739) takes 12-24 months of consistent positive behavior.

The speed depends on:

- What's causing your 450 score (recent problems fix faster than old ones)

- How aggressively you act in the next 30 days

- Whether you avoid new mistakes while fixing old ones

- How much money you can allocate to settling collections

Your action plan:

- Pull all three credit reports this week

- Identify errors and dispute them immediately

- Bring any past-due accounts current

- Open a secured credit card to start building positive history

- Negotiate "pay for delete" on collections before paying

- Make every payment on time for the next 6 months

- Keep utilization below 30% (ideally below 10%)

Most important: Start today. Every day you wait is another day your 450 score is costing you money, denying you housing, and limiting your options.

A client waited two years before coming to me. In those two years, he was denied three apartments, couldn't get a car loan, and paid premium prices for everything. When he finally took action, his score jumped 145 points in 90 days.

Don't wait two years. Pull your credit reports right now. Your 450 credit score doesn't have to define your financial future, but only if you start fixing it today.