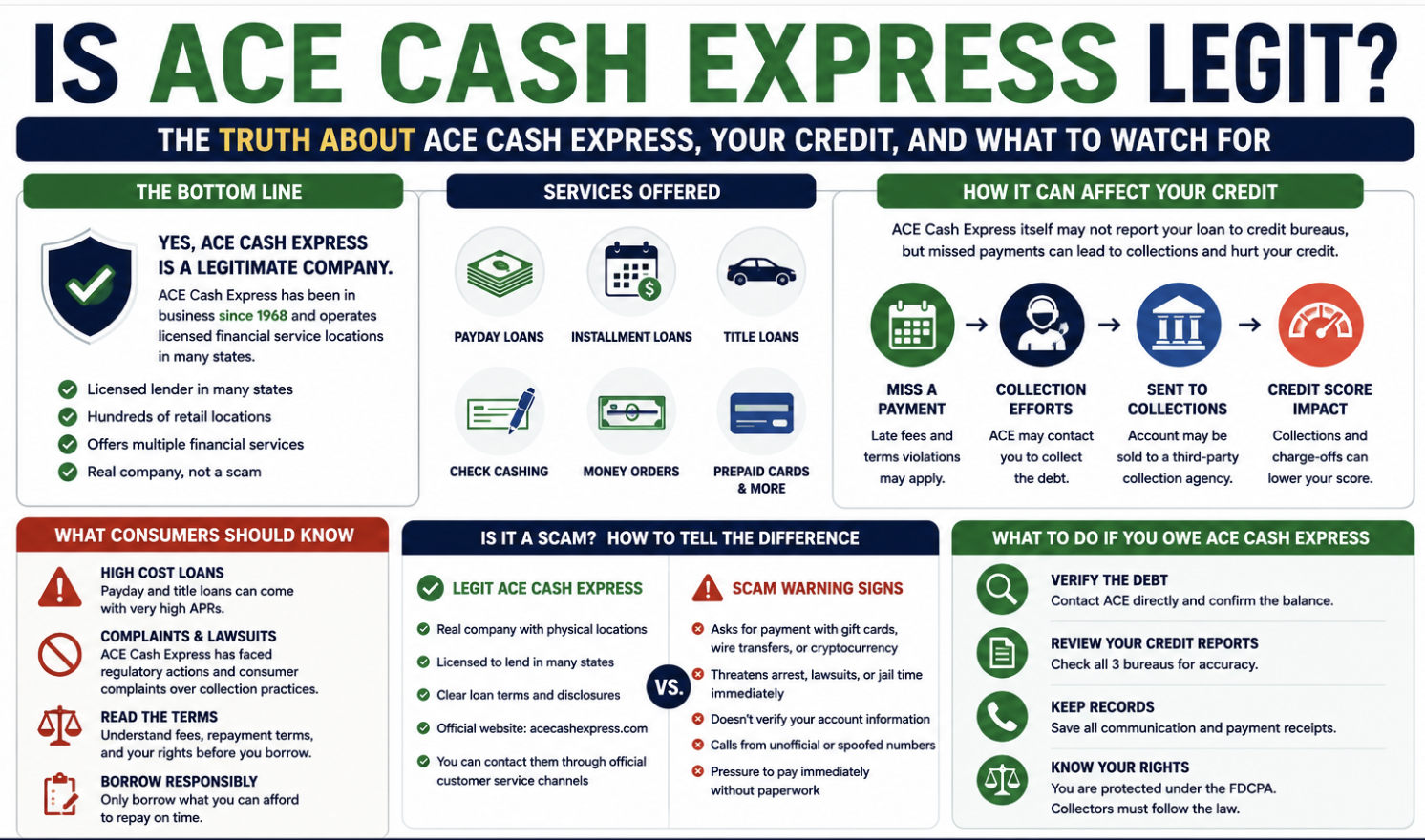

TL;DR: ACE Cash Express is a legitimate, licensed financial services company that has operated since 1968. It is not a scam. It offers payday loans, installment loans, title loans, check cashing, and related services at locations across 21 states and online in 7 states. However, being legitimate does not mean borrowing from ACE is without risk. A default, however, can result in the debt being sold to a third-party collection agency that will report it, potentially dropping your score by 50 to 100 points and staying on your report for seven years. Scammers frequently impersonate ACE Cash Express. Before paying any collector claiming to represent ACE, verify the account through ACE's official customer service.

Is ACE Cash Express Legit or a Scam?

ACE Cash Express is a legitimate company. It is not a scam.

The company has operated since 1968 and is headquartered in Irving, Texas. In 2019, ACE Cash Express changed its corporate parent name to Populus Financial Group Inc. while retaining the ACE Cash Express brand for its financial services operations. The company is licensed in every state where it operates, holds membership in INFiN (a national trade association for financial service centers), and maintains physical retail locations in 21 states plus online lending in 7 states.

Being legitimate and being without risk are not the same thing. ACE Cash Express has been the subject of two separate CFPB enforcement actions involving its lending and collection practices. Both are documented in public government records and are covered in detail in this article.

Borrowers should review those records alongside the loan terms before deciding to borrow.

Scammers also impersonate ACE Cash Express. Receiving a collection call or letter claiming to be from ACE does not confirm the contact is real. The section below on how to tell a real ACE call from a scam covers exactly what to verify before paying anything to anyone claiming to represent the company.

What Services Does ACE Cash Express Offer?

ACE Cash Express offers the following financial products and services, with availability varying by state:

Payday loans — Short-term loans typically due on the borrower's next payday. Amounts range from $100 to $500 depending on state. APRs range from 91% to 630% depending on state and loan term, per ACE's own disclosures as cited in 2026 third-party review data. ACE does not report payday loan payments to the three major credit bureaus.

Installment loans — Loans repaid in equal scheduled payments over a longer period. Available online in Missouri, Ohio, Florida, Texas, and other states. Loan amounts up to $2,500 depending on state. ACE does not report installment loan payments to the three major credit bureaus either, per the company's own FAQ pages.

Title loans — Loans that use a vehicle as collateral, available at select store locations. Failure to repay can result in vehicle repossession.

Check cashing — Available in-store. Fees range from 2% to 6% for personal checks and 2% for government checks, with a $5 minimum fee.

Money orders, bill payment, wire transfers, and prepaid debit cards — Additional services available at select locations.

Credit check policy: ACE does not run a hard inquiry with Equifax, Experian, or TransUnion when you apply. Instead, it uses FactorTrust, a non-traditional consumer reporting agency acquired by TransUnion in 2017. An inquiry with FactorTrust may affect your profile with that agency but will not affect your FICO score, per ACE's own published FAQ.

Does ACE Cash Express Report to Credit Bureaus?

This is the most important question for most borrowers and the one most articles get wrong or skip.

The direct answer: ACE does not report loan activity to Equifax, Experian, or TransUnion while your account is current.

ACE states this explicitly on its own website. From ACE's payday loan requirements page: "ACE does not report the loan amount or any associated activity to traditional credit bureaus." The same language appears on ACE's installment loan requirements page.

This means two things. First, paying your ACE loan on time will not help build your credit history with the three major bureaus.

Second, borrowing from ACE will not raise your credit utilization ratio or appear as a new account on your report while the loan is active and in good standing.

What does happen to your credit if you default on an ACE loan is a different story.

According to BBB complaint records reviewed for this article, when an ACE borrower defaults and internal collection efforts do not result in payment, ACE sells the account to a third-party debt buyer. A February 2025 BBB response from ACE's Senior Compliance Analyst confirmed this directly: "After ACE collection activities did not result in payment or payment arrangements on the outstanding balance, the account was sold to [a third-party debt buyer] with a balance of [amount] at the time of sale."

Once a third-party debt buyer purchases the account, they report it to the credit bureaus as a collection account. A collection account can drop a credit score by 50 to 100 points depending on the overall credit profile, and it stays on the report for seven years from the date of first delinquency with ACE, not from the date it was sold to the debt buyer.

For more on how payday loan defaults reach credit bureaus, read our full guide: Can Payday Loans Hurt Your Credit Score?

What Happens If You Miss an ACE Cash Express Payment?

The default timeline follows a pattern common to payday and installment lenders.

Based on ACE's own published materials, BBB complaint records, and third-party lender review data from 2025 and 2026, the sequence is:

Day 1 to 3: Payment is missed. ACE's collections department begins internal outreach. Per BadCredit.org's ACE review, payments that are more than three days late are turned over to ACE's internal Collections Department, which attempts to reschedule the payment. A return fee of $10 to $30 applies if a bank debit fails due to insufficient funds.

Days 4 through 30: ACE continues internal collection calls and attempts to debit the connected bank account. ACE's 2022 CFPB lawsuit alleged the company made multiple unauthorized debit attempts beyond what the loan agreement authorized. The 2022 case was voluntarily dismissed in April 2025, so that specific allegation was not adjudicated. Borrowers who see unexpected debit attempts should contact their bank to stop the authorization.

Days 30 to 90: If internal collection does not produce payment or a payment arrangement, ACE begins the process of referring or selling the account. The timing varies by state and loan type.

After 90 days: Account is sold to a third-party debt buyer. From the date of sale, the original ACE entry and the new collection account may both appear on the credit report. ACE's entry updates to show a charged-off or sold status. The debt buyer's collection entry is separate and begins reporting actively. Both entries harm the score and both remain for seven years from the original date of first delinquency with ACE.

Potential legal action: ACE can pursue a lawsuit in state court if the balance justifies it and the debt is within the applicable statute of limitations. The statute of limitations for contract debt varies by state from 3 to 6 years. Borrowers who receive a court summons must respond within the deadline on the summons. Not responding produces a default judgment that enables wage garnishment and bank levy in most states.

For a full breakdown of how collection accounts affect credit and what to do when a payday loan default reaches a third-party collector, read: Should I Pay Off a Debt in Collections, or Is It Better to Dispute It?

How to Tell a Real ACE Cash Express Call From a Scam

ACE Cash Express warns consumers on its own website that scammers impersonate legitimate financial companies including ACE to collect fake debts. This is one of the most searched angles related to ACE and one of the most dangerous for consumers.

Scammers who impersonate ACE and other lenders typically exhibit these patterns:

Demands for gift cards or wire transfers. ACE Cash Express does not accept gift cards or wire transfers as loan repayment. Any collector demanding payment in gift card numbers or a wire transfer is a scam.

Arrest threats. Debt collectors are prohibited from threatening arrest under the Fair Debt Collection Practices Act. A legitimate ACE collector cannot legally tell you that you will be arrested. This is a scammer script.

Immediate payment demands without account verification. A legitimate collector will provide a verifiable account number, a balance that matches ACE's records, and contact information you can independently verify. A scammer will push for immediate payment before you can verify anything.

Claims of no record in ACE's system when you call to verify. If you call ACE's official line at 866-ACE-CASH and they have no record of the account a collector described, the collector is not representing ACE.

Cannot identify the original loan date or amount. A legitimate ACE account has a specific origination date, loan amount, and account number that ACE can verify when you call. A scammer typically cannot provide these details accurately because they do not have access to ACE's actual records.

What to do when you receive a collection call claiming to be from ACE:

Write down the caller's name, the company name they give, the phone number they called from, and the account number and balance they reference. Do not provide payment information on the call. Call ACE directly and ask them to verify the account.

If ACE confirms the account, ask them to provide the third-party collector's name and contact information so you can verify independently. If ACE has no record of the account, report the call to the FTC at reportfraud.ftc.gov and to the CFPB at consumerfinance.gov/complaint.

Can ACE Cash Express Hurt Your Credit Score?

The answer is no while payments are current, and yes after a default.

Before default: ACE does not report to Equifax, Experian, or TransUnion. Your on-time payments do not appear. Your score is neither helped nor hurt by active loan payments. The application uses FactorTrust, not the three major bureaus, so the application inquiry does not affect your FICO score.

After default: The debt is sold to a third-party collection agency. The collection agency reports to the credit bureaus. A collection account causes an average drop of 50 to 100 points depending on the credit profile, per data from ASAP Credit Repair USA client files. The entry stays on the report for seven years from the date of first delinquency with ACE. The score impact is strongest in the first two years and weakens over time as positive account history accumulates on other accounts.

The compounding problem with payday defaults: ACE limits borrowers to one open loan at a time. Borrowers who roll over or repeatedly take new payday loans from ACE after repaying the prior one may create a pattern that, while not directly on the credit report, shows up in bank statements. Mortgage lenders review 60 to 90 days of bank statements during underwriting. Multiple payday loan transactions in a short period signal financial instability to a mortgage underwriter even if no collection entry appears on the credit report.

The CFPB's 2014 research found that 80% of payday loans are renewed or followed by another loan within 14 days. This is the cycle both CFPB enforcement actions alleged ACE was designed to perpetuate.

For more on how collections from payday loans affect credit and what options exist: Does Paying Off Collections Improve Your Credit Score?

Does ACE Cash Express Send Accounts to Collections?

Yes. Based on ACE's own BBB response documentation and consumer complaint records, the confirmed sequence is:

ACE conducts internal collection first. If internal collection does not produce payment or a payment arrangement within approximately 90 days, the account is sold to a third-party debt buyer. The BBB complaint response quoted earlier in this article confirms this directly from ACE's compliance department.

The third-party debt buyer then reports the account to Equifax, Experian, and TransUnion as a collection account. The original ACE entry on the credit report (which was not previously reporting) may also appear as a charged-off or sold account, depending on how ACE's reporting practices work with the three bureaus at that stage.

Borrowers who receive contact from a third-party collector claiming to own an ACE Cash Express debt should send a written debt validation request within 30 days of first contact. Under FDCPA Section 1692g, the collector must stop collection activity until they validate the debt. Debt buyers who purchase ACE portfolio accounts sometimes have incomplete documentation, particularly for older accounts that changed hands multiple times.

For a step-by-step guide on what to do when a payday loan debt enters third-party collections: How to Handle Accounts Marked Paid Collection on Your Credit Report

Can ACE Cash Express Sue You?

ACE Cash Express can sue borrowers in state court for unpaid debts. ACE is a licensed lender with a signed loan agreement, which is a contract that can be enforced in court.

Whether ACE or a third-party debt buyer who purchased the account will sue depends on several factors:

The balance. Small balances, particularly under $500, are less likely to generate a lawsuit because the cost of filing and pursuing the case may exceed the recovery.

The state statute of limitations. Once a debt is past the statute of limitations for contract debt in your state, a lawsuit is still possible but the debtor can raise the statute of limitations as an affirmative defense, which typically results in dismissal. Statutes of limitations for written contracts range from 3 years in states like Texas to 6 years in states like New York.

Who owns the debt. If ACE sold the account to a third-party debt buyer, that buyer decides whether to sue, not ACE. Third-party debt buyers are more variable in their litigation behavior than original lenders.

If you receive a court summons from ACE Cash Express or a debt buyer claiming to own an ACE account, respond in writing to the court before the deadline on the summons. Most states give 14 to 30 days from the date of service to file a written Answer. Not responding results in a default judgment, which enables wage garnishment in most states (Texas restricts wage garnishment for private consumer debts under its state constitution) and bank account levies.

How Does an ACE Cash Express Default Affect Mortgage Qualification?

This section does not appear in most other ACE Cash Express coverage, and it is the section that matters most for anyone planning a home purchase.

During active loan repayment: ACE does not report to the three major bureaus, so an active ACE loan does not appear on the credit report a mortgage lender pulls. However, bank statements are reviewed during mortgage underwriting, and multiple payday loan withdrawals or deposits within the review period can signal a pattern of financial instability to an underwriter.

After a default that reaches collections: A collection entry from a third-party debt buyer who purchased an ACE account follows the same mortgage underwriting rules as any other collection. FHA does not require payoff of non-medical collections below $2,000 total. Conventional loans under automated underwriting may not require payoff. USDA requires all collections to be paid before closing. Manual underwriting, which is used when automated underwriting systems refer the file, frequently requires collection payoff regardless of program minimums.

The key distinction: A borrower with a $500 ACE Cash Express collection on their report is in a better position than a borrower with a $500 collection that remains unpaid and is currently being pursued. The action step for anyone planning a mortgage application who has an ACE default in collections is to audit the collection entry, negotiate pay-for-delete before paying, and if pay-for-delete is unavailable, pay with a zero-balance letter and settlement documentation before applying.

Common Mistakes Borrowers Make With ACE Cash Express Accounts

Paying a scammer who claims to represent ACE. The most financially damaging mistake. Always verify through ACE's official line before paying any collector.

Assuming the ACE loan will not affect credit because ACE does not report. ACE does not report while the account is current. But a default that reaches a third-party collector does reach the credit bureaus. The distinction matters.

Borrowing repeatedly to cover prior ACE loans. Each new payday loan from ACE costs a fresh fee at the same APR. The cycle compounds the total cost without resolving the underlying cash flow shortage. The CFPB's 2022 lawsuit alleged ACE concealed free repayment plans specifically to prevent borrowers from exiting the cycle. That case was dismissed in April 2025 but the pattern it described was independently documented in CFPB complaint data.

Ignoring a collection notice from a third-party debt buyer. A notice from a third-party collector claiming to own an ACE debt is a time-sensitive communication. The 30-day window to request debt validation starts from first contact. Missing it removes the automatic collection-stop protection under FDCPA Section 1692g.

Paying the collection before negotiating deletion. Once payment is made, leverage disappears. Negotiating a pay-for-delete agreement before paying is the correct sequence.

Has an ACE Cash Express Collection Appeared on Your Credit Report?

Not every collection account is reported correctly. Before assuming you have to pay, review your credit report for inaccurate balances, duplicate accounts, or reporting errors that may affect your credit score.

Review My Credit Report Learn MoreKnow what's affecting your credit before negotiating with any collection agency.

For a step-by-step approach: Can Payday Loans Hurt Your Credit Score?

What to Do Before Paying Any ACE Cash Express Collection

Before making any payment to ACE Cash Express directly or to a collector claiming to own an ACE debt, work through this sequence.

Verify the account through ACE's official line. Call 866-223-2274 and confirm the account number, balance, and current status. If the account was sold, ask for the name of the purchaser so you can verify the collector's identity.

Pull all three bureau reports. Go to AnnualCreditReport.com. Search for any ACE Cash Express entry or any collection entry from a company you do not recognize that may have purchased an ACE account. Note the date of first delinquency, the reported balance, and the account status.

Send a written debt validation request if a collector has contacted you. Send by certified mail within 30 days of first contact. Request the original signed loan agreement, complete payment history, documentation of the debt buyer's chain of ownership, and the collector's license to collect in your state.

Check the date of first delinquency. If the original delinquency is more than seven years ago, the collection entry should already be off your report. File a written removal request with each bureau if it is still appearing.

Negotiate pay-for-delete before paying. If the debt is valid and within the statute of limitations, offer a settlement with a written pay-for-delete commitment before sending any money.

Before You Pay ACE Cash Express, Know How It Could Affect Your Credit.

If your account has been sent to collections or appears on your credit report, paying may not automatically improve your credit score. We'll review your report and help you understand the best next step before you make a payment.

Get My Free Credit Review →✓ No obligation ✓ Review collection accounts ✓ Personalized recommendations

More About ACE Cash Express

Is ACE Cash Express a legitimate company?

Yes. ACE Cash Express is a legitimate financial services company that has operated since 1968. It is licensed in every state where it provides services and offers payday loans, installment loans, title loans, check cashing, and related products. Being legitimate does not mean it is without risk. The company has faced two CFPB enforcement actions. Borrowers should read loan terms carefully before borrowing.

Is ACE Cash Express a scam?

No. ACE Cash Express itself is not a scam. However, scammers frequently impersonate ACE Cash Express to collect fake debts. If you receive a call demanding gift cards, wire transfers, or threatening arrest in ACE's name, that is a scam. Verify all collection contacts through ACE's official line at 866-223-2274 before paying anything.

Does ACE Cash Express report to credit bureaus?

ACE does not report loan activity to Equifax, Experian, or TransUnion while your account is current. On-time payments do not appear on your credit report and do not build your credit history. If an account defaults and is sold to a third-party debt buyer, that buyer reports the collection to the three bureaus. The collection can drop your score by 50 to 100 points and stays on the report for seven years.

Can ACE Cash Express hurt my credit score?

Not while payments are current. After a default that reaches a third-party collection agency, yes. The collection the debt buyer reports to the bureaus is what damages the score, not the original ACE loan activity.

Can ACE Cash Express sue me?

Yes, if the debt is within your state's statute of limitations for contract debt. If a third-party debt buyer purchased the account, that buyer decides whether to sue. Always respond to a court summons in writing before the deadline. Not responding produces a default judgment enabling collection enforcement.

Can ACE Cash Express garnish my wages?

Only after obtaining a court judgment through a lawsuit. ACE or a debt buyer must sue you, win or obtain a default judgment, and then seek a separate garnishment order from the court. Texas prohibits wage garnishment for private consumer debts under its state constitution. Other states permit it with valid judgments.

How do I remove an ACE collection from my credit report?

If the collection contains errors, file a written dispute with each bureau under FCRA Section 611. If the date of first delinquency has been re-aged or is incorrect, that is a disputable error. If the seven-year reporting window has closed, file a removal request. If the debt is accurate, negotiate a pay-for-delete agreement before paying.

For the full dispute process: How to Handle Accounts Marked Paid Collection on Your Credit Report

What is ACE's corporate parent company?

In 2019, ACE Cash Express changed its corporate parent name to Populus Financial Group Inc. The ACE Cash Express brand continues to operate under that parent. The company is headquartered at 300 E. John Carpenter Fwy, Suite 900, Irving, Texas 75062.

Is ACE Cash Express available in my state?

Online loans are available in Delaware, Florida, Louisiana, Missouri, Ohio, Oklahoma, and Texas as of 2026. In-store services are available in 21 states and the District of Columbia. ACE does not operate in all 50 states and is not available to military personnel because its APRs exceed the 36% cap set by the Military Lending Act.

One Loan Shouldn't Cost You Future Financial Opportunities.

Whether you're dealing with ACE Cash Express, another payday lender, or a collection agency, understanding what's on your credit report today can help you qualify for better financing tomorrow.

Start My Free Credit Review →✓ Identify reporting issues ✓ Prepare for future loans ✓ Understand your options

Key Takeaways

ACE Cash Express is a legitimate, licensed financial services company, not a scam, but borrowers should carefully review loan terms before accepting a loan.

Missing payments can lead to late fees, collections, and potential credit reporting, depending on the loan type and state regulations.

Scammers sometimes impersonate ACE Cash Express, so always verify any collection call or payment request before sharing personal or financial information.

Before paying a collection or defaulted payday loan, review your credit reports and confirm that the debt is accurate and being reported correctly.

Payday loan defaults can affect future borrowing, including mortgage applications, if they result in collections or other negative credit reporting.

Legal Disclaimer: ASAP Credit Repair USA is not affiliated with, endorsed by, or in any way connected to ACE Cash Express or Populus Financial Group, Inc. All information about ACE Cash Express in this article is drawn entirely from publicly available sources including government enforcement records, the company's own published statements, consumer review platforms, and third-party lender review databases. This article is provided for educational purposes only and does not constitute legal or financial advice. All company names, logos, and trademarks referenced are the property of their respective owners. Consult a licensed attorney or financial advisor for guidance specific to your situation.