Kikoff became popular for one simple reason:

A lot of people want to build credit without taking on real debt.

That is where Kikoff feels different from traditional credit cards or loans.

Most credit-building products require:

security deposits

hard inquiries

high interest

large monthly payments

risky spending habits

Kikoff tries to remove most of that friction.

The platform focuses on low-cost credit building through a small revolving account designed mainly to help payment history and utilization reporting. That makes it popular with beginners, people rebuilding after collections, and borrowers trying to improve their scores before applying for apartments, car loans, or credit cards.

I’ve noticed many people discover Kikoff after getting denied somewhere else.

Usually, they are looking for:

an easy approval option

a low monthly payment

a way to start reporting positive activity

something safer than opening another high-interest credit card

That is really the lane Kikoff occupies.

Not rewards chasing.

Not borrowing large amounts of money.

Mostly simple credit-building behavior designed to strengthen a thin or damaged profile over time.

What Is Kikoff? How This Low-Cost Credit Builder Works

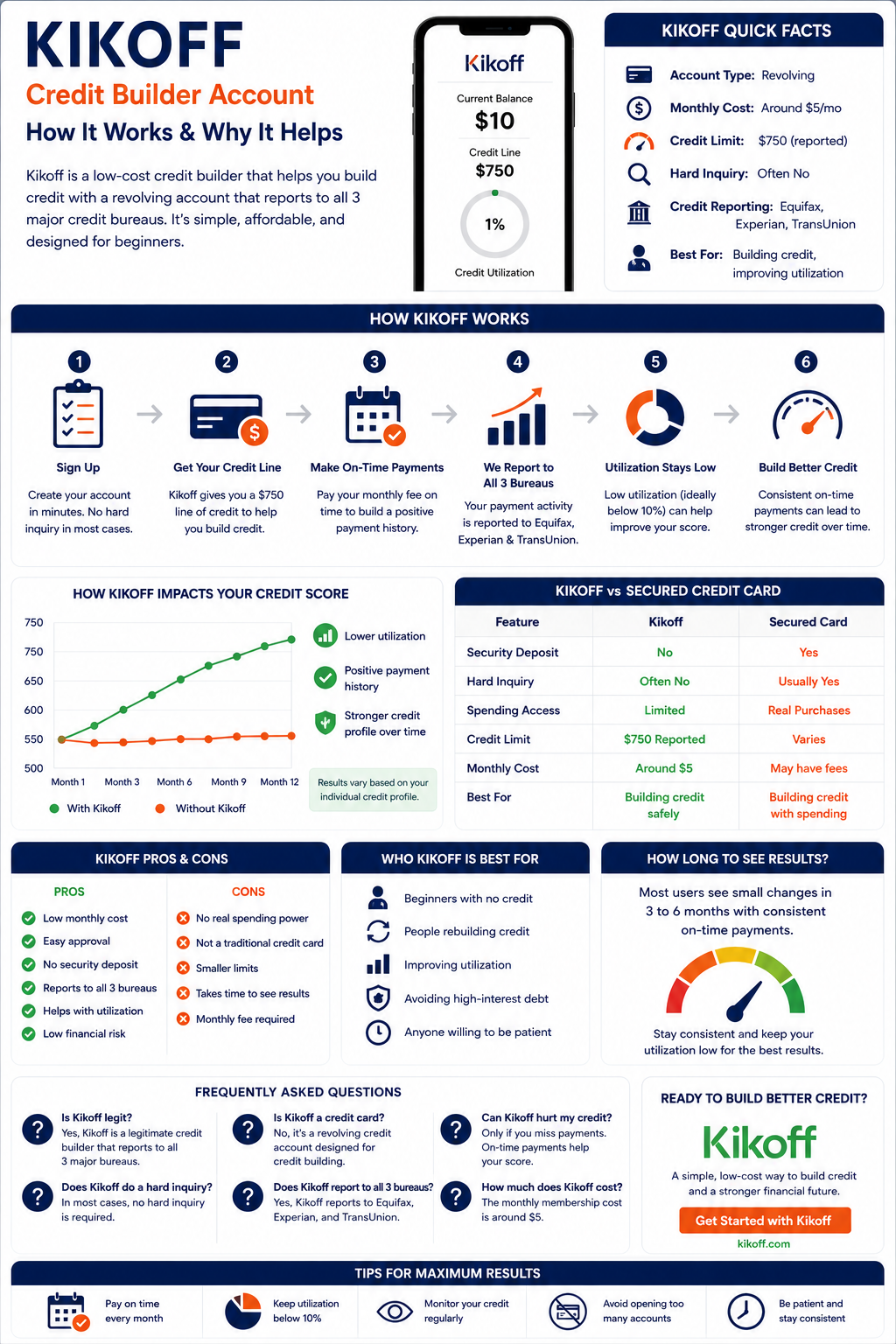

Kikoff is a low-cost credit builder platform that helps users build credit through a revolving account that reports payment activity to the major credit bureaus. Many users choose Kikoff because approval is easier, monthly costs are low, and no large security deposit is required.

What Is Kikoff

Kikoff is a fintech app that helps people build credit through a monthly subscription. You get a revolving credit line. You spend a small amount in Kikoff's online store each month. You pay it back on time. Kikoff reports your payment to Equifax and Experian. That consistent positive history builds your score over time. No deposit. No hard inquiry. No interest.

Kikoff was founded in 2021 and operates as Kikoff Inc. (NMLS ID 1930930). The model is different from traditional credit building tools.

A secured credit card requires a cash deposit. A credit builder loan locks your money in a savings account. Kikoff does neither. You pay a flat monthly fee, get access to a credit line, make a small purchase in their store, and pay it off. The entire process costs $5 and takes about 10 minutes to set up.

The platform is SOC 2 certified with end-to-end encryption. It is a real credit reporting account , not a workaround or loophole. The account reports as a revolving credit line on your Equifax and Experian reports the same way any credit card would.

How Kikoff Works

Kikoff does not run a hard pull when you apply. Your score does not drop from joining. Approval is instant. You provide basic personal information and a payment method for the monthly subscription fee.

The Basic plan gives you a $750 revolving credit line. Premium gives $2,500. Ultimate gives $3,500. This credit line is used only in Kikoff's online store , you cannot take it to Amazon or a regular retailer. The store sells financial literacy products and digital content.

You spend a small amount from your credit line , typically $5 or less. This keeps your utilization near zero relative to the $750 limit. Very low utilization is exactly what FICO rewards. You are not buying anything you need , you are creating a credit event that Kikoff reports.

Pay the balance before the due date. Set autopay so you never miss it. One late payment after the 30-day grace period posts a negative mark that costs 60-100 points. The entire credit-building benefit of Kikoff depends on consistent on-time payments.

Each month, Kikoff reports your payment and balance to Equifax and Experian. This posts a positive payment mark and a low-utilization revolving account to both bureaus. Over time, this builds payment history, contributes to credit mix, and increases account age.

How Kikoff Builds Your Credit Score

Kikoff touches four of the five FICO scoring factors. Payment history (35%) grows with each monthly on-time payment. Utilization (30%) stays near zero , Kikoff's $750 limit with a $5 balance is less than 1% utilization. Credit mix (10%) gains a revolving account. Account age (15%) grows every month the account stays open. The combination is why Kikoff produces meaningful score movement faster than many other tools.

Kikoff Plans and Pricing

- Revolving credit line

- Reports to Equifax + Experian

- No deposit required

- No interest charged

- Cancel anytime

- Everything in Basic

- Secured credit card

- Bill reporting

- Rent reporting

- Identity protection

- Everything in Premium

- Largest credit line

- Maximum score impact

- All available tools bundled

Pricing as of April 2026 per Firstcard review and Kikoff official site. Plans subject to change. All plans include the Kikoff Credit Account revolving line and bureau reporting.

Does Kikoff Really Build Credit

Yes. Kikoff builds credit for people who start with thin files or low scores because it adds positive payment history and a low-utilization revolving account to Equifax and Experian every month. The results are documented. Users starting below 600 average +86 points in the first year. Results require consistent on-time payments and no new negative accounts appearing during the building period.

Kikoff works best when:

- You have no credit history or a thin file

- You have a low score with few or no existing positive accounts

- You need a fast, low-cost entry point to start adding positive payment history

- You want to add a revolving tradeline without a deposit or hard inquiry

Kikoff works slower when:

- Your score is low because of existing collections or late payments , Kikoff adds positives but does not remove negatives

- You miss payments , a single late mark can erase months of Kikoff improvement

- You only care about TransUnion , Kikoff does not currently report there

Does Kikoff Report to All 3 Credit Bureaus

As of April 2026, Kikoff reports to Equifax and Experian only. It does not report to TransUnion. This means one of three bureaus receives no Kikoff data. For lenders or landlords who pull only Equifax or Experian, Kikoff builds credit effectively. For mortgage applications where lenders pull all three, add a separate account that reports to TransUnion.

Some older sources say Kikoff reports to all three bureaus. As of April 2026, this is not accurate. The Firstcard review (April 2026) and Kikoff's own current materials confirm Equifax and Experian only.

Practical implications:

- Kikoff builds your Equifax and Experian scores month by month

- A lender pulling only Experian sees the full benefit of your Kikoff account

- A mortgage lender pulls all three , your TransUnion score may not reflect Kikoff at all

- Pair Kikoff with a secured card or credit builder loan that reports to TransUnion for full three-bureau coverage

As Experian's credit building guide notes, payment history showing on multiple bureaus produces the broadest score impact. Two-bureau reporting still builds meaningful credit , just not for every lender in every situation.

For more options across different account types and bureau coverage, the full guide to credit building cards and accounts covers secured cards, installment builders, and revolving accounts side by side , including which ones report to all three bureaus.

Kikoff vs Other Credit Builders

| Feature | Kikoff Basic | Self (Credit Builder) | Secured Card |

|---|---|---|---|

| Monthly cost | $5 | $25+ | $0 (deposit required) |

| Deposit required | None | None | $200+ tied up |

| Hard inquiry | No | No | Sometimes |

| Interest charged | No | Yes (APR applies) | Only if you carry a balance |

| Account type | Revolving | Installment | Revolving |

| Bureaus reported | Equifax + Experian | All 3 | All 3 (most) |

| Affects utilization | Yes (very low) | No (installment) | Yes (manage manually) |

| Money returned | No | Yes (after term) | Deposit returned at close |

| Cancel penalty | None | Early close fee possible | Close anytime |

As CNBC Select's Kikoff review notes, Kikoff is particularly useful for people who have no credit history or poor credit, since the platform's on-time payment reporting directly impacts the payment history factor , the single largest component of a FICO score at 35%.

Does Kikoff Hurt Your Credit

Signing up does not hurt your credit , no hard inquiry. Missing a payment can hurt. Kikoff gives a 30-day grace period after the due date before reporting a missed payment. If the payment arrives within 30 days of the due date, no late mark posts. Past that window, the late mark costs 60-100 points and stays for seven years. Kikoff also never sells delinquent accounts to external collection agencies.

How Long Does It Take to See Results With Kikoff

Initial score movement typically appears within 1-3 months. The first statement close and payment report to the bureaus within 30 days of account opening. For thin-file borrowers, this often generates a first-ever FICO score within 30-60 days.

More meaningful improvement comes at 6-12 months:

- Month 1-2: First positive marks post. Thin-file borrowers may get their first FICO score.

- Month 3-6: Score movement becomes visible. Average +32 points over 6 months per third-party data.

- Month 6-12: Continued improvement as account age grows and payment history deepens. +58 points average at 6 months per Kikoff's reported data.

- Year 1: +86 points average for users starting below 600 (Kikoff data, Aug 2024-Aug 2025).

The timeline compresses or extends based on what else is in your credit file. A clean thin file with only Kikoff moves faster. A file with existing collections moves more slowly , Kikoff adds positives but does not remove negatives.

As myFICO's score improvement guide explains, consistent on-time payment behavior over 12-24 months produces the most durable score improvements. Kikoff's structure is designed around exactly that behavior pattern.

Is Kikoff Worth It

At $5 per month, Kikoff is one of the lowest-risk credit building entries available. For borrowers with no credit or thin files, it is almost always worth it. For borrowers with existing collections or serious derogatory history, Kikoff helps but is not a substitute for removing negative items. The +86 point average speaks to real results , but only for borrowers who pay on time and avoid new negative accounts during the building period.

Worth it for:

- First-time credit builders with no history

- People who cannot afford a secured card deposit

- Anyone who wants a revolving tradeline reporting to Equifax and Experian immediately

- Borrowers rebuilding after a collection who need positive accounts to offset negatives

Less worth it for:

- Borrowers who need TransUnion reporting specifically

- People whose score issues are driven by existing collections (Kikoff does not remove negatives)

- Anyone who cannot commit to consistent monthly payments

What is Kikoff and how does it work?

Kikoff is a subscription credit building service that gives you a revolving credit line. You spend a small amount in Kikoff's online store each month, pay on time, and Kikoff reports that payment to Equifax and Experian. The Basic plan costs $5 per month. No hard inquiry, no deposit, no interest. The account functions as a revolving credit line on your Equifax and Experian reports, building payment history and contributing to low utilization each month.

What is the Kikoff store?

The Kikoff store is an online marketplace where you spend from your Kikoff credit line. It sells financial literacy products, e-books, digital content, and educational materials. You are not buying everyday items , you are making a small credit transaction that Kikoff reports to the bureaus. The store purchase is the mechanism for creating the monthly credit event. You spend about $5, pay it back on time, and Kikoff reports the activity.

Can you cancel Kikoff?

Yes. Kikoff allows you to cancel at any time without penalty. If you cancel, the account closes and stops reporting new activity. The account history that posted to Equifax and Experian during your membership stays on your credit report for up to 10 years. The positive payment history remains even after canceling. Keep the account open as long as possible to maintain account age , closing it removes that ongoing benefit.

Is Kikoff a credit card?

No. The Kikoff Credit Account is a revolving credit line , not a Visa, Mastercard, or standard credit card. You can only use it in Kikoff's online store. It cannot be taken to gas stations, grocery stores, or anywhere else. The Premium and Ultimate plans include a Kikoff Secured Credit Card, which functions like a standard card. For the Basic $5 plan, you get the credit line only. If you need a card for everyday spending that also builds credit, look at a secured Visa or Mastercard alongside Kikoff.

Building With Kikoff Is Faster When Negatives Come Off First

Kikoff adds positive history. Collections, inaccurate entries, and re-aged accounts subtract from it. A free 3-bureau audit shows exactly what is suppressing your score on Equifax, Experian, and TransUnion so you can address the negatives while Kikoff stacks the positives.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Does Autopay Build Credit , And What Happens If You Miss a Payment Kikoff's entire scoring benefit depends on on-time payments. One missed payment after the 30-day grace period erases months of progress. This covers exactly how autopay interacts with credit building, which account types benefit most from it, and the one hidden risk of autopay that most borrowers do not know about until it is too late.

-

Credit Score Ranges , What Is Good and What Each Tier Opens Kikoff users starting below 600 average +86 points in the first year. This covers what opens at each score milestone , 580 for FHA, 620 for conventional mortgages, 670 for the Good tier, 740 for the best rates. Knowing your target makes the Kikoff building process purposeful rather than abstract.