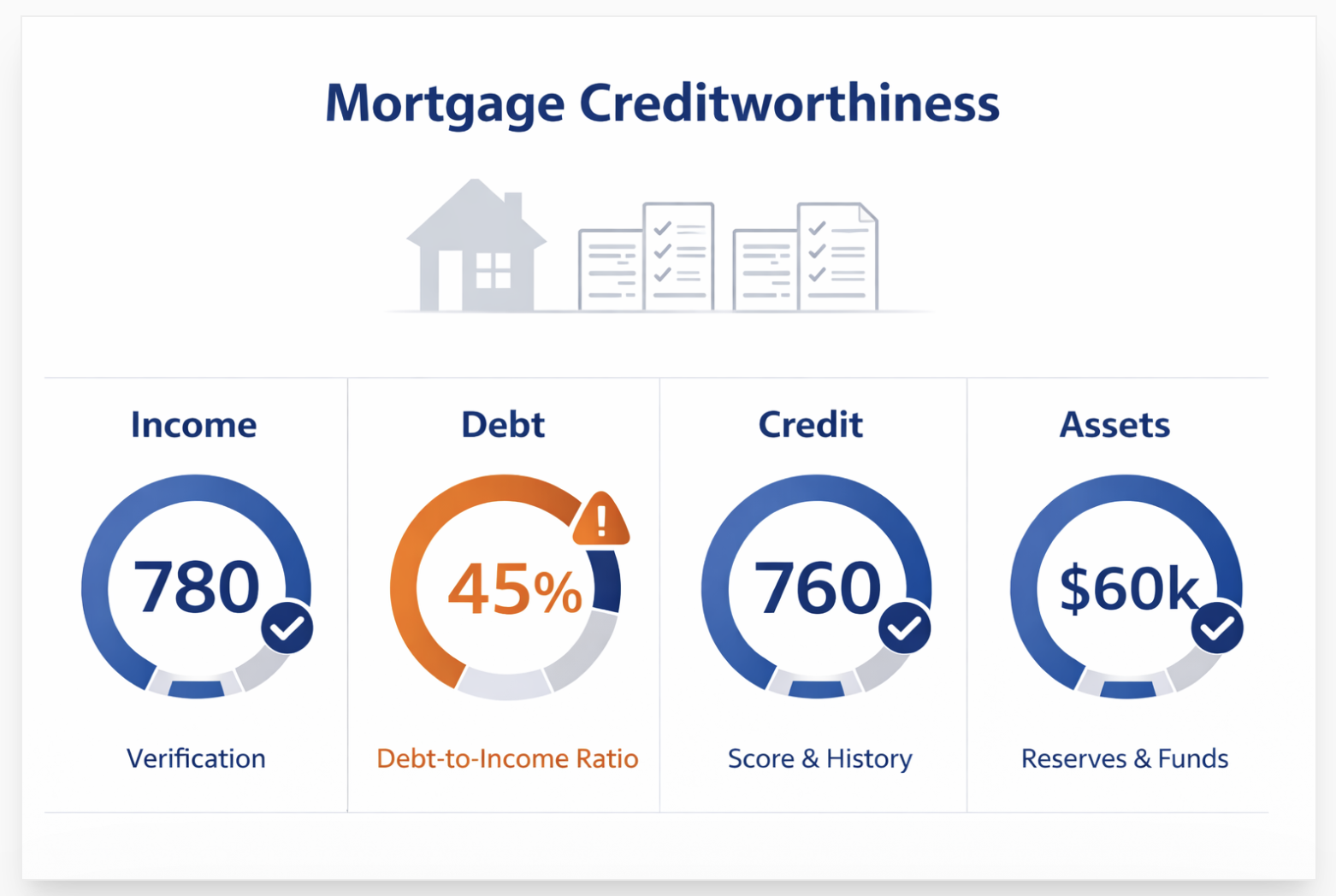

Laurel lenders calculate your creditworthiness for home loans by reviewing whether you can repay the mortgage on time and sustain the payment over the long term. The review usually includes income, debt obligations, credit history, assets, employment stability, and the property being financed. It is not based on credit score alone.

Many borrowers assume a high score guarantees approval. That is incomplete. In loan files we review, applicants with strong scores are still denied when debt ratios are too high or income cannot be verified. At the same time, borrowers with moderate scores may still qualify when income is stable, reserves are strong, and debts are controlled.

Lenders often focus on risk layering. A lower score combined with high debt and low reserves may create concern. A lower score with low debt and strong savings may be viewed differently. This is why mortgage decisions can vary between applicants with similar scores.

For home loans, the goal is not only approval. It is approval on terms that fit the borrower’s budget. Interest rate, down payment, mortgage insurance, and reserve requirements all connect to creditworthiness.

This guide explains how Laurel lenders calculate creditworthiness for home loans. Also, what matters most in underwriting, and what borrowers can improve before applying.

How Creditworthiness Is Calculated for Mortgages in LaurelMD

Laurel lenders do not make approval decisions based on a single number. They run every application through an automated underwriting system (AUS), Desktop Underwriter (Fannie Mae) or Loan Product Advisor (Freddie Mac), which weighs all five factors simultaneously. The output is an Approve/Eligible or Refer recommendation that either clears the path or sends it to manual underwriting.

Factor 1: Credit Score

Lenders pull a tri-merge report from all three bureaus, Equifax, Experian, and TransUnion, and use your middle score. If two borrowers apply together, the lender uses the lower middle score of the two.

For most Laurel lenders and loan products:

- Conventional loan: 620 minimum credit score, 3 to 20% down payment, PMI required under 20% (cancelable), best rates above 740

- FHA loan: 580 minimum credit score, 3.5% down payment, lifetime MIP at 3.5% down, 500 score allowed with 10% down

- VA loan (veteran): 620 preferred by most lenders, 0% down payment, no MIP, no official minimum score

- USDA loan: 640 minimum for most lenders, 0% down payment, annual fee of 0.35%, applies to rural areas around Laurel

- MMP (Maryland Mortgage Program): 640 minimum score, 3% or more down, 50% DTI allowed for scores above 680

Sources: Maryland Mortgage Program Product Matrix, January 2025; New American Funding Maryland FHA guide; Bankrate Maryland mortgage requirements. Some MMP conventional products allow 45% DTI at 640 to 679 and 50% at 680 and above.

What the score reflects: payment history (35%), amounts owed and credit utilization (30%), length of credit history (15%), new accounts (10%), and credit mix (10%).

Every missed payment, every high-balance card, and every recent hard inquiry affects the score the AUS sees on the day your lender pulls it, not the score from last month, and not the score on Credit Karma, which often differs from a mortgage-specific FICO score.

What to do: Pull all three bureau reports before applying. Dispute any inaccurate entries simultaneously across all three. One removed collection can move a score 30 to 60 points, potentially moving you from FHA to conventional or from a 6.8% rate to a 6.3% rate.

Factor 2: Debt-to-Income Ratio (DTI)

DTI is the most common denial reason in Laurel.

DTI is your total monthly debt payments divided by your gross pre-tax monthly income. Lenders calculate two numbers. Front-end DTI covers proposed housing costs only, principal, interest, taxes, insurance, and HOA if applicable. Back-end DTI covers the housing payment plus all monthly debt obligations: car loans, student loans, credit cards, and personal loans.

On a Laurel home at $400,000 with 5% down at 6.5% interest, principal and interest alone runs approximately $2,435 per month. Add property taxes (roughly $350 to $400 per month in Prince George's County) and homeowners insurance (roughly $150 per month), plus any existing debt, and DTI climbs fast.

DTI limits by loan type for Laurel lenders:

- Conventional (standard): 43% maximum DTI

- Conventional (with AUS approval): up to 50%

- FHA (standard): 43% maximum DTI

- FHA (with compensating factors): up to 57%

- MMP with score 680 and above: 50% maximum DTI

- MMP with score 640 to 679: 45% maximum DTI

Source: Maryland Mortgage Program Product Matrix, January 2025. FHA 57% DTI requires compensating factors, typically substantial reserves, no discretionary debt, or significant residual income. Most Laurel lenders set a practical cap lower than the technical maximum.

The fastest way to lower DTI before applying: pay off the smallest monthly debt obligations first, not the highest balance. A $300 per month car payment eliminated saves more in DTI than $3,000 paid off a credit card with a $75 per month minimum. When you talk to a Laurel mortgage lender, ask them to run the numbers with and without specific debts paid so you know exactly which payoffs move the approval dial.

Key insight: Lenders use your gross income, not take-home pay. And they use the minimum payment on revolving debt, not the full balance. Paying minimums on a card versus closing it entirely affects DTI differently than you might expect. Know the math before you make any payments.

Factor 3: Employment History and Income Stability

Laurel lenders verify employment through pay stubs, W-2s, and employer contact. Two years of consistent employment is the standard. A Laurel borrower who has worked the same job for three years checks this box cleanly. One who switched from a retail job to a tech job 14 months ago in the same industry at higher pay usually qualifies. One who left a stable job eight months ago to freelance has to document 24 months of self-employment tax returns before that income counts.

Specific situations that complicate employment review in Laurel's market: federal government contractors common near the NSA Annex and NASA Goddard facility on short-term contracts need to show renewal history. Borrowers with seasonal or commission income are averaged over two years, so one high year does not define the qualifying number. Gaps of more than 30 days in the past two years need a written explanation.

What Income Counts

Income that counts: W-2 wages, verified self-employment income (two-year average from tax returns), rental income (typically 75% of gross rents on documented properties), Social Security, pension, and disability.

Income that does not count: cash income not reported on taxes, gifts, stock value (only dividends count, not the stock itself), or any income you cannot document with official records.

Verdict: If you are planning a job change, do it after closing, not before. Changing jobs mid-application, even for higher pay, can pause or kill an approval in underwriting. Talk to your lender before making any major employment moves.

Factor 4: Down Payment

In Laurel's market with homes ranging from $300,000 to $600,000, down payment options matter. Maryland's median down payment was $35,585 in 2024 according to ATTOM data, which reflects real buyer behavior in a market where 20% is not the norm.

What the Down Payment Controls

It sets your loan-to-value ratio (LTV), which determines whether you pay PMI or MIP and affects the rate you receive. At 20% down, no PMI on a conventional loan. At 10% down, PMI applies until you reach 20% equity and it is cancelable. At 3.5% down on FHA, lifetime MIP applies and it cannot be removed without refinancing.

It also affects which programs are available. The Maryland Mortgage Program offers down payment assistance up to $6,000 deferred and zero-interest for buyers who qualify for MMP products and meet the 640 minimum score. Prince George's County, which covers the eastern portion of Laurel, has additional DPA programs. Stacking MMP assistance with Prince George's County assistance is possible and can eliminate most of the cash needed at closing on a moderately priced Laurel home.

A larger down payment does not guarantee approval on its own, but it can offset a weaker credit score or higher DTI in the AUS calculation. A borrower with a 610 score putting 20% down signals something very different to the system than the same borrower putting 3% down.

Verdict: If you are a first-time buyer in Laurel, research MMP products before deciding on a down payment amount. Sometimes, 3.5% with MMP assistance and a 640 score produces a lower total monthly payment than 10% down with a 620 score, because of the rate differential and program benefits.

Factor 5: Cash Reserves and Assets

After your down payment and closing costs clear, lenders want to see that you have something left. Reserves are measured in months of housing payment (principal, interest, taxes, and insurance). Conventional loans typically require two to three months for single-family primary residences with strong credit. FHA loans have minimal reserve requirements for most purchases.

The MMP specifies that applicants cannot have liquid assets exceeding 20% of the home's purchase price. That means too much cash can actually disqualify you from MMP assistance programs.

What Counts as Reserves

Counts as reserves: checking, savings, and money market accounts; 100% of vested 401(k) and IRA balances minus any 10% early withdrawal penalty; and stock account balances.

Does not count: equity in another property, unvested retirement funds, expected gifts not yet received, and the down payment funds you are already using.

Reserves also tell the lender something about how you manage money. A borrower who has $40,000 saved for a down payment and $12,000 remaining in savings is a different risk profile than one who depleted every account for the down payment and has $400 left.

Note for MMP buyers: The MMP's 20% liquid asset limit is a disqualifier that many Laurel buyers do not know about. If you have saved aggressively and your liquid assets exceed 20% of the purchase price, you may not qualify for MMP down payment assistance even if your score and DTI are fine.

What Happens After You Submit Your Laurel Home Loan Application

Once you submit a complete application in Laurel, the lender runs it through an AUS, typically Fannie Mae's Desktop Underwriter (DU) for conventional or the FHA TOTAL Scorecard for FHA. The AUS evaluates all five factors simultaneously and returns one of three findings: Approve/Eligible (proceed to underwriting), Refer with Caution (manual review, harder to approve), or Out of Scope (does not qualify under standard guidelines).

If you get an Approve/Eligible, an underwriter still reviews your documentation manually. They verify the income documents, confirm the credit report data, review the appraisal, and check compliance with the specific loan program rules. This is where undisclosed debts, unexplained large deposits, or recent credit inquiries can create problems. The AUS did not see them, but the underwriter does.

One thing Laurel buyers often miss: Maryland passed new disclosure requirements in 2025 for conventional home mortgage loans regarding loan assumability in divorce situations (Maryland Banking Commissioner advisory, September 2025). Your lender is now required to provide written disclosure about assumption rights before collecting financial documentation. This is procedural and does not affect creditworthiness, but it is part of what Laurel lenders must complete before moving to underwriting review.

How to Improve Your Creditworthiness Before Applying in Laurel

Three months before applying is the minimum useful window for credit improvement. Six months gives you real options.

Pull All Three Bureau Reports First

Errors are common. A Bridgeforce Data Solutions analysis found 15 to 25% of trade lines submitted to credit bureaus contain errors. A wrong date on a delinquent account, a duplicate collection entry, or an account that was settled but still shows as open, any of these are disputable under the FCRA and can move a score 20 to 60 points when removed. If you are at 614 and need 620, one dispute resolution can get you there. Our guide on building clean credit files across all three bureaus walks through the simultaneous dispute process that gets results within 30 to 45 days.

Pay Down Revolving Balances Before Applying

Credit utilization is 30% of your FICO score and responds fast. Get every card below 30% of its limit. Getting below 10% produces the most score lift. Do this in the month before your lender pulls credit. The payoff needs to show on the statement that reports to the bureau before the pull date.

Do Not Open New Accounts or Take on New Debt

Every new hard inquiry costs 5 to 10 points and stays on your report for two years. New accounts lower your average account age. A new car loan in the three months before a mortgage application raises your DTI and your inquiry count at the same time. Hold off on everything until after closing.

For Laurel buyers specifically, the distance between loan products matters more than it does in cheaper markets. Qualifying for a conventional loan at 620 instead of FHA at 580 eliminates lifetime MIP, a difference of $130,000 to $170,000 on a 30-year loan in the $375,000 to $440,000 price range. Working with a Laurel credit repair specialist before applying can identify exactly which items on your report are suppressing your score and which disputes move you across the thresholds that matter for the loan you are targeting.

Do not pay any collection account before consulting a lender and checking the account's accuracy. Paying an inaccurate collection validates it without removing it. Paying a legitimate old collection may not move your score and does not guarantee FHA or conventional approval. Disputing an inaccurate entry under the FCRA is free, does not require payment, and if successful removes the item entirely. Do the dispute review before the payment decision.

Maryland Mortgage Program income limits for Prince George's County (2025): Households of 1 to 2 people on most MMP products: approximately $131,700. Households of 3 or more: approximately $153,650. These limits are higher for buyers in targeted areas. If your income is below these thresholds and your credit score is 640 or above, MMP products with down payment assistance are likely available to you. An MMP-approved lender can confirm eligibility in one conversation.

Frequently Asked Questions

What credit score do I need to buy a home in Laurel, MD?

For a conventional loan: 620 minimum, though rates improve substantially above 680 and again above 740. For an FHA loan: 580 with 3.5% down, or 500 with 10% down. The Maryland Mortgage Program requires 640 for most products. VA loans have no official minimum but most Laurel lenders prefer 620. On a $400,000 Laurel home, the rate difference between a 620 and a 740 score is typically 0.5 to 1.0%, which translates to $70,000 to $140,000 in additional interest over a 30-year loan.

What DTI is too high for a mortgage in Laurel?

Most conventional lenders cap at 43 to 45% DTI. FHA allows up to 50 to 57% with compensating factors. The Maryland Mortgage Program allows 50% for borrowers with scores of 680 or higher and 45% for scores of 640 to 679. DTI is the most common denial reason in Prince George's County home loan applications. If your DTI exceeds 50%, including the proposed housing payment, most programs will not approve you. Lowering it requires either reducing monthly debt obligations or increasing income, not just improving your credit score.

What down payment assistance is available in Laurel, MD?

Maryland Mortgage Program 1st Time Advantage loans include up to $6,000 in down payment assistance, zero interest, deferred until sale or refinance. SmartBuy 3.0 pairs MMP loans with student loan payoff assistance. Prince George's County, which covers part of Laurel, offers additional county-specific DPA programs that can be layered with MMP. The minimum credit score for MMP DPA products is 640, and borrowers must complete a HUD-approved homebuyer education course. Income limits apply, in Prince George's County, approximately $131,700 for 1 to 2 person households.

How does a collection account affect my Laurel home loan application?

It depends on the loan type and the account's accuracy. FHA does not automatically require collection accounts to be paid before closing. Conventional underwriters often require resolution of collection accounts above certain dollar thresholds, typically $1,000 or more. Before paying any collection, verify its accuracy across all three bureaus. Inaccurate collections are disputable under the FCRA without payment. Medical debt was removed from credit score calculations under 2023 and 2024 CFPB rule changes and should not affect FHA qualification. Resolving an inaccurate collection through dispute can produce a 30 to 60 point score improvement within 30 to 45 days.

Does a recent job change hurt my mortgage application in Laurel?

It depends on the change. Moving from the same field to a new employer with higher pay typically does not disqualify you. Switching from W-2 employment to self-employment less than two years before applying means the self-employment income cannot be used to qualify. Starting a new career in a different field within the past 12 months requires more documentation and lender discretion. The safest approach: talk to a lender before making any employment change, and wait until after closing if the new job involves a different industry or employment type.

Closing

Laurel lenders usually calculate creditworthiness by asking one core question: can this borrower handle the payment with acceptable risk. Credit score matters, but it is only one part of the file. Income, debt load, and cash reserves often carry equal weight.

If you plan to apply soon, review the parts you can control first. Lower revolving balances, avoid new debt, organize income documents, and build reserves before submitting an application. Small changes can improve both approval odds and loan terms.

The strongest mortgage file is not always the highest score. It is the file that shows stable repayment capacity.