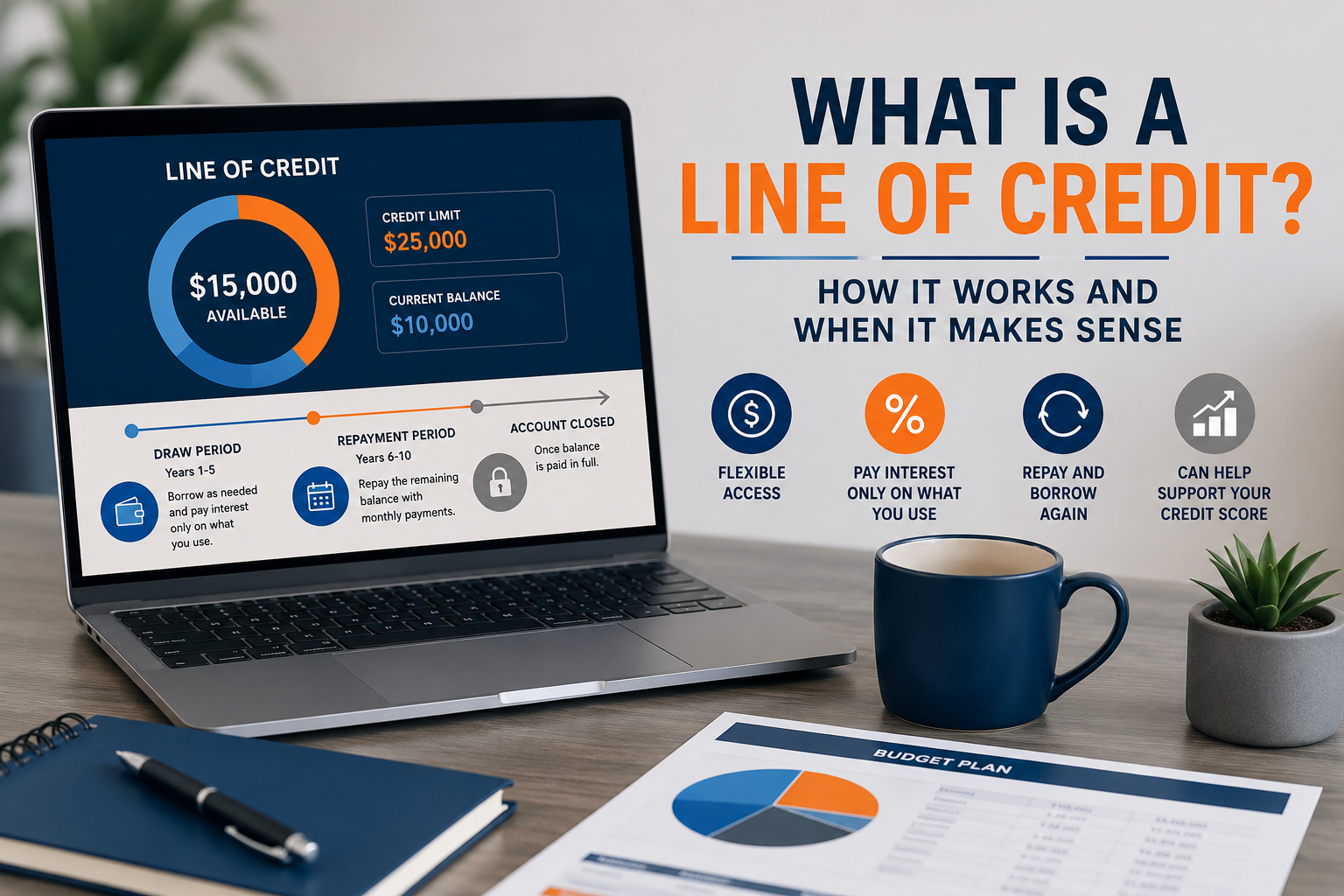

A line of credit is a flexible borrowing account that lets you pull funds up to a set limit, pay them back, and borrow again, only paying interest on what you use. Most people encounter this question when their bank offers them one, or when a traditional loan feels like too much commitment for what they actually need.

Running a credit repair company, I see this question almost weekly. Last month alone, we had 14 clients come in confused about whether a line of credit had helped or hurt their score, and in most cases, the problem was not the product; it was that nobody explained it to them first.

A 2024 r/personalfinance thread on Reddit showed a similar pattern. Dozens of users admitted they did not fully understand draw periods or variable rates until they were already in repayment. You can read that thread here. The Consumer Financial Protection Bureau also reports that 43% of families had difficulty paying bills or expenses in 2024, up from 38% the year before — a sign that flexible credit tools are more relevant than ever. (Source: CFPB Making Ends Meet Report, 2024)

What a Line of Credit Is (Plain and Simple)

A line of credit (LOC) is a preset amount of money a bank or credit union agrees to lend you. You do not receive a lump sum upfront. Instead, you draw from it when you need it. You pay interest only on what you borrow, not on the full limit.

Think of it like a water tap. The tank holds a fixed amount of water. You turn it on when you need it, turn it off when you do not. You pay for the water you use, not for what stays in the tank.

Key terms to know:

How a Line of Credit Works Step by Step

Understanding the mechanics protects you from surprises later. Here is how the full process works:

You apply to a bank or credit union. The lender checks your credit score, income, and debt-to-income ratio.

The lender approves a credit limit and sets an interest rate. This application triggers a hard inquiry on your credit report.

You receive access to the funds usually through online transfers, a linked debit card, or paper checks.

You draw what you need, when you need it. Interest starts the moment you draw, not when you apply.

You receive a monthly statement. It shows your balance, the minimum payment due, and your available credit.

You pay down the balance. As you repay, the available credit refills just like a credit card.

The draw period ends. After that window closes, you can no longer pull new funds and must repay the remaining balance.

One important note: unlike a credit card, most personal lines of credit do not have a grace period. Interest begins accruing on drawn funds immediately. According to Bankrate, as of May 2026, the average personal loan rate is 12.27%, and personal lines of credit often sit in a similar range depending on your credit tier.

Types of Lines of Credit

Not all lines of credit work the same way. Knowing the differences helps you pick the right one.

Personal Line of Credit (PLOC) A personal line of credit is unsecured, meaning no collateral is required. Limits typically range from $1,500 to $100,000. Approval depends heavily on your credit score and income. Interest rates tend to be lower than credit cards but higher than secured options.

Home Equity Line of Credit (HELOC): A HELOC uses your home as collateral. Because the lender has a secured asset, rates are lower. Draw periods on HELOCs typically run 5 to 10 years. The tradeoff: if you default, you risk losing your home.

Business Line of Credit Lenders design this product for a company's cash flow needs. Business owners use it to cover payroll gaps, buy inventory, or bridge slow seasons. It works like a personal LOC but underwritten on the business's financials.

Personal Line of Credit: A Closer Look

A personal line of credit is the most common type for individual borrowers. It gives you flexible access to cash without needing to name a specific purchase. This makes it useful for home renovations with uncertain costs, medical bills that come in stages, or income gaps for freelancers and self-employed workers.

To qualify, most lenders want:

A credit score of at least 670 (some require 700+)

Proof of stable income

A debt-to-income ratio below 40%

A solid credit history with no recent missed payments

In our credit repair practice, this is where we see the most friction. Clients want a personal LOC but do not qualify because of old collection accounts or high utilization. Cleaning up those items first before applying makes a measurable difference in the rate and limit offered.

Line of Credit vs. Personal Loan: What Is the Actual Difference?

People often confuse these two products. Both involve borrowing from a lender. Both affect your credit. But the mechanics are very different.

A personal loan gives you a lump sum upfront. You begin paying interest on the full amount immediately, even before you spend a dollar. Repayment is fixed at the same payment every month until the loan closes.

A line of credit gives you a limit you can draw from as needed. You pay interest only on what you borrow. Payments fluctuate with your balance. It stays open and reusable during the draw period.

Here is when a personal loan makes more sense: you know the exact amount you need and want a predictable monthly payment. Here is when a line of credit wins: your costs are variable, unpredictable, or spread over time.

According to U.S. News, total personal loan debt in America reached $249 billion as of Q3 2024, up 64% over five years. Much of that growth came from people using loans for the same variable expenses that a line of credit handles better.

Line of Credit Pros and Cons

Pros

You pay interest only on what you use. A $20,000 limit does not cost you anything if you never draw from it.

Funds recharge as you repay. You do not need to reapply every time you need cash.

Rates beat credit cards. Most personal LOCs carry lower rates than credit cards, which averaged over 20% APR in 2024 according to the CFPB.

Flexible use. No restrictions on what you spend the money on, unlike student or auto loans.

Builds credit mix. Adding a revolving credit account improves the diversity of your credit profile, which counts for about 10% of your FICO score.

Cons

Variable rates create uncertainty. Your payment can increase if benchmark rates rise, and they did significantly from 2022 to 2024.

No grace period. Interest starts as soon as you draw. Credit cards give you up to 30 days before interest kicks in.

Qualification is strict. Most lenders require good to excellent credit. Borrowers with scores below 670 often cannot access unsecured PLOCs.

Overspending risk is real. Easy access to revolving credit makes it tempting to borrow more than needed.

Fees add up. Annual fees, maintenance fees, and origination fees are common. Always read the fine print.

How a Line of Credit Affects Your Credit Score

Opening a line of credit triggers a hard inquiry. That inquiry typically drops your score by 5 to 10 points temporarily. After that, how you manage the account determines whether it helps or hurts long term.

Three factors matter most:

Credit utilization. The CFPB found the average cardholder had a utilization rate of 22.6% in 2023. Keeping your LOC utilization below 30% protects your score.

Payment history. On-time payments build a positive record, which is the single largest factor in your FICO score at 35%.

Credit mix. Adding a revolving credit account to a file that only has installment loans can improve your score over time.

In our office, we have seen clients whose scores dropped after opening a LOC — not because of the inquiry, but because they drew heavily and let utilization spike above 60%. The product did not hurt them. Their spending habits did.

Who Should and Should Not Use a Line of Credit

A line of credit works well for people with:

Variable or freelance income who need a cash flow buffer

Ongoing projects with uncertain costs (home renovations, medical treatment)

Strong credit scores who can access lower rates

The discipline to borrow only what they can realistically repay

A line of credit is a poor fit for people who:

Struggle to limit their spending when credit is available

Have a specific, known expense — a personal loan is simpler and often cheaper

Already carry high revolving balances — adding another line increases risk

Have credit scores below 670 and would face high rates anyway

One thing we tell clients clearly: a line of credit is a tool, not an emergency fund. Leaning on it for basic expenses month after month leads to compounding interest that is hard to reverse.

Before You Apply

Thinking About Opening a Line of Credit?

A line of credit can help when used the right way, but old collections, high utilization, or credit report errors may lead to higher rates or denial. Check your credit first before you apply.

Get Your Free Credit Report ReviewNo pressure. Just a clear look at what may be holding your credit back.

How to Apply for a Personal Line of Credit

The application process is straightforward once your credit is in order.

Check your credit report first. Pull it free at AnnualCreditReport.com and dispute any errors before applying.

Compare lenders. Banks, credit unions, and online lenders all offer PLOCs. Credit unions often have lower rates. The NCUA reported an average three-year loan rate of 10.72% at credit unions in Q3 2025, compared to higher bank averages.

Prequalify where possible. Some lenders offer soft-pull prequalification, which does not affect your credit score.

Submit your application. Provide proof of income, identification, and bank account details.

Review the terms carefully. Check the draw period length, repayment terms, variable rate details, and all fees before signing.

Frequently Asked Questions

Does a line of credit hurt your credit score? Opening one causes a temporary dip from the hard inquiry. Long-term, responsible use, low utilization, and on-time payments improve your score.

What credit score do you need for a personal line of credit? Most lenders require at least 670. Some require 700 or higher for their best rates. Borrowers with scores above 720 typically receive the most favorable terms.

Is a line of credit the same as a credit card? Both are revolving credit. The key differences: a LOC usually has higher limits, no physical card for swiping at retail, no grace period, and often a defined draw period that credit cards do not have.

Can you pay off a line of credit early? Yes. Most lenders do not charge prepayment penalties on PLOCs. Paying early reduces the total interest you owe.

What happens when the draw period ends? You can no longer access new funds. You enter the repayment period and must pay off the remaining balance, often in fixed monthly installments.