Loan modification vs refinancing is not just a comparison of two options. It’s a financial decision that can impact how much you pay over the life of your loan by thousands, sometimes tens of thousands of dollars.

At a surface level, both strategies aim to lower your monthly payment. But the way they achieve that result, and the long-term cost implications, are fundamentally different.

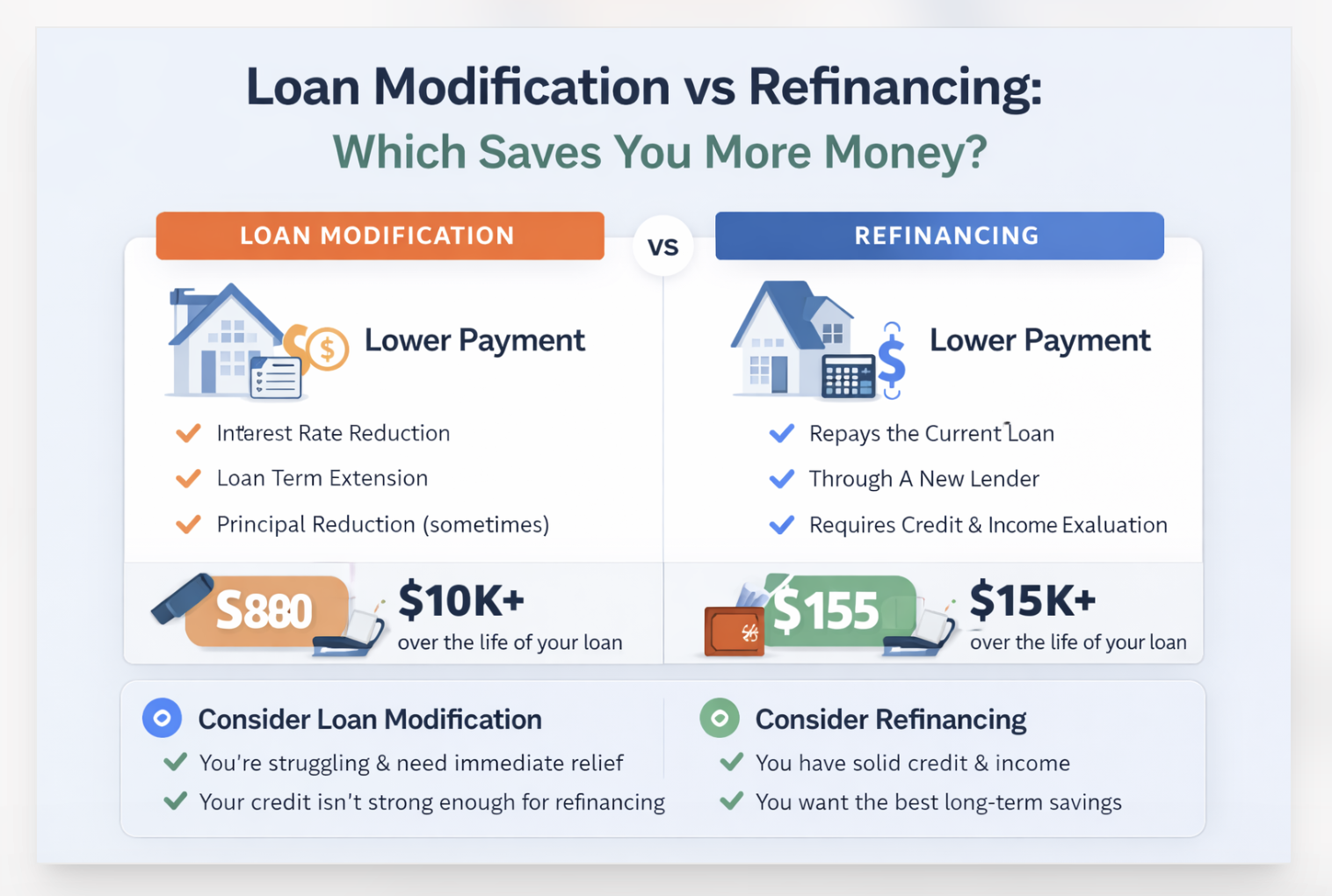

A loan modification typically reduces payments by adjusting the existing loan terms, often through interest rate reductions, term extensions, or, in some cases, principal adjustments. Refinancing, on the other hand, replaces your current loan with a new one, ideally at a lower interest rate, but often with new closing costs and a reset repayment timeline.

Wanna know the real difference?

Well, based on common lending scenarios, refinancing can generate higher long-term savings when borrowers qualify for significantly lower interest rates. However, loan modifications may result in lower immediate payments without the upfront costs, but can increase the total interest paid over time due to extended terms.

In practical terms, we’ve seen situations where refinancing saved borrowers over $10,000 in interest across the life of a loan, while loan modifications reduced short-term financial pressure but extended repayment by several years, increasing the overall cost.

That’s why the better option isn’t universal.

It depends on your credit profile, current interest rate, financial stability, and whether your goal is immediate relief or long-term savings.

In this guide, we’ll break down loan modification vs refinancing using real cost comparisons, explain when each option makes financial sense, and help you determine which one actually saves you more money based on your situation.

Loan Modification · Mortgage Refinancing · Home Loan Options · Financial Hardship · Mortgage Relief

Two tools. One mortgage. Completely different outcomes depending on your financial situation. This guide runs the actual numbers on both options so you can make the decision with data, not guesswork.

Updated March 2026 · Sources: Consumer Financial Protection Bureau, Federal Housing Finance Agency, Freddie Mac Primary Mortgage Market Survey, U.S. Department of Housing and Urban Development, Fannie Mae mortgage guidelines

- Loan modification restructures your existing loan without replacing it. It requires proof of financial hardship and typically results in a credit score impact of 50 to 150 points.

- Refinancing replaces your existing loan with a new one. It requires qualifying for credit at current market rates and costs 2% to 5% of the loan balance in closing costs.

- Under FICO 8, the scoring model used in 90% of lending decisions, a modification appears as a derogatory mark. A successful refinance does not.

- The break-even point on a refinance, calculated as closing costs divided by monthly savings, determines whether refinancing makes financial sense given how long you plan to stay in the home.

- Most borrowers who complete a loan modification must wait 12 to 24 months before they can qualify for a refinance.

- Modification produces the largest immediate payment relief. Refinancing typically produces the largest long-term savings when rates are favorable.

Loan Modification vs. Refinancing: The Full Comparison at a Glance

| Factor | Loan Modification | Refinancing |

|---|---|---|

| What happens to your loan | Existing loan terms are changed. Loan stays in place. | Existing loan is paid off. New loan is originated. |

| Credit requirement | No minimum score required. Financial hardship must be demonstrated. | Typically 620+ for conventional; 580+ for FHA. Better rates require 740+. |

| Upfront cost | None. Lenders do not charge closing costs for modifications. | 2% to 5% of loan balance in closing costs ($6,000 to $15,000 on a $300,000 balance). |

| Income requirement | Must demonstrate hardship (reduced income, medical event, job loss). Too much income can disqualify. | Must prove stable, sufficient income to service the new loan. Debt-to-income ratio typically must be below 43% to 50%. |

| Home equity requirement | No minimum equity required. Underwater properties (negative equity) can qualify. | Typically 20% equity for best rates. 3% minimum for some conventional products. FHA requires 2.25%. |

| Credit score impact | Significant negative impact: 50 to 150 point drop. Entry noted as "modified" or "not paid as agreed." | Minor temporary impact: 5 to 10 points from hard inquiry. No derogatory mark if completed. |

| Time to complete | 30 to 90 days. Some government programs take 3 to 6 months. | 30 to 60 days for a standard rate-and-term refinance. |

| Long-term interest cost | Term extension increases total interest paid over life of loan significantly. | Rate reduction can save tens of thousands in total interest without extending the term. |

| Future refinance eligibility | Mandatory waiting period: 12 to 24 months of on-time payments post-modification before refinancing. | Can refinance again after 6 months (most lenders) with no waiting period if creditworthy. |

| Best for | Borrowers in financial hardship who cannot qualify for refinancing. | Borrowers with stable income and credit who can secure a lower rate or better terms. |

People Also Ask: The Direct Answers

The Real Numbers: Side-by-Side Savings Calculation

Scenario: A homeowner has a $300,000 remaining mortgage balance, originally a 30-year loan with 22 years remaining, at a 7.5% interest rate. Current monthly principal and interest payment: $2,098.

The lender offers a modification to 5.5% interest for 30 years. The market offers a refinance to 6.25% for a new 30-year term at a closing cost of $8,500.

How to Calculate the Refinance Break-Even Point

Before choosing refinancing, every borrower needs to calculate the break-even point: the month at which cumulative monthly savings equal the upfront closing costs. If you plan to sell or move before reaching break-even, refinancing costs you money rather than saving it.

Qualification Requirements: Who Qualifies for Each Option

- Documented financial hardship: job loss, income reduction, medical event, divorce, or natural disaster

- Currently delinquent on the mortgage or able to demonstrate imminent default risk

- Property must typically be a primary residence (investment properties rarely qualify)

- Existing loan must be owned or guaranteed by Fannie Mae, Freddie Mac, FHA, VA, USDA, or a cooperating private lender

- Current monthly mortgage payment exceeds a threshold percentage of gross income (typically 31% for government programs)

- Ability to make a reduced modified payment must be demonstrated

- No minimum credit score required

- No minimum equity required -- underwater properties can qualify

- Minimum credit score: 620 for most conventional programs; 580 for FHA; 640 to 680 for jumbo loans

- Stable, verifiable income for the past 24 months (W-2, tax returns, or bank statements for self-employed)

- Debt-to-income ratio (DTI) below 43% to 50% depending on lender and loan type

- Minimum 3% equity for conventional rate-and-term refinance; 20% to avoid PMI; 80% LTV for cash-out

- 6 months of on-time payments on current mortgage (most lenders; some require 12 months)

- Property appraisal confirming current market value supports the new loan amount

- Ability to pay closing costs of 2% to 5% of the loan balance upfront or rolled into the new loan

- No active bankruptcy or foreclosure proceedings

Which Option Wins in Each Financial Scenario

The Credit Score Impact: Why This Matters More Than Monthly Savings for Some Borrowers

The credit score impact of choosing modification over refinancing extends beyond the score number itself. A damaged score from a modification can affect auto insurance premiums in most states, rental applications if the home is eventually sold, employment background checks for financial positions, and the rate available on any future mortgage. According to the CFPB's guidance on credit scoring, a single derogatory event like a modification can affect lending decisions for the full duration of its 7-year reporting window.

Your Credit Score Determines Which Option Is Even Available to You. Know Where You Stand First.

Refinancing requires qualifying credit. A score below 580 takes refinancing off the table entirely, leaving modification as the only option. A free 3-bureau audit identifies your current score, every negative entry affecting it, and what would need to change to open the door to refinancing eligibility.

Pros and Cons of Loan Modification

- No upfront costs or closing fees. The lender absorbs administrative costs in exchange for avoiding foreclosure expenses.

- No credit score or equity minimum. Underwater and damaged-credit borrowers qualify.

- Immediately stops the foreclosure process when approved under most program structures.

- Can significantly reduce monthly payment, sometimes by $300 to $700 per month.

- No new loan means no new closing costs, no new appraisal, and no income verification beyond hardship documentation.

- Rate reduction is often below market rate for the borrower's credit profile.

- Requires demonstrating default or imminent default, which almost always produces a significant credit score drop.

- Modification notation appears as derogatory on credit report for up to 7 years from the date of first delinquency.

- Term extension substantially increases total interest paid over the life of the loan.

- 12 to 24-month mandatory waiting period before you can refinance at a better rate.

- The lender has significant discretion. Modification is not a right, it is a negotiated outcome.

- Some modifications capitalize missed payments into the principal, increasing the total balance owed.

Pros and Cons of Mortgage Refinancing

- Produces no derogatory credit notation. A successfully completed refinance is a positive financial event on your credit file.

- Access to the full market rate available to creditworthy borrowers, not just what the current lender offers.

- Option to shorten the loan term (e.g., from 30 to 15 years) to save significantly on total interest without extending the repayment timeline.

- Can eliminate private mortgage insurance (PMI) if the new LTV ratio qualifies.

- Cash-out refinance option allows tapping home equity for renovations, debt consolidation, or investment.

- Can be refinanced again within 6 to 12 months if rates continue to fall.

- Upfront closing costs of 2% to 5% of the loan balance must be paid or rolled into the new loan, increasing the balance.

- Requires qualifying credit, income, and home equity. Not available to borrowers in financial hardship.

- Extending the loan term resets the amortization clock, increasing total interest paid even at a lower rate.

- Break-even point analysis is mandatory. Refinancing costs money if you sell or move before recouping closing costs.

- Full underwriting process requires income documentation, appraisal, and credit review, which takes 30 to 60 days.

- Rate-and-term refinance requires adequate equity. Negative equity situations cannot access this option.

How to Apply for a Loan Modification: Step-by-Step

How to Apply for a Mortgage Refinance: Step-by-Step

Debt Decisions That Affect Both Options: The Bigger Picture

Whether you choose modification or refinancing, the decision sits inside a larger financial framework of how you are managing debt overall. The same income, credit profile, and balance sheet that determine your mortgage options also affect every other financial decision you face.

Before committing to either path, it is worth understanding how mortgage relief interacts with other debt obligations. Our analysis of whether to pay down debt or invest your available cash covers the interest rate arbitrage question that applies directly here: if you can refinance to a lower rate, does it make more sense to make extra principal payments or redirect that capital to investment returns? The answer depends on the spread between your mortgage rate and expected investment returns.

There is also the question of whether existing unsecured debt -- credit cards, personal loans, collection accounts -- is affecting your refinance eligibility. High credit card utilization can push a 700 score to 640, potentially moving you from one rate tier to another. And choosing credit repair vs. debt settlement as your strategy for resolving those accounts has a direct impact on how quickly you become refinance-eligible and at what rate tier.

Before You Can Choose Between Modification and Refinancing, You Need to Know Your Exact Credit Position.

A borrower at 640 and a borrower at 680 face different rate tiers, different lender requirements, and different timelines to refinance eligibility. A free 3-bureau audit tells you exactly where you stand, what is keeping your score where it is, and what would move the needle before your next mortgage application.

Frequently Asked Questions

What is the difference between loan modification and refinancing?

Loan modification amends your existing mortgage with your current lender, requires documented financial hardship, costs nothing upfront, and leaves a derogatory mark on your credit. Refinancing replaces your mortgage with a new loan from any lender, requires qualifying credit and income, costs 2% to 5% of the loan balance in closing costs, and produces no credit derogatory mark when completed successfully.

Does a loan modification hurt your credit score?

Yes, significantly. Most lenders require delinquency before approving a modification, and those late payments drop your score 50 to 150 points. The modification itself is noted as "modified" or "not paid as agreed" on your credit report, which lenders treat as a derogatory mark for the duration of the 7-year reporting window.

How much does a loan modification save per month?

Monthly savings depend on the size of the rate reduction and any term extension. A borrower with a $300,000 balance seeing their rate drop from 7.5% to 5.5% with a 30-year term saves approximately $395 per month. A term extension from 20 to 30 years at the same rate saves roughly $300 to $500 per month on principal and interest but substantially increases total interest paid over the life of the loan.

Can you refinance after a loan modification?

Yes, with a mandatory waiting period. Most conventional lenders require 12 to 24 months of consecutive on-time payments post-modification. FHA Streamline refinances require 12 months. The credit score damage from the modification also needs time to recover, and in practice most borrowers wait 2 to 4 years before refinancing produces a better rate than the modified rate they already have.

What is the break-even point on a refinance?

The break-even point is calculated by dividing total closing costs by monthly payment savings. If closing costs are $8,500 and monthly savings are $251, break-even is 34 months. If you sell or move before 34 months, the refinance costs you money rather than saving it. The break-even calculation is essential before committing to a refinance regardless of how attractive the rate appears.

Is a loan modification considered a derogatory mark?

Yes. A modification is typically reported as "modified" or "not paid as agreed" on your credit tradeline, which lenders classify as a derogatory event. It can affect mortgage eligibility for future home purchases, rental applications, and any other lending decision for up to 7 years from the date of first delinquency associated with the modification process.

How long does a loan modification take to process?

Standard loan modifications take 30 to 90 days from application submission to approval. Government-backed programs under Fannie Mae or Freddie Mac guidelines, or FHA formal loss mitigation programs, can take 3 to 6 months including the Trial Payment Plan period. Under CFPB mortgage servicing rules, servicers must acknowledge a complete application within 5 business days and evaluate it within 30 days of receiving a complete package.

Related Reads and Sources

- I Paid My Collection and My Score Didn't Change — The FICO 8 mechanics that govern why paying collections produces no score improvement, and the correct sequence for addressing collection accounts if you are trying to improve your score before a refinance application.

- Pay Down Debt vs. Invest: The Financial Guide — The interest rate arbitrage framework that applies directly to refinancing decisions: when does reducing your mortgage balance produce better returns than investing the same capital, and how to model the decision with your specific numbers.

- Credit Repair vs. Debt Settlement — If unsecured debt is suppressing your score and preventing refinance eligibility, understanding the difference between credit repair and debt settlement determines which path restores your score faster and with less long-term credit damage.

- CFPB: What Is a Loan Modification? — Official federal guidance on loan modification programs, borrower rights under CFPB mortgage servicing rules, the Trial Payment Plan process, and how to escalate if a servicer fails to evaluate your application within regulatory timelines.

- CFPB: How to Find the Best Mortgage Loan — The CFPB's data showing that borrowers who obtain 5 lender quotes save an average of $3,000 over the life of the loan versus those who take the first offer, and the Loan Estimate comparison framework for evaluating multiple refinance offers.

- HUD: Avoiding Foreclosure — The Department of Housing and Urban Development's full framework of foreclosure avoidance options including modification, forbearance, repayment plans, and how to access a free HUD-approved housing counselor who can review your full financial picture and identify accessible options.

- Federal Reserve: Selected Interest Rates (H.15) — Weekly benchmark interest rate data including the primary source for 30-year fixed mortgage rate trends used in refinancing decisions. Comparing your current rate against the H.15 30-year rate provides a baseline for whether refinancing is worth modeling in detail.