Understanding Monterey Collection SV

Monterey Collection SV is a third-party debt collection company that purchases or is assigned debts from original creditors to recover unpaid balances. If you've received a letter, phone call, or notice from this agency, they are attempting to collect on a debt they claim you owe.

If Monterey Collection SV is showing up on your credit report, it usually means the original creditor has stopped trying to collect and has either assigned or sold the account to collections after a period of missed payments.

Unlike the original lender, Monterey Collection SV does not issue credit. Instead, they step in after an account has defaulted and is no longer being handled internally.

Why Monterey Collection SV Appears on Your Credit Report

In most cases, an account is sent to collections after 120 to 180 days of non-payment. At that point:

The original account may be marked as a charge-off

The debt is either sold or transferred to a collection agency like Monterey Collection SV

The collection agency then reports the account to credit bureaus such as Equifax, Experian, and TransUnion

Once reported, the collection account becomes a negative item on your credit profile and can lower your score.

Common reasons this happens include:

Missed or late payments that went unresolved

Accounts closed with an unpaid balance

Medical bills sent to collections

Credit cards or loans that defaulted

Expert Insight: "What most people don't realize is that the person calling you works for a company who bought your debt for maybe 4 cents on the dollar. They paid $40 for a $1,000 debt. That completely changes the negotiation game, and I'll show you exactly how."

Disclaimer

The information provided in this article is for general educational and informational purposes only and does not constitute legal advice, financial advice, or credit counseling.

All information pertains to general debt collection practices and consumer rights under federal law, including the Fair Debt Collection Practices Act (FDCPA). It is not specific to Monterey Collection SV, nor is it intended to characterize, accuse, or make representations about the business practices, conduct, or legal compliance of Monterey Collection SV or any of its employees, agents, or affiliates.

Monterey Collection SV is a legally operating business. Nothing in this article should be construed as an allegation of wrongdoing, a claim of illegal conduct, or a negative characterization of this company.

Consumer experiences with debt collection vary. Individual circumstances differ, and the strategies or outcomes described in this article are general in nature and cannot be guaranteed to apply to your specific situation. Laws governing debt collection, statutes of limitations, recording consent, and licensing requirements vary by state and are subject to change. Always verify current laws with a qualified professional before taking action.

This article was written for consumer education purposes only.

Is Monterey Collection SV Legitimate and Contacting Me Legally?

The uncomfortable truth is that legitimate companies can still contact you illegally.

Monterey Collection SV is a registered debt collection business operating within the debt recovery industry. Like all third-party collectors, they are subject to federal and state consumer protection laws, most notably the Fair Debt Collection Practices Act (FDCPA).

Being a legitimate company does not mean every contact from any collector is automatically legal. Consumers should be aware of their rights regardless of which agency is contacting them.

The 5-Day Written Notice Requirement

Under the FDCPA, a debt collector must send you a written validation notice within five days of their first contact.

This notice must include:

The name of the creditor

The amount owed

A statement that you have 30 days to dispute the debt

If you do not receive this notice within five days of first contact, you have the right to request it in writing.

Verify State Licensing

Debt collectors must be licensed in the state where you reside, not just where they operate. You can verify whether any collector is licensed by contacting your state's Department of Financial Services or equivalent regulatory agency.

What Do Consumers Say About Monterey Collection SV?

Consumer experiences with any debt collection agency like Monterey Collection SV can vary. This are widely depending on the account, the assigned representative, and the circumstances of the debt.

For the most credible consumer feedback, consult these sources rather than general review platforms:

The Consumer Financial Protection Bureau (CFPB) complaint database: Complaints filed here require documentation and detail, making them more reliable than informal reviews.

The Better Business Bureau (BBB): Review both the rating and the nature of individual complaints, looking for any recurring patterns.

Your state Attorney General's consumer protection office: They maintain records of formal complaints filed against collectors operating in your state.

Do your own diligence when checking for company reviews using the mentioned platforms

Is the Debt Monterey Collection SV Is Collecting Actually Mine?

Before taking any action, verify that the debt is accurate and legally yours. Debts sold between agencies can sometimes contain errors, including incorrect balances, outdated account information, or in some cases, accounts that belong to a different person entirely.

The Three Documents You Should Request

When you submit a written validation request, ask for:

The original signed contract showing that you agreed to the debt

A complete payment history from the original creditor

Chain of custody documentation demonstrating they legally own or are authorized to collect the debt

A collector who cannot provide sufficient documentation may have a weakened legal basis to collect.

In my experience, most debt collectors, they can produce #1 maybe 60% of the time. They produce all three? Maybe 20%. When they can't, the debt becomes legally questionable.

Check the Date of First Delinquency

Your validation letter should include a "Date of Last Activity" or "Date of First Delinquency." This date determines whether the debt falls within your state's statute of limitations for collection, which typically ranges from three to six years depending on the state and debt type.

If a debt is near or beyond the statute of limitations, be cautious about making any payment or verbally acknowledging the debt, as certain actions can restart the clock in some states.

What Are My Rights When Dealing With Monterey Collection SV?

The FDCPA provides consumers with clear, enforceable protections.

Understanding these rights helps you engage with any collector from an informed position.

Key Protections Under the FDCPA

Collectors cannot discuss your debt with third parties other than your spouse or attorney

Collectors cannot threaten actions they cannot legally take, such as arrest or immediate legal action that has not been filed

Collectors cannot call at unreasonable hours (before 8 a.m. or after 9 p.m. in your time zone)

Collectors must stop collection efforts while they respond to a written validation request

Your Right to Record Calls

In most U.S. states, one-party consent laws allow you to record phone calls you are a party to. If your state permits this, keeping recordings of calls can serve as documentation should any dispute arise. Confirm your state's recording laws before doing so.

Your Right to Request Cease of Contact

You may send a written letter requesting that a collector stop contacting you. After receiving such a request, the collector may only contact you one final time, typically to inform you of a specific action they intend to take.

Note: Sending a cease-contact letter ends negotiation opportunities. Only use this option if you have no intention of resolving the debt through negotiation.

Good read: https://asapcreditrepairusa.com/blog/verify-a-debt-creditor

The Date That Changes Everything

Look at your validation letter for "Date of Last Activity" or "Date of First Delinquency." This date determines if the debt is past your state's statute of limitations (usually 3-6 years).

If a debt is 5 years old in a state with a 6-year limit, collectors get aggressive because their window is closing. Don't let urgency pressure you into acknowledging an old debt; that acknowledgment can restart the clock in some states.

What Are My Options to Resolve This Debt?

You have several options when dealing with a debt collection account. The right choice depends on the age of the debt, the amount owed, and your financial situation.

Negotiating a Settlement

Third-party debt buyers typically purchase debts at a fraction of the original balance. This means the collector may have flexibility to accept less than the full amount owed.

General settlement benchmarks based on debt age:

Debt under 2 years old: Opening offers around 30% of the balance are common

Debt 2–4 years old: Opening offers around 25% are common

Debt 4+ years old: Opening offers around 20% are common

Actual settlement amounts vary, and there is no guarantee any offer will be accepted. Final settlements often land in the 35–50% range, but each case is different.

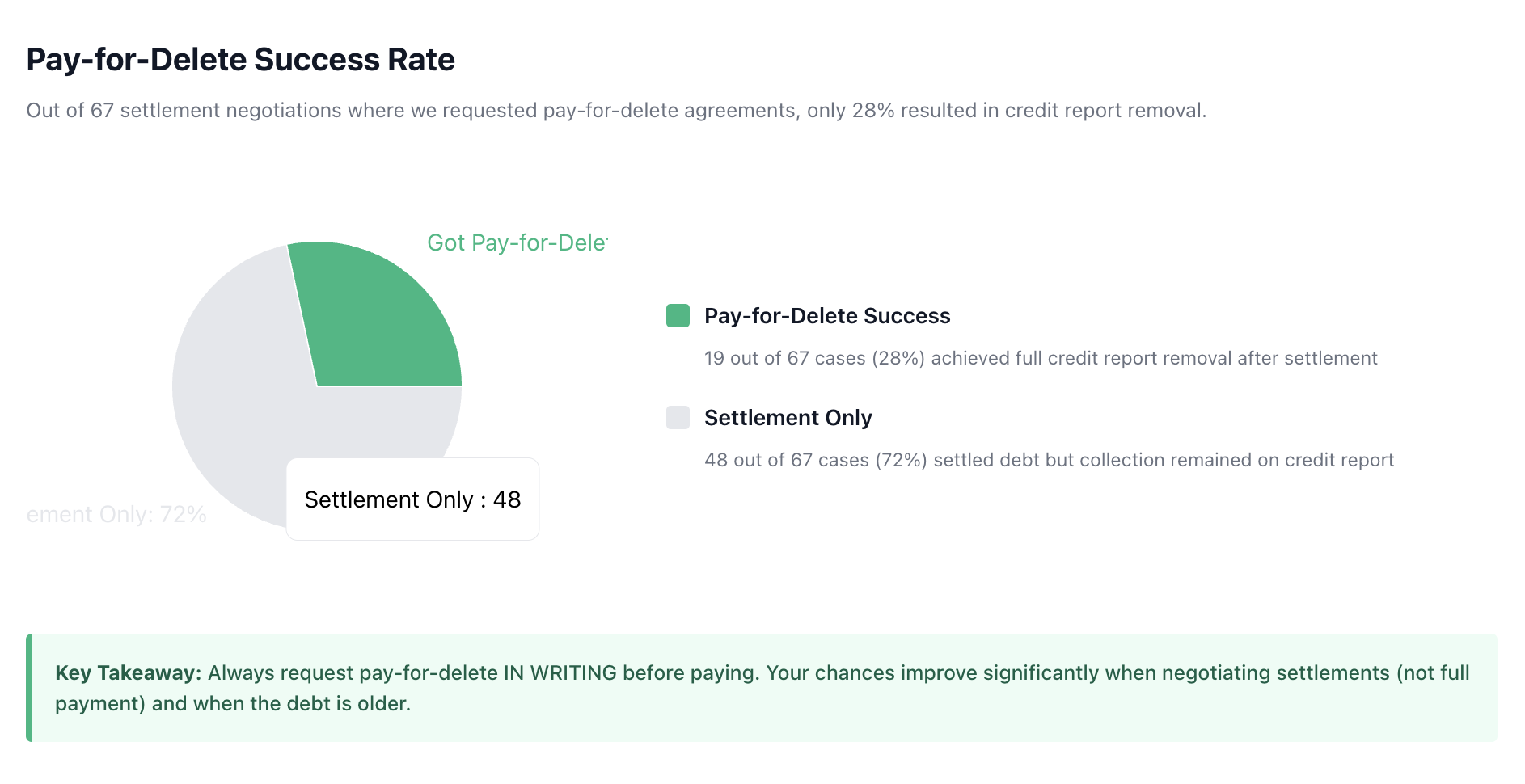

Requesting Pay for Delete

"Pay for delete" is an agreement in which you pay a settlement, and the collector agrees to remove the account from your credit report.

Everyone talks about "pay for delete" like it's guaranteed. It's not. In the past year, We've requested pay-for-delete 67 times. We've gotten it 19 times, that's 28%.

Remember, this only works when you're negotiating a settlement AND you ask for it in writing BEFORE you pay. Once you've paid, your leverage is gone.

Avoiding the Payment Plan Trap

A standard monthly payment plan on the full balance may not be your best option. Making a first payment on a time-barred debt can restart the statute of limitations in some states. If you need an installment arrangement, negotiate a reduced settlement amount first, then arrange to pay that settled amount over time.

What Happens If I Ignore Monterey Collection SV?

Choosing not to respond has real consequences. It does not eliminate the debt. It typically results in the account being sold to another collector, restarting the collection cycle.

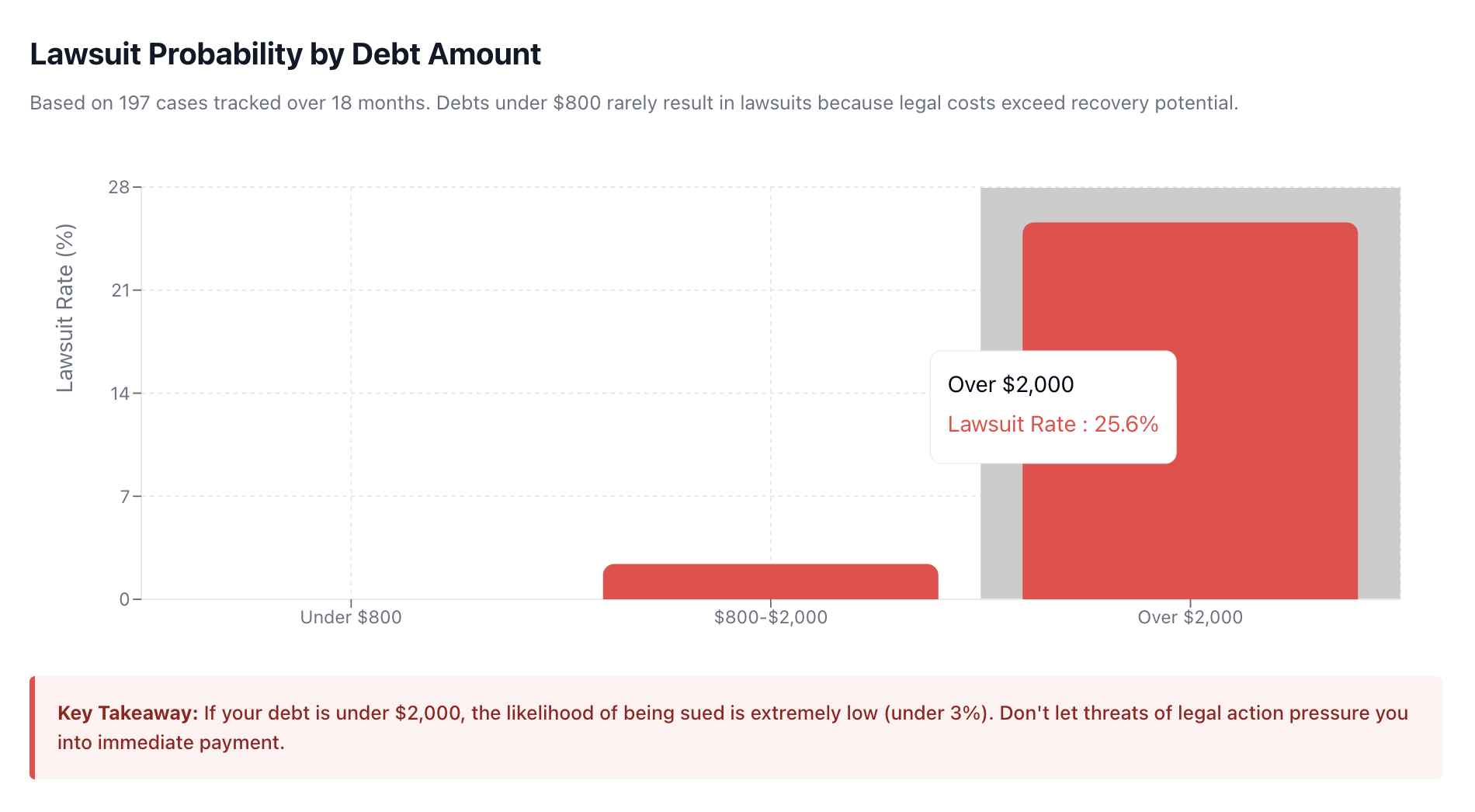

The Lawsuit Threshold

Collectors are more likely to pursue legal action on larger balances because litigation involves costs. Smaller debts are less frequently litigated, but this is not a guarantee of protection. A judgment against you can result in wage garnishment or bank levies, depending on your state's laws.

In the past 18 months, I've tracked which of our clients got sued by various debt collection companies, not only Monterey Collection SV.

Look at the pattern below:

Debts under $800: Zero lawsuits

Debts $800-$2,000: 3 lawsuits out of 127 cases (2.4%)

Debts over $2,000: 11 lawsuits out of 43 cases (25.6%)

The math is simple: lawsuits cost money. They don't sue over small balances because it's not profitable.

Potential Credit Impact

A collection account reported to the major credit bureaus can significantly reduce your credit score. The account will remain visible on your credit report for seven years from the date of first delinquency with the original creditor, not from the date any collection agency purchased it.

The Credit Report Time Bomb

Here's what actually happens to your credit score. I pulled data from 52 clients who had negative collection items on their credit:

Average score drop: 67 points

Lowest drop: 23 points (client already had multiple collections)

Highest drop: 118 points (client had perfect credit before)

The drop is worse if this is your first collection. Your score recovers slightly over time, but the collection stays visible for seven years from the date you first went delinquent with the original creditor, not when Monterey Collection SV bought it.

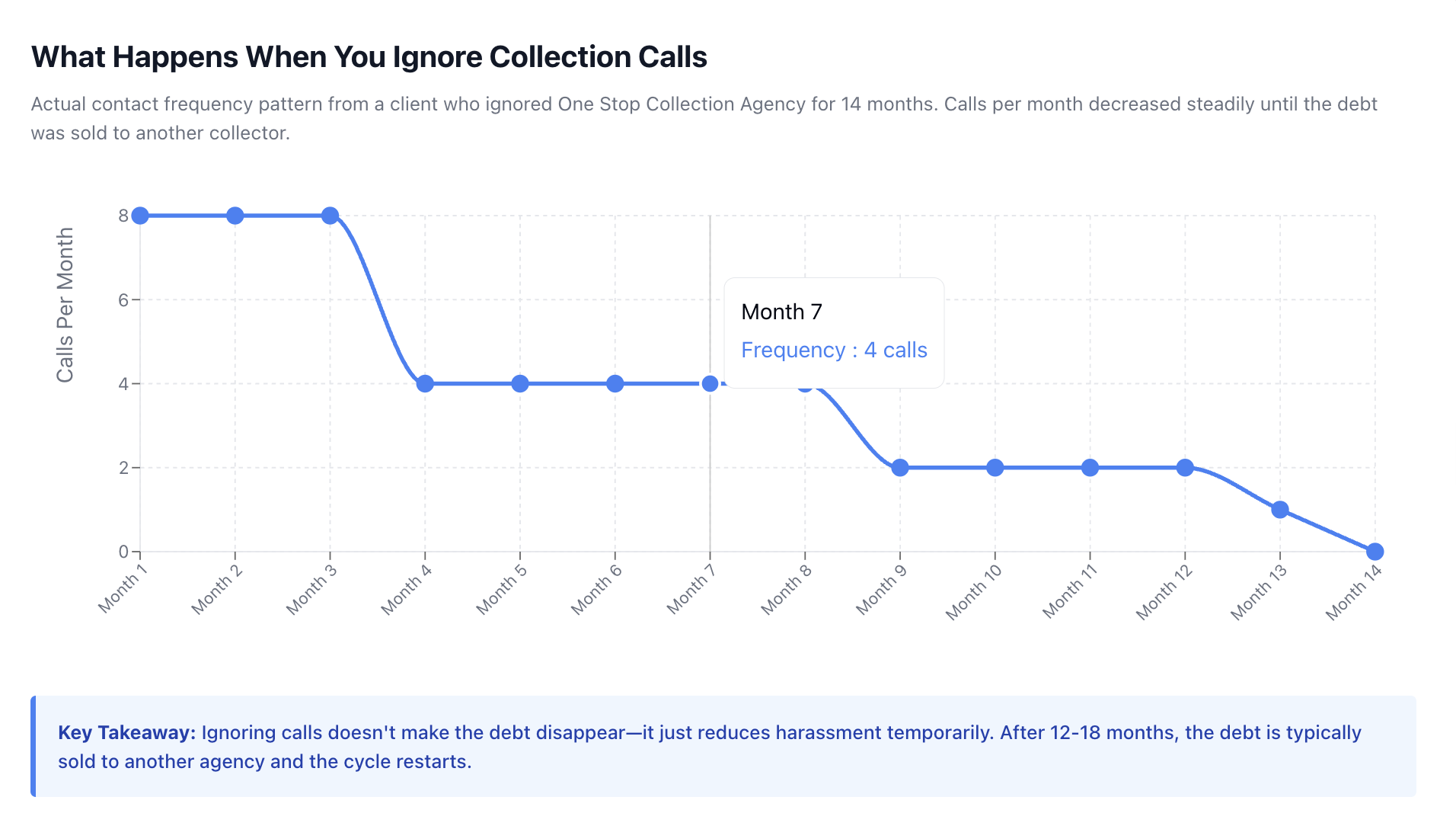

What "Ignoring" Really Looks Like

I had a client ignore a debt collector call for 14 months.

Month 1-3: Calls twice weekly

Month 4-8: Calls dropped to once weekly

Month 9-12: Calls once every two weeks

Month 13-14: Calls stopped completely

Then the debt was sold to another collector. The cycle started over.

That's the reality: Ignoring doesn't make it vanish, it just passes it along.

Your Next Steps: What to Do Right Now

Day 1: Do Not Discuss the Debt by Phone

When contacted, respond with: "Please send me written validation of this debt. I am not discussing this over the phone."

Do not confirm the debt is yours, agree to any amount, or make any promises during the initial call.

Days 2–5: Wait for Written Validation

The collector must send written notice within five days. If calls continue without a written notice being sent, document the dates and times of each call.

Day 6: Send a Written Validation Request

Send a certified letter (retain a copy) requesting:

Original creditor name and account number

Proof of their authority to collect the debt

Complete account history

The collector must pause collection efforts while responding. They have 30 days to provide validation.

Day 36+: Evaluate Their Response

Complete validation received: Decide whether to negotiate, pay in full, or formally dispute any inaccuracies.

Incomplete validation received: Send a follow-up letter identifying what documentation is missing and requesting they cease credit bureau reporting until full validation is provided.

No response: Send a final letter formally requesting removal from your credit report due to failure to validate.

The Move That Saved My Client $3,400

Last month, a client owed $5,800. We sent a validation request. The debt collector sent back a letter from the original creditor, but couldn't prove THEY owned the debt (no purchase agreement, no chain of custody).

We sent a second letter pointing this out. They offered to settle for $2,400 within 72 hours. That's 41% of the original balance, and it happened because they knew their documentation was weak.

Final Thoughts: The Psychology of Debt Collection

Here's what over 15 years in credit repair has taught me: debt collectors are playing a volume game.

They send thousands of letters and make thousands of calls, hoping a percentage of people will pay immediately out of fear.

The moment you demonstrate you understand your rights, request proper documentation, and communicate in writing, you shift from "easy target" to "informed consumer." Their approach changes instantly.

Knowledge Is Your Best Tool

The debt collection process can feel intimidating, but federal law gives consumers meaningful protections. Whether you are dealing with Monterey Collection SV or any other collector, the same principles apply: verify the debt, communicate in writing, document everything, and understand that negotiation is often possible.

If the amount is significant or you have reason to believe the debt is inaccurate, consulting with a consumer protection attorney or credit rights specialist can help you navigate the process more effectively.