Received a Notice of Default. How many days do you actually have?

In most cases, the notice gives a limited window, often around 30 days, to bring the account current or take action. The exact timeline depends on the type of debt, the terms of the agreement, and state law.

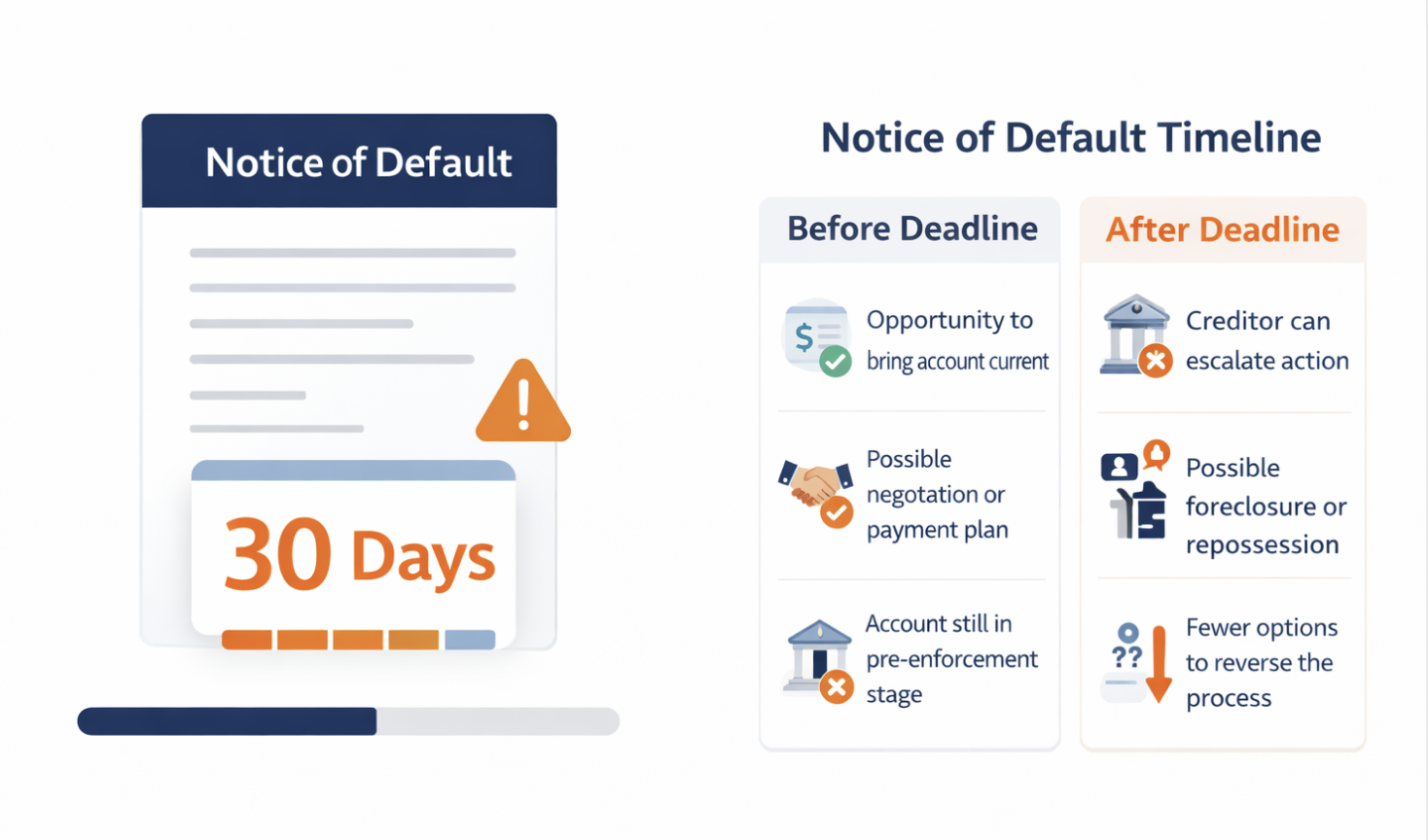

A Notice of Default is a formal step. It signals that the account is in serious delinquency and that the creditor is preparing to move forward if the issue is not resolved. In files we review, this is the stage where options still exist, but time is limited. Some assume they have more time than they do or wait for another notice. The timeline usually continues whether action is taken or not.

The number of days is not just a deadline. It is the period where you can still cure the default, negotiate terms, or stop escalation. Once that window closes, the next step may involve foreclosure, repossession, or legal enforcement, depending on the account.

This article explains how many days a Notice of Default typically gives, what affects that timeline, and what actions can be taken before the deadline expires.

Updated April 2026 · Sources: CFPB mortgage foreclosure guidance, Nolo foreclosure timeline guide, California Civil Code 2924 (AB 2424 2024 update), HUD housing counseling resources, Upsolve mortgage reinstatement guide September 2025

- 120 days minimum delinquency before a lender can legally begin the foreclosure process under CFPB rules. Most lenders wait until 90 to 150 days of missed payments.

- In nonjudicial states (California, Texas, Georgia, Arizona), you have approximately 90 days after the Notice of Default to cure before a sale can be set.

- In judicial states (New York, Florida, New Jersey, Illinois), the process goes through court. You typically have 20 to 35 days to file a response after being served.

- You can stop foreclosure even after a Notice of Default through reinstatement, loan modification, forbearance, repayment plan, short sale, or bankruptcy.

- Ignoring the notice is the worst response. Each day of inaction narrows your options. The notice does not close options - inaction does.

- A HUD-approved housing counselor provides free guidance and can negotiate with your servicer on your behalf. Call 1-800-569-4287.

What Is a Notice of Default?

The notice contains your name and property address, the name of your lender or servicer, a description of the default (typically a list of missed payments and the dates), the total amount required to cure the default, and instructions for how to pay. That total - all missed payments plus late fees and costs - is called your reinstatement amount.

Under federal law governed by the CFPB, servicers cannot begin the foreclosure process until you are at least 120 days behind on your mortgage. This means by the time you receive a Notice of Default, you have already missed at least four monthly payments and the damage to your credit has already occurred. The notice itself is not the credit event. The missed payments are.

How Many Days Do You Actually Have?

| State | Type | Days After NOD to Sale | Respond-by Deadline | Key Rule |

|---|---|---|---|---|

| California | Nonjudicial | 90 days cure + 20 days notice | 90 days to reinstate | AB 2424 (2024) adds delay rights for listed properties |

| Texas | Nonjudicial | 20 days after notice of sale | 20 days from sale notice | One of the fastest; total process as short as 41 days |

| Georgia | Nonjudicial | 30 days from notice of sale | 30 days from notice | No post-sale redemption right |

| Florida | Judicial | 4 to 18+ months | 20 days to respond to summons | Court process; lender must file lawsuit |

| New York | Judicial | 12 to 36+ months | 20 to 30 days to respond | Mandatory settlement conference can add months |

| New Jersey | Judicial | 4+ months (often 12+) | 35 days to file Answer | NJ Fair Foreclosure Act requires specific notices |

| Illinois | Judicial | 7 to 12+ months | 30 days to respond to summons | 10-year statute of limitations for lenders to file |

| Arizona | Nonjudicial | 90 days after notice | 90 days to reinstate | Trustee sale must be published 3 times |

As the CFPB's foreclosure guidance states, the legal foreclosure process cannot start until you are at least 120 days behind. After that point, the timeline depends on your state. Your single most important action on the day you receive the notice is to read it, write down the cure deadline, and call your servicer.

What Happens If You Ignore a Notice of Default?

Your Options After Receiving a Notice of Default

Two additional options apply when staying in the home is not possible: a short sale (selling the property for less than you owe with lender approval) and a deed in lieu of foreclosure (transferring the title to the lender voluntarily). Both are better credit outcomes than a completed foreclosure. After a foreclosure, you must wait 7 years to qualify for a conventional mortgage. After a deed in lieu, that wait drops to 4 years.

How to Respond to a Notice of Default: Step by Step

- Read the notice today and find your cure amount and cure deadline. The reinstatement amount is the total you must pay to fully cure the default. The cure deadline is when that window closes and the lender can move forward with the sale. Write both numbers down. Set a calendar reminder for 10 days before the deadline.

- Call your servicer's loss mitigation department within 48 hours. Ask specifically for the "loss mitigation" or "home retention" department, not general customer service. Explain you received a Notice of Default and want to discuss your workout options. Federal dual-tracking rules require servicers to review a complete loss mitigation application before proceeding with foreclosure. That protection only applies if you apply. Ask what forms you need and what the documentation deadline is.

- Contact a HUD-approved housing counselor the same week. HUD counselors provide free guidance, review your finances, help you understand which programs you qualify for, and can communicate with your servicer on your behalf. Call 1-800-569-4287 or visit HUD.gov. This service is free and significantly improves your outcome. Counselors have established relationships with servicer loss mitigation departments.

- Submit your application in writing with all required documents. Most servicers require recent pay stubs, two years of tax returns, bank statements, a hardship letter, and a completed financial worksheet. Incomplete applications are denied. A partial application buys no time. Submit everything requested on the first submission. Send by certified mail and email if possible so you have delivery confirmation.

- Get every agreement in writing and confirm the foreclosure is on hold. Once a workout agreement is in place, confirm in writing that the servicer has paused the foreclosure process pending review or approval. Federal rules prohibit dual-tracking (pursuing foreclosure while a complete loss mitigation application is under review), but you must have the application submitted to trigger that protection.

If your default stems from a lump-sum financial crisis rather than an ongoing inability to pay, the distinction between reinstatement and a negotiated workout matters. Our breakdown of lump sum versus payment plan strategies covers when paying a large amount at once produces a better outcome than a structured repayment plan, how to calculate what you can realistically raise, and how to approach that conversation with a servicer from a position of information.

Does the Notice of Default Affect Your Credit Score?

A completed foreclosure stays on your credit report for 7 years from the date of the first missed payment. If you resolve the default through reinstatement or modification before the foreclosure completes, the foreclosure notation does not appear. The missed payments remain, but the score trajectory changes significantly once the account returns to good standing.

As Nolo's foreclosure timeline guide explains, the distinction between a judicial and nonjudicial state matters for credit, too. Judicial foreclosures move through court and produce a court judgment that can appear separately in the public records section. Nonjudicial foreclosures do not produce a court judgment unless the lender separately sues for a deficiency. Either way, stopping the foreclosure before it completes is better for your credit than letting it proceed.

If you ultimately cannot keep the home, understanding what happens after a judgment or a sale is important. Our article on settling debt after a judgment covers how judgments appear on credit reports, what Satisfaction of Judgment means, and how to address the credit reporting after a court-ordered resolution.

Frequently Asked Questions

How many days do I have after receiving a Notice of Default?

In nonjudicial states like California, Texas, Georgia, and Arizona, you typically have 90 days after the Notice of Default is recorded to cure the default by paying all past-due amounts, fees, and costs. After that window, the lender can issue a Notice of Trustee Sale and schedule the auction. In judicial states like New York, Florida, and New Jersey, you have 20 to 35 days to respond to the court summons after being served. Your specific deadline is printed on the notice itself.

What happens if I ignore a Notice of Default?

If you ignore the notice in a nonjudicial state, the lender issues a Notice of Trustee Sale, sets an auction date, and your home is sold without any court involvement. In judicial states, the lender files a lawsuit and if you do not respond to the summons, a default judgment is entered automatically and the sale proceeds. Either way, the foreclosure completes, you lose the home, carry a foreclosure on your credit report for 7 years, and may owe a deficiency judgment on any remaining balance. Ignoring the notice removes options - it does not remove obligations.

Can I stop foreclosure after receiving a Notice of Default?

Yes. A Notice of Default begins the foreclosure process but does not end your options. You can stop foreclosure through reinstatement (paying all past-due amounts), a loan modification (restructuring your loan terms), a forbearance agreement (pausing payments temporarily), a repayment plan (catching up over 3 to 6 months), a short sale (selling the property with lender approval), a deed in lieu of foreclosure, or by filing for bankruptcy which triggers an automatic stay that immediately halts all collection and foreclosure action. Contact your servicer and a HUD-approved counselor as soon as possible.

What is the difference between a Notice of Default and a Notice of Trustee Sale?

A Notice of Default is the first formal step, issued after 120 days of missed payments. It gives you a cure period - typically 90 days in nonjudicial states. A Notice of Trustee Sale is issued after the cure period expires without resolution. It sets the actual date for the public auction of your home. In California, the lender must wait at least 20 days after recording the Notice of Trustee Sale before holding the auction. Once the Notice of Trustee Sale is issued, your reinstatement window typically closes. The Notice of Default is the critical window - that is when you have the most options available.

Does a Notice of Default hurt your credit score?

The Notice of Default is a public record filed with the county recorder. The larger credit damage came earlier: 90 or more days of missed mortgage payments is already a significant negative on your credit report before the notice is filed. A completed foreclosure stays on your report for 7 years. Stopping the foreclosure through reinstatement or modification prevents the foreclosure notation from appearing and significantly limits further damage. A loan modification returns the account to good standing on your report once completed.

What is a reinstatement amount and how do I get one?

A reinstatement amount is the total you must pay in one lump sum to bring your loan current and stop the foreclosure. It includes all missed monthly payments, late fees, inspection fees, attorney fees the lender has incurred, and any other costs. Call your servicer and request a written reinstatement quote. Ask for the "good through" date on the quote - that is when the amount expires and a new (higher) amount would apply. Pay before the expiration date. Get written confirmation that the foreclosure process has been stopped after payment is received and processed.

Missed Payments Already on Your Report? Let's See What Can Be Fixed.

The missed payments that led to your Notice of Default are already on your Experian, TransUnion, and Equifax reports. A free 3-bureau audit shows exactly what is reporting, whether the dates are accurate, and which items are disputable under the FCRA - because errors in how missed payments are reported happen more than most people realize.

Get My Free Credit Audit → Secure · 2 minutes · No credit card required-

How to Settle Credit Card Debt After a Judgment If the foreclosure produced a deficiency judgment or you are also managing credit card debt alongside a mortgage default, this covers how judgments appear on your credit report, what Satisfaction of Judgment means, and how to resolve a judgment for less than the full amount.

-

Lump Sum Settlement vs Payment Plan: What's Smarter? Reinstatement requires a lump-sum payment. If you cannot reinstate in full, understanding whether a repayment plan or a lump-sum settlement serves you better on other debts helps you prioritize cash flow during a financial crisis where mortgage reinstatement is the top priority.

-

Credit Repair vs Debt Settlement: Which One Is Right for You? After a Notice of Default, your credit report will carry the damage of missed mortgage payments. This As Upsolve's mortgage reinstatement guide explains, servicers are required to evaluate all loss mitigation options before proceeding. This covers when credit repair addresses the damage effectively, when debt settlement changes the trajectory, and how to sequence both alongside an active foreclosure situation.

Closing

A Notice of Default sets a deadline that controls what options remain. The number of days depends on the agreement and state law, but the window is limited.

Acting within that period allows you to resolve the default or slow the process. Waiting reduces those options and increases the risk of enforcement.

The timeline does not reset. What matters is what you do before it expires.