Phone payments affect your credit score in ways most people get completely backwards. Paying your cell phone bill on time every month does not automatically build your credit. But missing one payment just one can damage your score for up to seven years. That asymmetry is the most important thing to understand before we go any further.

Running a credit repair company, this misconception comes up constantly. One case that stays with me involved a client who had been paying his cell phone bill on time for four years. He assumed that being alone was protecting or building his score. When he came to us, his score was 591, and he had no idea why. Four years of on-time phone payments had not added a single positive entry to his credit report. Carriers simply do not report them. What they do report is the bad stuff.

A recent r/personalfinance thread highlighted the same frustration, with dozens of users shocked to discover their years of on-time phone payments had never touched their credit file. (Source: r/personalfinance, reddit.com) According to Experian's 2025 data, the average U.S. credit score sits at 713. Yet, millions of consumers with clean phone and utility payment histories are stuck below that mark simply because those payments go unreported. (Source: Experian, 2025)

Does Paying Your Phone Bill Build Credit?

Paying your phone bill does not automatically build credit. Cell phone carriers AT&T, Verizon, T-Mobile, and most regional providers do not report your monthly service payments to Experian, TransUnion, or Equifax. That means years of on-time payments produce zero positive entries in your credit file.

This is the core problem. Credit scores reward repayment of borrowed money. A phone service bill is a payment for a service, not a debt repayment. Lenders and bureaus treat those differently.

Why Carriers Do Not Report to the Bureaus

Phone carriers check your credit when you sign up for a postpaid plan. They run a hard inquiry to assess whether you are likely to pay. But after that initial check, they typically stop sharing your account data with the bureaus unless something goes wrong.

The result is a one-sided system. Opening a new account can ding your score. Paying it perfectly for years does nothing. Falling behind sends a negative mark straight to all three bureaus.

How a Missed Phone Payment Damages Your Credit

Cell phone carriers report negative activity when you fall at least 30 days past due. At that point, the late payment enters your credit report and stays there for seven years from the original missed payment date.

The damage depends on two things: how late you are and what your score was before the miss.

Payment history is 35% of your FICO score, the single largest factor. A person with a score of 750 who misses a phone payment by 30 days can lose 90 points or more. A person already sitting at 620 may drop 40 to 60 points from the same event.

What Happens When a Phone Account Goes to Collections

Missing multiple payments leads to account termination. Once terminated, carriers send the unpaid balance to a collection agency. The collection agency then reports the debt to all three bureaus as a collection account.

Collection accounts are separate, additional negative marks. A phone bill that results in a collection entry creates two layers of credit damage: the original missed payments and the collection account itself. Both stay on your report for seven years.

In our office, we worked with 22 clients in the past six months who had collection accounts from phone carriers. In 17 of those 22 cases, the clients did not realize the account had gone to collections until they applied for a loan and got denied.

The Early Termination Problem

Ending a phone contract early without paying the termination fee also triggers a negative credit event. Many carriers treat unpaid termination fees the same as unpaid balances and send them to collections. This is one of the most overlooked sources of credit damage we see in credit repair cases.

Does Opening a New Phone Plan Hurt Your Credit Score?

Yes, but temporarily. Most carriers run a hard inquiry when you apply for a new postpaid plan or finance a phone through them. A hard inquiry can lower your score by up to 10 points. The impact fades within 12 months and disappears from your report entirely after 24 months.

If you are planning to apply for a mortgage, car loan, or personal loan within the next three to six months, think carefully before switching carriers or financing a new device. Each hard inquiry adds a small penalty at exactly the moment you want your score at its peak.

Hard inquiries from phone applications count as "new credit," which makes up 10% of your FICO score. One inquiry is manageable. Multiple inquiries in a short window compound the damage.

How to Get Credit for Your Phone Payments

Paying your phone bill, you're just not getting scored for it. Three strategies change that.

Strategy 1: Experian Boost

Experian Boost is a free tool that connects your bank accounts and scans your payment history for eligible recurring bills, including your cell phone, utilities, streaming services, and qualifying rent payments. It adds that history directly to your Experian credit file.

The results are real. According to Experian's own data, 62% of users who complete the Boost process see a score increase, with an average FICO Score 8 improvement of 13 points. For users who started with scores at or below 579, 87% saw improvement, averaging 22 points. (Source: Experian Boost Study)

Important limitations to know: Experian Boost only affects your Experian credit report and FICO Score. It does not change your TransUnion or Equifax files. Lenders who pull a different bureau will not see the boosted data. And Experian Boost only adds positive payment history; past late payments on those accounts do not get reported through the tool.

To use Experian Boost:

Create a free account at Experian.com

Connect the bank accounts or credit cards you use to pay your phone and utility bills

Experian scans up to 24 months of payment history

Verify the payments you want added to your file

Receive an updated FICO Score immediately

Strategy 2: Pay Your Phone Bill With a Credit Card

Charging your phone bill to a credit card and then paying the card in full each month creates two positive outcomes. First, the credit card issuer reports your on-time payment to all three bureaus. Second, regular use and on-time payment of a credit card builds the payment history that matters most to lenders.

This approach turns a bill that normally goes unreported into a monthly contribution to your credit score. The key discipline: pay the card balance in full every month. Carrying a balance negates the benefit and adds interest costs.

Some credit cards also offer cell phone protection insurance as a cardholder perk when you use the card to pay your bill. The card builds your credit and protects your phone. That is a genuinely useful combination.

Strategy 3: Finance Through the Phone Manufacturer or a Retailer

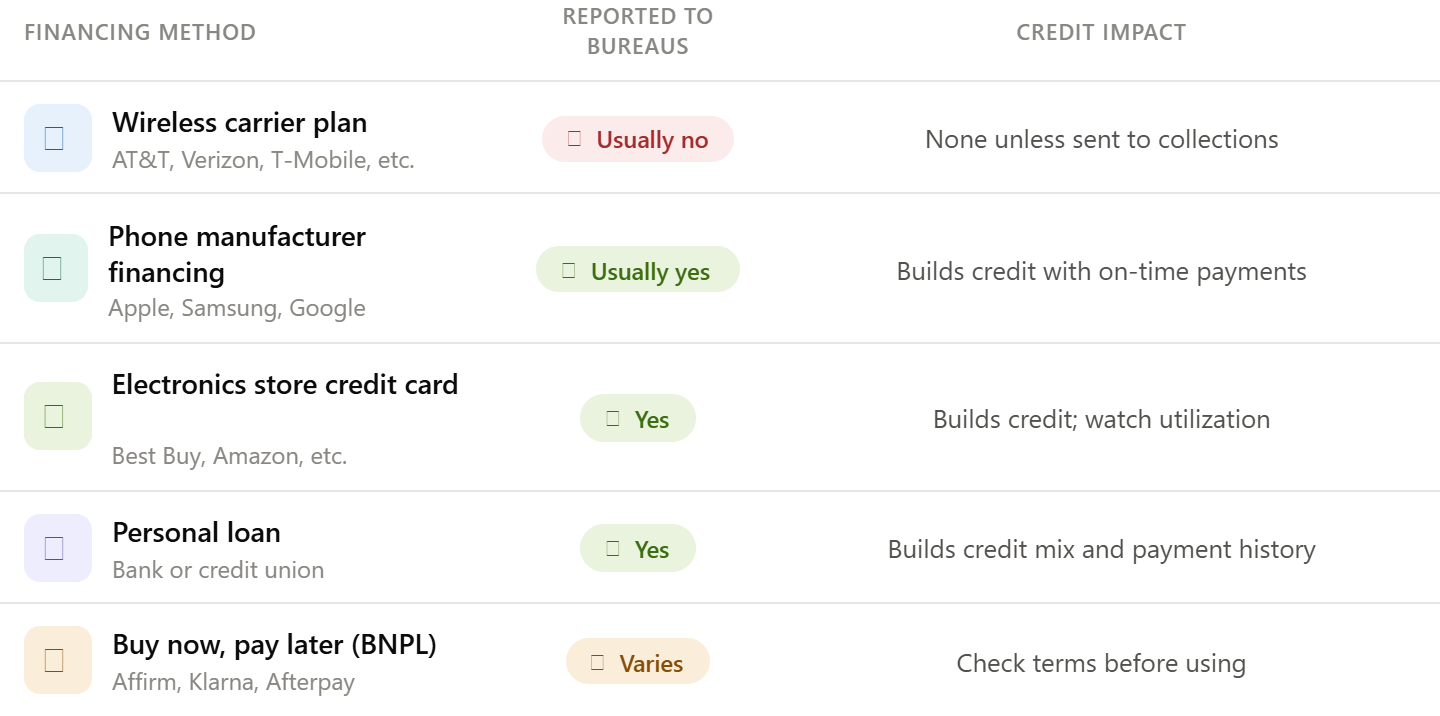

Wireless carrier financing rarely gets reported to the bureaus. Financing through the phone manufacturers Apple, Samsung, and Google often works differently. Manufacturers frequently use branded financing programs that function like credit accounts and do report payment activity to credit bureaus.

Financing through an electronics retailer like Best Buy using a store credit card also typically reports to the bureaus. Make monthly on-time payments, then build your credit history directly.

Before accepting any financing offer, ask the lender directly: "Do you report monthly payments to Experian, TransUnion, and Equifax?" If the answer is no, carrier financing is not a credit-building tool.

What to Do If You Cannot Afford Your Phone Bill This Month

Contact your carrier before the bill goes 30 days past due. This is the most important action you can take.

Most major carriers offer payment arrangements, split payments, due date changes, or temporary hardship plans when you reach out proactively. These options close once the account becomes delinquent. Calling after the 30-day mark is often too late to prevent a credit report entry.

Steps to take immediately if you are behind:

Call the carrier's billing department and ask about payment arrangements

Request a due date change to align the bill with your pay schedule

Ask whether a temporary reduced payment plan is available

If the account has already gone to collections, contact the collection agency and request a pay-for-delete agreement in writing before making any payment

Prepaid phone plans are also worth considering if consistent payment is difficult. With a prepaid plan, the provider receives payment before service is delivered. A missed month suspends service but produces no credit report entry because no debt exists to report.

Phone Financing and Credit Building: What Actually Gets Reported

Not all phone financing helps your credit. The method of financing determines whether your payments appear on your credit report at all.

If credit building is your goal, the financing method matters more than the device you are buying.

Are Phone Payments Hurting Your Credit Score?

Paying your phone bill on time may not build credit, but missed payments and collections can damage your score for years. Find out what is reporting, what can be disputed, and how to start improving your credit today.

Check Your Credit Report NowGet clarity before one missed payment turns into a bigger credit problem.

How to Check Whether Your Phone Account Appears on Your Credit Report

Pull your free credit reports from all three bureaus at AnnualCreditReport.com. Look for your wireless carrier's name under "accounts" or "tradelines." If you see it and payments are being reported, any on-time payments are building positive history. If you do not see it, your carrier is not reporting, meaning only negative events could ever appear.

Most consumers will not find their carrier listed under active accounts. They will only see a phone-related entry if a missed payment led to a collection. That is the standard setup for the U.S. wireless industry as it stands today.

Frequently Asked Questions

Does paying a prepaid phone bill build credit? No. Prepaid plans are not reported to credit bureaus. There is no debt associated with a prepaid account, so there is no credit entry of any kind, positive or negative.

Can a phone company check my credit without my permission? When you apply for a postpaid plan, you authorize a credit check by agreeing to the carrier's terms. For a prepaid plan, no credit check is required. If you are concerned about hard inquiries, prepaid is the way to avoid them entirely.

Will a disputed phone collection account be removed from my credit report? If a collection account is inaccurate, wrong amount, wrong account, or already paid, you can dispute it with the credit bureau under the FCRA. The bureau has 30 days to investigate. If the collector cannot verify the debt, the entry must be removed.

Does switching carriers hurt my credit? Signing up with a new carrier creates a hard inquiry, which can lower your score by up to 10 points temporarily. If you have an outstanding balance with the old carrier, make sure it is paid in full before switching. Unpaid balances from a closed carrier account frequently end up in collections.

How long does a phone-related collection account stay on my credit report? Seven years from the date of the original missed payment, not from the date the account went to collections or when you paid the balance.