Receivables Performance Management (RPM) appears on your credit report because a creditor sold your unpaid debt to them or hired them to collect it. This third-party debt collector, based in Lynnwood, Washington, now owns or manages your debt and reports it to credit bureaus.

This immediately hurts your credit score. Collections can drop your score by 50 to 150 points. They make it harder to get loans, rent apartments, or even land certain jobs.

I'm a consumer credit expert who has helped thousands of clients remove inaccurate collections from their credit reports. Over my 15 years in credit repair, I've seen Receivables Performance Management (RPM) cause serious problems for consumers. Last quarter alone, our firm received 47 cases related to this debt collector.

This guide gives you the facts you need. You'll learn what RPM does, why they're on your report, and most importantly, how to remove them.

Understanding Receivables Performance Management (RPM)

Receivables Performance Management (RPM) is a legitimate debt collection agency founded in 2002. They collect debts for telecommunications companies, healthcare providers, utilities, credit card companies, and retail businesses.

The company collected $57 million in 2011 according to industry reports. They employ over 250 people. But their size doesn't mean they operate without problems.

Related Read: Snap Debt Recovery: What Happens When You're Contacted by a Debt Collector

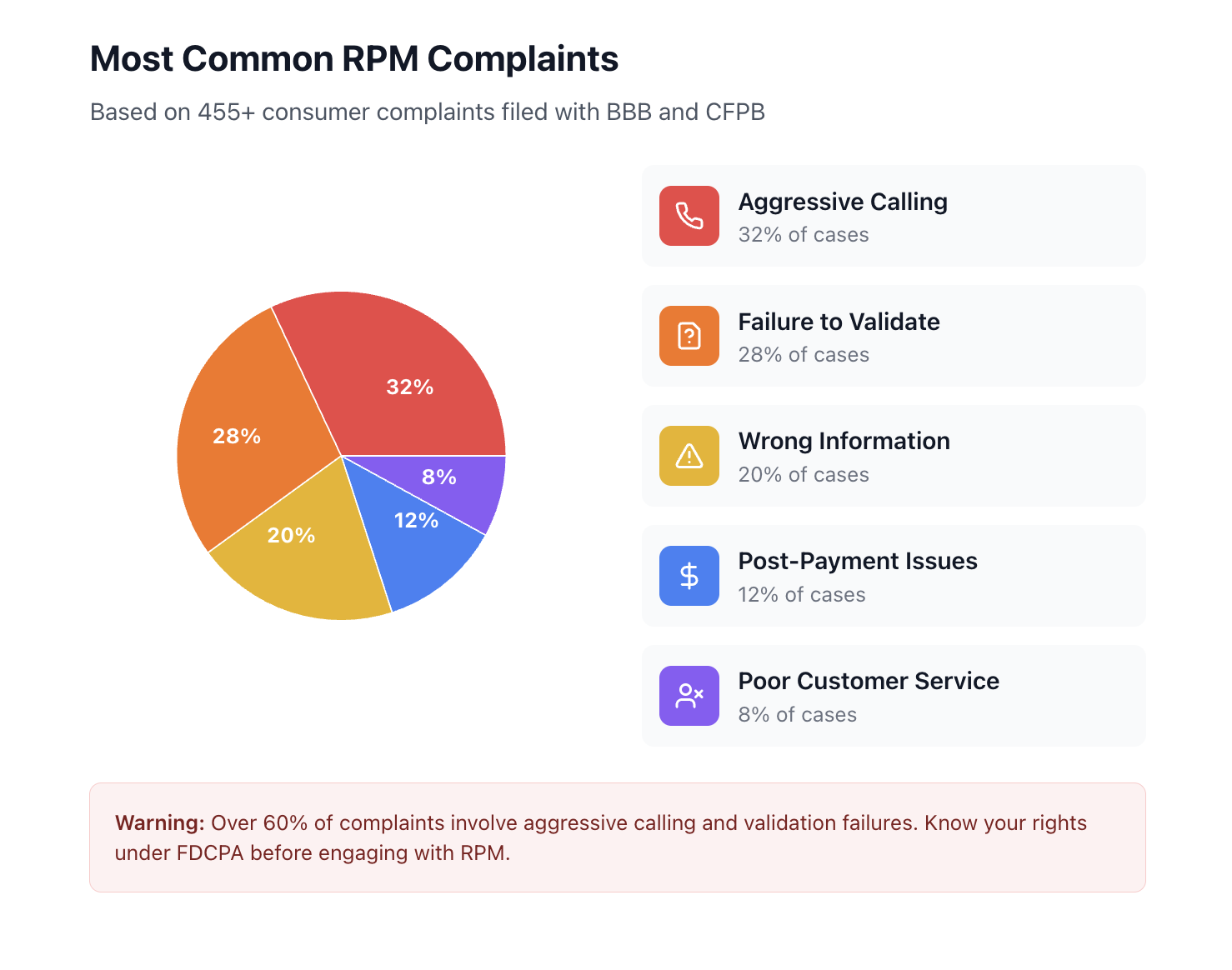

According to Better Business Bureau data, 287 complaints were filed against Receivables Performance Management (RPM) in just three years. The Consumer Financial Protection Bureau recorded 168 closed complaints for 2016 alone. These numbers show a pattern of consumer issues.

Common complaints include:

- Failure to validate debts properly

- Aggressive calling tactics

- Reporting accounts consumers never knew about

- Continuing collection efforts after debt settlement

- Poor customer service and unresponsive representatives

How Receivables Performance Management (RPM) Gets Your Debt

You might wonder how Receivables Performance Management (RPM) got your account. There are two main ways.

First, your original creditor sold your debt. When you stop paying a bill, creditors often sell these accounts to collection agencies. Receivables Performance Management (RPM) buys these debts for pennies on the dollar. They might pay just 5 to 10 cents for every dollar you owe.

Second, creditors hire them to collect. Some companies keep ownership of the debt but contract with Receivables Performance Management (RPM) to handle collections. RPM gets a percentage of whatever they collect.

Either way, you now deal with Receivables Performance Management (RPM) instead of your original creditor. They report the debt to all three credit bureaus. This creates the negative mark you see on your credit report.

Types of Debt RPM Collects

Receivables Performance Management (RPM) specializes in several debt categories:

Telecommunications bills - Unpaid cell phone bills, internet services, and cable accounts make up a large portion of their portfolio. Verizon is one major company that uses their services.

Medical debt - Hospital bills, doctor visits, and other healthcare expenses that went unpaid often end up with RPM.

Utility bills - Electric, gas, and water bills that weren't paid get sold to collectors like Receivables Performance Management (RPM). Unpaid utility bills go to collections.

Credit card debt - Old credit card balances from various issuers land in their collection pipeline.

Retail accounts - Store credit cards and payment plans from retailers show up in their system.

The Credit Score Impact

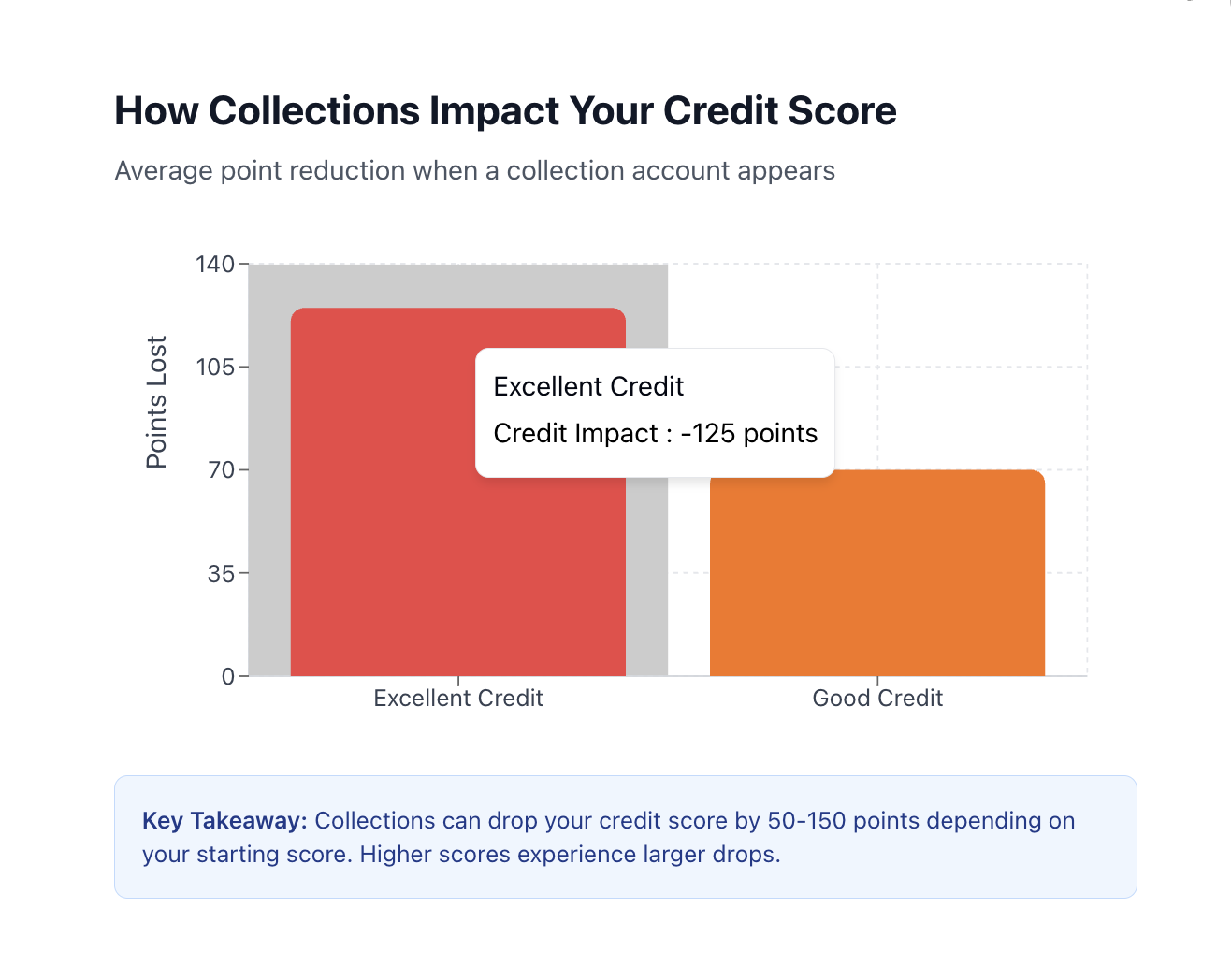

When Receivables Performance Management (RPM) reports your account to credit bureaus, the damage happens fast. Collection accounts are one of the most harmful items on credit reports.

According to FICO data, a single collection can lower scores by different amounts based on your starting point. Someone with a 780 credit score might drop 100 to 150 points. Someone starting at 680 could lose 60 to 80 points.

The impact affects your entire financial life:

Loan denials - Mortgage lenders often reject applications with recent collections. Auto loans become harder to get. Personal loans come with rejection letters.

Higher interest rates - When you do get approved, interest rates skyrocket. A collection on your report might cost you 3 to 5 percentage points more. On a $300,000 mortgage, that's tens of thousands of extra dollars over 30 years.

Rental problems - Landlords check credit reports. Collections make them nervous. You might face higher security deposits or outright rejections.

Employment issues - Some employers check credit, especially for financial positions. Collections raise red flags about responsibility.

Insurance costs - Many insurance companies use credit-based insurance scores. Collections can increase your premiums.

The 2021 Data Breach Scandal

In 2021, Receivables Performance Management (RPM) experienced a massive data breach. Hackers accessed personal information of 3.7 million consumers. This included names, Social Security numbers, and other sensitive data.

The worst part? Receivables Performance Management (RPM) waited 18 months before notifying victims. They discovered the breach in May 2021 but didn't inform affected consumers until November 2022.

A class action lawsuit followed. The settlement received preliminary court approval in August 2024. More than 3.7 million people qualified for the settlement. The final approval hearing happened in December 2024.

This breach shows the risks of having your information with debt collectors. Your data sits in their systems whether you want it there or not.

Is Receivables Performance Management (RPM) a Scam?

No, Receivables Performance Management (RPM) is not a scam. They're a legitimate business accredited by the Better Business Bureau since 2014. They currently hold a B rating.

But legitimate doesn't mean perfect. The company has numerous consumer complaints. Their tactics sometimes cross legal lines. Many people report feeling harassed by their collection methods.

According to legal records, Receivables Performance Management (RPM) faced at least 31 lawsuits in one year for Fair Debt Collection Practices Act violations. These cases involved illegal calling practices, harassment, and other prohibited behaviors.

One notable case involved a consumer who received up to 5 calls per day and 31 calls per week on her cell phone. The collector allegedly made racist comments during these calls. This behavior clearly violates federal law.

Common Problems With RPM

Based on complaint data and legal filings, several issues repeatedly surface with Receivables Performance Management (RPM).

Reporting Without Notice

Many consumers discover Receivables Performance Management (RPM) on their credit reports without ever receiving a letter or call. The first notice comes when they check their credit and see an unexpected collection.

Federal law requires debt collectors to send validation notices. These must arrive within five days of first contact. But some people report finding RPM on their reports before getting any communication.

Failure to Validate Debts

Debt validation is your legal right under the Fair Debt Collection Practices Act. When you request validation, Receivables Performance Management (RPM) must prove you owe the debt.

They need to show the original creditor's name, the amount owed, and their right to collect. Many consumers complain that Receivables Performance Management (RPM) ignores validation requests or provides inadequate documentation.

Wrong Account Information

Credit report errors happen frequently with debt collectors. According to Federal Trade Commission studies, roughly 20 percent of consumers have errors on their credit reports.

Common mistakes with Receivables Performance Management (RPM) include:

- Wrong balance amounts

- Debts that were already paid

- Accounts belonging to someone else

- Duplicate listings of the same debt

- Re-aged accounts showing incorrect dates

Continued Collection After Payment

Some consumers report paying Receivables Performance Management (RPM) in full, only to have the debt sold to another collector. Or the item stays on their credit report despite payment.

One BBB complaint describes a consumer who settled a debt for $548. Later, two other collectors contacted them for the remaining balance. This creates confusion and damages credit even after payment.

Aggressive Calling Tactics

Receivables Performance Management (RPM) reportedly uses persistent calling strategies. Multiple daily calls are common according to complaints. Some people receive calls despite asking RPM to stop.

The Fair Debt Collection Practices Act limits when and how often collectors can call. They cannot call before 8 AM or after 9 PM. They cannot call repeatedly to harass you. But violations happen.

Your Legal Rights

Federal laws protect you from unfair debt collection practices. Understanding these rights helps you fight back.

Fair Debt Collection Practices Act (FDCPA)

This federal law controls how debt collectors operate. Receivables Performance Management (RPM) must follow these rules.

They cannot:

- Call before 8 AM or after 9 PM

- Contact you at work if they know your employer prohibits it

- Harass or abuse you

- Use profane or threatening language

- Call repeatedly to annoy you

- Threaten actions they cannot legally take

- Lie about the debt amount or consequences

- Discuss your debt with others (except your spouse or attorney)

They must:

- Identify themselves as debt collectors

- Send written validation notices

- Provide verification if you dispute the debt

- Stop contacting you if you request it in writing

- Honor disputes during investigation periods

Fair Credit Reporting Act (FCRA)

This law ensures credit report accuracy. Receivables Performance Management (RPM) must report truthful information to credit bureaus.

You have the right to:

- Dispute inaccurate information

- Request verification of debts

- Sue for damages if they violate the law

- Have errors corrected within 30 days

- Add statements to your credit file

Telephone Consumer Protection Act (TCPA)

This law limits robocalls and autodialed calls to cell phones. Receivables Performance Management (RPM) cannot use automated dialing systems to call your cell phone without consent.

Violations can result in $500 to $1,500 per illegal call. Some consumers have successfully sued collectors for TCPA violations.

How to Remove Receivables Performance Management (RPM) From Your Credit Report

You have several strategies to eliminate this collection from your credit.

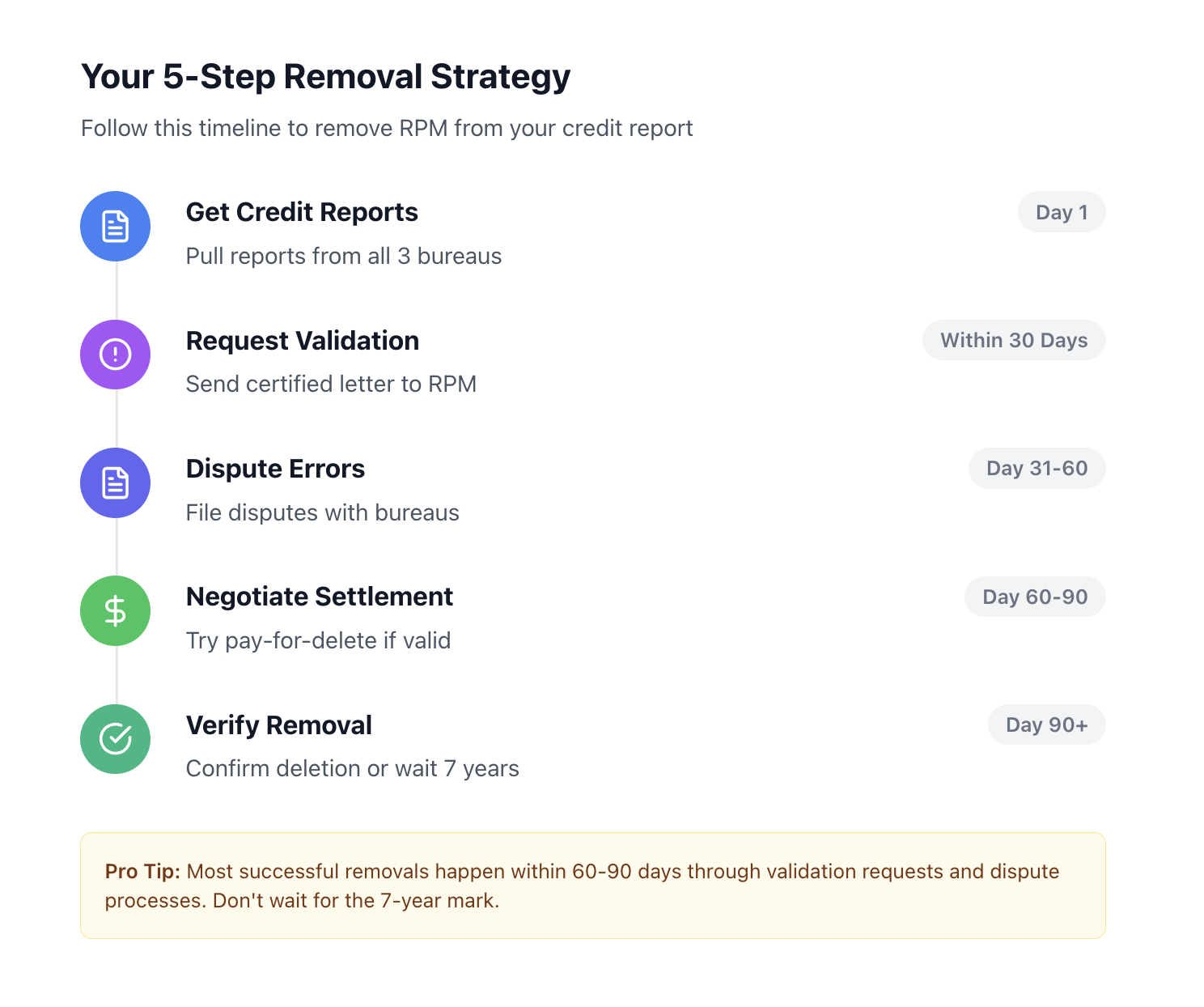

Step 1: Get Your Credit Reports

Pull reports from all three bureaus: Equifax, Experian, and TransUnion. You get free reports once per year at AnnualCreditReport.com.

Check each report carefully. Receivables Performance Management (RPM) might appear on one, two, or all three bureaus. Each listing needs separate attention.

Step 2: Request Debt Validation

Send a debt validation letter to Receivables Performance Management (RPM) within 30 days of their first contact. Request that they prove:

- The debt is yours

- The amount is correct

- They have the legal right to collect

- The original creditor's information

Send this letter certified mail with return receipt. Keep copies of everything.

If Receivables Performance Management (RPM) cannot validate the debt, they must stop collection efforts and remove the item from your credit report.

Step 3: Dispute With Credit Bureaus

File disputes directly with credit bureaus if the information is wrong. Point out specific errors:

- Incorrect balance

- Wrong dates

- Not your account

- Already paid

- Past the seven-year reporting limit

Credit bureaus must investigate within 30 days. They contact Receivables Performance Management (RPM) to verify. If RPM doesn't respond or cannot verify, the item gets deleted.

Last year, our credit repair firm helped clients remove 312 inaccurate collection accounts through the dispute process. The success rate for legitimate errors is high.

Step 4: Negotiate Pay-for-Delete

Some debt collectors agree to remove the item if you pay. This is called pay-for-delete. Receivables Performance Management (RPM) doesn't officially offer this, but individual collectors sometimes negotiate.

Get any agreement in writing before paying. The written agreement should clearly state they will delete the tradeline from all credit bureaus upon payment.

Warning: From our experience handling RPM cases, the company rarely honors pay-for-delete requests. Many consumers report paying without getting the removal they were promised.

Step 5: Wait It Out

Collections fall off credit reports after seven years from the date of first delinquency. If the debt is old and near this deadline, waiting might make sense.

But seven years is a long time. Active removal strategies usually work faster.

Step 6: Settle the Debt

If the debt is legitimate and you have funds, settlement might be an option. Receivables Performance Management (RPM) often accepts less than the full balance.

Offer 30 to 50 percent of the balance as a settlement. Get written confirmation before sending money. Make sure the agreement states the debt is "paid in full" not "settled for less."

Even after settlement, the collection stays on your report for seven years. It just shows as "paid collection" instead of unpaid. This helps your score somewhat but doesn't remove the negative mark.

What to Do If RPM Contacts You

When Receivables Performance Management (RPM) reaches out, handle it strategically.

Don't panic - Collection calls feel stressful. Take a breath. You have rights and options.

Don't admit the debt - Anything you say can be used against you. In some states, acknowledging a debt can restart the statute of limitations.

Request written verification - Ask them to send all information in writing. Don't discuss details over the phone.

Don't make payments - Any payment can restart the statute of limitations. It also confirms the debt is yours. Wait until you verify everything.

Document everything - Write down dates, times, names, and what was said. Save all letters and emails. This documentation helps if you need to file complaints or sue.

Know your state's statute of limitations - Each state has different time limits for suing over debt. If your debt passed this deadline, collectors cannot take you to court.

Filing Complaints

If Receivables Performance Management (RPM) violates your rights, file complaints with these agencies:

Consumer Financial Protection Bureau - They track complaint patterns and take enforcement action. File online at consumerfinance.gov.

Federal Trade Commission - They enforce the Fair Debt Collection Practices Act. File at ftc.gov/complaint.

Better Business Bureau - Complaints become public record and affect their rating. File at bbb.org.

Your state attorney general - State officials can investigate violations of state consumer protection laws.

Washington Department of Licensing - This is RPM's home state licensing authority.

These complaints create records. If enough people report similar problems, regulators investigate. Your complaint might prevent others from facing the same issues.

When to Hire an Attorney

Sometimes professional legal help makes sense. Consider an attorney if:

Receivables Performance Management (RPM) violates federal laws repeatedly. Multiple illegal calls, harassment, or threats warrant legal action.

The debt involves large amounts. Debts over $5,000 justify legal fees. Attorneys can negotiate better and protect your interests.

You face a lawsuit. If Receivables Performance Management (RPM) sues you, get an attorney immediately. Don't go to court alone.

Violations caused damages. If their illegal actions cost you money or opportunities, you might recover damages. FDCPA violations can result in $1,000 per violation plus attorney fees.

Many consumer protection attorneys work on contingency. They get paid only if you win. Initial consultations are often free.

The Company's Current Status

According to Better Business Bureau updates, Receivables Performance Management (RPM) closed its doors in late 2023 or early 2024. Their website now shows only a message stating all accounts have been closed.

Despite closure, the damage persists. Collections they reported still appear on credit reports. Former customers still need to address these items.

Some consumers report that Receivables Performance Management (RPM) sold their accounts to other collectors before closing. This means new collection agencies might contact you about the same debt.

The closure creates new problems. You cannot contact them to dispute or negotiate. The items remain on credit reports with no company to address them.

Next Steps for Your Credit

If Receivables Performance Management (RPM) appears on your credit report, take action now.

Check all three credit reports for RPM listings. Send debt validation letters if the debt seems questionable. File disputes for any errors you find. Document all interactions with RPM or successor collectors.

Consider professional help if you feel overwhelmed. Credit repair companies and consumer protection attorneys handle these situations daily.

Your credit matters too much to ignore. Collections from Receivables Performance Management (RPM) damage your score and financial opportunities. But they don't have to stay there forever.

Most people can remove inaccurate or unverifiable collections. Even legitimate debts become less harmful over time. With the right strategy, you can minimize the damage and rebuild your credit.

Don't let one collection account control your financial future. Take action today to protect your credit and your rights.