Most people do not search Midland Credit Management unless something already went wrong.

Usually, the story starts after a credit score drops, a loan gets denied, or a mortgage lender points out a collections account during underwriting.

That is when people notice Midland Credit Management on their credit report for the first time.

I’ve seen this happen a lot during mortgage prep. Someone thinks their credit is finally improving, then a collections account suddenly becomes the reason rates increase or approvals get delayed.

The frustrating part is that many consumers do not fully understand:

where the debt came from

whether the balance is accurate

whether the account is old enough to dispute

whether Midland can fully validate the debt

And honestly, that confusion is common with debt buyers.

Midland Credit Management purchases charged-off accounts from original creditors. That means mistakes can happen during transfers, balance calculations, account ownership records, and reporting updates.

This guide focuses on the part that actually matters:

How to remove Midland Credit Management from your credit report.

What dispute options exist.

When validation matters, and how to avoid hurting your score even more during the process.

How to Remove Midland Credit Management From Your Credit Report

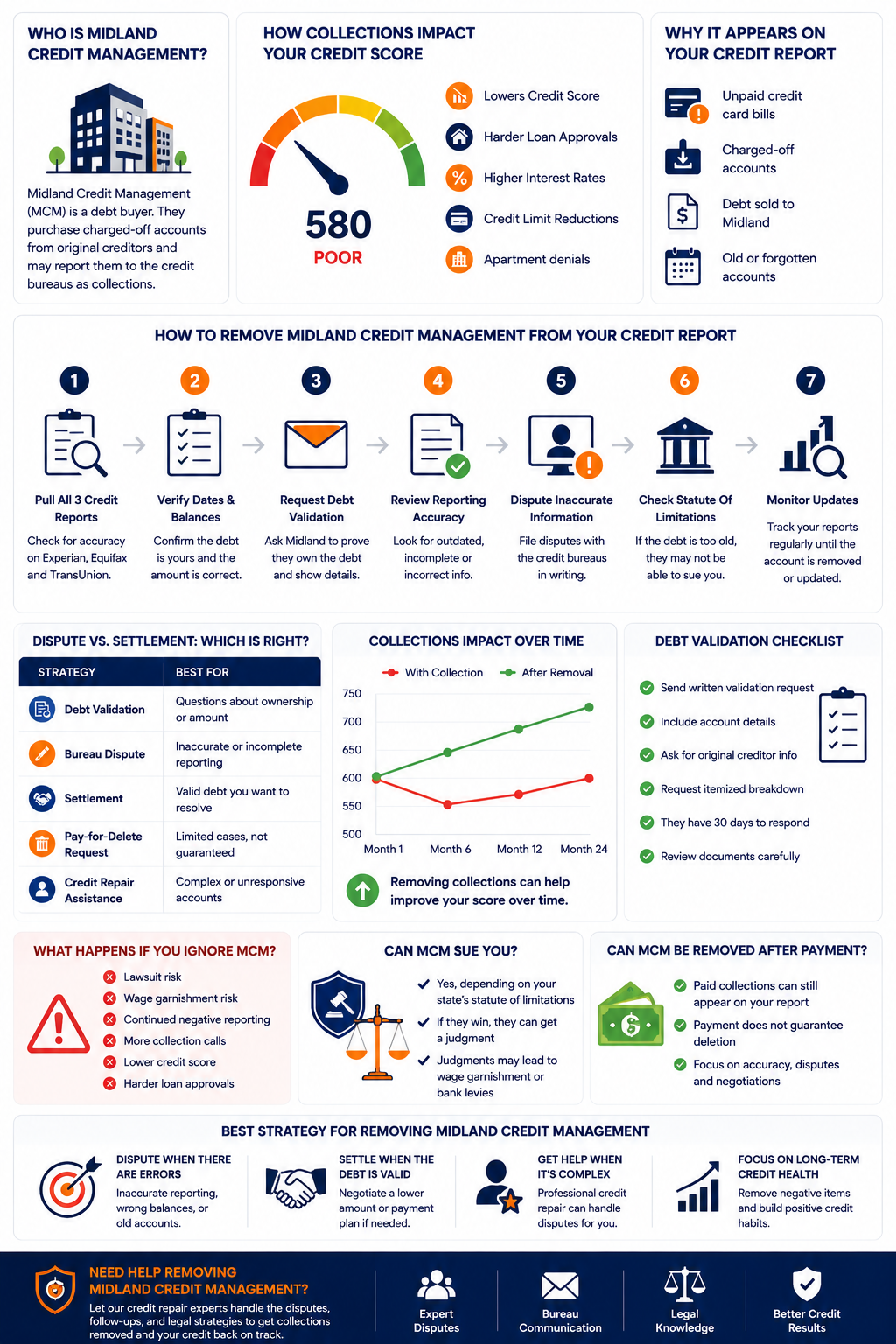

What Is Midland Credit Management

Midland Credit Management (MCM) is a debt buyer and subsidiary of Encore Capital Group (NASDAQ: ECPG), founded in 1953 and headquartered in San Diego, California. MCM purchases charged-off consumer debts for pennies on the dollar and collects the full stated balance. What makes MCM different from most collectors is scale and litigation volume. They are one of the most active debt collection lawsuit filers in the country.

Encore Capital Group also operates Midland Funding LLC , the entity that actually holds purchased debt , alongside MCM. When you see "Midland Credit Management" on your credit report or in a lawsuit, the underlying debt is often held by Midland Funding. This matters in dispute paperwork: the assignment must trace from the original creditor through to whichever Encore entity is actually collecting.

MCM's enforcement history is substantial and ongoing.

Why MCM Is Different From Most Debt Collectors , and Why That Matters

Most debt collectors rely on phone calls, letters, and credit reporting to pressure payment.

MCM layers all of that with litigation at high volume. Suing consumers is not a last resort for MCM. It is a primary strategy. This changes the timeline of what you need to do and when.

With a typical small debt collector, you can sometimes wait. Take time to verify the debt. Research your options. Decide whether to pay or dispute over a few months.

With MCM, the window is shorter. If the debt is within your state's statute of limitations and MCM decides to file, you could have a court summons before you finish researching. A default judgment , from simply not responding to the summons , gives MCM the power to garnish wages and freeze accounts.

The urgency here is specific to MCM's litigation model. Other collectors on this list , like Portfolio Recovery Associates , also sue. But MCM's volume makes the risk more concrete for most consumers.

Can You Remove Midland Credit Management From Your Credit Report

Yes. Multiple paths exist. The fastest is a debt validation dispute , if MCM cannot produce complete documentation proving they own the debt and the information is accurate, the bureau must remove or correct the entry. Federal regulators fined MCM repeatedly for filing documentation-deficient debt collection actions. This same pattern makes validation disputes particularly effective.

| Removal Path | When to Use It | Timeline | Cost |

|---|---|---|---|

| Debt validation + bureau dispute | MCM cannot produce complete documentation | 30-45 days | $0 |

| FCRA dispute , inaccurate info | Wrong balance, wrong date, re-aged entry | 30-45 days | $0 |

| Pay-for-delete negotiation | Debt is valid and you want to resolve and remove | 1-3 months | Settlement amount |

| FDCPA or TCPA counterclaim | MCM violated your rights , robo-called, lied, continued contact after cease and desist | Variable | May recover damages |

| SOL defense (if sued) | Debt is past your state's statute of limitations | During lawsuit response | Attorney recommended |

| Automatic aging off | 7 years from original delinquency date | Already in progress | $0 |

How to Dispute Midland Credit Management Before They Sue

Go to AnnualCreditReport.com. Find the MCM tradeline. Note the original delinquency date , this is when the original creditor marked the account past due, not when MCM purchased it. Check whether both Midland Credit Management and Midland Funding LLC appear as separate entries. A single underlying debt that appears twice is a disputable error under the FCRA.

Free | The original delinquency date drives every strategic decisionIf the original delinquency is older than your state's SOL for credit card debt (typically 3-6 years), MCM cannot win a lawsuit on it. They are required by the 2015 and 2020 consent orders to disclose time-barred status before collecting. If they contacted you without disclosing this, that may itself be an FDCPA violation. Verify the SOL before any communication.

Time-barred debt = significantly stronger dispute positionRequest the original creditor's name, original account number, complete assignment chain from the original creditor to MCM and/or Midland Funding LLC, itemized balance accounting, and SOL disclosure if time-barred. MCM operates a "Consumer Resolution Center" , send to both their general collections address and the Chief Compliance Officer address. MCM drew two federal fines specifically for failing to provide this documentation within 30 days.

Certified mail, return receipt | 30-day FDCPA window from first contactMCM purchases debt in large portfolios. The assignment documentation often does not include account-specific records tracing from the original creditor through every intermediate owner to Midland Funding. A generic bill of sale that references the portfolio but not your specific account number is insufficient. Compare their response line by line against what you requested. Every gap is grounds for the next step.

Robo-signing history means court documents may also be deficient , the same pattern applies to validation responsesFile separate FCRA disputes with Equifax, Experian, and TransUnion. Include: the validation letter you sent, MCM's incomplete response, and any specific inaccuracies in the credit entry. Each bureau investigates independently. MCM must verify the specific account information with each bureau during a 30-day window. If they cannot, the entry must be corrected or removed.

File all three separately | 30-day investigation window per bureauMCM paid $15 million for robo-calling violations. If they called your cell phone multiple times using an auto-dialer without your written consent, that may be a TCPA claim worth $500-$1,500 per call. If they continued calling after a written cease and desist, that is an FDCPA violation. Log every call with the date, time, and phone number. Consumer protection attorneys take MCM cases regularly on contingency , no upfront cost to you.

TCPA statute of limitations: 2 years from violation | FDCPA: 1 yearWhat MCM Must Prove , and Why They Often Cannot

MCM was fined twice for the same core problem: collecting without complete documentation.

The 2015 consent order prohibited MCM from suing consumers or collecting without possessing the required documentation to prove the debt. The 2020 action imposed a $15 million penalty specifically because MCM violated that consent order , the same documentation failures continued after the first enforcement action.

This pattern has a practical implication for you.

When you request validation, MCM must produce:

- Complete chain of assignment from the original creditor through every intermediary to the current holder

- Account-specific documentation , not just a portfolio-level bill of sale

- Original account agreement or equivalent documentation establishing the debt terms

- Itemized accounting of the current balance versus the original amount

- Disclosure that the debt is time-barred if the statute of limitations has passed

MCM's documented history of robo-signing court documents , producing fabricated or unsigned affidavits in debt collection lawsuits , was part of what drove the penalty actions. If the same documentation standards that failed in court also fail your validation request, you have concrete grounds for a bureau dispute.

Midland Credit Management , Settlement vs Dispute

- MCM cannot produce complete chain-of-title documentation

- The debt is past your state's statute of limitations

- The balance on the report is wrong or inflated

- The entry contains re-aged delinquency dates

- The debt is not yours or may involve identity theft

- MCM violated your FDCPA or TCPA rights

- Debt is verified, valid, and within the statute of limitations

- MCM has threatened or filed a lawsuit on the debt

- You want the account resolved rather than aged off

- A written pay-for-delete agreement is obtainable

- Budget allows a lump sum settlement (25-50% is typical)

MCM's settlement behavior is worth understanding. They paid 2-4 cents per dollar to acquire most accounts. Settling for 30-40 cents per dollar of the stated balance is still profitable for them. The closer the debt is to the statute of limitations, the stronger your negotiating position , they lose the ability to sue if they delay too long.

The TCPA Claim Most People Miss

The Telephone Consumer Protection Act (TCPA) prohibits using an auto-dialer to call a consumer's cell phone without prior written consent. MCM settled a $15 million class action specifically for doing this. If MCM called your cell phone repeatedly using what sounds like a pre-recorded or automated call, you may have an independent TCPA claim worth $500 to $1,500 per violation , completely separate from any credit dispute. Log every call. Note the date, time, and whether it sounded automated. Consumer attorneys handle TCPA cases against MCM on contingency. You pay nothing unless they win. The statute of limitations for TCPA claims is 2 years from each violation date.

This claim exists whether or not your underlying debt is valid. The credit dispute and the TCPA claim are separate legal tracks. Pursuing both simultaneously often produces the best outcome , MCM may settle the TCPA claim and agree to remove the credit tradeline as part of the resolution.

The NerdWallet guide on time-barred debt collection notes that collectors who pursue time-barred debts without required disclosures open themselves to FDCPA liability. As the FTC's debt collection rights guide confirms, consumers retain the right to sue for documented violations of both the FDCPA and TCPA within the applicable statute of limitations. MCM's enforcement history means these claims are not theoretical , regulators and courts have confirmed the violation patterns repeatedly.

How Midland Credit Management Affects Your Credit Score

A collection account from MCM drops most scores by 50-100 points, with the highest impact in the first 12-24 months. The damage decreases as the account ages.

Watch for two specific errors that MCM accounts show more frequently than most collectors.

Dual entry problem. Midland Credit Management and Midland Funding LLC both appear on some reports for the same underlying debt. The original creditor's charge-off entry may also remain. Three negative entries from one debt is more common with MCM than with most collectors. Each separate entry is individually disputable. Getting any one of them removed reduces the scoring impact.

Re-aging. The CFPB has acted against MCM for FCRA violations including inaccurate credit reporting. Check the original delinquency date shown on the MCM entry against what the original creditor reported. If MCM shows a newer date, that is re-aging , an FCRA violation and grounds for dispute with each bureau showing it.

As Experian's credit score guide explains, collection accounts are among the most damaging entries on a credit file , but their impact decreases significantly with each passing year as the account ages and the rest of the file shows positive behavior.

Can Midland Credit Management be removed from my credit report?

Yes. If the information is inaccurate, unverifiable, or the debt is not yours, dispute it under the FCRA and MCM must verify or the bureau removes it. If the debt is valid, negotiate a pay-for-delete agreement before payment. The entry also ages off automatically at seven years from the original delinquency date. Federal regulators fined MCM multiple times for filing documentation-deficient collection actions , those same documentation problems make validation disputes particularly effective against them.

What should I do if Midland Credit Management sues me?

Respond to the summons in writing before the deadline , 14-30 days depending on your state. File a written answer with the court. In your answer, assert the following defenses: lack of standing (MCM cannot prove chain of title), statute of limitations if applicable, and any FDCPA violations you documented. Regulators penalized MCM for filing lawsuits without required documentation and for robo-signing court documents. Forcing them to produce documentation in court is the same strategy that works in a bureau dispute. An FDCPA or consumer protection attorney who works with MCM cases can file a stronger answer and potentially countersue , many work on contingency.

Does paying Midland Credit Management remove it from my credit report?

Not automatically. Paying updates the account status to "paid collection," but the entry stays on your report for the full seven years from the original delinquency date. Payment alone does not remove it. If you want removal in exchange for payment, negotiate a written pay-for-delete agreement before sending any money. Get the specific terms in writing , the account number, the settlement amount, and the confirmation that MCM will remove the tradeline from all three bureaus upon receipt of payment. Without that agreement in writing, MCM is not obligated to remove it.

Does Midland Credit Management buy debts and resell them?

MCM and its affiliated entity Midland Funding LLC primarily purchase and hold debts rather than reselling them. The Encore Capital Group corporate structure has MCM as the collection operation and Midland Funding as the entity that legally holds purchased debt. When you see Midland Credit Management on your credit report, the actual debt owner is often Midland Funding LLC. This distinction matters for dispute paperwork , the assignment documentation must trace correctly from the original creditor through to the specific Encore entity currently collecting.

-

How to Remove Portfolio Recovery Associates From Your Credit Report Portfolio Recovery Associates and Midland Credit Management are the two largest debt buyers in the US. Both use similar documentation-deficient collection tactics, both carry major CFPB enforcement histories, and both respond to the same validation-first dispute strategy. This covers the full dispute process for PRA including their $51M in penalties, settlement math, and when FDCPA counterclaims apply.

-

Debt Validation , When Collectors Must Prove You Owe MCM drew two federal fines specifically for failing to validate debts within 30 days of consumer requests. This guide covers exactly what a valid validation response requires under the FDCPA, what MCM and other collectors must provide, and what to do when the response comes back incomplete , including how to use that gap in a bureau dispute.

-

Will Responding to a Debt Collector Restart the Statute of Limitations? MCM collected time-barred debt without required disclosures , one of the specific violations named in both the 2015 and 2020 consent orders. Before you call MCM back, respond to any letter, or make any payment, understand what actions restart the SOL clock in your state. A single payment or verbal acknowledgment can give MCM a renewed legal window to sue on a debt they currently cannot touch.