The holidays bring joy, but also financial stress because of mounting holiday debt. If you're planning to use credit cards this season, you need a solid plan.

The numbers tell a sobering story: 36% of Americans took on holiday debt in 2024, averaging $1,181 per person.

Even worse, 28% of credit card users still haven't paid off last year's holiday purchases.

This year doesn't have to be the same.

Here are proven strategies to manage credit wisely during the holiday season without sacrificing celebrations or damaging your financial future.

The Real Cost of Holiday Spending

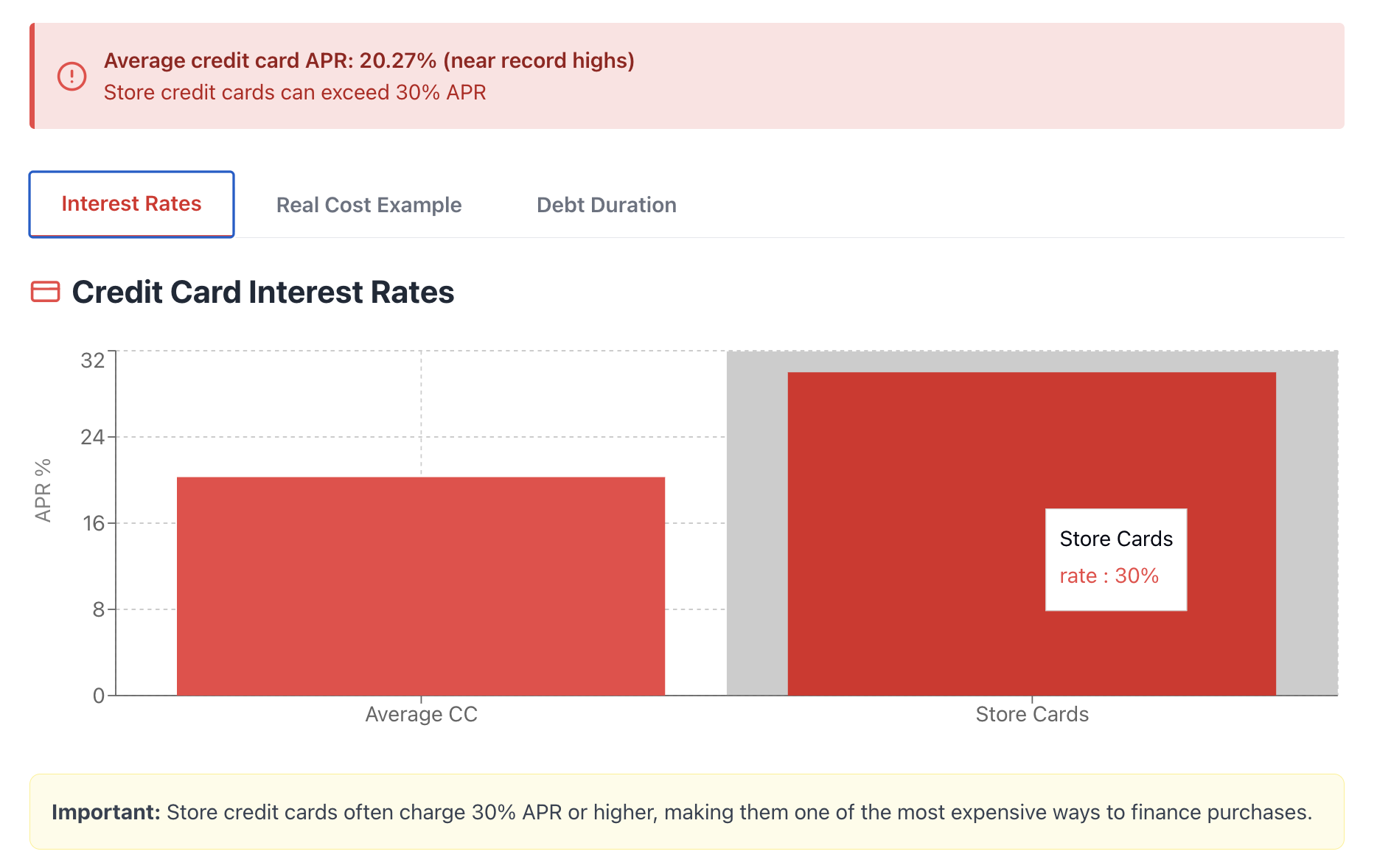

Before you swipe that card, understand what you're really paying. Average credit card interest rates currently sit at 20.27%, near record highs.

Store credit cards are even worse, with some charging over 30% APR.

What This Means in Real Money:

- A $1,200 holiday balance at 20% APR costs $240 in interest annually

- Making minimum payments only? You'll pay that debt for years

- 21% of people who take on holiday debt expect it'll take five months or longer to pay off

The math gets ugly fast. That $100 gift charged at 25% APR costs $125 if you take a year to pay it off. Suddenly, that sweater doesn't seem like such a bargain.

Set Your Budget Before You Shop

This sounds basic, but only 44% of people who took on debt actually planned to do so. The rest overspent without meaning to.

Create Your Holiday Spending Plan:

- Calculate what you can actually afford - Not what you want to spend. Look at your income, regular expenses, and what's left over.

- List everyone you're buying for - Write down every person, plus travel, food, decorations, and parties.

- Assign dollar amounts - Be realistic. A $50 gift limit per person is better than going into debt for $100 gifts.

- Track every purchase - Use a simple spreadsheet or notes app. Check it before every purchase.

Sara Rathner, credit cards expert at NerdWallet, puts it simply: Set your budget early and stick to it. The pressure to overspend is real, but debt that sticks around long after the decorations come down isn't worth it.

Avoid Holiday Debt By Strategic Credit Card Use

Credit cards aren't evil, but they're powerful tools that require respect and planning.

If You're Starting Debt-Free

You're in the best position to use credit cards to your advantage. Cards with rewards can actually save you money, if you pay them off completely.

Smart Strategies:

- Use cash back cards for holiday purchases

- Pay off the balance in full each statement

- Never spend more than your budget allows just for rewards

Rathner notes that if you're debt-free, you're in a strong position to take advantage of credit card rewards. But only if you pay the balance in full.

If You're Already Carrying Debt

Half of credit card holders currently carry balances, yet 96% will still make holiday purchases. If this is you, extra caution is critical.

Damage Control Tactics:

- Use debit or cash instead of adding to existing card balances

- If you must use credit, choose your lowest-interest card

- Consider a 0% balance transfer card to tackle existing debt first

Avoid These Dangerous Traps

Retailers know how to get you to spend more. Don't fall for these common pitfalls.

Store Credit Cards

According to Federal Reserve Consumer Credit Data, 1 in 5 Americans plan to take out store credit cards this holiday season. This is almost always a mistake. Federal Reserve Consumer Credit Data

Why Store Cards Hurt You:

- Interest rates average 30.45%, the highest ever recorded

- Opening new cards drops your credit score temporarily

- Easy approval encourages overspending

- You likely won't use the card after the holidays

Greg McBride, chief financial analyst at Bankrate, warns: "Store credit cards often charge higher interest rates than general credit cards do." That 20% discount isn't worth years of 30% interest payments.

Buy Now, Pay Later Services

BNPL services like Affirm and Klarna seem harmless. They're not.

The Hidden Dangers:

- Easy to stack multiple loans without realizing it

- Most BNPL users have multiple installment loans open simultaneously

- Often attracts people whose finances are already stretched

- Missed payments damage your credit

Matt Schulz, LendingTree's chief credit analyst, explains: "The problem with buy now, pay later is that because it's so easy to get, people end up getting several of them at a time and stockpiling them."

Maxing Out Cards

48% of credit card holders plan to max out at least one card by season's end. This is credit score suicide.

Why Maxing Out Cards Destroys Your Credit:

- Your credit utilization ratio spikes

- Your credit score drops significantly

- You'll pay more interest on future borrowing

- You have no available credit for emergencies

Keep your credit utilization below 30% of your limit. Under 10% is even better.

Smart Shopping Tactics

Small changes in how you shop can save hundreds of dollars.

Shop Early and Hunt for Deals

Candy Valentino, author of "The 9% Edge," recommends starting holiday shopping early to take advantage of discounts.

Black Friday and Cyber Monday aren't always the best deals, watch prices throughout November and December.

Money-Saving Moves:

- Compare prices across multiple retailers

- Use browser extensions like Honey or Capital One Shopping

- Check for promo codes before checkout

- Consider refurbished or last year's models for electronics

Cut Costs Without Cutting Joy

Howard Dvorkin, chairman of Debt.com and certified public accountant, challenges the assumption that you must spend a lot: "Somehow it's been programmed into the American consumer that essentially says 'I have to spend a lot of money on people I care about.' It doesn't have to be that way."

Alternative Approaches:

- Pool money with family members for group gifts

- Set spending limits with friends and family

- Focus on experiences over expensive items

- Make homemade gifts or baked goods

Valentino adds: "Try pooling funds among family or friends to share the cost of holiday gifts." This approach maintains generosity while protecting your budget.

Related Content: Post-Holiday Budget Reset: 7 Steps to Bounce Back from Overspending

If You're Already in Debt

Don't ignore last year's holiday debt while adding more this year.

Tackle Existing Balances First

Three Proven Methods:

- Balance Transfer Card - Move high-interest debt to a 0% APR card. Some offers last 21 months. Divide your balance by the number of 0% months and pay that amount monthly.

- Debt Consolidation Loan - If you have good credit, a personal loan at 7-12% beats credit cards at 20%+.

- Pay Highest Rate First - Focus extra payments on your highest-interest card while making minimums on others (the "avalanche method").

Reduce Your Interest Rate

Before taking on new holiday debt, try these tactics:

Call your credit card company and ask for a rate reduction. It sounds too simple, but it works. Explain your situation, mention your payment history, and ask directly.

You won't always get a yes, but many issuers will lower your rate, especially if you've improved your credit score or increased your income since getting the card.

Must Read: Why Are People Struggling With Debt? Understanding The Reasons Behind

Protect Your Credit Score

Your credit score affects more than just credit cards. It impacts loan rates, apartment approvals, and even job opportunities.

Monitor Your Credit Regularly

Check your credit reports from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com. You're entitled to free reports once per year from each.

What to Look For:

- Errors or accounts you don't recognize

- Fraudulent activity

- Balances that seem incorrect

Many banks now offer free credit monitoring. Use it.

Protect Your Score While Shopping

Every action you take affects your credit:

Do This:

- Keep balances under 30% of limits

- Pay on time, every time (payment history is 35% of your score)

- Avoid opening multiple new accounts

Don't Do This:

- Apply for multiple store cards in one shopping trip

- Max out existing cards

- Make late payments, even one, damages your score for years

Recommended: Credit Score Impact: How Card Stacking Affects Your Score

After the Holidays: Recovery Mode

January brings credit card bills. Be ready.

Create Your Payoff Plan

As soon as January statements arrive:

- List all holiday debt with interest rates

- Calculate how much you can pay monthly

- Decide on the avalanche method (highest rate first) or the snowball method (smallest balance first)

- Set up automatic payments so you never miss a due date

Rebuild Your Emergency Fund

Once you've paid off holiday debt, start building an emergency fund. Even $500-$1,000 prevents you from going into debt for unexpected expenses.

Valentino recommends reallocating funds by canceling unwanted subscriptions and negotiating down utility costs. "A few hundred dollars here and there really adds up."

The Bottom Line About Holiday Spending

Holiday spending doesn't have to mean holiday debt. The key is planning ahead, setting firm limits, and having the discipline to stick to them.

Remember:

- 36% of Americans took on an average of $1,181 in holiday debt last year

- Credit card rates average 20.27%, and debt is expensive

- 28% still haven't paid off last year's purchases

You can celebrate the holidays without sacrificing your financial future. Start with a realistic budget, use credit strategically, avoid store cards and BNPL traps, and have a payoff plan before you buy.

The best gift you can give yourself is financial peace of mind in January and beyond.