What Is a Snap Debt Recovery Lawsuit?

When you don't pay, they sue you in court to get a judgment that lets them garnish your wages or freeze your bank account. I run a Texas credit repair company, and we help clients fight these lawsuits every single day.

Last month alone, we worked with 47 clients who received court summons from Snap Debt Recovery. Most of them panicked because they didn't know what to do. Some ignored the paperwork completely, the worst mistake you can make.

Others thought the debt was too old to matter. The truth is, debt collectors like Snap Debt Recovery count on you doing nothing. When you ignore a lawsuit, they win automatically.

Snap Debt Recovery Lawsuit Credit Score Impact

This matters because a court judgment against you creates serious financial damage that lasts for years. Your credit score drops 100+ points.

Collectors can take money directly from your paycheck. Your bank account gets frozen without warning. I've seen clients lose their rent money, miss car payments, and struggle to pay for groceries because they didn't understand how these lawsuits work.

Let me walk you through everything you need to know, based on real cases we've handled.

How Snap Debt Recovery Lawsuits Actually Happen

Most people don't see the lawsuit coming.

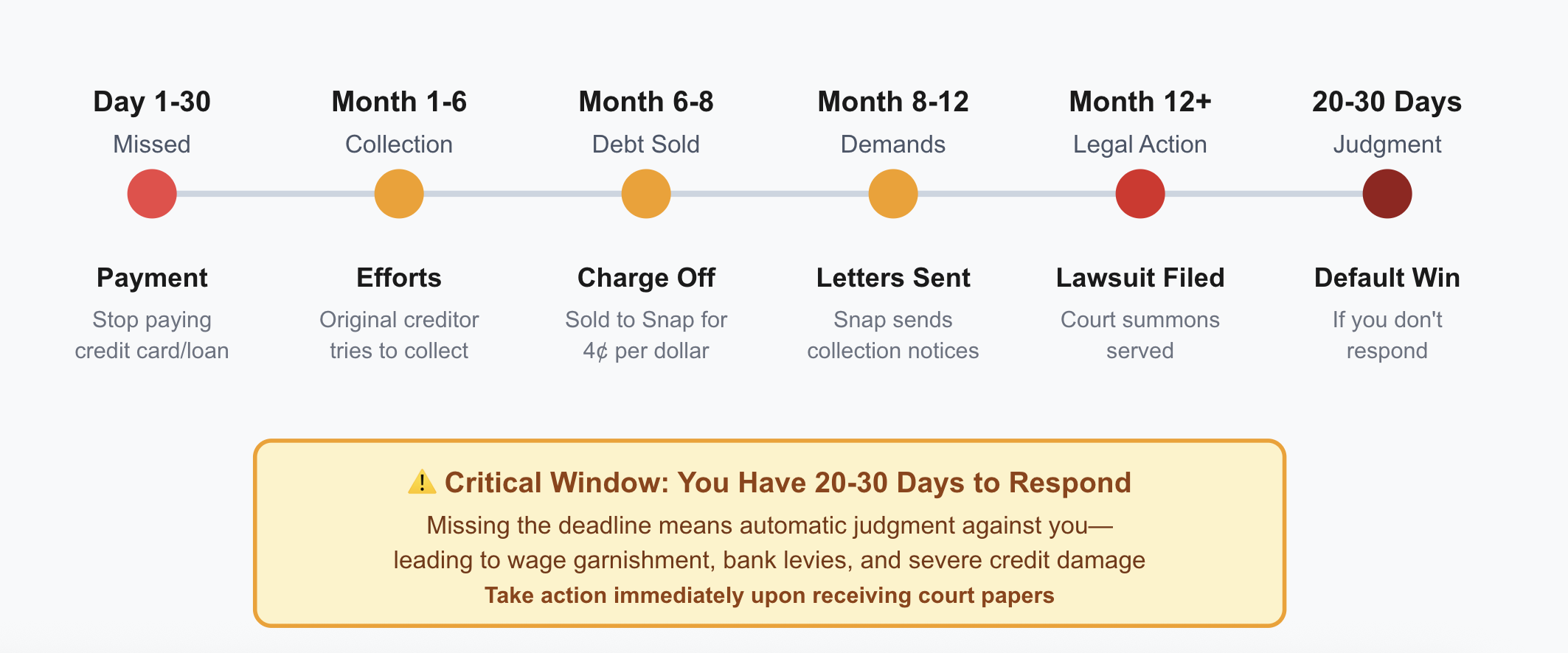

Here's the typical timeline:

30 days of Missed Payment. You stop paying a credit card or loan.

Collection Efforts. The original creditor tries to collect for 3-6 months, then gives up.

Charge Off. They sell your debt to Snap Debt Recovery for maybe 4 cents per dollar owed. Snap sends you collection letters demanding payment. You ignore them or can't afford to pay.

Lawsuit. They file a lawsuit in your county court.

A process server shows up at your door or workplace with court papers. You have 20-30 days to respond (the exact deadline is on the summons). If you don't file an answer with the court, Snap Debt Recovery wins by default. The judge signs a judgment without ever hearing your side.

In our company, we had a client named Marcus who owed $3,200 on an old credit card from 2019. He lost his job during the pandemic and couldn't keep up with payments. Snap Debt Recovery bought the debt in 2023 and sued him in early 2024.

Marcus thought the lawsuit would just go away if he ignored it. Three months later, his employer received a wage garnishment order. They started taking 25% of his paycheck, $480 every two weeks, before he even saw the money.

Why Snap Debt Recovery Sues (And Why They Often Win)

Debt buyers like Snap Debt Recovery make money through volume. They buy thousands of debts cheaply and sue the ones that seem worth pursuing. They win about 90% of their cases, not because they have strong evidence, but because people don't show up to court.

Think about their business model: They pay $400 for a $10,000 debt. If they collect even $2,000, they profit. Lawsuits are their leverage. They know most people don't have lawyers. They know court procedures confuse people. They know fear and shame keep people from fighting back.

But here's what they don't advertise: Many of these lawsuits have serious problems. The debt might be old (past the statute of limitations). They might lack proper documentation proving you actually owe the money. They might violate the Fair Debt Collection Practices Act by harassing you or making false threats.

What Happens If You Lose a Snap Debt Recovery Lawsuit

A judgment gives Snap Debt Recovery powerful tools to collect from you:

Wage garnishment takes money straight from your paycheck before you receive it. In most states, they can take up to 25% of your disposable income. Some states allow more.

Bank account levy freezes your checking or savings account. The bank sends your money directly to the collector. You can't access those funds until the judgment is satisfied or you successfully challenge the levy in court.

Property liens attach to your house or car. You can't sell or refinance without paying off the judgment first.

Credit reporting damages your credit score for seven years from the judgment date. You'll struggle to get approved for apartments, car loans, mortgages, or even cell phone plans.

Here's a visual illustration:

The judgment also grows. Interest accrues every year, often 8-12% depending on your state. A $5,000 judgment becomes $6,500 after three years, even if you're making small payments.

In our company, we worked with a client named David who ignored a Snap Debt Recovery lawsuit for $12,000. He thought they'd forget about him. Two years later, they levied his bank account on payday, Friday afternoon, before a three-day weekend. They took $3,800.

David couldn't pay his mortgage or buy food. It took him five days to get a court hearing and prove some of that money was exempt (Social Security benefits). He got $1,200 back, but the stress and financial damage were devastating.

Your Legal Rights When Sued by Snap Debt Recovery

Federal and state laws protect you during debt collection lawsuits:

They must prove you owe the debt. Snap Debt Recovery needs to show documentation, the original contract, account statements, and proof that they own the debt. Many debt buyers don't have complete records.

The debt can't be super old. Every state has a statute of limitations (typically 3-6 years). If the debt is older, you can get the case dismissed.

They can't harass or deceive you. The Fair Debt Collection Practices Act prohibits abusive collection tactics, calling before 8 AM or after 9 PM, contacting you at work after you tell them to stop, threatening actions they can't legally take.

You can challenge the lawsuit. Filing an answer lets you dispute the debt, question their evidence, and raise legal defenses. Most people don't realize this is an option.

Some income is protected. Social Security, disability benefits, and unemployment are usually exempt from garnishment. Many states also protect a portion of your wages and bank balance.

Steps to Take When You Receive Lawsuit Papers

Don't panic and don't ignore it. The worst response is doing nothing. That guarantees you lose.

Read the summons carefully. Note the exact deadline to respond, usually 20-30 days from when you were served. Missing this deadline means automatic judgment against you.

Request debt validation. Send Snap Debt Recovery a certified letter demanding they prove you owe the debt. Ask for the original contract, itemized account statements, and documentation showing they own the debt. They have 30 days to respond. If they can't provide adequate proof, their case weakens significantly.

File an answer with the court. This is a legal document responding to their complaint. You can admit or deny each claim they make. You can also raise affirmative defenses (the debt is too old, you already paid it, you never received services, etc.). Many courts have free answer forms online. Filing an answer forces Snap Debt Recovery to actually prove their case instead of winning by default.

Gather your evidence. Find old bank statements, payment records, credit reports, or anything showing the debt's history. Document every communication with Snap Debt Recovery, dates, times, what they said, how they contacted you.

Consider legal help. Many consumer attorneys offer free consultations for debt collection cases. Some work on contingency (you don't pay unless you win). Legal aid organizations help low-income individuals for free.

Show up to court. If there's a hearing, attend it. Bring your evidence and be prepared to explain your side. Judges appreciate people who make an effort, even without lawyers.

Common Defenses Against Snap Debt Recovery Lawsuits

Statute of limitations expired. If the debt is older than your state's time limit for legal action, the lawsuit should be dismissed. This is often the strongest defense.

Mistaken identity. Sometimes, debt collectors sue the wrong person, someone with a similar name or address. Proving you're not the debtor ends the case immediately.

Debt already paid or settled. If you paid the original creditor or settled the account, Snap Debt Recovery shouldn't be collecting. Show proof of payment.

Lack of documentation. Debt buyers often have incomplete records. If they can't produce the original contract or a complete chain of ownership, they can't prove you owe them money.

FDCPA violations. If Snap Debt Recovery harassed you, made false threats, or violated federal law, you might have a counterclaim. This can result in damages paid to you and dismissal of their lawsuit.

Amount is wrong. They might be suing for more than you actually owed, or including fees and interest they're not entitled to collect.

What Happens After You Respond to the Lawsuit

Once you file an answer, Snap Debt Recovery must prove its case. Many debt buyers drop lawsuits at this point because fighting costs more than the debt is worth.

If they continue, discovery happens next. Both sides exchange evidence and information. You can request documents proving the debt. They might ask you questions about your finances.

Settlement negotiations often occur here. Snap Debt Recovery might offer to settle for 40-60% of the claimed amount, sometimes less. Whether to settle depends on the strength of their case and your financial situation.

If no settlement happens, you go to trial. The judge hears both sides and decides. Trials for these cases usually last under an hour.

How to Negotiate With Snap Debt Recovery

If the debt is legitimate and you want to avoid judgment, negotiating makes sense:

Get everything in writing before paying anything. Don't trust verbal promises. Demand a settlement letter stating the exact amount, that payment satisfies the debt completely, and that they'll dismiss the lawsuit.

Start low. Offer 25-30% of the claimed amount. They'll counter higher. You'll meet somewhere in the middle, usually 40-60%.

Pay only if they dismiss the lawsuit. The settlement should include dismissal with prejudice (meaning they can't sue you again for the same debt).

Recommended Content: What To Do If You Have Been Sued By Debt Collectors

Use a cashier's check or money order. This creates a clear payment record. Never give them direct access to your bank account.

Request credit reporting changes. Ask them to delete the collection account or mark it "paid in full" rather than "settled for less."

Rebuilding After a Snap Debt Recovery Lawsuit

Whether you win, lose, or settle, your credit needs attention:

Dispute inaccurate information. If the debt appears on your credit report incorrectly, wrong amount, wrong dates, shows as unpaid when it's settled, dispute it with the credit bureaus.

Build positive payment history. Get a secured credit card, become an authorized user on someone else's account, or take out a credit builder loan. Consistent on-time payments gradually improve your score.

Monitor your credit regularly. Use free services like Credit Karma or AnnualCreditReport.com to check for errors and track improvements.

Create a debt management plan. If you have other debts, address them before they become lawsuits, too. Nonprofit credit counseling agencies offer free help.

When to Hire an Attorney

Get legal help if:

- The debt amount exceeds $5,000

- You don't understand court procedures

- Snap Debt Recovery has strong documentation

- You're already facing wage garnishment or bank levies

- You believe they violated the FDCPA

- You need help negotiating a complex settlement

Many consumer protection attorneys offer free consultations and work on contingency for FDCPA violations. This means you pay nothing unless they win your case and recover damages.

Final Thoughts

Snap Debt Recovery lawsuits feel overwhelming, but you have more power than you think. Most people lose these cases simply because they don't fight back. When you respond appropriately, file an answer, request validation, raise legal defenses, you dramatically improve your odds.

I've watched hundreds of clients successfully challenge these lawsuits. Some got cases dismissed entirely. Others negotiated settlements for 40% of the claimed amount. A few even won counterclaims for FDCPA violations and got paid.

The key is acting quickly. The moment you receive lawsuit papers, start working on your response. Every day counts toward your deadline. Miss it, and your options disappear.

Don't let fear or shame stop you from protecting yourself. Debt collection companies bet on your inaction. Prove them wrong.