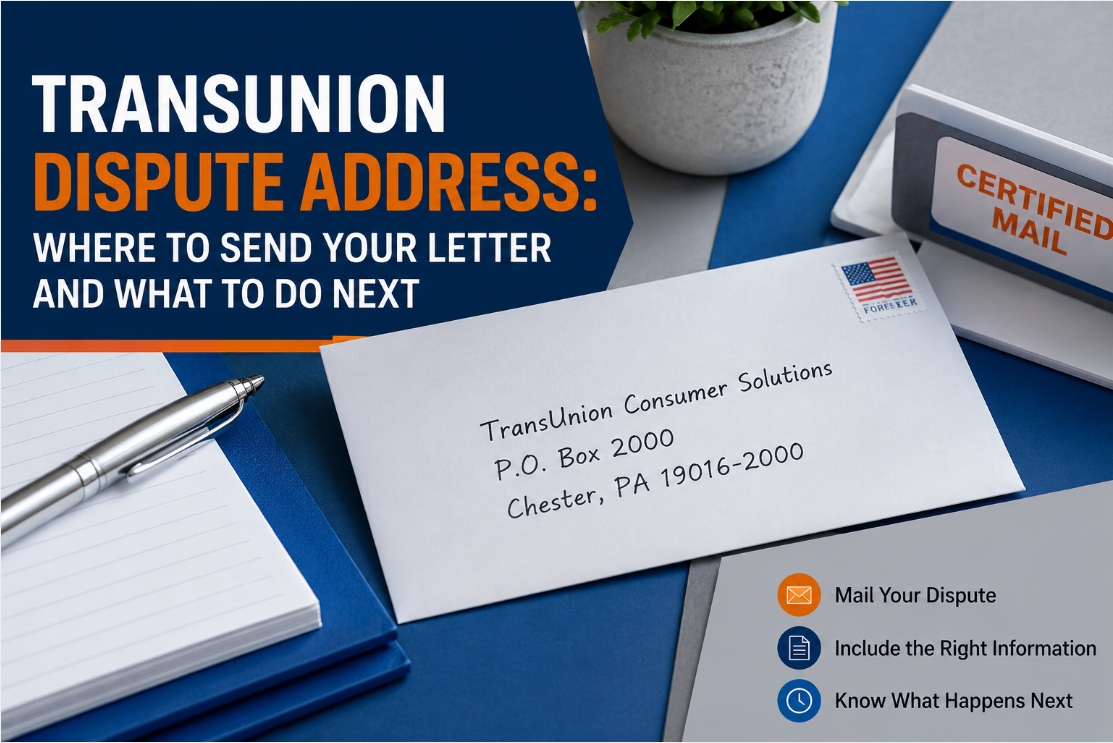

The TransUnion dispute address you need is TransUnion Consumer Solutions, P.O. Box 2000, Chester, PA 19016-2000. That is where you mail your dispute letter. You can also go online at transunion.com or call 800-916-8800. If you mail it, use certified mail. That way, you have proof they got it.

I run a credit repair company. Clients ask me about the TransUnion dispute address almost every week. One case I will never forget: a client mailed his dispute letter to an old address he found online. Three months went by. Nothing happened. He ended up losing a mortgage deal over it. One wrong address. That is how much this matters.

And it happens more than you think. From January 2024 to June 2025, the CFPB received over 5.6 million consumer complaints. Almost 4.8 million of them were about credit reports. About 3.9 million pointed at the three major bureaus, including TransUnion (CFPB Annual Report, 2025). If you have an error in your report right now, you are far from alone.

What Is the Correct TransUnion Dispute Address?

Here is the address. Write it down or save this page.

TransUnion Consumer Solutions P.O. Box 2000 Chester, PA 19016-2000

This comes directly from TransUnion's official website. They accept regular mail and certified mail at this address. Use certified mail every time. Ask for a return receipt. That small step gives you a paper trail in case things go sideways.

Got a serious complaint that has already been ignored? There is a second option. TransUnion has an Executive Complaint office at 555 West Adams Street, Chicago, IL 60661. Save that address for situations where the normal process has already failed you.

How Do You Know If Your TransUnion Report Has an Error?

Before you mail anything, you need to know what you are disputing.

Go to AnnualCreditReport.com and pull your free credit report. Read through it slowly. You are looking for anything that does not look right.

Here are the most common errors people find:

An account that is not yours at all

A payment marked late even though you paid on time

An account you closed that still shows as open

A balance that is higher than it should be

The same debt is listed twice by different collectors

A negative item that is too old to still be on the report

Write down the creditor name, account number, and exactly what is wrong. You will need those details when you write your dispute letter. Do not put this off. The sooner you send your letter to the TransUnion dispute address, the sooner they will start investigating.

How Do I File a Dispute With TransUnion?

You have three ways to do it: mail, online, or phone. Each one works. But they are not equal.

Option 1: Mail Your Dispute to the TransUnion Dispute Address

This is the best option. Here is why. When you mail a dispute, the Fair Credit Reporting Act (FCRA) requires TransUnion to do three things. They must send you the results in writing. They must pass your dispute to the original creditor. And they must prove how they verified the information. None of those three requirements applies to online or phone disputes.

Mail your letter to: TransUnion Consumer Solutions, P.O. Box 2000, Chester, PA 19016-2000

Here is everything your letter needs to include:

Your full name, home address, date of birth, and Social Security number

Your File ID Number can be found in the top right corner of page one of your TransUnion report

The creditor name and account number you are disputing

A plain explanation of what the error is

Copies of any documents that back you up, never send originals

A copy of your driver's license or another government-issued ID

Something that shows your current address, like a recent utility bill

Once you have all of that, sign the letter, print your name, and make a copy of everything before you seal the envelope.

Option 2: File Online

Go to transunion.com/credit-disputes. Create a free account. Find the item you want to dispute and follow the steps. You can upload documents right there. It is quick and easy. But remember — you give up three legal protections the moment you skip the mail.

Option 3: Call TransUnion

Dial 800-916-8800. Lines are open Monday through Friday, 8 a.m. to 11 p.m. ET. On weekends, they are open 8 a.m. to 5 p.m. ET. Have your File ID number with you when you call.

One thing to know: even if you call, TransUnion will still ask you to mail copies of your documents. So have everything printed and ready before you pick up the phone.

At my company, we almost always go with email first. Last quarter alone, we took on 40-plus cases where clients had filed online and had nothing to show for it when the dispute went wrong. A mailed dispute with certified tracking is your safety net.

What Happens After You Send Your Dispute?

Once TransUnion gets your letter at the dispute address, their clock starts. The FCRA gives them 30 days to finish their investigation. If you send in more documents during that time, the window extends to 45 days.

Here Is What They Do During That Time

They reach out to the creditor who reported the item

The creditor looks at your dispute and sends back a response

TransUnion either fixes the item, deletes it, or leaves it as is

They send you a written summary of what they decided

If they rule in your favor, you can ask them to contact any lender who pulled your credit in the past six months. That is useful if the error hurt a recent loan application.

If the item stays on your report, TransUnion must explain exactly why and tell you how they ran the investigation.

Here is something worth knowing about how this process really works. In 2021, TransUnion had just 171 people handling disputes for 38 million line items (ProPublica, March 2026). That is an enormous workload. A dispute letter with clear evidence and a specific explanation stands a much better chance than a vague one.

What If TransUnion Does Not Reply in 30 Days?

It happens. If 30 days go by and you have heard nothing, call 800-916-8800. Have your certified mail tracking number ready. Have the date you sent the letter ready too.

Still nothing? File a complaint with the CFPB at consumerfinance.gov/complaint. You can also report it to the FTC at reportfraud.ftc.gov.

Here is the part most people do not know: under the FCRA, if TransUnion does not investigate within 30 days, they are required to delete the item. That is not a maybe. That is the law. Use it if you need to.

What If TransUnion Rejects Your Dispute?

A rejection stings. But it is not the end of the road.

Why Do They Reject Disputes?

You did not include enough supporting documents

Your letter was too vague or missing key details

The creditor told them the information is accurate

Read the rejection notice carefully. TransUnion has to tell you the reason. Once you know why, gather stronger evidence and refile.

You Can Add a Statement to Your Report

Even if the dispute is rejected, you have the right to add a 100-word consumer statement to your TransUnion report. Every lender who pulls your credit will see it. Use it to tell your side of the story while you keep working on the dispute.

Consider Talking to an FCRA Attorney

If you believe TransUnion handled your dispute unfairly, an FCRA attorney can step in. They can send a formal demand letter. TransUnion can be held liable for actual damages and attorney fees when they violate the law. That kind of pressure often produces results that consumer letters alone cannot.

Something important to keep in mind: a 2026 ProPublica investigation found that TransUnion resolved far fewer consumer complaints in people's favor after CFPB oversight weakened (ProPublica, 2026). The environment is tougher now. Strong documentation is not optional anymore; it is essential.

Can You Dispute the Same Item Again?

Yes, and sometimes you have to. TransUnion will take another look if you include new supporting documents. Do not just resend the same letter. Add something they have not seen yet — a payment receipt, a letter from your creditor, a court record. Fresh evidence is what moves the needle.

Not Sure What to Send to TransUnion?

Mailing your dispute to the right TransUnion dispute address is only the first step. The bigger challenge is knowing what to include, how to document the error, and what to do if the dispute gets rejected.

ASAP Credit Repair can help you review your credit report, identify inaccurate items, and build a stronger dispute strategy.

Get My Credit Report ReviewedTransUnion Dispute Address and Full Contact Details

Method: What You Need to Know. MailTransUnion Consumer Solutions, P.O. Box 2000, Chester, PA 19016-2000. Phone: 800-916-8800 (Mon–Fri 8 am–11 pm ET, Sat–Sun 8 am–5 pm ET)Onlinetransunion.com/credit-disputesEscalation555 West Adams Street, Chicago, IL 60661

No matter which method you choose, the same 30-day clock applies. Mail gives you the strongest legal standing. Use it whenever the error on your report is costing you something real, a loan approval, a rental, a job offer.

If all three bureaus show errors, know that Equifax and Experian have their own separate dispute addresses and processes. Fixing all three at the same time gets you the cleanest result.

The CFPB has a free dispute letter template and step-by-step guidance at consumerfinance.gov. It is worth bookmarking.