Wakefield And Associates collects debts for other companies. They started in 1986 and focus on medical bills like hospital visits, doctor fees, and ambulance rides.

About Wakefield And Associates

Wakefield And Associates is a debt collection agency based in Colorado, specializing in medical debt collection. They work with hospitals, clinics, and healthcare providers to collect unpaid bills from patients. Founded in 1986, they operate across several states, including Colorado and Tennessee.

How to Contact Them:

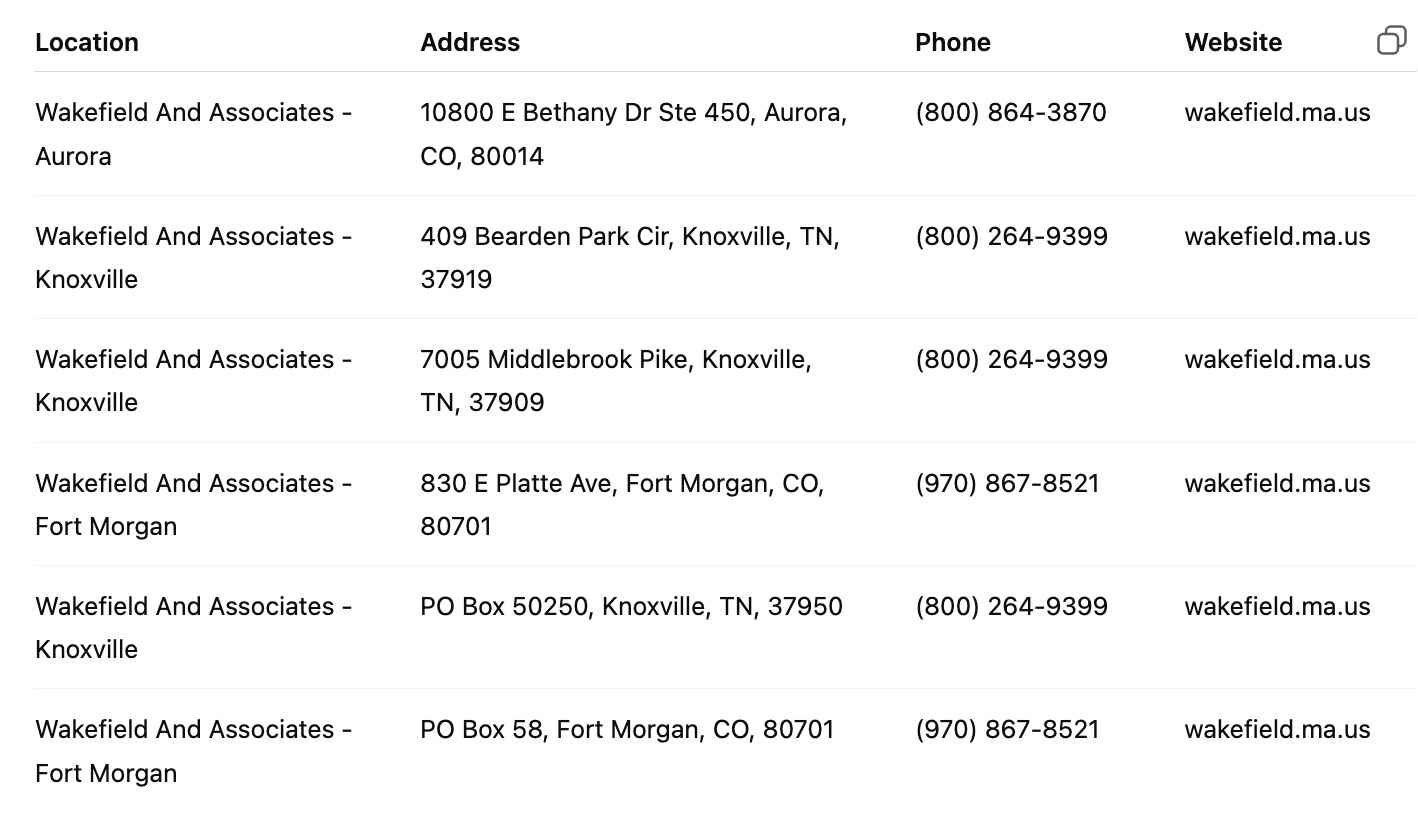

- Main Office: 10800 E Bethany Dr., Ste 450, Aurora, CO 80014-2697

- Phone: (970) 867-8521 or 303-537-2900

- Send Disputes To: C/O Compliance Team Department, Knoxville, TN 37995

- When They're Open: Monday-Thursday 8 AM-8 PM, Friday 8 AM-12 PM

Wakefield And Associates Locations Summary Table

Check if Wakefield And Associates shows up on your credit reports, get a full credit analysis to find out.

Is Wakefield And Associates Real or Fake?

Wakefield And Associates is a real company. They've been around for over 75 years. But scammers sometimes pretend to be them to steal your information. Always check if someone really works for them before giving out personal details.

If you see them on your credit report and don't know why, ask them to prove the debt is yours. If they break the rules, you can complain to your state's Attorney General, the FTC, or the CFPB.

Wakefield And Associates Reviews and Complaints

While the company is legitimate, your experience can vary greatly. Many consumers report mixed interactions with Wakefield And Associates. Some say they are professional and willing to work with you, while others describe aggressive tactics, errors, or difficulty getting clear answers.

According to the BBB and CFPB databases, common complaints include:

- Incorrect or surprise billing

- Failure to validate debts properly

- Repeated or harassing calls

Reading reviews and complaints can help you understand what to expect, and prepare you to stand up for your rights. If you believe Wakefield And Associates has violated debt collection laws, don’t hesitate to file a complaint and seek help.

Why Does Wakefield And Associates Appear on Your Credit Report?

Wakefield And Associates may show up on your credit report because they have been assigned or purchased a debt from another company you owed money to, most commonly a medical provider.

When you don’t pay a bill (like a hospital visit or doctor’s invoice) and it goes unpaid for a long time, the original creditor may either sell the debt to a collection agency or hire them to collect it on their behalf. Once Wakefield And Associates gets involved, they typically report the account to one or more credit bureaus (Experian, Equifax, and TransUnion).

Here’s why this happens:

- Unpaid medical bills: The most common reason. Even small bills can end up with a collector if ignored long enough.

- Insurance delays or denials: Sometimes, insurance doesn’t pay as expected, and the remaining balance gets turned over to collections.

- Missed or partial payments: Any gaps in payments can trigger collections.

- Incorrect or surprise bills: Errors in billing can also lead to an account being sent to collections if not resolved quickly.

Once a collection account is reported, it can remain on your credit report for up to seven years, even after you pay it off, unless you successfully negotiate a removal.

The Impact of a Collection Account from Wakefield And Associates

A collection account, especially from a medical debt, can severely damage your credit score. In fact, medical collections are one of the most common negative marks that hurt credit, sometimes dropping scores by 100 points or more.

Beyond just affecting your score, a collection account can also:

- Make it harder to get approved for loans or credit cards

- Increase your interest rates on future loans

- Impact your ability to rent a home or get utilities without a deposit

- Even affect employment opportunities in some fields

Got a Letter from Wakefield And Associates? Here's What to Do

Don’t panic if you get a letter from Wakefield And Associates. First, read it carefully and take a deep breath. The most important thing is to stay calm and avoid rushing into a payment without checking the details.

Many people feel pressured to pay immediately just to make the problem go away, but that’s a mistake. Before you do anything, verify that the debt is actually yours.

Look closely at the bill details. Do you recognize the medical visit or service? Check the date, the amount, and the provider’s name. If something doesn’t look familiar, or if you’re unsure, talk to a lawyer or a trusted credit repair professional before responding.

You have the right to ask for proof. Send a debt validation letter requesting that Wakefield And Associates show documentation that the debt is valid and belongs to you. By law, they must stop contacting you until they provide this proof.

Where to Send Your Letter:

Wakefield & Associates, LLC

C/O Compliance Team Department

Knoxville, TN 37995

“When I first got the letter, I was terrified and almost paid it right away. But after I asked for validation, it turned out they had the wrong person! I’m so glad I didn’t just pay without checking.” — Reddit user u/medicalbillnightmare

Taking these steps can save you from paying a debt that might not even be yours and protect your credit in the long run.

How to Fight a Wrong Debt

If Wakefield And Associates says you owe money but you don't think you do, send them a dispute letter. When you do this, they have to prove:

- The debt is really yours

- You still owe the money (it's not too old)

- They have permission to collect it

If they can't prove these things, contact your state's Attorney General or a lawyer. You have rights, and you can report companies that break the rules.

You can find sample dispute letters online to help you write yours. If you want a more personalized approach, you can also check out our guide on what should be included in your dispute letter.

What If I Can't Pay? Will They Take Less Money?

Some people wonder if they should pay the full amount or try to pay less. If you pay less than what they say you owe, it will still hurt your credit score for up to seven years. Only pay if you're sure the debt is yours and they can prove they have the right to collect it.

Be careful with payment plans. Read everything before you sign. Sometimes these plans cost more than you think.

You can ask them to remove the debt from your credit report if you pay. Get this deal in writing before you pay anything. Never let them take money directly from your bank account.

The best thing to do is prove the debt isn't yours if that's true. You might need an expert’s help with this.

Can Wakefield And Associates Take Me to Court?

They can't threaten to sue you just to scare you. But if you really owe the money and don't pay, they might take you to court.

Can They Take Money from My Paycheck?

If they sue you and win, a judge might let them take money from your paycheck to pay the debt.

Can They Have Me Arrested?

No, you can't be arrested just for owing money. But you could get in trouble if you ignore a court order about the debt.

How They Can Contact You

Wakefield And Associates must follow rules about how they contact you:

- They can only call during normal hours - usually not before 8 AM or after 9 PM

- If you tell them not to call you at work, they have to stop

- They can call, text, email, or mail you

- They can't call you too many times - that's harassment

If they're bothering you, write down every time they contact you. Note the date, time, and what they said. Threats are not allowed.

Other Languages: If you don't speak English well, you can ask for help in your language.

How to Complain About Wakefield And Associates

If they break the rules, you can complain to:

- Federal Trade Commission (FTC)

- Consumer Financial Protection Bureau (CFPB)

- Your state's Attorney General

- Better Business Bureau (BBB)

- Your state's consumer protection office

Can I Get Them Removed from My Credit Report If I Pay?

Even after you pay a debt collector, it can stay on your credit report for years. You can try to get them to remove it by offering to pay the full amount in exchange for taking it off your report. This is called a "pay for delete" letter.

Only do this if you have enough money to pay the full amount. Also, check if other people have had success with this company before.

Will This Hurt My Credit Score?

Yes, having a debt collector on your credit report can hurt your credit score. It can stay there for up to seven years and make it harder to get loans or credit cards.

Good News:

- Small medical bills (under $500) might not show up on some credit reports

- Paid collections don't hurt your score as much with newer scoring systems

- If your credit was good before, collections will hurt more

How to Remove Wakefield And Associates from Your Credit Report

If you challenge the debt and they can't prove it's yours, it might be removed from your credit report. ASAP Credit Repair helps people remove wrong or unfair items from their credit reports. Contact us if you need help removing these items.

Watch Out for Scams: Even though Wakefield & Associates is real, scammers use their name. Be careful if someone:

- Demands payment right away over the phone

- Threatens to arrest you

- Asks for gift cards or wire transfers

- Won't give you written proof

- Calls at weird hours

- Can't tell you details about the debt

Recommended Content

Disclaimer:

While we strive to provide up-to-date and accurate information, this content is for informational purposes only and does not constitute legal advice. Laws and practices may change over time. Always consult a qualified professional for guidance specific to your situation.