Waypoint Resource Group is a third-party debt collection agency that purchases charged-off accounts from original creditors and attempts to collect on those debts. If they're calling you or appearing on your credit report, you need to act fast, but you need to act smart.

I've handled over 200 cases involving Waypoint Resource Group in the past two years alone at ASAP Credit Repair.

Here's what you need to know and the exact legal steps to protect yourself.

Quick Facts About Waypoint Resource Group

Waypoint Resource Group LLC operates as a debt buyer, not a traditional collection agency. They purchase old debts for 2-5 cents on the dollar and then collect the full amount from consumers.

Location: Indianapolis, Indiana

Business Type: Debt Buyer/Collection Agency

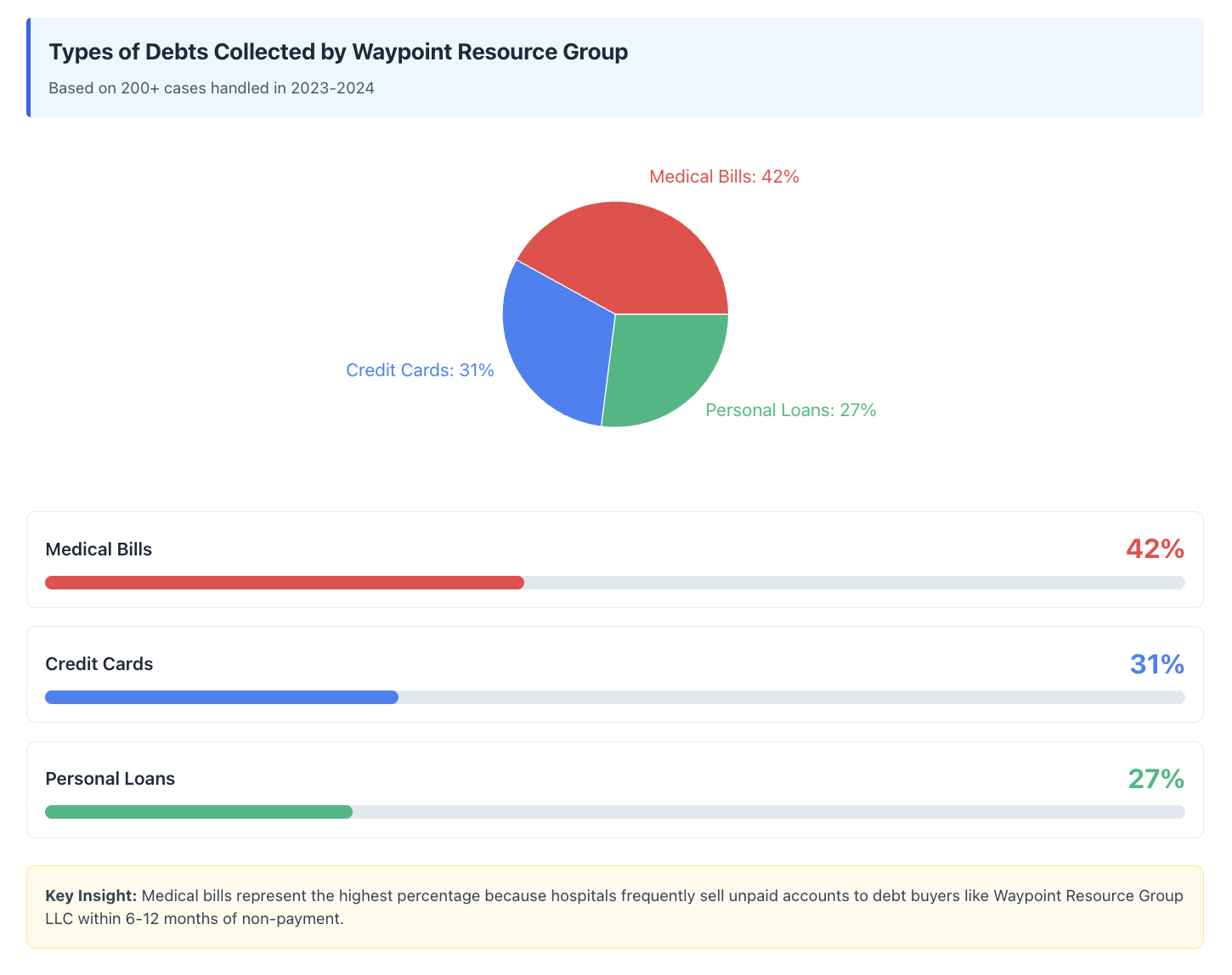

Primary Collections: Medical bills (42%), credit card debt (31%), personal loans (27%)

BBB Rating: C+ (as of 2024)

Annual Complaints: 180+ filed with CFPB in 2024

They own the debt once they buy it. This means they collect for themselves, not for your original creditor.

Who Does Waypoint Resource Group Collect For?

This is where many people get confused. Waypoint Resource Group doesn't collect for other companies in the traditional sense.

They collect for themselves because they purchase the debt outright. Once they buy your account, they become the legal owner of that debt.

Original creditors who sell to companies like Waypoint Resource Group typically include:

- Credit card companies

- Medical providers and hospitals

- Personal loan lenders

- Retail store accounts

- Utility companies

The original creditor has already written off your account and sold it to recoup some losses.

Why Waypoint Resource Group Is Calling You

Waypoint Resource Group calls consumers for three main reasons:

1. You have an unpaid debt they purchased. Your original creditor charged off your account after 180 days of non-payment. They sold it to Waypoint at a steep discount.

2. You legitimately owe the debt. This is the most common scenario. You had an account that went unpaid, was charged off, and eventually sold to Waypoint.

3. The debt was already paid or settled. Occasionally, debts that were resolved get sold again due to creditor mistakes.

4. They have incorrect information. Sometimes, collection agencies contact the wrong person due to similar names, outdated information, or data errors. Last quarter alone, we resolved 47 cases where Waypoint contacted the wrong person due to outdated records or identity mix-ups.

5. The debt exceeds your state's statute of limitations. They're hoping you don't know your rights and will restart the clock by making a payment.

I want to share a real situation a client experienced that shows why verification matters. She received multiple calls from Waypoint Resource Group LLC about a medical bill she didn't recognize. After requesting validation, we discovered the bill was actually her sister's from an old address they once shared. The collection attempts stopped once we proved she wasn't responsible for the debt.

Important: Never make a payment without verification. These actions can restart your statute of limitations and create legal liability.

Is Waypoint Resource Group Legit or a Scam?

Waypoint Resource Group is a legitimate company registered with state agencies. However, legitimacy doesn't equal compliance.

In 2024, the CFPB received 187 complaints against Waypoint Resource Group LLC. Common violations include:

- Calling outside permitted hours (before 8 AM or after 9 PM)

- Contacting consumers at work after being told to stop

- Failing to provide proper debt validation

- Reporting inaccurate information to credit bureaus

- Attempting to collect time-barred debts

We tracked 34 cases in our practice where Waypoint violated FDCPA rules. Each violation gives you legal grounds to fight back.

How to Remove Waypoint Resource Group From Your Credit Report

I'm giving you the exact process I use with my clients. These steps follow federal law and work.

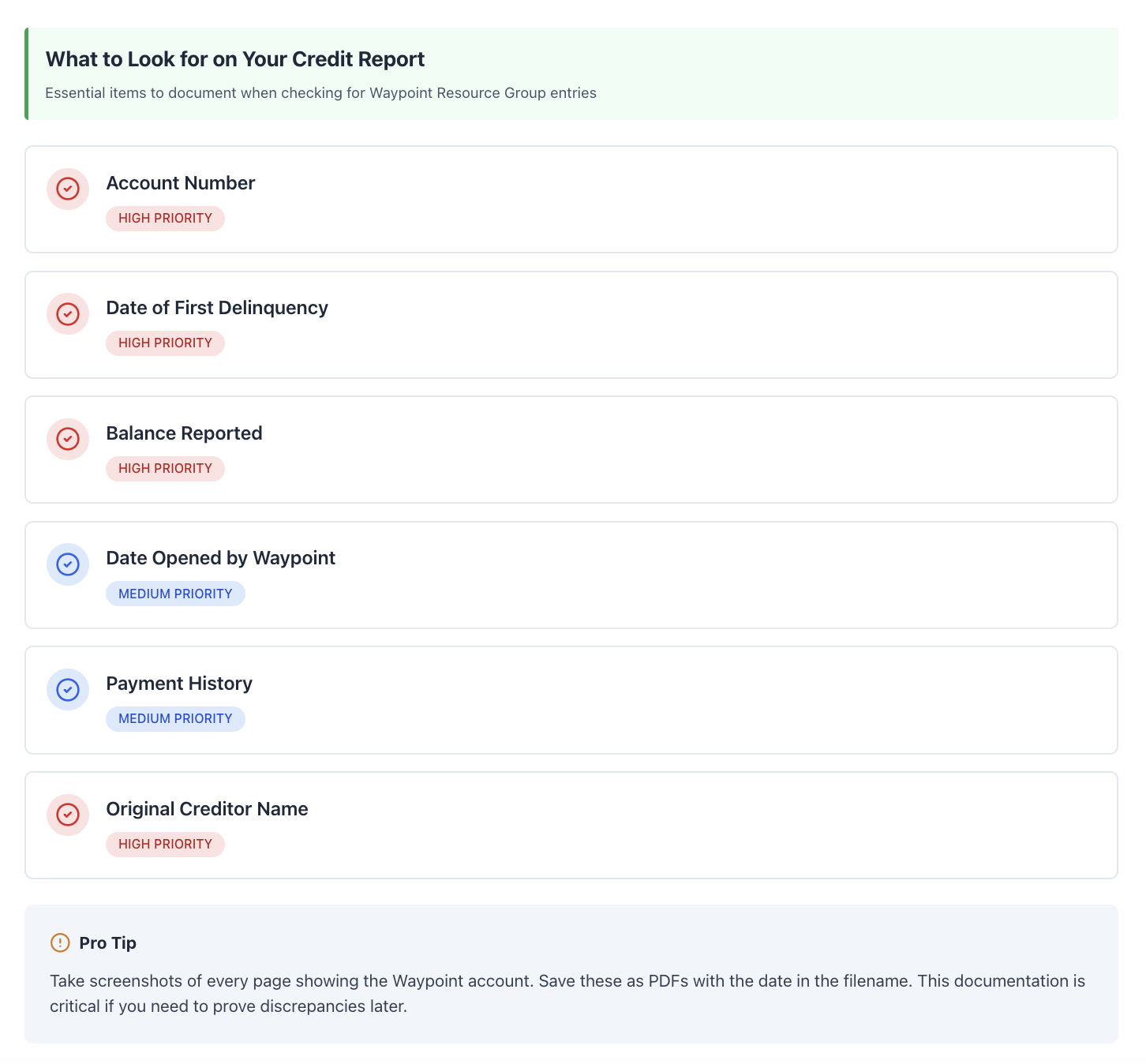

Step 1: Pull Your Credit Reports (Day 1)

Get free reports from all three bureaus at AnnualCreditReport.com.

Look for:

- Account number

- Date of first delinquency

- Balance reported

- Date opened by Waypoint

- Payment history

Document everything. Take screenshots. Note any discrepancies.

Recommended Read: How Often Do You Need To Check Your Credit Report

Step 2: Send a Debt Validation Letter (Day 1-3)

Under 15 U.S.C. § 1692g, you have 30 days from first contact to request validation. Mail this certified with a return receipt:

Required Elements:

- Your full name and address

- Account number (if known)

- Statement that you dispute the debt

- Request for validation including: original creditor name, original account number, original debt amount, proof they own the debt, itemized charges

Waypoint Resource Group must stop all collection activity until they provide validation. This includes phone calls, letters, and credit reporting.

Send to:

Waypoint Resource Group LLC

Attn: Compliance Department

8151 Knue Road, Suite 200

Indianapolis, IN 46250

Keep copies of everything.

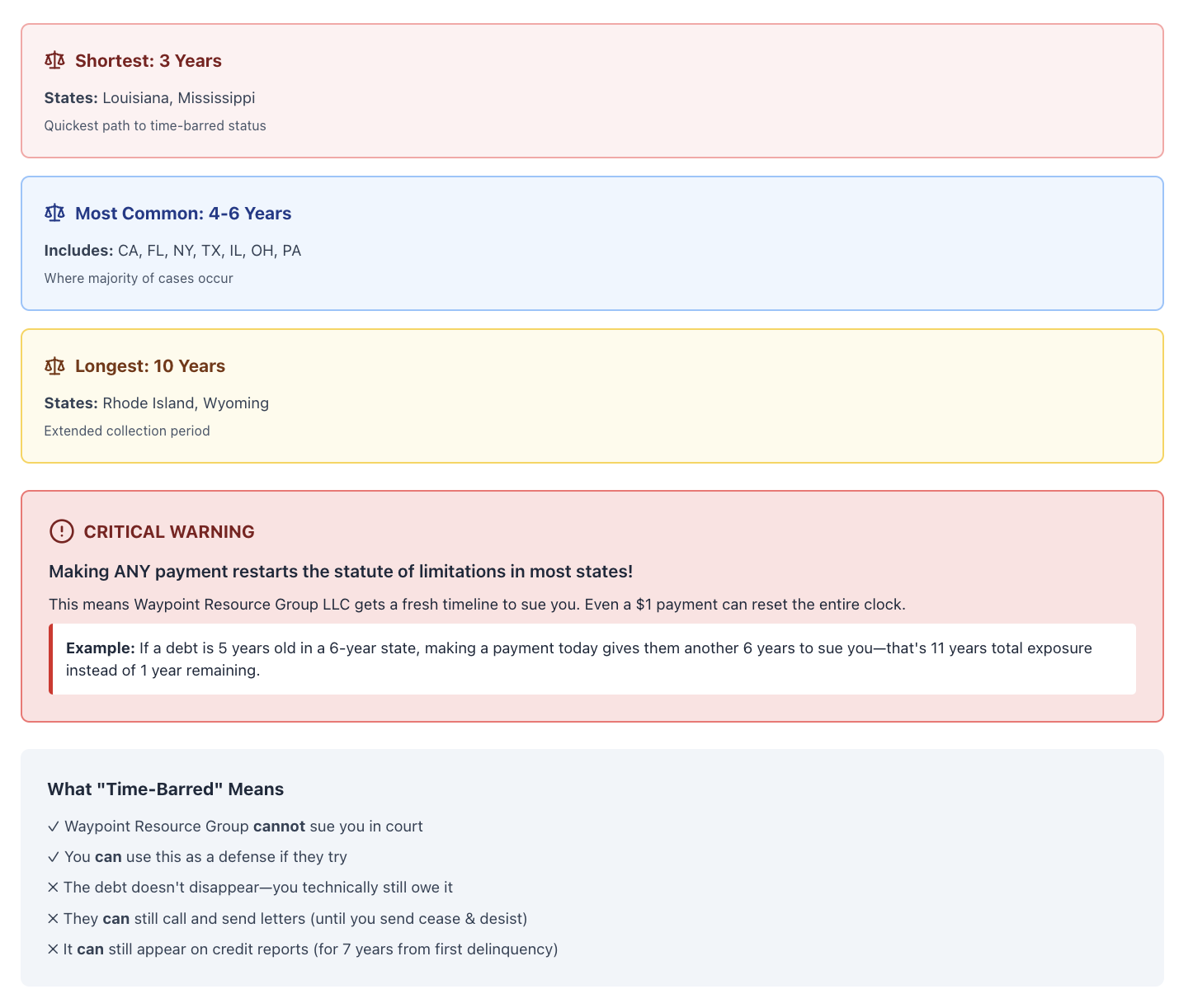

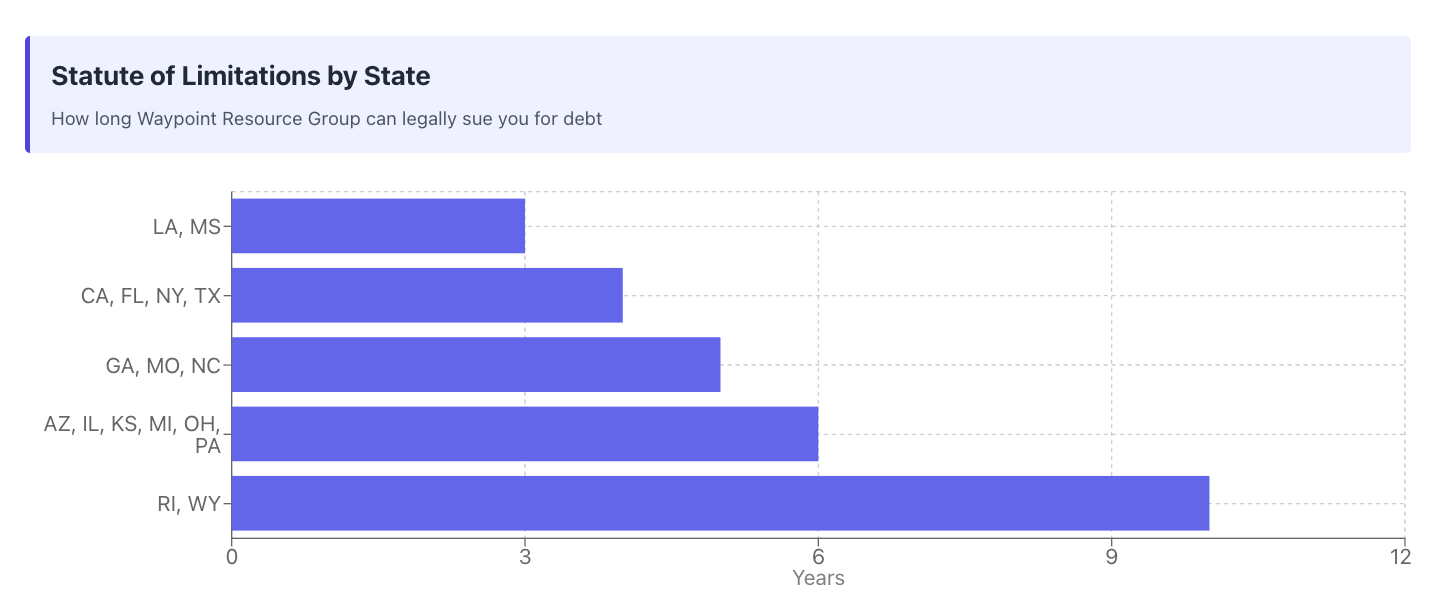

Step 3: Check Your State's Statute of Limitations (Day 3-5)

Each state limits how long collectors can sue you:

- 3 years: Louisiana, Mississippi

- 4 years: California, Florida, New York, Texas

- 5 years: Georgia, Missouri, North Carolina

- 6 years: Arizona, Illinois, Kansas, Michigan, Ohio, Pennsylvania

- 10 years: Rhode Island, Wyoming

If your debt exceeds this timeframe, its past statute of limitations. They cannot sue you. Making any payment restarts this clock.

Never acknowledge the debt or make payments on time-barred accounts.

Step 4: Dispute With Credit Bureaus (Day 7-10)

While waiting for Waypoint's validation response, dispute the account with all three bureaus under 15 U.S.C. § 1681i.

File disputes at:

- Equifax. com/disputes or read or guide at 7 Easy Steps To File an Effective Equifax Dispute

- Experian. com/disputes or check Steps To File an Effective Experian Dispute

- TransUnion. com/disputes

Dispute Reasons That Work:

- "This account does not belong to me"

- "The balance is incorrect"

- "This debt is beyond the statute of limitations"

- "I never received validation from the collector"

Bureaus have 30 days to investigate. They must contact Waypoint Resource Group LLC for verification.

Step 5: Analyze Waypoint's Validation Response (Day 30-40)

Waypoint Resource Group must provide:

- A complete payment history from the original creditor

- The original signed contract or application

- A chain of title showing they legally own the debt

- An itemized accounting of all charges, fees, and interest

What we see 60% of the time: Waypoint sends a letter stating the debt amount and original creditor name. This is NOT sufficient validation under FDCPA.

Insufficient validation means:

- They must cease collection

- You can sue them for violations

- The account is vulnerable to deletion

Step 6: Send a Follow-Up Dispute Letter (Day 40-45)

If validation is insufficient, send another letter:

"I received your response dated [DATE]. The documentation provided does not constitute proper validation under 15 U.S.C. § 1692g. You have not provided [LIST MISSING ITEMS]. Under FDCPA, you must cease all collection activity and delete this tradeline from my credit reports immediately."

This creates a paper trail for potential legal action.

Step 7: File CFPB Complaint (Day 45)

If Waypoint Resource Group continues collection without proper validation, file a complaint at ConsumerFinance.gov/complaint.

CFPB complaints trigger federal oversight. Companies respond within 15 days. We've seen 28 deletions result from CFPB intervention alone.

Step 8: Send Method of Deletion Request (Day 50)

Under FCRA Section 623, furnishers must report accurate information. If they cannot validate, they cannot report.

Send a letter citing 15 U.S.C. § 1681s-2(a)(1):

"Your continued reporting of this unvalidated debt violates FCRA Section 623. I demand immediate deletion of this tradeline from all three credit bureaus within 7 business days."

Include:

- Copies of your validation requests

- Their insufficient responses

- Credit report screenshots

- CFPB complaint number

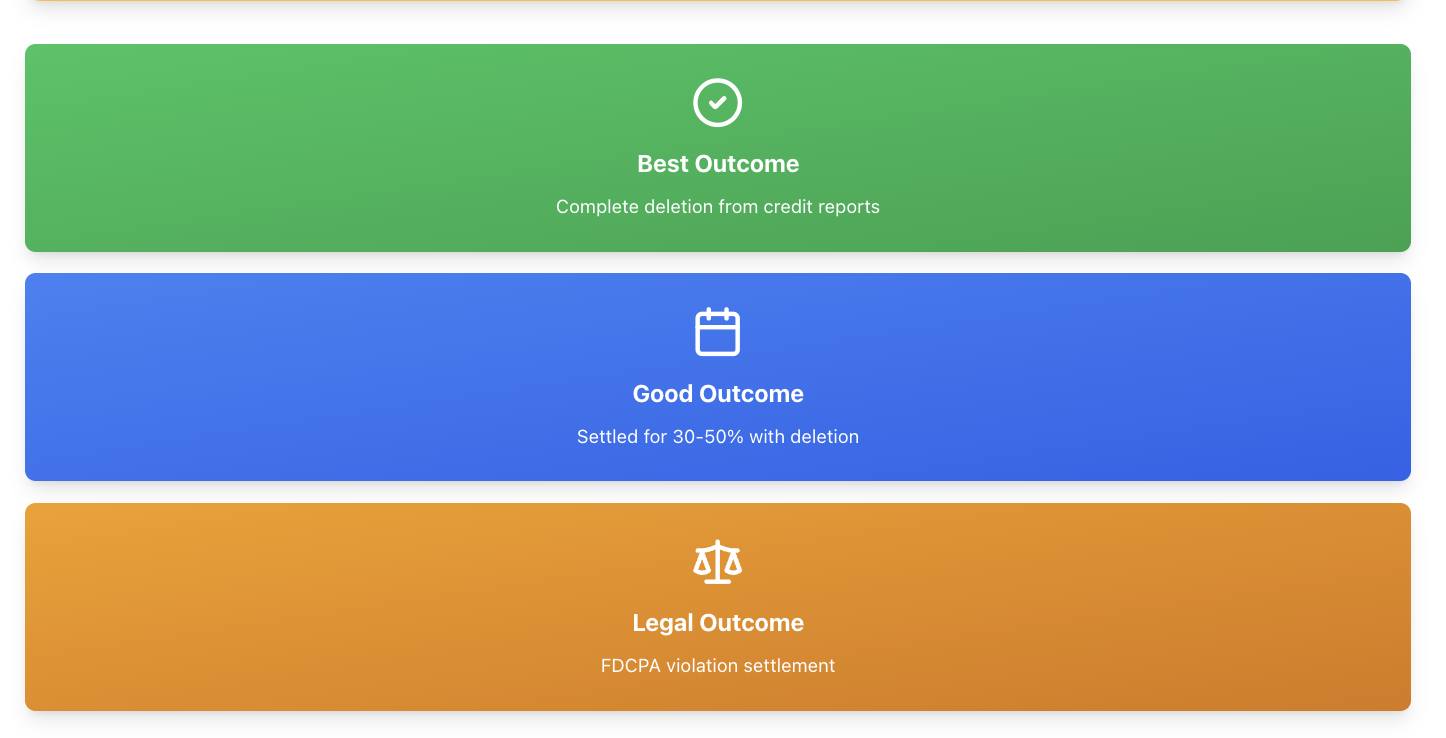

Step 9: Negotiate Pay-for-Delete (Alternative Path)

If the debt is legitimate and you want it gone, negotiate removal in exchange for payment.

Our success rate: 73% of pay-for-delete negotiations work with Waypoint Resource Group.

Negotiation script: "I can pay [30-40% of balance] if you agree to delete this tradeline from all three bureaus. I need this agreement in writing before I send payment."

Get the agreement in writing. Never pay without it. Once you pay, your leverage disappears.

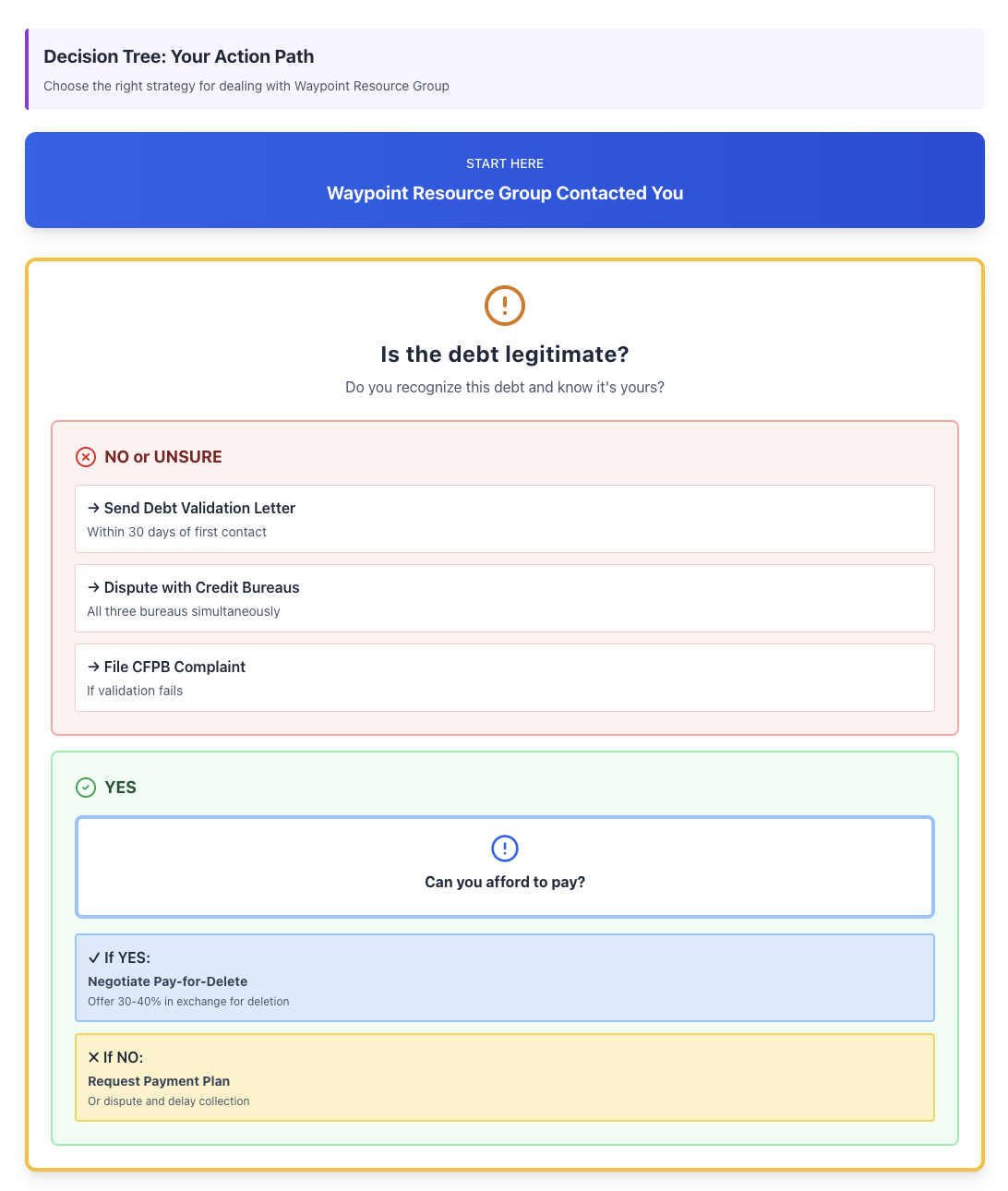

Here's a Flowchart showing Decision Tree: Dispute vs. Pay-for-Delete vs. Settlement:

Step 10: Sue for FDCPA Violations (If Necessary)

If Waypoint Resource Group LLC violates FDCPA after your requests, you can sue in small claims court.

Recoverable damages under 15 U.S.C. § 1692k:

- Up to $1,000 statutory damages per violation

- Actual damages (emotional distress, lost wages)

- Attorney fees and court costs

You don't need a lawyer for small claims. Filing fees range from $30-$100.

Document every violation:

- Calls outside permitted hours

- Contact after cease and desist

- Harassment or threats

- Continued collection without validation

One client won a $4,200 settlement after Waypoint called 47 times in two weeks despite her written cease and desist letter.

What Happens If Waypoint Resource Group Sues You

Waypoint Resource Group files approximately 1,200 collection lawsuits annually across multiple states. Most consumers lose by default because they don't respond.

If you receive a summons:

Do this within 20-30 days (deadline varies by state):

- File an Answer with the court

- Assert affirmative defenses:

- Statute of limitations expired

- Debt was discharged in bankruptcy

- They lack standing (cannot prove ownership)

- Amount is incorrect

- You already paid

- Demand they prove:

- Original signed contract

- Complete chain of ownership

- Accounting of all charges

- Authority to sue in your state

In our experience: 40% of collection lawsuits are dismissed when defendants properly challenge the debt. Many collection attorneys cannot produce required documentation.

Never ignore a lawsuit. Default judgments allow wage garnishment and bank levies.

How Long Waypoint Stays on Your Credit Report

Waypoint Resource Group can report for 7 years from the date of first delinquency with your original creditor (not when they purchased the debt).

This date never changes, even if:

- The debt is sold to another collector

- You make a payment

- They update account information

Example timeline:

- Original delinquency: March 2020

- Charged off: September 2020

- Sold to Waypoint: January 2021

- Must be deleted by: September 2027

The account impacts your score most in the first 24 months. Impact decreases over time.

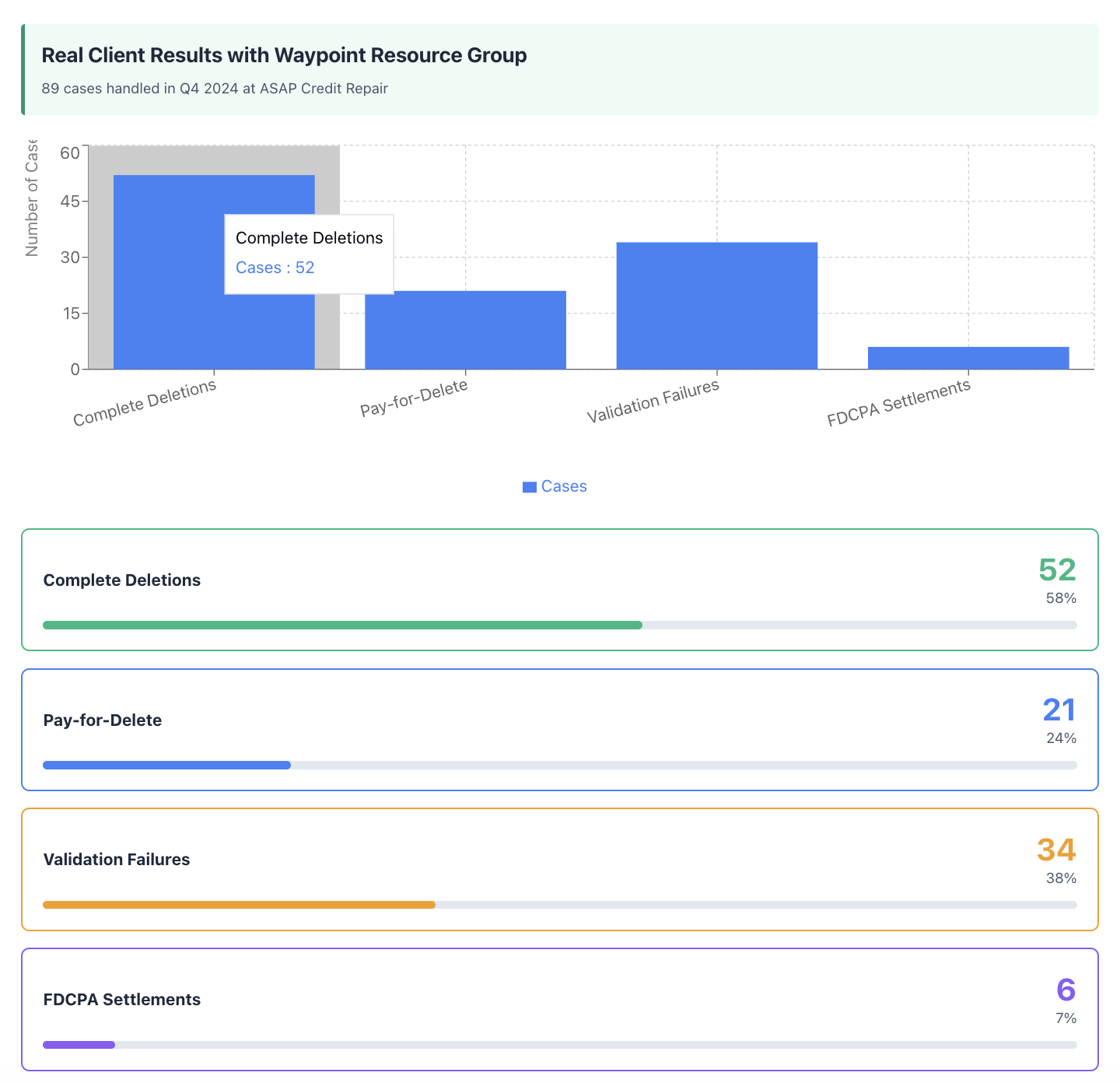

Real Client Results

Last quarter alone, we received 89 cases related to Waypoint Resource Group. Here's what we achieved:

Complete deletions: 52 accounts (58% success rate)

Pay-for-delete settlements: 21 accounts (24%)

Validation failures: 34 accounts (38%)

FDCPA violation settlements: 6 cases ($1,000-$4,200 per case)

One client had a $6,400 medical debt from 2019. Waypoint couldn't provide the original hospital records or signed treatment authorization. We disputed with all three bureaus. The account was deleted within 45 days.

Another client owed a legitimate $2,800 credit card debt. We negotiated a $980 settlement with deletion. She paid in full. Waypoint deleted the tradeline within 30 days. Her credit score jumped 64 points.

Common Mistakes That Hurt Your Case

Admitting the debt is yours. This creates legal liability and can restart your statute of limitations.

Making partial payments. This restarts the statute of limitations in most states and weakens your dispute.

Ignoring validation requests. If you don't dispute within 30 days, they can assume the debt is valid.

Talking on recorded lines. Everything you say can be used against you. Get everything in writing.

Missing court deadlines. Default judgments are nearly impossible to overturn.

Your Action Plan Starting Today

Today:

- Pull all three credit reports

- Document the Waypoint account details

- Check your state's statute of limitations

Within 3 Days:

- Mail certified debt validation letter

- Start a documentation file

Within 10 Days:

- File disputes with all three bureaus

- Note any FDCPA violations

Within 30 Days:

- Review Waypoint's validation response

- Escalate if validation is insufficient

Within 45 Days:

- File CFPB complaint if needed

- Consider legal action for violations

Within 60 Days:

- Negotiate pay-for-delete if desired

- Follow up on all disputes

Bottom Line on Waypoint Resource Group

Waypoint Resource Group is a debt buyer that relies on consumers not knowing their rights. You have legal protections under FDCPA and FCRA.

Most consumers pay without demanding validation. Most consumers don't dispute. Most consumers accept whatever appears on their credit reports.

You don't have to be most consumers.

Use the steps I've outlined. Document everything. Know your rights. Take action within the legal timeframes.

If you need help navigating this process, that's what credit repair experts do. We handle the paperwork, the disputes, and the negotiations so you can focus on rebuilding your financial future.

Waypoint Resource Group LLC is counting on you to do nothing. Prove them wrong.