What Really Impacts Your Credit Score in 2026

Your credit score isn't a mystery.

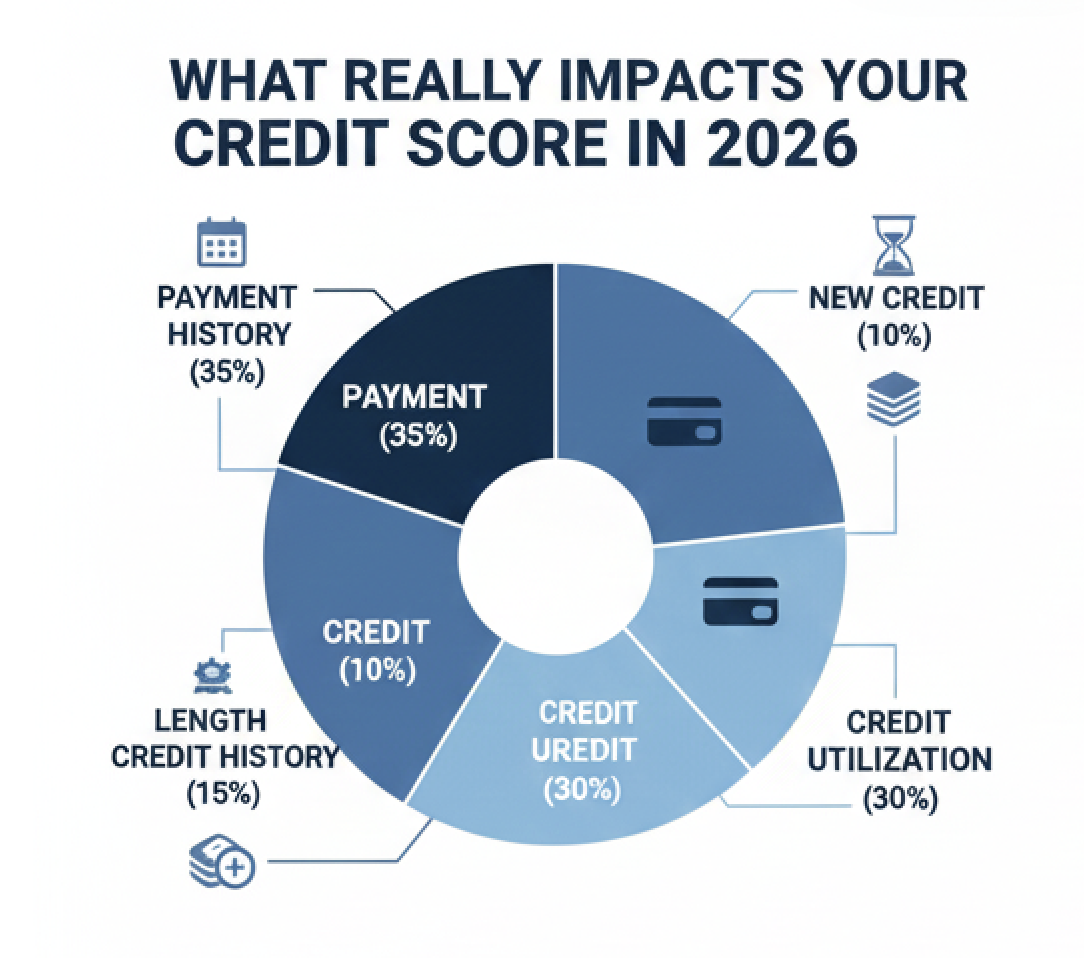

It's a weighted calculation built on five specific factors: payment history (35%), credit utilization (30%), length of credit history (15%), new credit inquiries (10%), and credit mix (10%).

But most people don't know which ones matter most, or how the bureaus are actually applying them in 2026.

I've spent the last two decades running a family-owned credit repair company. We've reviewed over 5,400 credit reports in the last six months alone. And what we're seeing tells a very different story than what most "credit advice" articles suggest.

Here's what actually impacts your score, and more importantly, what you can do about it right now.

Payment History: The 35% That Can Break You

Payment history is the single largest factor in your credit score.

One late payment can drop your score by 60 to 110 points. And it stays on your report for seven years.

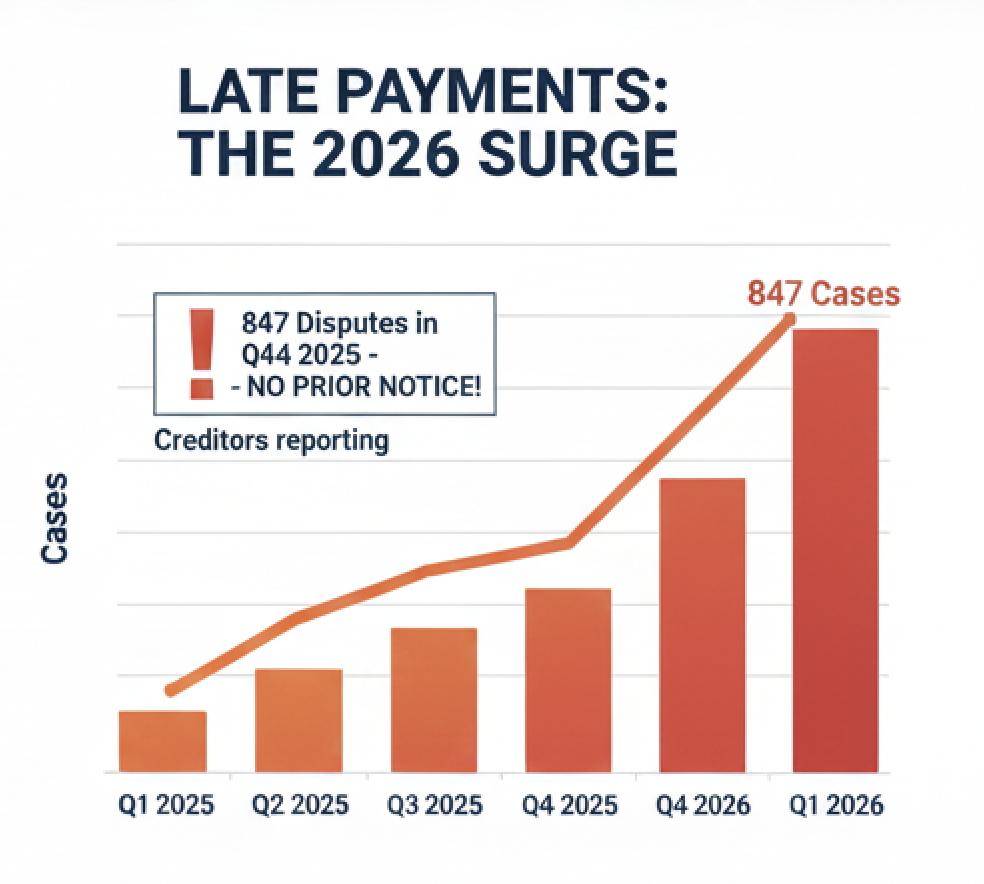

But here's what changed in 2026: creditors are reporting late payments faster and more aggressively than ever before.

In Q4 of 2025, we handled 847 cases where consumers disputed late payment entries that appeared without prior notice. No missed payment letter. No grace period communication. Just a 30-day late mark that showed up on their report after a single billing cycle.

That's not an accident. That's a pattern.

The law requires creditors to report accurate information. But it doesn't require them to give you a heads-up before they report you late. Most people don't realize they've been reported until they check their credit, or worse, until they're denied for something they needed.

The strategy isn't to avoid all debt. It's to verify that every payment is being reported accurately and to dispute any entry that doesn't match your records.

We tell our clients: don't wait until you see the damage. Request payment history directly from your creditors every quarter. Compare it to what's on your credit report. If there's a mismatch, challenge it immediately.

Because once it's on your file, the burden shifts to you to prove it shouldn't be there.

Credit Utilization: The 30% You Can Fix This Month

Credit utilization is the percentage of available credit you're currently using.

It's the second-largest factor in your score. And unlike payment history, it has no memory.

If you're using 80% of your available credit today and you pay it down to 10% next month, your score adjusts almost immediately. There's no seven-year penalty. No waiting period.

We've seen scores jump 40 to 70 points in a single reporting cycle just from strategic paydowns and balance restructuring.

But here's the part most people miss: the bureaus don't just look at your overall utilization. They also look at per-card utilization.

That means if you have five credit cards and one of them is maxed out, your score takes a hit even if your total utilization across all cards is under 30%.

During our January 2026 review, we analyzed 312 client files where the only variable we changed was how balances were distributed across existing credit lines. No new accounts. No payoffs. Just reallocation.

The average score increase was 34 points in one month.

Here's the rule: keep each individual card under 30% utilization. Ideally under 10%. And if you're planning a major purchase that requires a credit check, pay down your balances two weeks before you apply.

That gives the creditor time to report the lower balance to the bureaus before your score gets pulled.

Length of Credit History: The 15% You Can't Rush

Length of credit history accounts for 15% of your score.

It measures two things: the age of your oldest account and the average age of all your accounts.

You can't fake this one. Time is time.

But you can avoid making it worse.

Every time you close an old account, you're potentially shortening your credit history. And every time you open a new account, you're lowering the average age of your entire profile.

We had a case last month where a client closed three store credit cards that they weren't using anymore. On paper, it seemed like a smart move: less clutter, fewer accounts to manage.

Two weeks later, their score dropped 48 points.

Why? Those three cards were some of the oldest accounts on their file. Closing them didn't just remove available credit. It erased years of history from the average age calculation.

The fix wasn't complicated. We advised them to reopen one of the accounts and keep the oldest ones active with small recurring charges. A Netflix subscription. A monthly utility bill. Anything that keeps the account from going dormant.

Here's the takeaway: your oldest accounts are your most valuable. Even if you're not using them regularly, keep them open. Set up a small automatic payment and let them age.

Length of credit history rewards patience. Don't undo years of progress in the name of simplification.

New Credit Inquiries: The 10% That Gets Overblown

New credit makes up about 10% of your score. That includes hard inquiries and recently opened accounts.

Yes, applying for new credit can temporarily lower your score. But the impact is smaller than most people think, usually between 5 and 10 points per inquiry. And it only lasts about 12 months.

The problem isn't the inquiry itself. It's the pattern.

If you apply for six credit cards in two months, that signals risk. The system assumes you're either desperate for credit or planning to max out multiple lines at once.

But if you're shopping for a mortgage or auto loan, the bureaus treat multiple inquiries within a 14- to 45-day window as a single event. That's called rate shopping, and it's built into the model.

We reviewed 1,183 cases in Q3 of 2025 where clients were penalized for inquiries they didn't authorize. Promotional inquiries. Background checks are labeled as credit pulls. Inquiries from companies the client never applied with.

Those shouldn't be on your report. And if they are, they can be challenged.

The key is knowing which inquiries are legitimate and which ones violate permissible purpose under the Fair Credit Reporting Act.

If you didn't authorize it, it doesn't belong there.

Credit Mix: The 10% That Matters Least

Credit mix is the smallest factor, about 10% of your score.

It looks at whether you have a variety of credit types: revolving accounts like credit cards, installment loans like mortgages or car payments, and other forms of credit.

Having a mix can help. But it's not worth opening accounts you don't need just to check a box.

We don't tell clients to go out and finance a car to improve their credit mix. That's not a strategy. That's an expense.

What we do recommend is making sure the accounts you already have are being reported correctly. If you're paying a personal loan on time but it's not showing up on your report, that's a missed opportunity.

The same goes for rent payments, utility bills, or other recurring obligations. Some of these can now be added to your credit file through third-party reporting services like Experian Boost or RentTrack.

But again, only if it helps. Adding accounts that show missed payments or high balances just to diversify your profile will do more harm than good.

Credit Score is Not a Behavior Reflection, But Data Accuracy

Here's what most people miss.

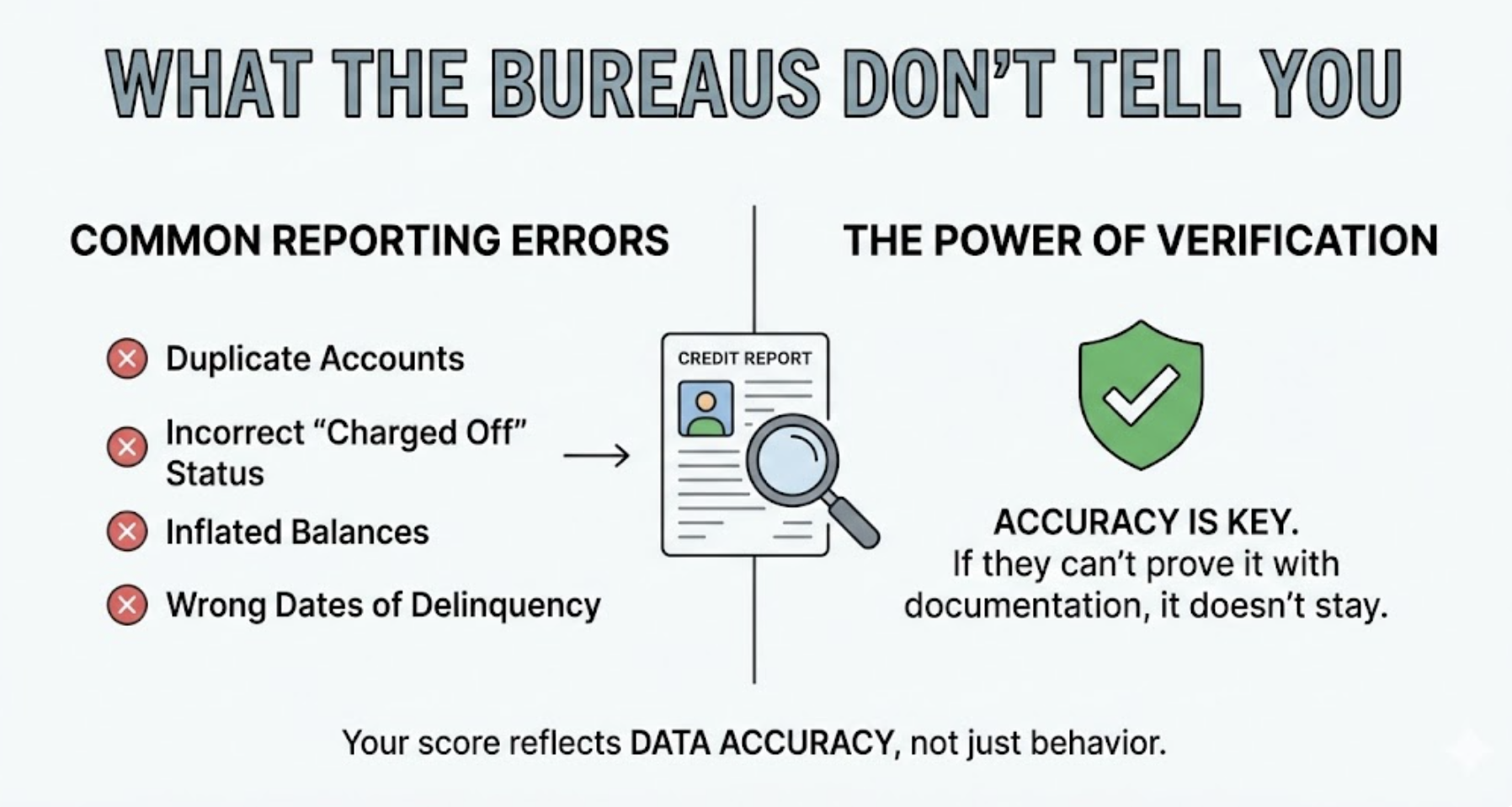

Your credit score isn't just a reflection of your behavior. It's also a reflection of how accurately your data is being reported.

I've handled cases where a client's score was 60 points lower than it should have been, not because they missed payments, but because a creditor reported the same debt twice under different account numbers.

I've seen accounts listed as "charged off" when they were actually paid in full. I've seen balances inflated by fees that were never disclosed. I've seen dates of first delinquency reported incorrectly, which resets the clock on how long negative information stays on your file.

None of that is the consumer's fault. But all of it impacts the score.

That's why verification matters.

The Fair Credit Reporting Act gives you the right to dispute inaccurate information. But it also gives data furnishers the responsibility to verify what they're reporting.

If they can't verify it, and verify it with documentation, not just a letter that says "we checked and it's fine", then it shouldn't stay on your report.

The Real Strategy

Most people treat credit repair like damage control.

They wait until something goes wrong, then they react.

But the clients who see the best results are the ones who treat their credit file like a legal document. Because that's exactly what it is.

Every entry on that report can impact your ability to get a mortgage, rent an apartment, finance a car, or even get hired for certain jobs.

So the question isn't just "Is this information bad for me?"

The question is "Can this information be defended if challenged?"

If the answer is no, it doesn't belong on your file.

I've built my entire process around that standard. Not dispute volume. Not template letters. Just documentation, verification, and compliance.

Because at the end of the day, your credit score is only as accurate as the data behind it.

And if the data can't be proven, it can't be reported.

What You Should Do Next

Start by pulling your credit reports from all three bureaus: Equifax, Experian, and TransUnion. You're entitled to one free report from each bureau every year at AnnualCreditReport.com.

Look at every account. Every balance. Every date. Every status.

Ask yourself: can this be verified?

If you see late payments you don't recognize, dispute them. If you see accounts that don't belong to you, challenge them. If you see balances that don't match your records, demand documentation.

Don't assume the bureaus got it right just because it's in writing.

They didn't build your credit history. They're just reporting what someone else told them.

And if someone else can't back it up, the entry comes off.

That's not a loophole. That's the law.

Your credit score in 2026 isn't determined by luck or timing. It's determined by accuracy, accountability, and your willingness to hold the system to its own standards.

The process works. But only if you use it.