If you are wondering what is a debt collection agency, they're a company that collects unpaid debts on behalf of original creditors. If you have received a collection letter, phone call, or discovered a collection account on your credit report, you may be wondering what a debt collection agency actually does.

Debt collection has become a major industry in the United States. According to the Consumer Financial Protection Bureau (CFPB), millions of consumers interact with debt collectors each year regarding credit cards, medical bills, personal loans, auto loans, utilities, and other unpaid accounts.

Many consumers assume the company contacting them is the original creditor. In reality, the debt may have been assigned to a third-party collection agency or sold to a debt buyer that now owns the account.

Understanding how debt collection agencies operate, how they acquire debt, what rights consumers have under federal law can help consumers make informed decisions and avoid costly mistakes.

What Is a Debt Collection Agency?

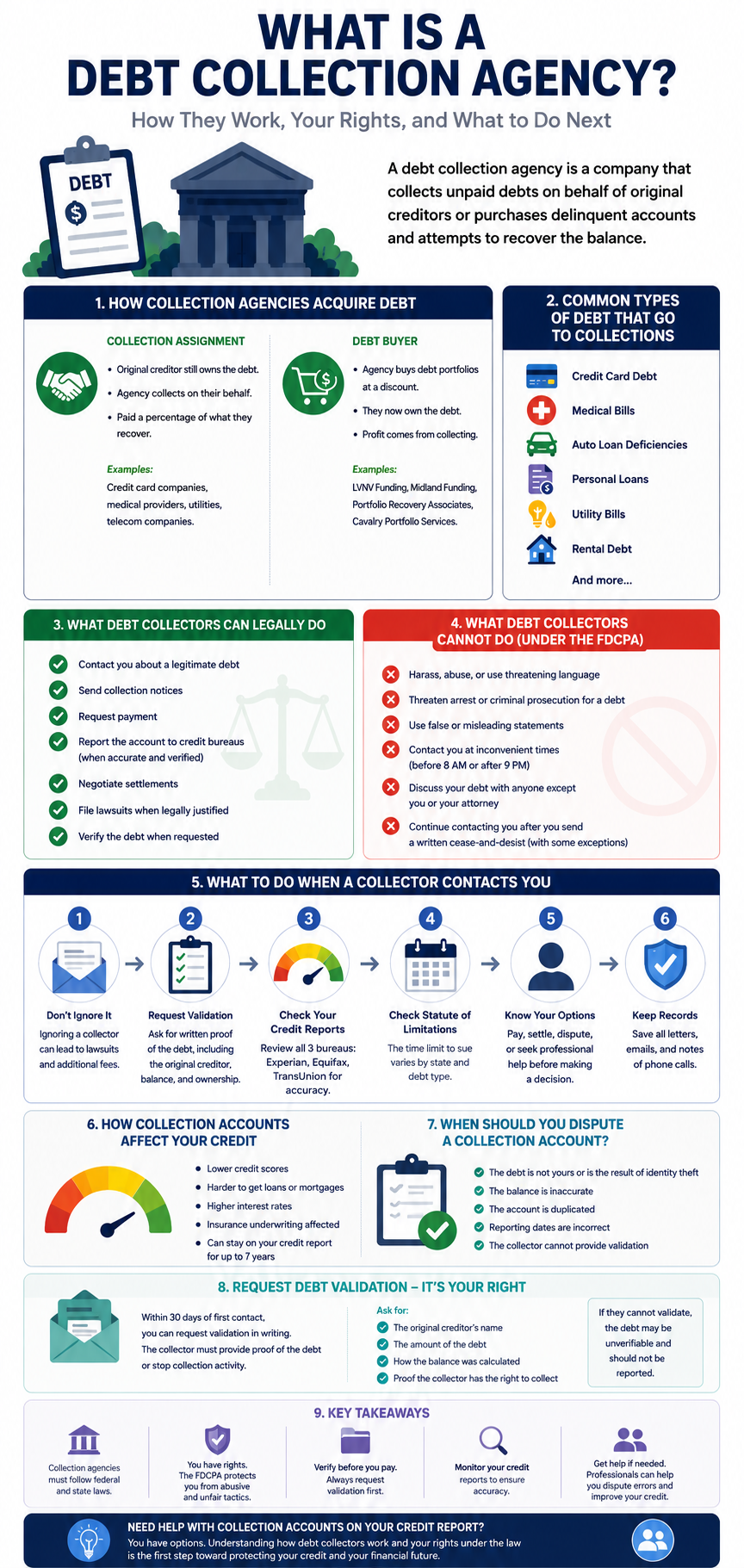

Looking at the infographic below, you can easily understand what is a debt collection agency.

How Debt Gets From You to a Collection Agency

The path from a missed payment to a collection call has several steps. Each one matters.

A credit card, medical bill, loan, or utility bill goes unpaid. The original creditor marks the account as delinquint. Late payment marks appear on your credit report at 30, 60, and 90 days.

Usually after 90 to 180 days of non-payment, the creditor writes the debt off their books as a loss. This is called a charge-off. It is an accounting event, not debt forgiveness. You still owe the money.

The creditor either hires a third-party collection agency (assignment) or sells the account to a debt buyer. In both cases, a new company is now trying to collect your debt.

Calls, letters, emails, or texts arrive from the collector. They may also report a collection account to the three credit bureaus. This is often when consumers first learn the debt has moved to collections.

The Two Types of Debt Collection Agencies

Works for: The original creditor

Owns the debt: No , the original creditor still owns it

Paid by: A percentage of what they collect (typically 25% to 50%)

Goal: Recover as much as possible for the creditor

What they report: May report a collection account while the original account also shows on the report

Works for: Themselves , they own the debt

Owns the debt: Yes , they aquired it from the original creditor

Paid by: Whatever they collect (paid pennies, keep dollars)

Goal: Maximize recovery on a portfolio they bought cheaply

What they report: Reports as a new collection account, often years after the original charge-off

The Largest Debt Buyers in the United States

These companies purchase and collect billions in debt portfolios each year.

What Types of Debt Go to Collections

What Debt Collectors Can and Cannot Do Under the FDCPA

As NerdWallet's FDCPA guide confirms, the law limits when and how collectors can contact you. They cannot call before 8 a.m. or after 9 p.m. They cannot call more than seven times per week per debt. They cannot share your debt details with unauthorized third parties. These are not policies , they are federal rules with enforcement teeth.

- Contact you by phone, mail, email, or text

- Send a written validation notice within 5 days of first contact

- Request payment on a legitimate debt

- Report the collection account to credit bureaus

- Negotiate a setlement for less than the full balance

- File a lawsuit when legally permitted

- Contact your attorney if you have one

- Call before 8 a.m. or after 9 p.m.

- Call more than 7 times per week per debt

- Threaten arrest for unpaid consumer debt

- Use abusive or harassing language

- Misrepresent the amount owed or their legal authority

- Discuss your debt with neighbors, coworkers, or family without permission

- Continue contacting you after a written cease request

Real Example: Why Validation Stopped a $2,400 Collection

A consumer received collection calls for a $2,400 credit card debt. The collector demanded payment immediately. The consumer had not verified whether the debt was accurate or whether the collector could document ownership.

Instead of paying, the consumer sent a written debt validation request. The validation process revealed: incorrect balance calculations, missing account records from the original creditor, and incomplete ownership documentation showing the transfer of the account from creditor to collector.

The collector ultimately closed the account. The consumer did not pay.

The lesson: a debt collection agency must be able to prove the debt is valid, that the balance is accurate, and that they have the legal authority to collect it. Many debt buyers , especially those who aquired accounts in large portfolio purchases , cannot produce complete documentation for every account. That documentation gap is where disputes succeed.

Many consumers focus on one thing: making the collection calls stop.

They pay the collector. The calls stop.

But the collection account stays on the credit report for seven years from the original delinquency date. Paying does not remove it. The score damage continues.

A collection account can prevent mortgage approval, raise car insurance rates, and block apartment applications , long after the last phone call was ever made.

Addressing the collection activity and addressing the credit report impact are two seperate strategies. Both matter. Most consumers handle one and ignore the other.

"I've reviewed files where a consumer paid off a collection years ago. They were proud they paid. They called the debt resolved. And then they come to us wondering why they still can't get approved for a mortgage. The collection is still on the credit report , paid status, but still there. Paid doesn't mean removed. Seven years from the original delinquency date is when it legally must come off. That's the timeline the FCRA sets. Paying before that date doesn't shorten it. The only way to shorten it is a successful dispute, a pay-for-delete agreement that actually gets honored, or the 7-year window expiring on its own."

Joe Mahlow's team at ASAP Credit Repair reviews every collection account for reporting errors, validation gaps, inaccurate balances, and wrong delinquency dates , the specific issues that make collection accounts disputable under the FCRA and FDCPA.

Get a Free Credit Review →What to Do When a Debt Collector Contacts You

As Experian's FDCPA guide confirms, when a collection agency contacts you, the amount of interest charged is often dictated by the original contract , and you have the right to request documentation of the debt before making any payment.

How Collection Accounts Affect Credit Scores and Loan Applications

A collection account is among the most damaging entries a credit report can contain. The damage is not just the score drop. It is the downstream impact that follows.

- Credit score. A single collection can drop a 720 score by 60 to 100 points depending on the profile. A score in the 580-620 range may drop 20 to 40 points from an additional collection.

- Mortgage approval. Most mortgage lenders require a score above 580 for FHA loans and above 620 for conventional loans. A collection can push a borderline score below these thresholds.

- Auto loan terms. Auto lenders use a separate FICO Auto Score. Collections push borrowers into subprime tiers with rates above 15%.

- Apartment applications. Most landlords screen for collection accounts. A delinquint debt from a prior landlord is particularly damaging.

- Insurance underwriting. In many states, credit scores affect auto and homeowners insurance premiums. Collection accounts can raise premiums.

Understanding this full impact is why ASAP Credit Repair reviews both the collection activity and the accuracy of the balance being reported , including whether any interest added to the balance is properly authorized.

Decision Framework , What to Do Based on Your Situation

As Bankrate's FDCPA guide confirms, documenting all communication with the debt collector and keeping records of every letter sent and received is one of the most important protections consumers have when dealing with collection agencies , especially if a dispute becomes necessary later.

Related Questions

Is a debt collection agency the same as the original creditor?

No. The original creditor is the bank, hospital, or company you originally owed money to. A debt collection agency is either a third party hired by the creditor to collect on their behalf or a debt buyer that aquired your account outright. The original creditor and the collection agency are separate companies. In many cases, when a debt buyer contacts you, the original creditor has already written the account off and moved on , the buyer is now the entity pursuing the balance.

Can a debt collector sue me?

Yes. Debt collectors can file a lawsuit when legally permitted within the statute of limitations. If they win a judgment, they may be able to garnish wages, levy bank accounts, or place liens on property depending on state law. The risk of lawsuit increases when the debt is large, recent, and within the statute of limitations. Ignoring collection notices rather than responding increases the risk of a default judgment , which the collector wins without a hearing.

What happens if I ignore a debt collector?

Ignoring a collector does not eliminate the debt. The collection account remains on the credit report for seven years. The risk of a lawsuit increases the longer the account remains open. If the collector files a lawsuit and you do not respond, the court may enter a default judgment in the collector's favor , without reviewing the merits of the debt. A default judgment can result in wage garnishment, bank levies, or property liens depending on state law. Responding to collection contact , even just to request validation , preserves your options.

- Debt collection agencies either work for original creditors (third-party collectors) or aquire debt portfolios outright (debt buyers)

- Debt buyers often purchase delinquint accounts for one to ten cents per dollar , creating setlement room that benefits both sides

- The FDCPA sets federal rules on when, how, and how often collectors can contact consumers

- Requesting debt validation in writing stops collection activity until the collector provides documentation

- Collection accounts stay on credit reports for seven years from the original delinquency date , payment does not remove them

- Getting the calls to stop and fixing the credit report damage are two seperate problems requiring two seperate strategies

- Nearly 400,000 CFPB complaints about debt collection were filed in 2025 , CFPB complaint is a formal escalation option for consumers facing violations

Joe Mahlow's team at ASAP Credit Repair reviews all three bureau reports for collection accounts , checking the original delinquency date, the reported balance, the validation status, and the reporting accuracy on each account across all three bureaus. The review identifies what can be disputed, what can be negotiated, and what the realistic credit repair timeline looks like. Free, no obligation.

Get My Free Credit Review → CROA Registered | 20 Years in Business | Free, No Obligation-

Debt Validation: When Collectors Must Prove the Debt Is Yours Step two after understanding what a debt collection agency is: knowing how to use debt validation to stop collection activity and force documentation of the debt. This covers exactly what collectors must provide, what to do when they can't, how to write the validation request letter, and what FDCPA rights apply when a collector refuses or provides incomplete documentation.

-

Can a Debt Collection Agency Charge Interest? What the Law Says A collection balance that grew significantly after the original charge-off may or may not be legal. This covers the three sources that give collectors the right to add interest, how to verify whether the interest was calculated correctly, and where most balance disputes actually succeed , not in whether interest was added, but in whether the rate and start date match the original contract.

-

How to Dispute Identity Theft Collections Some collection accounts that consumers don't recognize are not just unfamiliar debt buyers , they may be the result of identity theft. This covers how to identify fraudulent collection accounts, file an FTC Identity Theft Report, and use FCRA blocking rights to remove collections that were opened by a thief, not by you.