TL;DR: Dispute identity theft accounts and stop collection activity by proving the debt is fraudulent and requesting removal. You have rights under the Fair Credit Reporting Act (FCRA) and Fair Debt Collection Practices Act (FDCPA) to dispute the account and request removal. The fastest path is to create an FTC Identity Theft Report. You can also dispute the account with all three credit bureaus, notify the collection agency in writing, and maintain documentation proving the debt does not belong to you.

Identity theft collections are among the most frustrating credit report problems because the debt often belongs to someone else entirely.

According to the Federal Trade Commission (FTC), identity theft consistently ranks among the most reported consumer fraud categories in the United States. Generating hundreds of thousands of complaints annually. Many victims do not discover the problem until they apply for credit, review a credit report, or receive a collection notice for an account they never opened.

At ASAP Credit Repair, one of the most common identity theft scenarios involves consumers discovering a collection account months or years after the fraudulent account was opened. In many cases, the collector assumes the debt is valid because it is attached to the victim's personal information.

The good news is that federal law provides a dispute process specifically designed for identity theft victims.

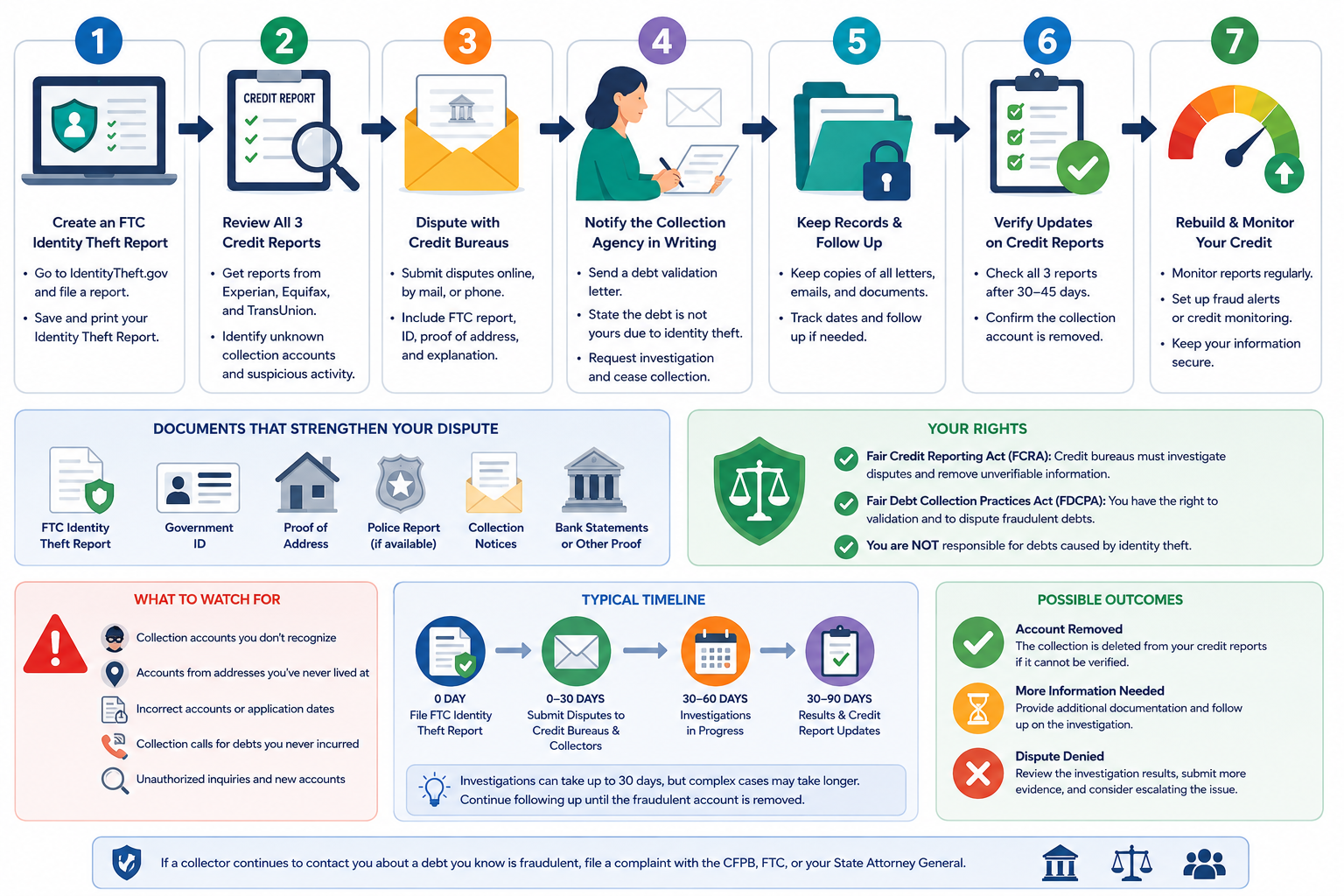

How to Dispute Identity Theft Collections

The dispute process involves four critical steps:

Create an FTC Identity Theft Report

Review All Three Credit Reports

Dispute With Credit Bureaus

Notify the Collection Agency

The Four-Step Dispute Process , In Order

Order matters here. Each step creates evidence for the next one. Do not skip to step three without completing step one first.

Go to IdentityTheft.gov and complete the identity theft report. It takes 15 to 20 minutes. The FTC creates a personalized recovery plan and generates pre-filled dispute letters you can send to bureaus and collectors. This report is your most important document , it activates specific FCRA protections that do not apply to standard disputes.

Contact any one of the three bureaus , Experian, Equifax, or TransUnion , and request a fraud alert. That bureau is required to notify the other two automatically. An initial fraud alert runs for one year. As a verified identity theft victim with an FTC report, you qualify for an extended fraud alert that runs seven years. Fraud alerts require lenders to contact you and verify your identity before opening new accounts in your name , protecting you while disputes are in process.

Submit written disputes to Equifax, Experian, and TransUnion as three separate submissions , the same fraudulent collection may appear differently on each. In each dispute, include your FTC Identity Theft Report, a copy of your government-issued ID, proof of your current address, and a written statement that the collection account resulted from identity theft and was not opened by you.

You can file disputes online through each bureau's dispute portal or by certified mail. Online disputes are generally faster. Certified mail creates a trackable paper record that helps if the dispute needs to be escalated later.

Under the FDCPA, you have the right to request that a collector validate the debt , meaning they must provide documentation proving the debt is yours. For identity theft accounts, this is often where the case resolves. Debt buyers who purchased a portfolio containing your information frequently cannot produce the origional application. When they cannot validate, the collection must be removed.

Send your validation request in writing via certified mail. Include a copy of your FTC Identity Theft Report. State clearly that you are an identity theft victim and that you dispute the debt on that basis under both the FCRA and FDCPA.

Documents That Strengthen Your Identity Theft Dispute

A dispute saying "this is not my account" without documentation is weak. The same dispute with these documents shifts the burden to the collector to prove the debt is yours.

Real Example: Collection Account From Identity Theft

A consumer came to ASAP Credit Repair after discovering a $3,200 telecommunications collection account on all three bureau reports. The account had been opened in another state. The consumer had never lived there. The collection appeared six months before a scheduled mortgage application.

What they did: Filed an FTC Identity Theft Report at IdentityTheft.gov the same day. Gathered prior-year utility bills showing their home address during the period the fraudulent account was opened. Submitted disputes to all three bureaus with the FTC report, ID, and utility bills. Sent a debt validation request to the collector via certified mail.

What happened: The collector could not produce the origional application signed by the consumer. They also could not explain why an account was opened in a state where the consumer had no address history. All three bureaus removed the collection. The mortgage application proceeded without the collection in the file.

Key lesson: The dispute succeeded not because of the dispute letter itself , it succeeded because the documentation proved the consumer could not have opened the account where and when the identity thief did. Address history was the deciding factor.

Why First Disputes Sometimes Don't Work

Three main reasons identity theft disputes fail on the first round:

- No FTC report included. The most common reason. Without the FTC report, the dispute is treated as a standard account dispute , not an identity theft matter with separate legal protections.

- Incomplete documentation. A dispute missing the ID, address proof, or a clear written statement that the account was opened by fraud , not just "this isn't mine" , gives the collector a reason to verify without investigation.

- Only disputing with one bureau. A fraudulant collection may appear on all three reports. Removing it from one doesn't remove it from the others. Always dispute with all three separately.

As NerdWallet's credit dispute guide confirms, when filing a dispute related to identity theft, including a copy of your FTC complaint or police report gives the bureau and collector the documented evidence they need to investigate properly , rather than performing an automated confirmation of the account's existence.

Identity Theft Dispute vs Standard Credit Dispute

Used when: The account is yours but the information is reported incorrectly

Documents needed: Statements, payment records, the specific inaccurate field

Legal basis: FCRA general dispute rights

Collector's burden: Confirm the account information is accurate

Common result: Correction of specific errors (date, balance, status)

Used when: The account does not belong to you at all , opened by a thief

Documents needed: FTC Identity Theft Report, ID, address proof

Legal basis: FCRA identity theft blocking rights + FDCPA validation rights

Collector's burden: Prove the debt was created by the actual consumer

Common result: Account blocked and deleted when collector cannot prove ownership

What Identity Theft Victims Often Miss

Most victims find one fraudulent collection and focus entirely on that account. Identity theft rarely affects just one thing. By the time a collection appears, the thief may have created multiple problems across the report.

"The collection is what brought the consumer to us. But when we pull all three reports, there are usually two or three other things that didn't come up on their monitoring app. A fraudulant address from another state. An inquiry from a credit card application they never made. In some files, a second account that hasn't reached collections yet but is showing 30-day lates. Fixing the collection and leaving those on the report is like fixing a roof leak and ignoring the water damage inside. A complete three-bureau review is the first step every identity theft victim needs before they focus on any single account."

As Experian's identity theft reporting guide confirms, the FTC's recovery plan at IdentityTheft.gov generates a personalized checklist based on the specific type of theft , because criminals use stolen information for far more than just opening credit accounts, and each type of misuse requires a different response step.

Joe Mahlow's team pulls all three bureau reports and reviews every account, inquiry, address, and account status for signs of identity theft. The free review identifies all fraudulent items, not just the collection that brought you in.

Get a Free Three-Bureau Review →How Long Does the Identity Theft Dispute Process Take

| Action | Time to Complete | What It Produces |

|---|---|---|

| FTC Identity Theft Report | 15 to 20 minutes (same day) | Official case number, personalized recovery plan, pre-filled dispute letters |

| Fraud alert placement | Same day | All three bureaus notified; lenders must verify identity before new accounts |

| Bureau dispute investigation | 30 to 45 days from submission | Dispute result: deletion, correction, or verified response |

| Debt validation response | 30 to 60 days | Collector validates or cannot validate , cannot-validate = removal |

| Score update after deletion | 30 to 60 days after deletion confirmed | Score recalculates; improvement depends on rest of credit profile |

As Bankrate's identity theft and credit bureau guide confirms, placing a fraud alert with one national credit bureau automatically extends to the other two , making it a fast first protection step while the longer dispute investigation runs. An initial fraud alert runs one year and can be extended after that for verified identity theft victims.

Decision Framework , What to Do Based on Your Situation

Related Questions

Can debt collectors legally pursue identity theft victims?

Collectors can attempt to collect until they receive notice that the debt resulted from identity theft. Once you submit your FTC Identity Theft Report and dispute documentation, they are on notice. Under the FDCPA, they cannot use harassing tactics, and under the FCRA, they must investigate rather than simply re-verify the account's existence. A collector who continues reporting a known fraudulent account after receiving identity theft documentation may be in violation of federal law. Consult a consumer law attorney if this occurs.

What happens if the collector cannot validate the identity theft debt?

If a collection agency cannot provide documentation proving the debt belongs to you , specifically the origional application signed by the consumer , they must cease collection activity on that account. The bureaus must then remove or block the account during and after the investigation. Most debt buyers who purchased a portfolio containing fraudulent accounts cannot produce the original application. This is the most common reason identity theft collection disputes succeed: the collector bought the debt but cannot prove it's yours.

Should I contact the original creditor or only the collection agency?

Contact both. The original creditor may have records from the application , the address used, the device used to apply, the IP address , that confirm the account was not opened from your location. In some cases, the original creditor will conduct their own fraud investigation and send an update to the bureaus removing the account from both their records and the collection agency's record. This can resolve the dispute faster than a standard bureau investigation.

How does an identity theft dispute affect my credit score?

Filing the dispute does not hurt the score. The collection account is already damaging it. If the dispute is successful and the collection is removed, the score may improve , how much depends on the rest of the credit file, as discussed in the guide to why collection removal doesn't always produce a large score gain. If the dispute fails, the score stays the same as it was with the collection reporting.

- Filing an FTC Identity Theft Report at IdentityTheft.gov is the most important first step , it activates federal protections that don't apply to standard disputes

- Dispute with all three bureaus separately. A deletion from one does not delete from the others

- Send a debt validation request to the collector under the FDCPA , most debt buyers cannot prove the origional application belongs to the victim

- Place a fraud alert immediately. One bureau notifies the other two. Verified victims can place a 7-year extended alert

- Review all three reports for every sign of fraud, not just the collection you found first

- Disputes filed without the FTC report are treated as standard disputes , the legal framework that protects identity theft victims only activates when the FTC documentation is included

- Payment of a fraudulent collection does not eliminate your dispute rights. You are not legally responsible for identity theft debts

Joe Mahlow's team at ASAP Credit Repair reviews all three bureau reports for every indicator of identity theft , fraudulent collection accounts, unknown addresses, unauthorized inquiries, and accounts you didn't open. The review identifies all fraudulent items before the dispute process starts, so nothing is left behind. Free, no obligation.

Get My Free Credit Review → CROA Registered | 20 Years in Business | Free, No Obligation | Not Legal Advice-

Collection Removed But Score Didn't Increase? Here's Why After a successful identity theft dispute removes the fraudulent collection, the score may not jump as much as expected , especially if other credit issues exist in the file. This covers every reason a removed collection produces minimal score movement: high utilization, remaining late payments from the original account, charge-offs, and thin credit history. The guide everyone should read after winning an identity theft dispute to understand what to address next.

-

Why You're Not Seeing Credit Repair Results After 30 Days Identity theft disputes take 30 to 90 days from dispute submission to confirmed deletion. This covers the FCRA investigation timeline, why scores lag behind bureau file updates, and how to tell when the wait is normal versus when a dispute stalled and needs follow-up. The timing guide for anyone who filed an identity theft dispute and is wondering why nothing has changed yet.

-

Debt Validation: When Collectors Must Prove the Debt Is Yours Step 4 of the identity theft dispute process is sending a debt validation request to the collector under the FDCPA. This covers exactly what collectors are required to provide, what happens when they can't produce documentation, how debt validation works alongside FCRA disputes, and the specific language to include in the validation request letter. The essential companion guide for identity theft victims who are also dealing with collection calls.