Why are you not seeing credit repair results after 30 days of entering a program?

Usually, the answer has more to do with timing than effectiveness. Most credit bureaus have up to 30 days to investigate disputes, and creditors may need additional time to verify account information before changes appear on a credit report.

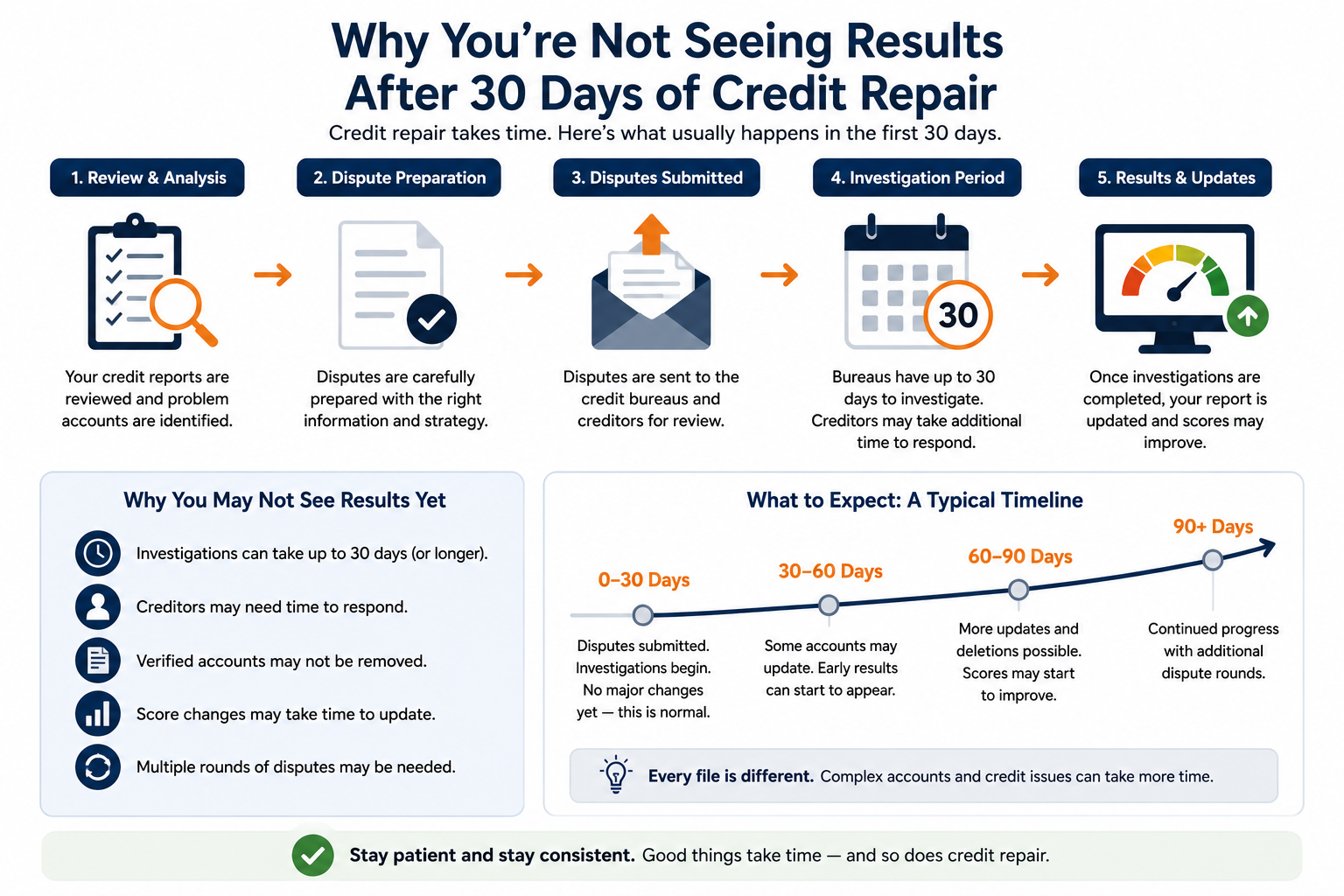

Many consumers expect collections, charge-offs, or reporting errors to disappear within the first month. However, the initial 30 days are often spent reviewing credit reports, preparing disputes, gathering documentation, and waiting for investigation results. Even when a dispute is successful, score changes may not appear immediately.

Being informed on what typically happens during the first month of credit repair can help set realistic expectations. This identify whether a delay is normal or a sign that additional action may be needed.

Why You're Not Seeing Credit Repair Results After 30 Days

Not seeing credit repair results after 30 days is often normal.

Credit bureaus generally have up to 30 days to investigate disputes. Then an additional time may be required for creditors to respond, updates to appear on reports, and credit scores to recalculate.

The first month is often focused on gathering documentation, submitting disputes, and initiating investigations rather than producing immediate score increases.

"Most clients who don't see results after 30 days is actually on schedule. I've been saying this for 20 years and it never stops being true. The first month is the begining of the process. Disputes get submited, bureau investigations open, creditors get contacted. None of that produces a score number that moves on day 29. What it produces is the foundation for what happens in month two and month three. The people who quit at 30 days are the ones who had no results and would have had significant results by day 60. Credit repair has a lag built into it by federal law. The 30-day investigation window is the minimum, not the finish line."

Is It Normal to See No Results After 30 Days

Yes. The most common reason: the 30-day bureau investigation window hasn't closed yet. The FCRA gives bureaus up to 30 days from the date they receive a dispute to complete their investigation. If disputes went out on day 5 of the program, the investigation is still running on day 35. Score movement happens after the investigation closes and after the next scoring cycle updates. Both of these steps take time beyond the dispute submission date.

Consumer expectations about credit repair speed are often shaped by the same frustration that drove the search for help in the first place. Years of damaged credit built up over many months. The expectation is that a professional service reverses it in less time than it took to create.

In reality, federal law builds a minimum 30-day investigation window into every dispute. That window runs from the bureau's receipt of the dispute, not the date the program started or the date a payment was made. A program that started on March 1, reviewed the report, and submitted disputes on March 8 won't close those investigations until April 7 at the earliest.

What Happens During the First 30 Days of Credit Repair

The first 30 days of credit repair involve: pulling all three bureau reports, reviewing every account for inaccuracies, identifying which items are disputable under FCRA and which require FDCPA validation requests, preparing dispute letters for each account and bureau separately, and submitting those disputes. The disputes then enter the bureau investigation period. Results from that period don't appear until 30 to 45 days after submission, which means the visible outcome of first-month work shows up in month two.

What happens in the first 30 days that consumers don't see:

- Three-bureau credit report review. Each of the three bureaus maintains a separate file. The same collection may appear with different dates or balances on each. Identifying these differences takes time before a letter goes out.

- Dispute strategy development. Not every item disputes the same way. An inaccurate late payment disputes differently from an unverifiable debt buyer collection. A collection with a wrong original delinquency date requires a different approach than a duplicate entry. This analysis determines which type of challenge letter fits each specific account.

- Dispute letter preparation. Each letter names the specific account, the specific inaccuracy, and the specific bureau receiving the dispute. For a file with eight items across three bureaus, that may mean 18 to 24 separate dispute documents prepared before a single one gets sent.

- FDCPA debt validation requests. Collection accounts require separate validation letters sent directly to the collector via certified mail, in addition to FCRA bureau disputes. These run parallel processes with different timelines and different response requirements.

- Submission and tracking. Disputes go out. Investigation windows open. The waiting begins. This stage produces no visible score change , but everything that produces a score change depends on it happening correctly.

7 Reasons You May Not See Results Yet

The FCRA gives bureaus 30 days to investigate. That window extends to 35 days when the consumer provides additional information during the investigation. If the program submited disputes in the first two weeks, the investigation window may still be running at day 30. No results appear until investigations close. Investigations close on their own timeline, not on the consumer's preferred schedule.

When a bureau receives a dispute, it contacts the creditor or debt buyer that reported the item. The creditor has its own response window within the bureau's 30-day period. Creditors who receive high volumes of dispute requests sometimes use the full 30 days before responding. The bureau investigation doesn't close until the creditor responds or the window expires.

Some items return "verified" after the first dispute cycle. This means the creditor confirmed the information to the bureau. A verification is not the end of the process. It's the begining of a second approach. A different dispute strategy, additional documentation, or a follow-up challenge with new information sometimes produces deletion on round two when round one produced verification. One cycle of disputes is rarely the complete process.

Credit scores don't update in real time. Even after a bureau closes an investigation and removes or updates an account, the score recalculates only at the next scoring cycle. Lenders who pull a score between two scoring cycles see the old score. The new score showing the deleted item won't appear until the next time a score is generated from the updated bureau file.

Files with multiple negative items across three bureaus require multiple dispute cycles. The first cycle addresses the highest-priority items. Results from cycle one inform the strategy for cycle two. Cycle two addresses items that survived the first round plus any new information that emerged from the investigation responses. This sequential process takes 3 to 6 months to run through a complex file fully.

Some files have 3 negative items. Others have 15, spread across multiple debt buyers, reporting different balances on different bureaus, with different original creditor information. The lenght of the process scales with complexity. A file that takes 3 months for a simple profile may take 12 months for a profile with identity theft, mixed file issues, and collections from 7 different buyers.

Credit damage that built up over 2 to 5 years doesn't reverse in 30 days. Each negative item has its own dispute cycle, investigation window, and potential follow-up round. The more items in the file, the longer the timeline. A realistic expectation for most consumers is 60 to 90 days for first visible results and 3 to 6 months for meaningful score improvement.

What Joe Mahlow and ASAP See During the First Month

"At ASAP Credit Repair, the most common call we get around day 28 to 35 is a client asking why nothing has changed. We pull up their file and show them: 14 disputes submited, 3 bureau investigation windows still open, 2 validation requests sent to collectors awaiting response. Everything is running exactly on schedule. The client's frustration is completely understandable. They're paying for a service and seeing nothing visible yet. What I tell them: credit repair has a built-in delay that federal law created. The 30-day investigation window isn't a failure. It's the process working the way Congress designed it to work. Month two is when the letters start coming back."

Patterns from reviewing ASAP client files at the 30-day mark:

- Most common situation at day 30: investigations still open. The majority of ASAP clients at the one-month mark have at least one bureau investigation still within the 30-day window. Nothing changes until those windows close and responses arrive.

- Second most common: first results already arrived but score hasn't updated. The bureau closed an investigation and deleted an item. The creditor updated its reporting. The consumer pulled their score from a credit monitoring app and it still shows the old number. The app often uses a cached score, not a real-time pull. The actual lender-pulled score would show the improvement.

- Third most common: dispute verified on first round. One or two items returned "verified" , the creditor confirmed the information to the bureau. These are not lost causes. Second-round disputes with different approaches, additional documentation, or FDCPA validation requests change outcomes that first-round verifications didn't.

A free credit report review from ASAP Credit Repair shows exactly where disputes stand across all three bureaus , which investigations are open, which returned results, and what the next round of challenges should address. Understanding the investigation cycle gives a clearer picture of actual progress versus a stalled process.

See Where My Disputes Stand →When Should You Expect to See Credit Repair Results

As Money's 2026 credit repair guide confirms, consumers may see a score increase around one to three months after disputed errors are removed , not at the moment disputes are submitted. The gap between submission and visible score change is built into the system by the FCRA investigation timeline and the scoring cycle update lag.

The detailed breakdown of what to expect at each stage and how to read dispute results is covered in the credit score improvement timeline guide, which includes the specific point estimates for different starting scores and file types.

Signs Credit Repair Is Actually Working

- Investigation results letters are arriving from Equifax, Experian, or TransUnion

- Some accounts show "deleted" or "updated" on bureau notifications

- The company can show documentation of each dispute letter sent and the specific accounts targeted

- Validation responses from collectors are arriving (even if they respond with documentation, this shows the process is running)

- The credit report shows fewer negative items in month 2 than in month 1

- Score begins moving at the 45 to 60 day mark as first-cycle results compound

- No communication at all after 30 days , no investigation results, no updates, no contact from the company

- Company cannot show documentation of dispute letters sent for specific accounts

- No investigation response letters from any bureau after 45 days

- Score continues dropping without explanation , new collections or new late payments may be appearing

- The company promises score guarantees or claims to remove accurate information

- Requests to pay the full program fee before any services are delivered

When Should You Be Concerned

Concern is warranted when three or more months pass with no investigation results from any bureau, when the company cannot produce documentation of letters sent for specific accounts, when no communication comes from the company between monthly fees, or when the credit score continues to fall without new collections or late payments explaining the drop. Normal credit repair produces bureau investigation results within 30 to 45 days of each dispute cycle. Two complete cycles without any results document warrants a direct request for dispute documentation.

As Bankrate's credit dispute guide confirms, bureaus generally have 30 days to investigate after receiving a dispute and 5 days to notify the consumer of results. If no notification arrives within 45 days of a dispute being submitted, that specific dispute warrants follow-up.

And as NerdWallet's credit repair services guide confirms, credit bureaus are not required to investigate disputes they deem "frivolous" , so the specific language and documentation in a dispute letter affects whether the bureau opens a full investigation. Generic or template-only letters may receive this classification more often than targeted, documented disputes.

How Long Does Credit Repair Really Take

| File Type | Expected Timeline | Key Variables |

|---|---|---|

| 1-2 items, simple inaccuracies | 30 to 90 days for results | Single dispute cycle often sufficient. Fast files. |

| 3-6 items, mixed types | 60 to 120 days | Multiple cycles needed. Results compound across rounds. |

| 7+ items, multiple bureaus | 3 to 6 months | Full program required. Each cycle addresses priority items. |

| Identity theft involved | 6 to 12 months | FTC affidavits, fraud alerts, credit freezes add steps and time. |

| Mixed credit files | 6 to 18 months | Bureau file correction is slow. May require escalation to achieve resolution. |

| Significant rebuilding needed | 12 to 36 months | Disputes plus positive history building. Timeline reflects full recovery, not just dispute completion. |

The full breakdown of how the credit repair process works at each stage covers what happens inside each dispute cycle, how bureau investigation windows work, and how follow-up strategies differ from first-round approaches when items return verified.

Why are my disputes still pending after 30 days?

Disputes remain in investigation status for up to 30 days from the date the bureau receives them, not from the date the program started or the payment was made. If disputes were submitted on day 8 of the program, the investigation window runs until approximately day 38. The bureau may also extend the window to 35 days when the consumer provides additional documentation during the investigation. Pending status means the investigation is running , not that it failed. Results arrive when the investigation closes, not when it opens.

Why was my dispute verified if the information was wrong?

Creditors sometimes verify disputed information even when the dispute has merit. The verification means the creditor confirmed the information to the bureau , not that the information is provably accurate. A second dispute with additional documentation, a different approach (FDCPA validation request instead of FCRA bureau dispute), or a direct challenge to the creditor based on the documentation they provided during verification can change the outcome. One verification on the first round is not a final answer. It is a signal about which strategy to try next.

Can credit repair take 90 days or longer?

Yes , and for most files with multiple negative items, 90 days is the point where meaningful progress becomes clearly visible, not where the process ends. Two complete dispute cycles take 60 to 90 days. Some items resolve in cycle one. Others require cycle two. Complex files with many accounts, identity theft damage, or items spread across all three bureaus under different reporting names often require 6 to 12 months of consistent dispute work before the score reaches its improvement potential.

-

Is It Worth Paying Someone to Fix My Credit? Honest Cost vs Results The frustration behind "why aren't I seeing results?" often connects to a deeper question: was this money well spent? This covers the honest answer from Joe Mahlow as a credit repair company owner, including when professional credit repair produces clear ROI and when it doesn't. The cost-vs-results calculation helps frame whether the absence of 30-day results means the process is working on schedule or whether the wrong service tier was chosen for the specific file type.

-

How Long Does It Take to Raise a Credit Score? Realistic Timelines The specific point estimates and month-by-month timeline for each action type , utilization reduction (30 days), dispute wins (30-90 days), collection deletions (3-12 months), full rebuilding (12-36 months). This gives context for measuring whether the 30-day experience is on schedule or behind. The bar chart comparing points-gained-per-action shows exactly why the timeline for each action type differs and what the realistic cumulative improvement looks like at each stage of a credit repair program.

-

Does Credit Repair Always Involve Lawyers? What Consumers Should Know When a credit repair program stalls , items verified repeatedly, bureaus ignoring follow-ups, or a debt buyer continuing to report after failed validation , the next question is whether legal intervention changes the outcome. This covers exactly when attorney involvement adds value the standard dispute process cannot: FCRA violations, repeated re-insertion of deleted items, FDCPA violations, and civil lawsuits. Understanding the line between a normal dispute process and a situation requiring legal escalation is the tool for navigating a stalled program.