A 522 credit score feels frustrating because most people know they need a higher score. What they do not know is how long the process actually takes.

I have seen people go from the low 500s to the mid-600s in less than a year. I have also seen people stay stuck for years because they focused on the wrong things.

The truth is that a 522 credit score does not improve on a fixed timeline.

The answer depends on what caused the score to drop in the first place.

A maxed-out credit card can often be fixed much faster than a collection account, charge-off, repossession, or bankruptcy.

Before worrying about how many points you need. It helps to understand which problems are holding the score down and which ones can realistically be improved over the next few months.

How Long Does It Take to Increase a 522 Credit Score?

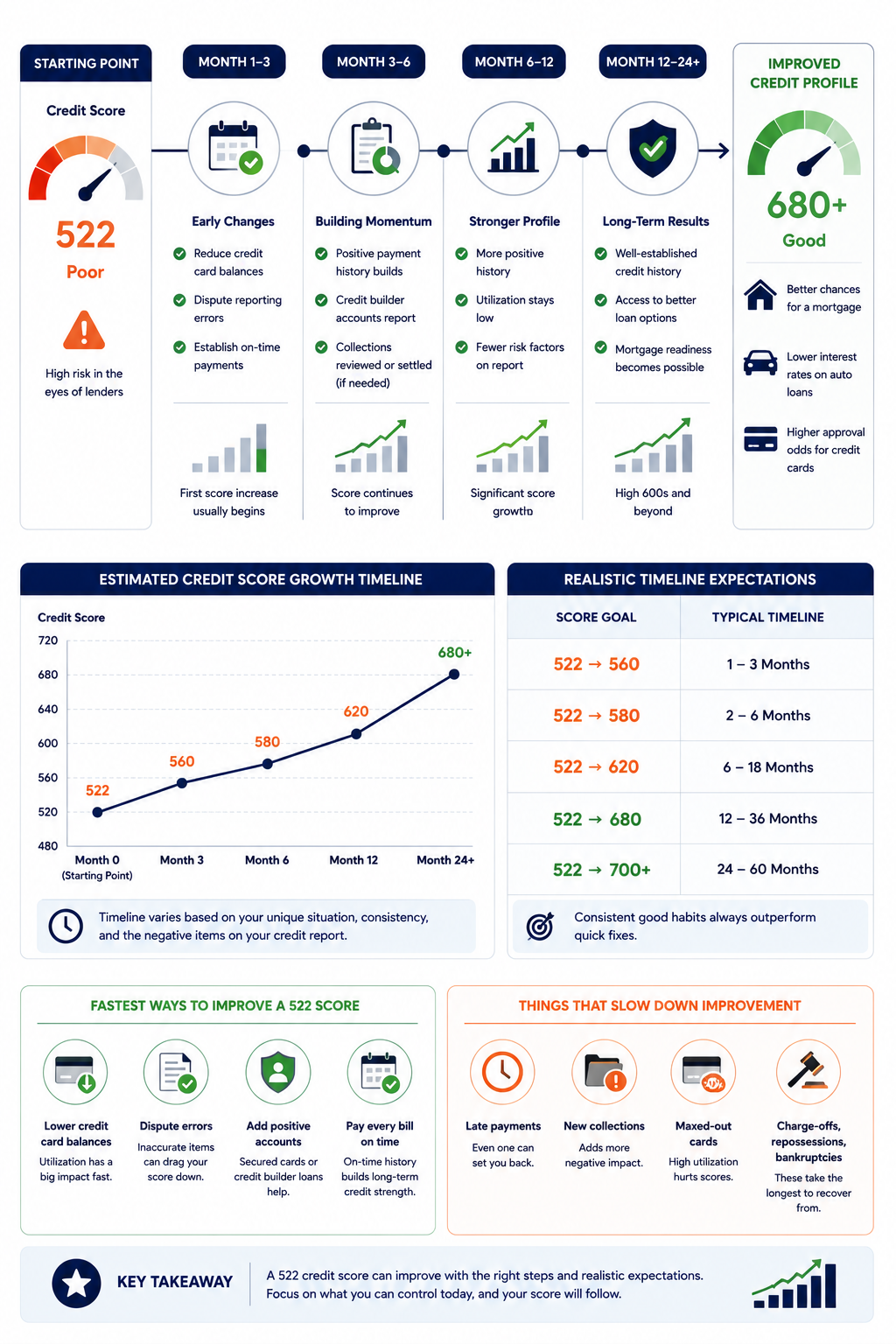

Most people can see noticeable improvement from a 522 credit score within 30 to 180 days. This is if they reduce credit card balances, correct reporting errors, and establish positive payment history.

Larger improvements often take 6 to 24 months depending on collections, charge-offs, repossessions, or bankruptcies appearing on the credit report.

522 Credit Score Recovery Timeline

A 522 credit score can improve faster than most people expect, but the timeline depends on what is holding the score down.

The chart below shows realistic improvement ranges based on common credit problems and consistent rebuilding habits.

How Long Does It Take to Increase a 522 Credit Score

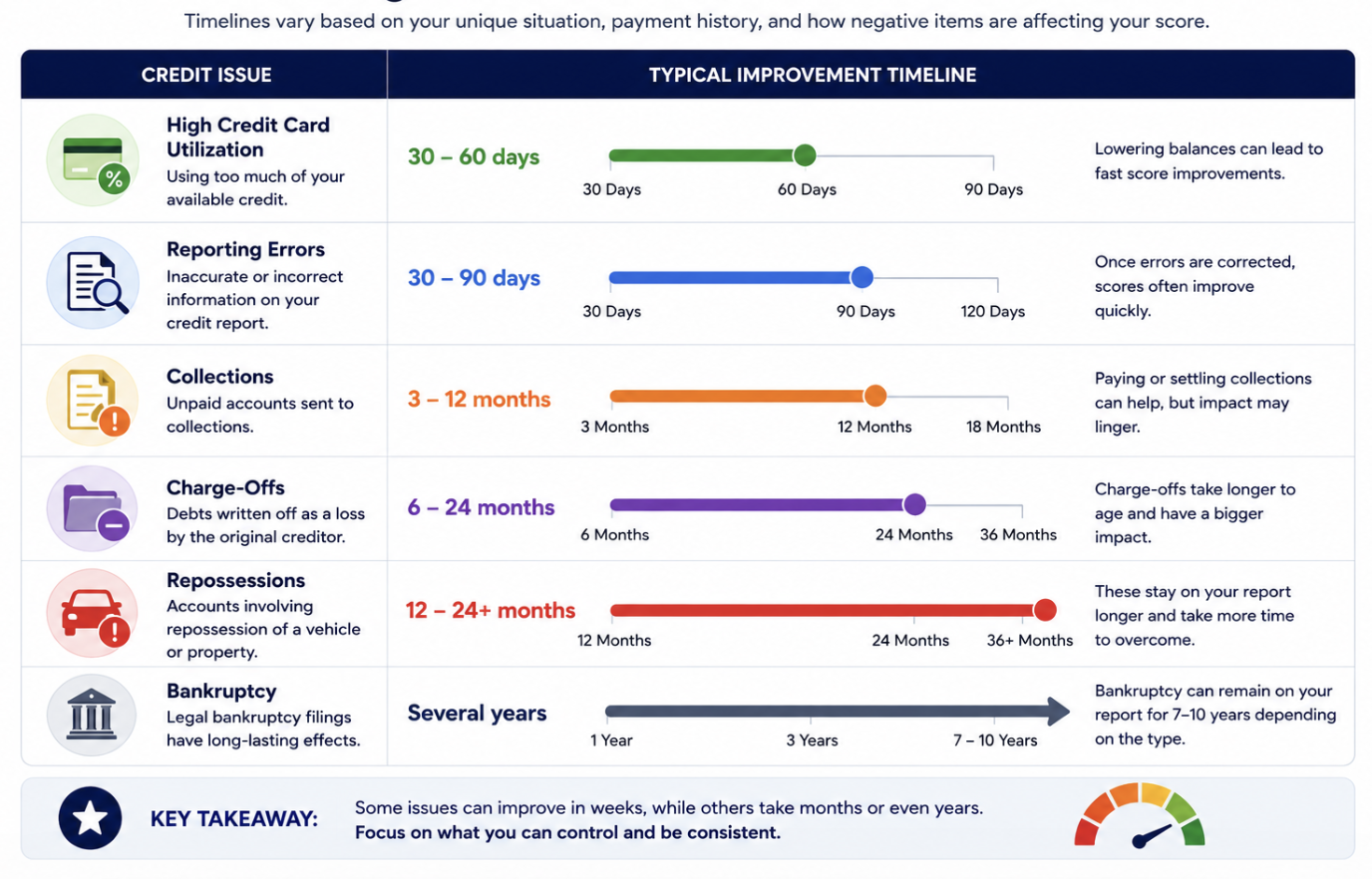

There is no single answer. A 522 caused by high utilization alone can improve in 30 days. A 522 caused by multiple collections, a charge-off, and a thin credit history may take 18 to 24 months to meaningfully recover. The issue type determines the timeline. The table below shows what you can realistically expect from each.

| Credit Issue | Score Impact | Typical Timeline to Fix |

|---|---|---|

| High credit card utilization | -50 to -100+ points | 30 to 60 days after paying down |

| Inaccurate reporting errors | -10 to -80 points per error | 30 to 90 days per dispute cycle |

| Collection accounts | -40 to -100 points | 3 to 12 months to dispute and remove |

| Charge-offs | -60 to -120 points | 6 to 24 months |

| Repossession | -75 to -130 points | 12 to 24 months or more |

| Bankruptcy | -100 to -200 points | Several years |

Most 522-score files have more than one issue.

The average person at this level has high utilization, one or two collections, and limited positive history. That combination means the fix is not one thing. It is several things done in the right order.

Fix utilization first. It moves fastest and costs nothing. Then dispute collections. Then build positive history with secured accounts or credit builders. The sequence matters as much as the actions themselves.

What Each Action Does to Your Score , Points and Timeline

Why Some 522 Credit Scores Improve Faster Than Others

Two people can both sit at 522. One may need 60 days to recover. The other may need 2 years. The score does not tell you why it is there. A 522 from high utilization alone is an easy fix. A 522 from three collections, a charge-off, and zero positive accounts takes much longer. The path forward depends on the cause, not the number.

Here is how to think about it.

Scenario A: No collections. No late payments. Just credit cards maxed out. Score is 522 because utilization is 93%. Pay the cards down. Score jumps 60-90 points in one billing cycle. This person is at 600+ within 60 days.

Scenario B: Two collections. A charge-off. Thin credit history. No cards with available balance. Score is 522 because three separate negative events are dragging it. This person cannot fix it in 60 days. Each issue requires its own process. The collections take 3-12 months to dispute. The charge-off takes 6-24 months. Positive history takes time to build. This person may be 18 months away from 620.

Same score. Completely different situations.

The Fastest Ways to Increase a 522 Credit Score

The fastest moves are utilization reduction, disputing reporting errors, and adding an authorized user. All three can produce visible results within 30 to 60 days. None require opening new credit lines. None generate hard inquiries. They work immediately because they address the FICO factors that update every billing cycle.

- Pay credit card balances below 10% utilization. The average 522-score consumer carries 93.8% utilization (Experian). This is often the entire explanation for the low score. Paying cards down is the single biggest lever available. Even getting to 30% helps. Under 10% produces the maximum scoring benefit. Do it before the statement closes , that is when the balance reports to the bureaus.

- Dispute inaccurate items on the credit report. Pull all three bureau reports at AnnualCreditReport.com. Look for wrong dates, wrong balances, accounts that do not belong to you, late payments that did not happen, and collection accounts where you were never notified. One removed error can add 20 to 80 points depending on what it was.

- Get added as an authorized user. Ask a family member or trusted person with a long credit history, perfect payment record, and low utilization to add you as an authorized user on one of their older credit cards. Their account history posts to your file. Scores improve in 30 to 60 days. The account does not have to be used , it just needs to be reported.

- Open a secured credit card. A secured card with $200-$500 deposit gives you a revolving account that reports to all three bureaus. Use it for small purchases. Pay it in full every month before the statement closes. The combination of low utilization and perfect payment history compounds over 6 to 12 months.

- Add a credit builder installment account. Kikoff ($5/month) or Kovo ($10/month) add installment tradelines to Equifax and Experian without a hard inquiry or deposit. Installment history plus revolving history builds credit mix. Both factors contribute to score improvement over 3 to 12 months.

As Experian's 522 credit score data confirms, consumers at this score level carry an average 93.8% utilization , making balance paydown the highest-impact action available before any dispute or new account strategy.

Real Example: Going From 522 to 600

This is based on a real client profile from ASAP Credit Repair.

Starting situation: Score of 522. Three collections (two recent, one older). Credit card utilization at 88%. No new late payments in 14 months. No positive open accounts except one old credit card never used.

What actually drove the improvement was the sequence.

Month 1 was entirely utilization. One action. Cards paid down. Score jumped 36 points. No disputes. No new accounts. Just the utilization fix.

Months 2 and 3 were slow. Adding the secured card and credit builder created new positive tradelines, but those take time to build weight. The score moved modestly.

Month 4 was the second jump. One collection account deleted after a successful FCRA dispute. That removed a negative anchor that was holding the score down. Scores moved 17 points in one month without any payment to that collector.

The lesson: disputing and deleting beats paying and keeping on the report. Every time.

Why Some 522 Scores Improve Faster

| Goal | Realistic Timeline | Main Requirements |

|---|---|---|

| 522 to 560 | 1 to 3 months | Utilization reduction alone |

| 522 to 580 | 2 to 6 months | Utilization fix + secured card or credit builder |

| 522 to 620 | 6 to 18 months | Utilization + at least one collection deleted + 6+ months positive payment history |

| 522 to 680 | 12 to 36 months | All of the above + multiple collections resolved + consistent two-year payment record |

| 522 to 700+ | 24 to 60 months | Full negative item resolution + long positive history + low ongoing utilization |

What Slows Credit Score Growth

The actions that help are obvious. The things that stop progress are less talked about.

- One new late payment. A single new 30-day late payment at 522 can drop the score another 40-80 points. It resets the most important FICO factor. It extends the recovery timeline by 12-24 months. This is the most common reason people stay stuck.

- Paying collections instead of disputing them. Payment updates the status. The entry stays. The damage stays. Disputing and deleting removes the entry entirely. Most people at 522 with collections focus on paying instead of disputing and lose months of potential progress.

- Ignoring utilization while working on other things. Spending months disputing collections while credit card balances stay at 90%+ means the FICO model never sees the score benefit of the dispute wins. Fix utilization first. Then dispute. Both together compounds the gain.

- Opening too many new accounts at once. Every new application produces a hard inquiry. Hard inquiries are minor , 5 to 10 points each , but five new applications in a month at 522 is 25-50 points of damage on top of an already low score.

- Closing old accounts. An old account with a zero balance contributes to account age (15% of FICO) and available credit (part of utilization calculation). Closing it removes that contribution. At 522 with a thin file, every positive account matters.

Can You Reach 700 From a 522 Credit Score

Yes. But not quickly. Going from 522 to 700 takes most people 24 to 60 months. It requires fully resolving major negatives, building 2 to 3 years of clean payment history, maintaining low utilization consistently, and adding positive account types. The people who get there fastest are the ones who delete negatives rather than just pay them, and who start building positive accounts in month one instead of waiting until the disputes are done.

The jump from 522 to 620 is realistic in under 18 months for most people.

The jump from 620 to 700 is where it slows down significantly. There is less low-hanging fruit at 620. Utilization is already under control. Collections got resolved. What remains is time , building account age, building a longer payment history record, and keeping the file clean while older negatives gradually lose scoring weight.

As myFICO's score improvement guide confirms, rebuilding credit after significant negative items requires patience , the biggest improvements come from consistent behavior over 12 to 24 months, not from a single action or shortcut.

The path to 700 is: 522 → 580 (utilization fix, 2-6 months) → 620 (collection deleted, 6-18 months) → 660 (clean history building, 12-24 months) → 700 (all negatives resolved or aged, 24-48 months). Each step is real. Each step takes work.

The 522-to-620 Mortgage Timeline

FHA loans require 580 for 3.5% down. Conventional loans typically require 620. Going from 522 to 580 takes most borrowers 2 to 6 months with utilization fixes and clean payment behavior. Going from 522 to 620 usually takes 6 to 18 months and requires resolving at least one collection account. Starting the process 12 to 18 months before the planned application date gives the most flexibility.

- Target: FHA at 580. Pay down credit cards. Dispute any reporting errors. Add a secured card or credit builder for positive history. Avoid new late payments. Most borrowers can reach 580 in 2 to 6 months with these actions alone.

- Target: conventional at 620. Everything above plus at least one collection or charge-off deleted from the report. The dispute process for collections takes 3 to 12 months. Start disputing while also fixing utilization.

- Lender overlays matter. Some FHA lenders require collections to be resolved before closing regardless of the guideline minimum score. Know what your target lender requires before assuming 580 is enough.

- Start 12-18 months before you plan to apply. This is not a last-minute fix. Underwriters see everything. Starting the repair process early gives dispute outcomes time to post, positive history time to build, and your score time to stabilize.

Understanding exactly what each score milestone opens in the real world , what loan programs, what rates, what approval chances , is covered in detail in the guide on what each credit score range means for your financial access. Knowing the target makes every step toward it more purposeful.

The Biggest Mistake People Make With a 522 Score

Most people obsess over gaining points. The better question is: what is causing the score to stay at 522? Fixing the root cause moves the score faster than chasing any list of tips. A 522 from utilization fixes in weeks. A 522 from collections takes months. A 522 from a charge-off takes longer. The score is the symptom. The cause is what needs the attention.

I see this every day.

Someone comes in with a 522. They spent months trying to improve it. They opened a new secured card. They paid off a collection. They kept their utilization under 50%. Score barely moved.

Then we pull the full report. There is a charge-off from 2022 reporting with a recent update date , re-aging. There is a collection that reports under two different names for the same debt , disputable. There is an account showing late payments that the client never had , a reporting error.

None of those get fixed by opening a new secured card.

They get fixed by reading the full report, identifying every specific inaccuracy, and disputing each one with documentation. That is different work from what most people are doing.

The full lineup of credit building accounts , secured cards, installment builders, authorized user strategies , is covered in the guide to credit building cards and accounts. But adding positive accounts works best when the negatives have already been addressed. Do not build on a broken foundation.

As NerdWallet's credit score improvement guide explains, the most impactful credit score actions address the largest factors first , payment history and utilization together account for 65% of the FICO score. Everything else is incremental by comparison.

How long does it take to increase a 522 credit score?

It depends on the cause. High utilization alone can be fixed in 30 to 60 days. Reporting errors resolve in 30 to 90 days. Collections take 3 to 12 months to dispute and remove. Charge-offs take 6 to 24 months. Most people going from 522 to 580 can get there in 2 to 6 months. Most people going from 522 to 620 take 6 to 18 months. Going from 522 to 700 takes 24 to 60 months. The key is identifying the specific cause before deciding on the strategy.

Is a 522 credit score bad?

FICO classifies scores from 300 to 579 as "Poor." A 522 falls in that range. It means most mainstream lenders will decline applications or approve with high interest rates. FHA mortgage minimums start at 580, and some lenders will not approve under 620. Most credit cards require 580 or higher. The score is improvable , and for most people at 522, meaningful improvement is achievable within 6 to 18 months with focused action. The score is not permanent.

What is the fastest way to raise a 522 credit score?

Pay down credit card balances to under 10% of their limits. The average person with a 522 score has 93.8% utilization. Dropping that to under 10% can add 50 to 100 points in a single billing cycle , 30 to 60 days. No disputes needed. No new accounts needed. Just the balance reduction. If there is no credit card debt and the score is 522 for other reasons, the fastest path shifts to disputing inaccurate items on the credit report, which takes 30 to 90 days per dispute cycle.

Does paying a collection raise a 522 credit score?

Not significantly on its own. Paying a collection changes the account status from unpaid to paid. The derogatory entry stays on the report for seven years from the original delinquency date. The score impact of a paid collection is minimal compared to having it deleted. Dispute the collection first. If the dispute succeeds and the entry is deleted, that removes the negative entirely , which produces a 30 to 80 point gain. Paying without deletion produces far less improvement.

-

Credit Score Ranges , What Is Good and What Each Tier Opens Going from 522 is purposeful when you know what each milestone actually opens. This covers the real-world difference between 580, 620, 660, and 700 , which loan programs become available, what interest rate tiers change, and what approval doors open at each threshold. Knowing the destination makes the timeline more motivating.

-

Good Credit Building Credit Cards and Accounts The credit building accounts that work best while repairing from 522 , Kikoff for revolving history, Kovo for installment history, secured cards for spending power. This covers the full lineup with affiliate links, best-for descriptions, and how to stack accounts for maximum FICO factor coverage without hard inquiries or deposits beyond what each product requires.

-

How to Remove Portfolio Recovery Associates From Your Credit Report Many 522 scores include at least one collection from a major debt buyer. Portfolio Recovery Associates is the largest. This covers the dispute process, validation strategy, settlement vs dispute decision, and the FDCPA rights that apply when PRA cannot produce complete documentation. The same framework applies to any collection account holding the score below its potential.