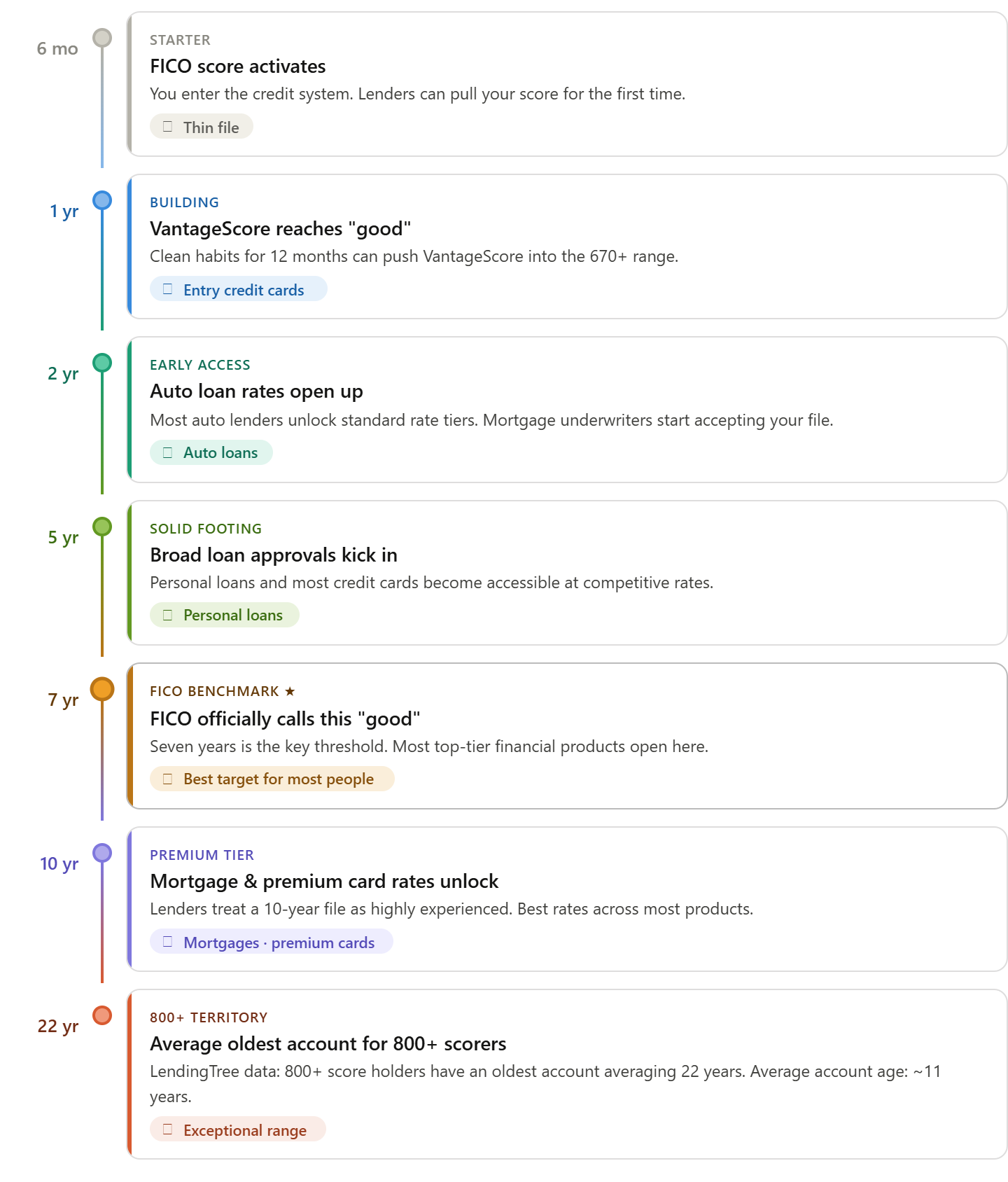

What is a good length of credit history? Seven years is the benchmark. FICO marks 7 years as "good." VantageScore sets "excellent" at over 9 years. Most top lenders reward borrowers most between 7 and 10 years.

Running a credit repair company, I see this weekly. One of the most unforgettable cases I handled was a client with a 740 score. He kept getting rejected for prime mortgage rates. His score looked strong. But his average account age was just 3.2 years. Lenders saw a short file and priced in the risk.

A Reddit thread in r/personalfinance (link) sparked a real debate on this. Dozens of users had scores in the 700s but still faced loan penalties. The common thread? Short credit histories, most under 5 years. One user with an 818 FICO shared that his average account age was 6 years and 4 months. LendingTree studied 100,000 users with 800+ scores. Their oldest accounts averaged nearly 22 years.

What Is a Good Length of Credit History: The FICO Definition

A good length of credit history is not just one number. FICO breaks it into three parts:

Age of your oldest account

Age of your newest account

Average age of all open accounts

All three show up on your credit report. FICO uses them to predict one thing: will you miss a payment by 90 days or more in the next 24 months? A longer track record gives lenders more data. More data means more confidence.

Length of credit history makes up 15% of your FICO score. VantageScore bundles it with credit mix under "depth of credit." That covers about 20% of your score. Either way, this factor has real weight. On a 700 score, 15% equals over 100 points.

How to Calculate Credit Age

Credit age is simple to figure out. Add up the age in months of every open account. Then divide by the number of accounts.

Here is an example:

Credit card opened 5 years ago (60 months)

Auto loan opened 3 years ago (36 months)

Student loan opened 1 year ago (12 months)

Total: 108 months. Divide by 3 accounts. That gives 36 months, or 3 years average age.

Opening a new account drops this average right away. Closing an old one can also shrink it. A closed account stays on your report for up to 10 years. But once it drops off, your average age shrinks. Check your free credit report at AnnualCreditReport.com to see every account age in one place.

Good Credit Score but Short History: Why the Gap Exists

You can have a good credit score with a short history. But your score will hit ceilings. FICO needs at least 6 months of credit use on one account before it creates a score. VantageScore is faster. It can generate a score after just one month.

Here is what a good length of credit history looks like across each range:

Less than 2 years: Thin file. Most lenders call this "limited history." Mortgage and premium card approvals drop.

2 to 5 years: Fair. Scores of 680–720 are possible with good habits. But lenders often add risk fees.

5 to 7 years: Good. Auto loans and personal loans become easier to get at fair rates.

7 to 10 years: Very good. FICO sees this range as strong for most products.

10+ years: Excellent. Borrowers here get the best rates from most lenders.

People with 800+ scores have the oldest accounts that average 22 to 30 years. Their average account age sits around 11 years, per FICO and LendingTree data.

Payment history (35%) and credit use (30%) add up to 65% of your FICO score. A borrower can score well on both and still cap out. Length of credit history (15%) and credit mix (10%) hold them back. Last year, our office handled over 40 cases where clients had strong scores but thin files. Every single one had an average credit age under 4 years.

The fix is not to game the system. The fix is time and smart account choices. Keep old accounts open. Do not close your first credit card because you stopped using it. That old account is doing real work for your score.

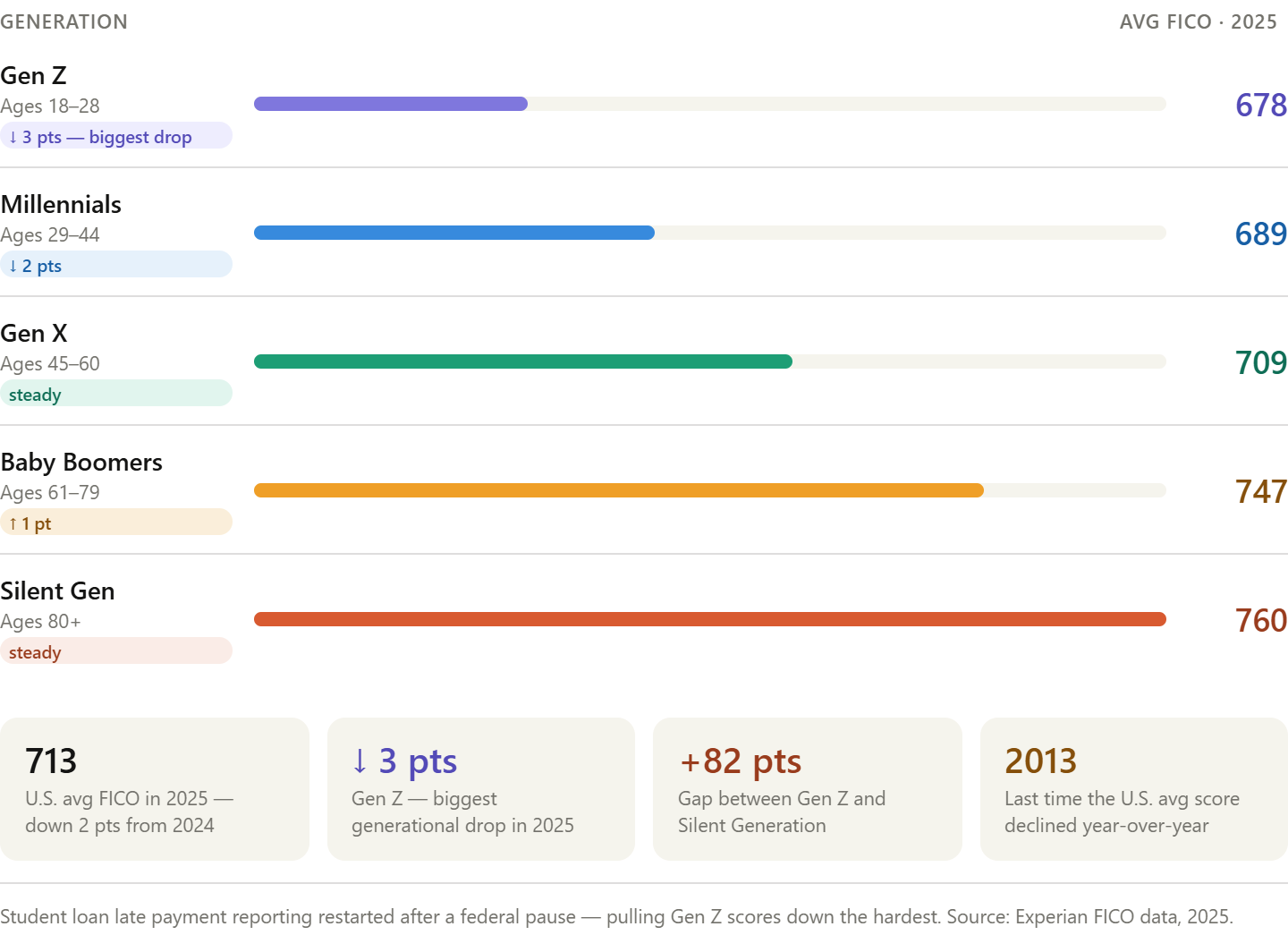

Credit Score Average by Age: What the Data Shows

Age and credit score move together. But not because of your birthday. Older people have simply had more time to build credit history.

Here is the breakdown from Experian's 2025 FICO data:

The gap between Gen Z and Baby Boomers is 69 points. Much of that gap comes from credit history length alone. A 25-year-old cannot have 20 years of history. No matter how well they manage credit. Time is the only fix.

Insufficient Length of Credit History: What Happens on Applications

"Insufficient length of credit history" is an actual denial reason under the Fair Credit Reporting Act. Lenders use it to decline credit or offer worse terms. Mortgage lenders often need at least 2 years of credit history. Many prefer 4 or more. Premium credit cards from Chase or American Express also look at average account age.

When a lender sees thin history, your file gets a "thin file" flag. This blocks approvals for mortgages, auto loans, and even some rentals.

The fastest legal way to build history is to become an authorized user. Ask a family member to add you to a long-standing account. You inherit that account's full age. A card open for 15 years adds 15 years to your profile right away. That raises your average account age in one move.

Understanding what is a good length of credit history also means knowing how lenders define "enough." Two years open most auto loan doors. Seven years open most mortgage doors. Ten years open the rest.

How Long Does It Take to Build the Highest Credit History Score?

An 850 FICO score takes decades. FICO data shows the average oldest account for 850-score holders is 30 years. But you do not need 30 years to get the best rates.

Here is what matters at each point:

The target for most people is 7 years. Hit that with a clean payment history and low credit use. You will qualify for most products at good rates. Each year after that adds more strength to your score.

Length of Credit History Calculator: How to Estimate Your Credit Age

No public tool from FICO or Experian gives a live credit age number. But you can calculate it yourself in three steps:

Pull your free credit report at AnnualCreditReport.com.

List every open account and its open date.

Count the months each account has been open. Add those up. Divide by the total number of accounts.

That result is your average credit age. For your overall credit history length, find the date your oldest account opened. That date marks the start of your credit timeline.

Credit monitoring tools like myFICO, Credit Karma, and Experian's app show your average account age on their dashboards. They update in real time. You can see exactly how opening a new account drops your average before you apply.

Build Credit the Smart Way

Is Your Credit History Holding You Back?

A short credit history can affect loan approvals, mortgage rates, and credit card offers, even if your score looks good. Let ASAP Credit Repair help you review your credit report and find the next best step.

Get Your Free Credit ReviewCheck your credit report before your next loan or mortgage application.

Three Actions That Move the Needle Now

A good length of credit history grows slowly. But these three steps speed it up:

Keep your oldest accounts open. Even unused cards protect your credit age.

Ask to become an authorized user on an older account. You inherit the full age without opening new credit.

Do not open multiple new accounts at once. Each new account drops your average age and adds a hard inquiry.

Credit history cannot grow overnight. But it grows every month you keep accounts in good standing. That track record is exactly what lenders pay attention to most.