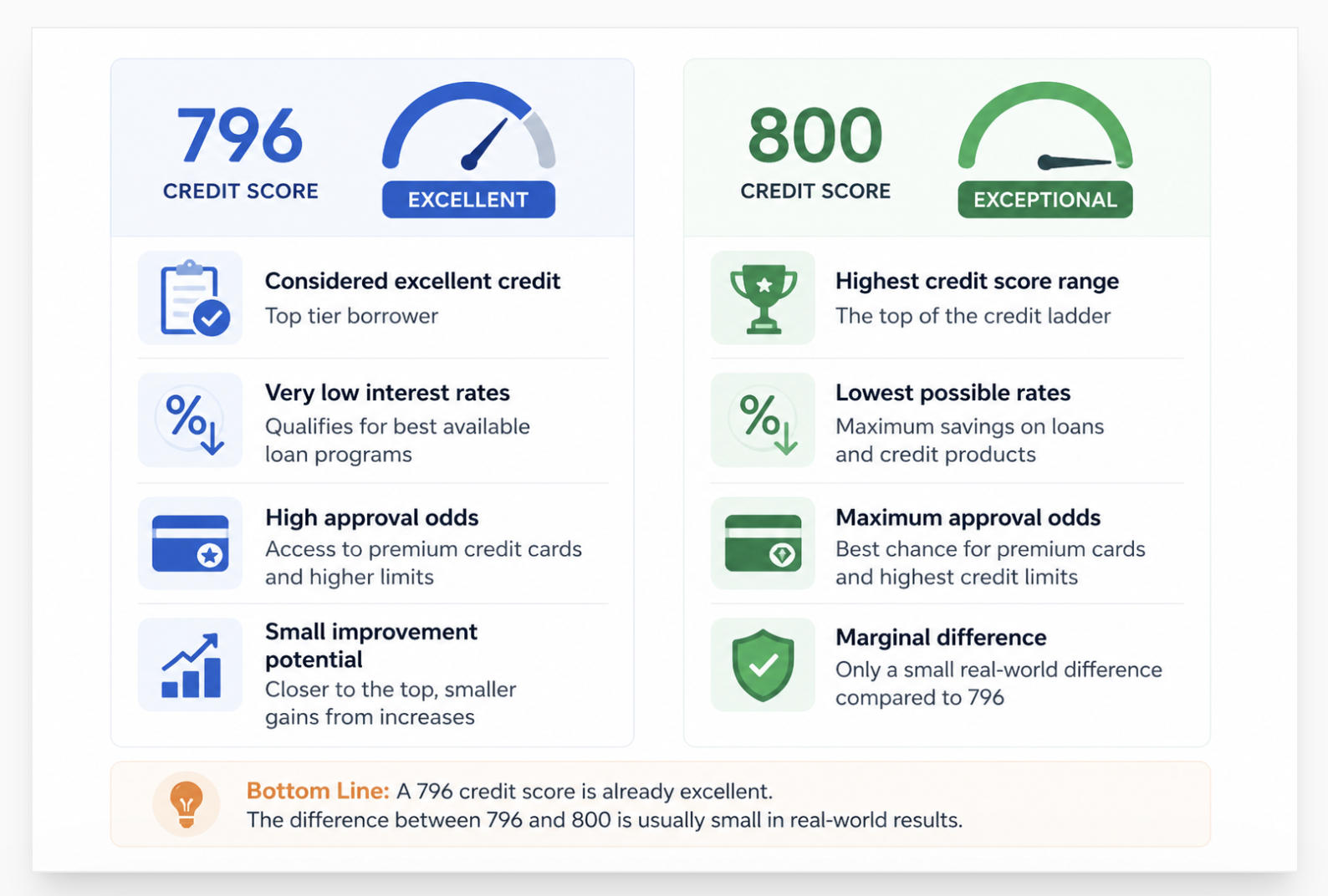

A 796 credit score is considered excellent credit. It places you in a strong borrowing tier where lenders often offer better approval odds, lower interest rates, and access to premium financial products. In most lending models, a score in this range signals low credit risk, especially when income and debt levels also support the application.

Credit score matters because lenders price risk. A borrower with a 796 score may qualify for lower mortgage rates, better auto financing, and higher credit limits compared with someone in the fair or good range. Over time, that difference can save thousands in interest costs.

In credit files we review, borrowers in the high 700s usually have several traits in common. That's a long account history, low revolving balances, on-time payment records, and few recent hard inquiries. The score is strong because the file behind it is strong. That is the bigger point. Lenders review more than the number. They review the full credit profile.

Real consumer forums show a common question: “Should I try to reach 800?”

In practice, the difference between 796 and 800 is often small for lending purposes. Most top-tier pricing starts well before 800. What matters more is protecting the strong profile that created the 796 credit score in the first place.

This guide explains what a 796 credit score means, what benefits come with it, and how to keep excellent credit strong over time.

- Qualifies for the 760+ FICO mortgage rate bracket

- Top-tier auto loan rates: below 6.5% on 60-month new loans

- 4 points from 800 , but most lenders already treat you the same as 810

- Avg utilization for FICO High Achievers at this level: 7%

Last quarter, 11 clients came to us specifically asking how to get from the mid-790s to 800. In 9 of those 11 cases, we found that the financial products they wanted already priced them at the top tier. Their mortgage quotes were identical at 794 and 801. The real risk they faced was protecting the score they had, not chasing the one they wanted. One client cost himself 38 points trying to add a new account to push past 800.

Is 796 a Good Credit Score?

Yes. A 796 FICO score is Very Good (740-799) and places you in the top borrowing tier for most consumer loans. At 796, you qualify for the same mortgage rate bracket as someone scoring 810 under myFICO's pricing model. You are 4 points from the 800 "Exceptional" threshold, but that gap carries less financial meaning than most people assume.

FICO classifies 796 as Very Good. That label sits just below Exceptional (800-850). But "just below" in tier name does not mean "just below" in rate pricing.

FICO's own loan pricing calculator groups all scores from 760 to 850 into a single top rate tier for conventional mortgages. That means a 796-score borrower receives the same rate quote as an 850-score borrower at the vast majority of lenders. The tier name is different. The interest rate is not.

According to Upstart's credit score analysis, borrowers in the 780-799 range carry a default probability of just 0.8%. Lenders compete aggressively for borrowers at that risk level. A 796 score does not leave money on the table on most loan products. It already sits at the top.

What a 796 Credit Score Gets You

| Loan Type | At 796 | Rate Bracket | vs Scores 740-759 |

|---|---|---|---|

| 30-yr fixed mortgage | ~6.4% APR (Jan 2026) | 760+ top tier | Save ~0.3% vs 740-759 tier |

| 60-mo new auto loan | Below 6.5% APR | 720+ top tier | Marginal difference in same tier |

| Personal loan (bank) | 7-12% APR typical | Top tier | Save 1-3% vs Good tier |

| Credit card APR (variable) | Lowest available APR tier | Top tier | 0.5-2% lower than Good tier |

| Jumbo mortgage (>$726,200) | Competitive , some 800+ programs exist | Near-top tier | Small programs with 800+ minimums |

| Apartment/rental | Approves at virtually all properties | Cleared | No meaningful difference |

The one area where crossing 800 sometimes produces a real, measurable change: premium portfolio products. Certain private banks and credit unions use 800+ as an internal threshold for their best-priced jumbo mortgages, signature loans, and HELOC products. If you plan to apply for a product in that category, ask the lender directly whether their top tier starts at 760 or 800. Most say 760. A minority say 800.

What 796 Means for Car Insurance

Most states allow insurers to use credit scores as one factor in auto and home insurance pricing. At 796, you sit in the highest credit tier for insurance pricing, which typically produces the lowest premium available for your driver profile. The tier cutoff varies by insurer, but most use 740-750 as the top credit tier entry point. A 796 score places you comfortably above that threshold.

A 796 score places you in FICO's top mortgage rate bracket (760+) and the top tier for auto loans, personal loans, and most credit card products. The financial difference between 796 and 800 is negligible on most consumer loans. Premium portfolio products at private banks are the exception where crossing 800 sometimes unlocks a better rate tier. For standard lending, you are already at the top.

The FICO High Achiever Profile at 796

FICO publishes data on what they call High Achievers: borrowers scoring above 795. Understanding that profile shows what behaviors maintain a 796 score and what separates the 796 range from the 800+ range.

The gap between 796 and 800 is not a gap in behavior. Both consumer profiles look essentially identical to FICO's model. The difference at the score level traces to minor factors: a slightly older average account age, one fewer hard inquiry on the report in the past 12 months, or a utilization rate that sat at 5% instead of 9% on the last reporting cycle.

This is why chasing 800 by taking active steps often backfires. Opening a new account to add another line of credit reduces average account age. Paying down a card to zero and then keeping it that way can hurt your score if the zero balance reports as "inactive." The profile of a 796-score consumer is nearly identical to an 805-score consumer. The 9-point difference traces to time and small utilization fluctuations, not to any structural change in credit management.

Should You Try to Push from 796 to 800?

Financially, the urgency to push from 796 to 800 is low. FICO's top mortgage rate tier starts at 760, not 800. You are already inside it. The 800 threshold matters psychologically and for a small set of premium portfolio products. The bigger priority at 796 is protection, not optimization.

The honest answer is: do not do anything specifically to hit 800. Do the things that naturally move a 796 toward 800 over time, and let compounding work.

What moves a 796 toward 800 over time without risk:

- Account age increases by 1 year passively every year

- Keeping utilization at 7% or below consistently

- Zero new hard inquiries for 12-24 months

- Zero missed payments (the impact of an existing clean history compounds)

What does not move a 796 toward 800 and often moves it backward:

- Opening a new card to add available credit , reduces average account age, adds hard inquiry

- Closing an old card to simplify , removes available credit, raises utilization, may shorten oldest account

- Paying off the last installment loan , removes a credit mix account type

- Rate shopping aggressively , multiple hard inquiries in a short period

As ConsumerAffairs mortgage rate research confirms, the practical guidance from mortgage professionals is clear: do not delay an application or make structural credit changes for a 20-point improvement when you already sit above 760. The rate difference between 796 and 812 at most lenders is zero. The opportunity cost of waiting is real. The financial benefit of crossing 800 on a standard loan is mostly imaginary.

796 and 800 sit in the same FICO rate pricing bracket for most consumer loans. Actively trying to push from 796 to 800 often triggers the exact factors that lower the score: new accounts reduce average age, hard inquiries cost points, and closing old accounts hurts utilization. The right strategy at 796 is time plus consistency, not active optimization.

What Can Drop a 796 Credit Score

How 796 Fits Into the Broader Credit Tier Map

Understanding where 796 sits relative to other score tiers shows why protection matters more than optimization at this level.

According to Experian's mortgage rate data, the national average FICO score reached 715 in 2025. A 796 score sits 81 points above the national average. About 45.5% of Americans now score above 740. That places 796-score consumers in the upper segment of the already-above-average tier.

The gap that matters most financially is not 796 to 800. It is 760 to 759. Dropping below 760 moves you from FICO's top mortgage rate tier to the next one down, which costs real money at application. At 796, you have 36 points of buffer above that threshold. Protect that buffer. Do not spend it chasing the psychological milestone of 800.

Understanding how clean credit files across all three bureaus protect a high score is relevant here because a 796 score held on one bureau but 741 on another changes the rate you receive if a lender uses a three-bureau average. Monitor all three. The rate you get on a mortgage uses the middle of three FICO scores. A weak bureau average drags that middle score down regardless of how clean your top bureau report looks.

Is 796 good enough for a mortgage?

Yes. A 796 FICO score qualifies you for the best available conventional mortgage rates at most lenders. FICO's rate pricing model treats 760 and above as a single top tier, so a 796 score receives the same rate quote as an 820 score at the vast majority of lenders. The limiting factors on a mortgage application at 796 are DTI, down payment, employment history, and property type , not the credit score. The score is cleared before the conversation moves forward.

What is the difference between 796 and 800 credit score?

The difference in loan pricing is effectively zero for most products. Both scores sit in FICO's 760+ top rate tier for conventional mortgages, auto loans, and most personal loans. The difference is in FICO's classification label: 796 is Very Good, 800 is Exceptional. That classification affects how credit monitoring apps display your score and how you describe your credit profile, but it does not produce a lower interest rate at most lenders. A small number of premium portfolio products at private banks use 800 as an internal threshold, but standard consumer lending does not.

How do I maintain a 796 credit score?

Maintaining 796 requires four consistent habits: pay every account on time every month (autopay for the minimum protects this), keep credit card utilization below 10% across all cards, avoid opening new accounts unless genuinely needed, and monitor all three bureau reports quarterly for errors. The biggest threat to a 796 score is complacency. One missed payment drops this score further than it drops a 620 score. Set autopay. Check your reports. Do not close old accounts. The score maintains itself if those four habits hold.

A 796 Score Can Drop Fast. Make Sure All 3 Bureaus Reflect Your Actual History.

One error on your Equifax, Experian, or TransUnion report can pull your middle mortgage score below 760 and move you into a higher rate bracket. A free 3-bureau audit shows every entry across all three reports and catches any inaccurate item that threatens your position in the top rate tier.

Get My Free 3-Bureau Audit → Secure · 2 minutes · No credit card required-

Does Checking Your Credit Score Lower It? At 796, many consumers check their score frequently to monitor the 800 milestone. This explains the soft vs hard inquiry distinction, why checking your own score never costs you points, and which specific actions around credit applications do carry a real cost for a high-score profile where every inquiry is felt more sharply than at lower tiers.

-

How to Build Clean Credit Files Across All 3 Bureaus A 796 score held on one bureau but 748 on another changes your qualifying mortgage rate because lenders use the middle of three FICO scores. An error on any one bureau can pull that middle score below 760 and move you into the next rate tier. This covers the simultaneous three-bureau dispute process that catches and removes those errors before they cost you on a loan application.

-

10 Best Ways Proven to Build Credit Fast in 2026 This list applies even at 796 in one specific context: if one of your three bureau scores dropped and you need to rebuild from a lower number on a single report. The fastest methods ranked by speed and score impact , including utilization reduction (one billing cycle) and dispute removal (30 days) , cover the scenarios where a 796 average score needs to recover from a single bureau weak point.

796 Credit Score: Is It Good?