What is insolvency? Insolvency means you owe more than you own, and you cannot pay your debts when they come due. It is a financial state, not a legal one. Understanding insolvency also means knowing how it connects to debt forgiveness, credit damage, and bankruptcy.

Running a credit repair company, I see what insolvency does to people before they even know what to call it. One of the most unforgettable accounts came from a client who got a Form 1099-C in the mail. Her credit card company had forgiven her balance. She had no idea that forgiven debt counts as taxable income until the tax bill arrived.

The numbers back this up. According to the U.S. Courts, total bankruptcy filings rose 14.2 percent in 2024, reaching 517,308 cases. Business filings alone jumped 22.1 percent. Insolvency often comes first, long before any of those filings happen.

What Is Insolvency in Business?

Insolvency in business means a company can no longer pay its debts on time. Creditors stop getting paid. Suppliers may cut off shipments. Lenders start making calls.

For a business, insolvency shows up in two ways. First, cash runs dry, and bills pile up faster than revenue comes in. Second, the total value of what a business owes exceeds the total value of everything it owns.

Neither situation automatically ends a business. But both require fast action.

Businesses reach insolvency for many reasons:

A sudden drop in sales revenue

Rising costs without a matching rise in income

Poor cash flow management

Unexpected legal judgments or penalties

A major customer defaulting on large invoices

Last year alone, our firm handled dozens of cases where a small business owner had no idea their company was insolvent until creditors sent formal notices. By that point, options narrow quickly.

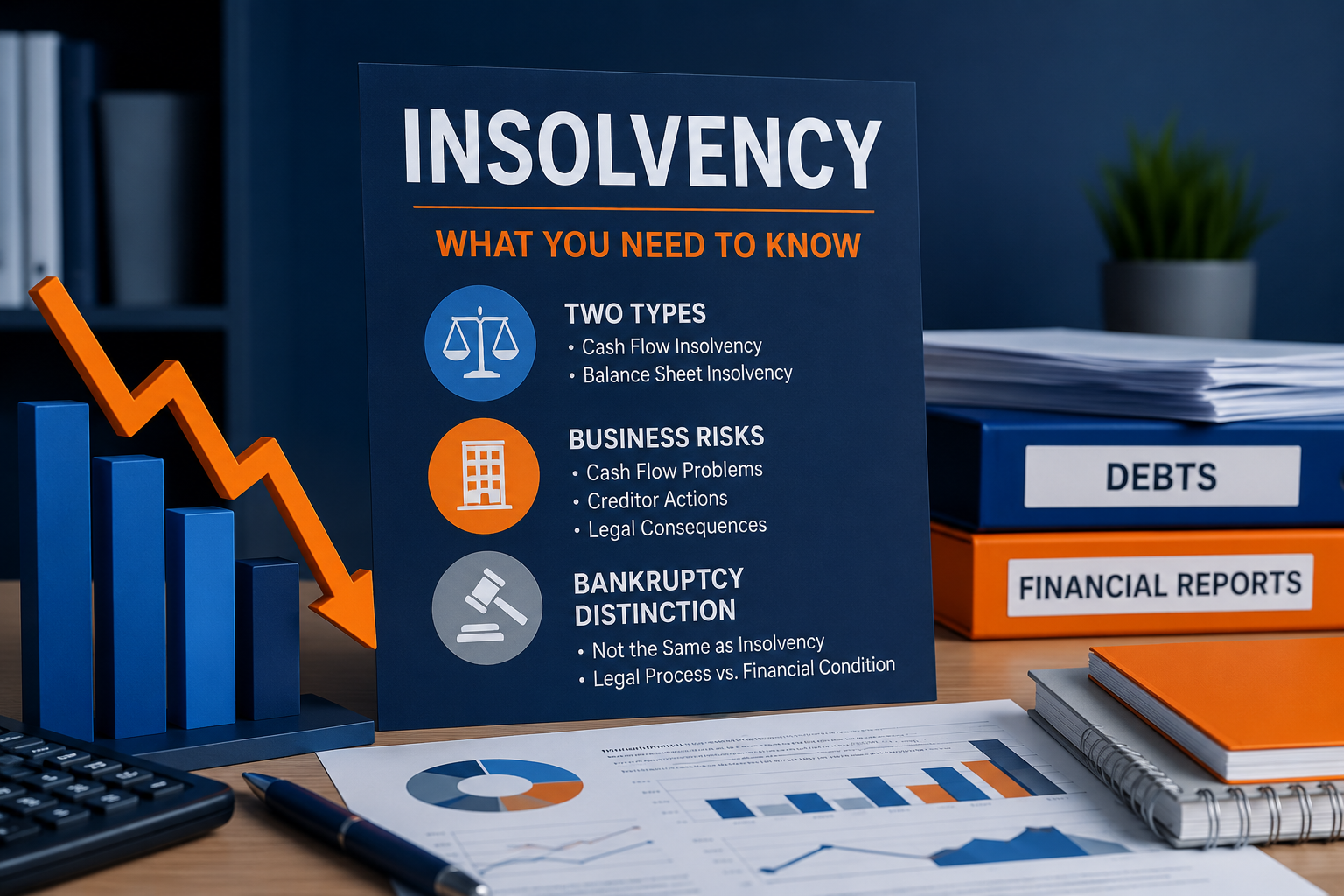

What Are the Two Types of Insolvency?

Insolvency falls into two types: cash flow insolvency and balance sheet insolvency.

Cash flow insolvency happens when a person or business has assets but cannot access cash fast enough. Think of a property owner who is asset-rich but cash-poor. Their building has value. Their bank account does not. Cash flow insolvency is often temporary.

Balance sheet insolvency happens when total debts exceed the total fair market value of all assets. Even if every asset were sold, the proceeds would not cover what is owed. This type is more severe.

The IRS defines insolvency this way: total liabilities minus total assets equals the insolvency amount. Balance sheet insolvency is the only type the IRS formally recognizes for tax purposes.

Here is a simple example. A person owes $120,000 across a mortgage, credit cards, and car loans. Their total assets add up to $105,000. That $15,000 gap makes their balance sheet insolvent.

Cash flow insolvency carries a lower risk of bankruptcy. Creditors often agree to restructure payment plans when they know assets exist. Balance sheet insolvency leaves fewer options.

So now you know what insolvency means and the two forms it takes. Next, here is how insolvency differs from bankruptcy, a distinction that trips up most people.

What Is the Difference Between Insolvency and Bankruptcy?

Insolvency is a financial condition. Bankruptcy is a legal process.

A person can be insolvent without filing for bankruptcy. But a person in bankruptcy is always insolvent by definition.

Insolvency is reversible. Someone can work out a payment plan, sell assets, or restructure their debt. Bankruptcy goes through a court and follows federal law.

Think of it this way: insolvency describes what your finances look like. Bankruptcy describes what happens next if insolvency goes unresolved.

Bankruptcy comes in several forms. Chapter 7 liquidates non-exempt assets to pay creditors. Chapter 11 lets businesses reorganize and keep operating. Chapter 13 lets individuals repay debt over three to five years. According to Congress.gov, Chapter 7 was the most common filing in 2024, making up 54.5 percent of all business bankruptcies.

Bankruptcy also leaves a mark on credit. A Chapter 7 stays on a credit report for ten years. A Chapter 13 stays for seven years. Insolvency itself does not appear on a credit report. The missed payments and collection accounts that caused it do.

Clients who come to us with insolvency questions often fear bankruptcy most. In many cases, addressing insolvency early avoids the courtroom entirely.

What Happens If a Business Is Insolvent?

When a business becomes insolvent, several things can happen. Much depends on how fast the situation gets addressed.

Creditors may start formal collection actions. Suppliers may demand cash before delivering goods. Lenders may declare a default and demand full repayment.

Businesses have three main paths forward:

Negotiate with creditors. Creditors often prefer a restructured plan over the risk of bankruptcy court. Last quarter, we saw seven small business cases where creditors agreed to extended timelines rather than take legal action.

Restructure operations. A business can cut costs, reduce staff, or renegotiate supplier contracts. This path works best in cash flow insolvency, where the business still has value.

File for bankruptcy protection. Chapter 11 lets businesses reorganize debt while staying open. Chapter 7 liquidates the business. Business bankruptcy filings in 2024 hit 23,107 cases — a 22.1 percent jump from the prior year, per the Administrative Office of U.S. Courts.

Insolvent businesses that act quickly tend to have better outcomes. Waiting makes the options smaller and the damage larger.

At this point, you know what insolvency means, both types, and how businesses respond to it. Now, here are the steps to tell you whether you actually qualify.

How Do You Calculate Insolvency?

Calculating insolvency requires two numbers: total liabilities and the fair market value of total assets.

Total liabilities include everything you owe. Credit cards, car loans, mortgages, medical bills, and student loans all count.

Total assets include everything you own at fair market value. Your home, car, retirement accounts, savings, and personal property all count, even assets creditors cannot touch.

The formula is simple:

Total Liabilities minus Total Fair Market Value of Assets = Insolvency Amount

If that result is a positive number, you are insolvent by that amount.

The IRS publishes a free worksheet inside Publication 4681. It walks through each category step by step. The IRS only lets you exclude canceled debt from income up to the exact amount you were insolvent.

For example, if you are $10,000 insolvent and a creditor cancels $14,000 in debt, only $10,000 is tax-exempt. The remaining $4,000 counts as taxable income.

Can You Recover from Insolvency?

Yes. Insolvency is not permanent. Many individuals and businesses move through it without ever filing for bankruptcy.

Recovery takes a clear approach. Start by identifying which type of insolvency applies. Cash flow insolvency often resolves faster because assets exist to generate funds. Balance sheet insolvency requires reducing total debt or increasing asset value over time.

Practical steps:

Contact creditors early and request restructured payment terms.

Review all expenses and cut non-essential costs.

Explore debt settlement if balances have become unmanageable.

Consult a financial advisor with insolvency experience.

File IRS Form 982 if a creditor cancels debt while you are insolvent.

Insolvency also damages credit. Missed payments and collection accounts show up on credit reports and lower credit scores. Recovering credit after insolvency takes time, consistent on-time payments, and sometimes a formal dispute process for errors or outdated negative items.

The earlier the insolvency gets addressed, the more options stay open.

Struggling With Debt or Credit Damage?

Insolvency Can Hurt Your Credit Before Bankruptcy Ever Happens

Missed payments, charge-offs, collections, and debt settlements can lower your score fast. Get a free credit report review and see what negative items may be hurting your financial recovery.

Get Your Free Credit Report ReviewNo pressure. Just a clear look at what may be holding your credit back.

What Does Insolvency Mean for Your Taxes?

Insolvency carries a specific tax benefit that most people miss. When a creditor cancels or forgives a debt of $600 or more, they file Form 1099-C with the IRS. The IRS treats that forgiven amount as taxable income.

If you were balance sheet insolvent at the time of the cancellation, you can exclude that income from your taxes, up to the amount you were insolvent. This is called the insolvency exclusion.

To claim it, file IRS Form 982 with your federal return for the year the debt was canceled. You do not need to be in bankruptcy to qualify. You only need to show that your liabilities exceeded your assets at the time.

The IRS confirms this: forgiven debt may be excluded from income to the extent a taxpayer is insolvent. That exclusion can save thousands of dollars during an already hard time.

Many people who come through our doors have already received a 1099-C and do not know this exclusion exists. Claiming it correctly requires accurate records of every asset and liability at the exact time the debt was forgiven.

Insolvency is a financial state, not a permanent outcome. Knowing what type you face, how to calculate it, and what recovery options exist gives you a real head start. The data on rising bankruptcy filings shows more Americans are reaching this point every year. Most wait too long to act. The ones who engage early with creditors, advisors, and the IRS protect far more of their financial future.