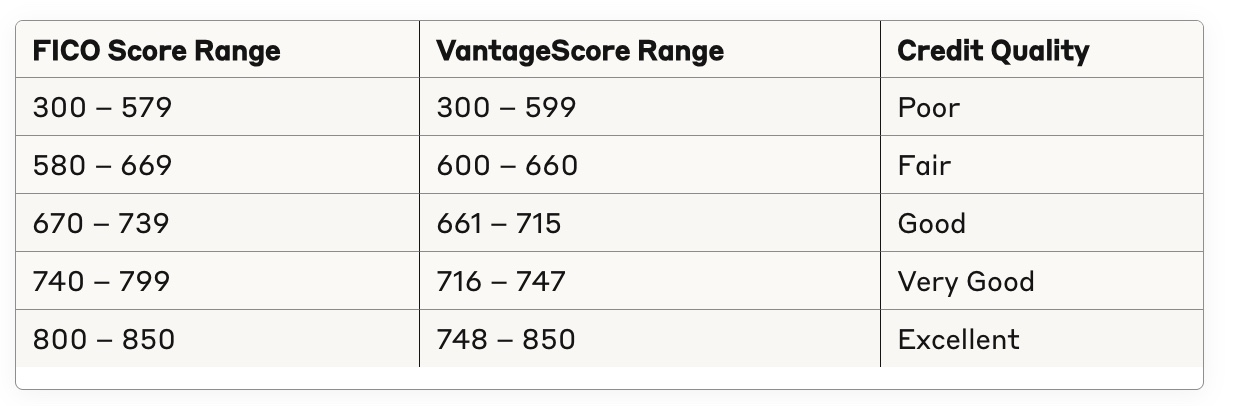

The lowest possible credit score is 300 for both FICO® and VantageScore® credit scoring models. This represents the absolute bottom of the credit score range, which extends from 300 to 850.

What most people don’t know is your credit score doesn’t start at zero, not even at 300 (which is the lowest credit score). In fact, you don’t get a score at all until you have credit activity reported to the bureaus. When you first begin building credit and make on-time payments, you’ll usually start in the 600s, which is considered “fair.”

It can just plummet to this rock-bottom level due to severe negative marks on your credit report. Understanding what causes scores to drop this low, and how to recover, is crucial for your financial future.

Credit Score Ranges: Where 300 Fits

A 300 credit score falls squarely in the "Poor" category and represents significant financial distress. While the average American credit score hovers around 716, a score of 300 means you're facing serious credit challenges that demand immediate attention.

Why Do Credit Scores Drop to 300?

Your credit score doesn't randomly drop to 300. This devastating score typically results from multiple severe negative marks that compound over time.

The most common culprits include:

Payment History (35% of your score): Consistently missing payments or stopping payments altogether creates a catastrophic pattern that destroys your creditworthiness.

Collection Accounts: When debts go unpaid, they're often sold to collection agencies. These accounts can devastate your score for up to seven years.

Bankruptcies and Foreclosures: These are among the most damaging events and can linger on your report. Chapter 7 bankruptcy lingers on your credit report for 7-10 years, while Chapter 13 bankruptcy and foreclosures remain for seven years.

Excessive Hard Inquiries: While one or two credit applications won't hurt much, multiple hard inquiries in a short period signal desperation to lenders.

Credit Report Errors: Mistakes happen, but when they're not corrected, they can unfairly drag your score down to dangerous levels.

Defaulting on loans: Defaulting on any type of loan can heavily impact your score.

Once your score hits this level, it may feel impossible to recover, but with a plan and consistent effort, rebuilding is absolutely possible.

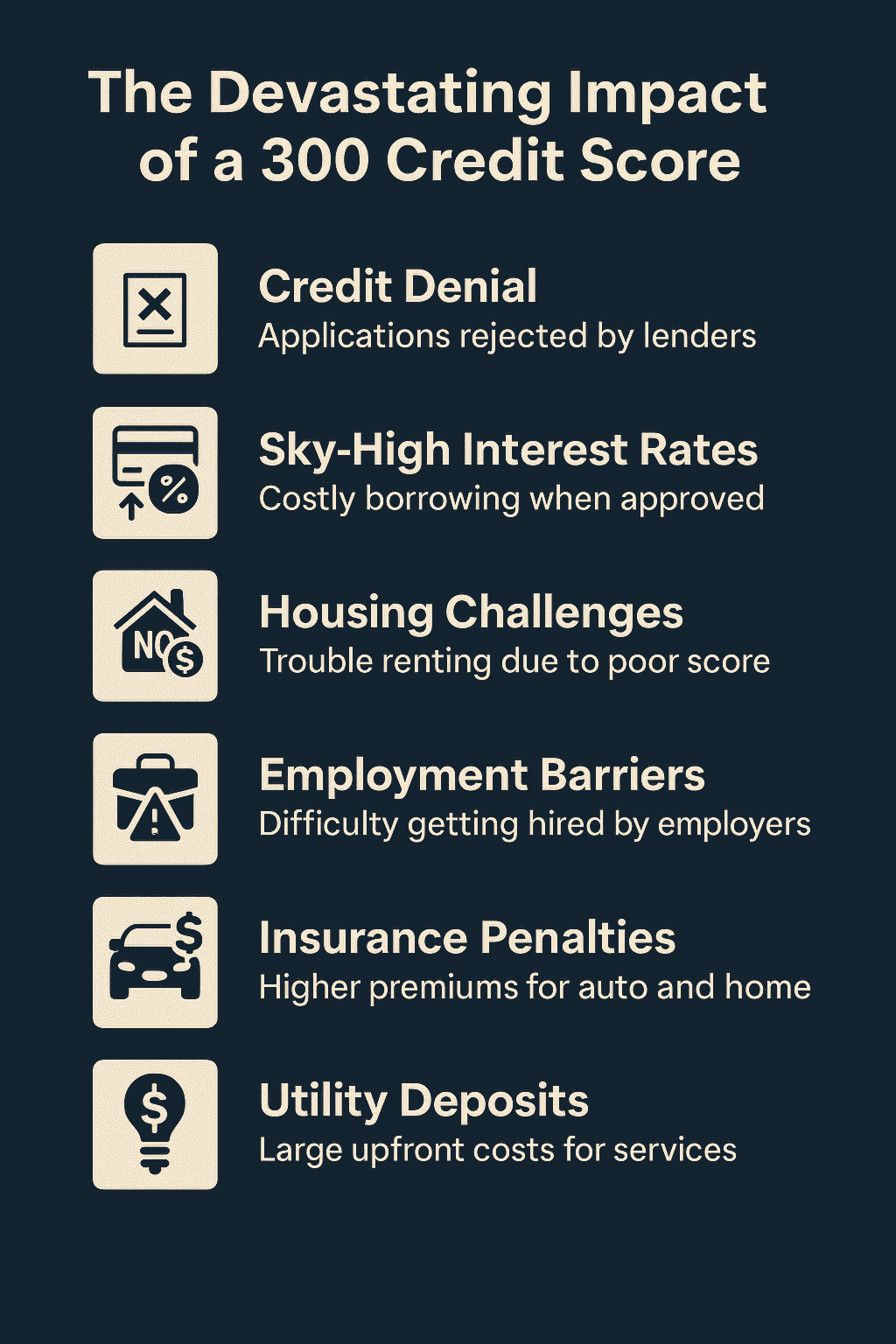

The Devastating Impact of a 300 Credit Score

A 300 credit score doesn't just limit your borrowing options—it can fundamentally alter your quality of life:

- Credit Denial: Most traditional lenders will flat-out reject your applications, leaving you with predatory lending options that trap you in cycles of debt.

- Sky-High Interest Rates: When you do qualify for credit, you'll pay premium rates that can cost you thousands of dollars over the life of a loan.

- Housing Challenges: Landlords routinely reject applicants with scores this low, forcing you into substandard housing or requiring substantial security deposits.

- Employment Barriers: Many employers check credit reports, especially for financial positions, potentially limiting your career opportunities.

- Insurance Penalties: Auto and home insurance companies often charge higher premiums to customers with poor credit.

- Utility Deposits: Basic services like electricity and phone service may require hefty security deposits.

Can You Recover from a 300 Credit Score?

Yes, absolutely. While a 300 credit score represents a financial emergency, it's not a permanent life sentence. Recovery requires strategic action and patience, but it's entirely possible to rebuild your credit to good or even excellent levels.

7 Proven Strategies to Escape the 300 Credit Score Trap

1. Eliminate Collection Accounts Immediately

Pay off collection accounts and send pay-for-delete letters to potentially remove these toxic marks from your report entirely.

2. Challenge Every Error Aggressively

Dispute any inaccuracies on your credit report immediately. Even small errors can significantly impact an already damaged score.

3. Automate All Payments

Set up automatic payments for at least the minimum amount due. On-time payments are the single most powerful tool for score recovery.

4. Slash Credit Utilization Below 30%

Keep your credit card balances well below 30% of your credit limits. If you owe $300 on a $1,000 limit card, that's your absolute maximum.

5. Monitor Your Progress Obsessively

Check your credit reports and scores regularly to track improvements and catch new errors quickly.

6. Add Strategic Credit Lines

Once you've stabilized your payment history, consider secured credit cards or becoming an authorized user to increase your available credit and improve your utilization ratio.

7. Create a Debt Avalanche Plan

List all your debts from highest to lowest interest rate. Pay minimums on everything, then attack the highest-rate debt with every extra dollar you have. This strategy saves you the most money in interest charges while accelerating your path to financial freedom.

Bottom line: A 300 credit score can feel like an inescapable financial prison, but it doesn’t have to define your future. By taking immediate action and making consistent improvements, you can rebuild your credit, regain access to better financial options, and ultimately improve your overall quality of life.

Loan Options with a 300 Credit Score

While some may thing its near impossible, obtaining loans with a 300 credit score may happen.

What is the lowest credit score to buy a house?

The lowest credit score to buy a house depends on the lender and loan type, but 580 is generally the minimum for an FHA loan. Conventional loans often require scores of at least 620. However, a higher score doesn’t just help you qualify — it can secure you lower interest rates and better terms, saving you thousands over the life of your mortgage. Even if you meet the minimum, aim higher to unlock the best deals.

What is the lowest credit score to buy a car?

Most traditional auto lenders look for a credit score of at least 610, but requirements vary widely. If your credit is below this, you might still get a subprime auto loan. These come with higher interest rates and stricter terms, but they can help you finance a car when other options aren't available.

What is the lowest credit score to qualify for a personal loan?

While each lender sets its own criteria, most require at least a 600 credit score for a standard personal loan. If your score is lower, you may still qualify through subprime lenders, but expect higher interest rates, stricter terms, and possibly the need for collateral.

What is the lowest credit score to get a credit card?

Secured credit cards are often available to those with scores as low as 300, since they require a refundable security deposit as collateral. For unsecured credit cards, most issuers prefer at least a 580–600 score. Higher scores open up better cards with lower fees, higher limits, and rewards programs.

Don’t let errors harm your credit

Mistakes on your credit report can drag down your score and cost you better loan offers. ASAP Credit Repair has helped thousands of clients repair credit since 2004, sending over 221 million disputes to credit bureaus. Get your free credit assessment today and see where you stand.

How Soon Can You Recover from a 300 Credit Score?

- 0–6 months: Stop negative actions, start paying on time, dispute errors.

- 6–12 months: Add secured cards or credit builder loans, keep utilization low.

- 12–24 months: Reach 580–650 if consistent.

- 2–5 years: Possible to achieve 700+ with strong habits.

With consistent effort, you can start seeing improvements in as little as 6 months.

You may reach 580–650 within 12–24 months, and it’s possible to achieve a score of 700+ within 2–5 years if you maintain strong credit habits.

"I started at 300 after a bankruptcy. In about a year, I was already at 620 just by paying on time, keeping my balances low, and not applying for new credit. It really works if you stick to it!" — Reddit user

Lowest Credit Score FAQ

Is it possible to have a 250 credit score?

Technically yes, but only for certain industry-specific FICO scores (which range from 250–900). The standard FICO score most lenders use ranges from 300–850.

Can you get a loan with a 300 credit score?

It’s possible, but extremely difficult. You’ll likely face high interest rates (predatory loans), large down payments, and limited lender options, often restricted to subprime loans.

Can your credit score recover from 300?

Yes! Even a score of 300 can be rebuilt. By making on-time payments, paying down balances, and disputing inaccuracies on your report, you can gradually climb back to good credit. We’ve even worked with clients who started at 300 , not many, but it proves that with the right plan, recovery is absolutely possible.

What is the highest credit score?

The highest FICO score is 850 and considered exceptional. Only about 1.5% of Americans ever reach this perfect score.

How rare is it to have the lowest credit score?

Extremely rare. According to FICO, less than 1% of Americans have a credit score below 500 — and almost no one has the absolute lowest score of 300. Reaching this level typically requires multiple severe negative events (like repeated missed payments, defaults, and collections) over an extended period.

The Bottom Line About The Lowest Credit Score

A 300 credit score represents the lowest possible standard credit score and signals severe financial distress. However, with consistent effort, strategic planning, and time, you can recover from this financial low point. The key is taking immediate action to address the underlying issues while building positive credit habits for the future.

Remember that every point of improvement matters when you're starting from 300. Even reaching 580 opens doors to conventional mortgages and better loan terms. Your credit score is not your enemy but it's your starting point for financial recovery.

Disclaimer: We strive to provide accurate and up-to-date information, and this article has been carefully fact-checked using reputable sources. However, credit scoring and lending standards can vary by lender and change over time. We do not guarantee the accuracy or completeness of this content, and it should not be considered financial or legal advice. Always consult with a qualified professional regarding your unique situation.