Why Credit is important? because it determines your access to housing, loans, jobs, insurance, and financial freedom, and a single number controls all of it.

Running a credit repair company, I see this play out every single week. One of the most unforgettable cases we handled was a young professional who got denied for an apartment not because he had bad debt, but because he had no credit at all. He had done everything "right" by avoiding debt. But to the landlord, he was invisible. That moment changed how he saw money. And it's one of the reasons I'm writing this.

Here is the data that backs this up: a LendingPoint survey of 2,000 Americans found that 71% of respondents had no idea about the full consequences of a bad credit score. Seven in 10 people said they personally felt held back in life because of poor credit. And 41% said bad credit caused them trouble renting an apartment.

The r/personalfinance community on Reddit regularly surfaces these stories of people denied for rentals, hit with high interest rates, or turned down for jobs, all tracing back to one overlooked number.

Why Credit Is Important?

Credit is your financial track record. Lenders, landlords, employers, and insurance providers use it to answer one question: Can we trust this person?

The Consumer Financial Protection Bureau (CFPB) explains it directly: businesses use your credit history to decide whether to open a bank account for you, offer a credit card, set your interest rate, approve a rental, or approve a mortgage. When negative items appear on your report, such as missed payments, high balances, and collections, it becomes harder and more expensive to do basic things.

Credit is not just a borrowing tool. Credit is access.

Without it, you pay more for the same things. You get locked out of housing. You lose job offers. You carry higher insurance premiums. People with strong credit pay less for almost everything that requires a contract.

Why Should You Have Access to Credit?

Access to credit lets you bridge the gap between what you earn today and what you need to build long-term.

Most people cannot buy a car or a home with cash. They cannot pay for college up front. Credit makes those milestones possible. More specifically, it makes them affordable if your score is strong.

Here is a real number that shows why this matters. According to FICO data, a person with a 650 credit score on a $200,000 30-year mortgage pays around $1,371 per month. A person with a 760 credit score pays significantly less; the difference over 30 years can exceed $50,000. Same house. Same loan amount. The only difference is the credit score.

Beyond home loans, access to credit affects your daily life in ways most people overlook:

Utility companies run credit checks before activating accounts.

Cell phone carriers pull your credit when you apply for a plan.

Some insurance companies set your premium based on your credit-based insurance score.

Landlords screen credit before approving rental applications.

Employers in certain industries check credit reports during hiring.

The CFPB confirms all five of these. Without credit access, you face deposits, higher rates, and rejections across every one of them.

Why Does Credit Matter?

Credit matters because it is a multiplier. Good credit makes everything cheaper. Poor credit makes everything cost more.

Think of credit as a financial reputation. Every on-time payment builds it. Every missed payment chips away at it. Lenders check your reputation before every major transaction in your life.

Last year alone, our firm handled over 200 cases where clients were denied housing or loans due to errors on their credit reports, items that were inaccurate but still costing them real money. This is not rare. Errors on credit reports affect millions of consumers, and most people never check.

According to the CFPB, the share of adults with a scored credit record increased from 81.6% to 87.5% between 2010 and 2020. That means roughly 25.3 million Americans still lack a usable credit score. Without one, they face a wall in nearly every financial transaction.

Credit matters not just for what it opens but for what its absence closes.

Why Is a Good Credit Report Important?

Your credit report is the raw data behind your credit score. Lenders do not just look at the number; they look at the full picture. What accounts do you have? How long have you held them? Do you pay on time? How much of your available credit do you use?

A good credit report tells a story of financial reliability. A damaged one tells the opposite story, even if the damage is from an error.

The CFPB notes that landlords check your credit history when deciding whether to rent to you and whether to ask for a larger security deposit. Mortgage lenders use it to determine your rate. A strong history means lower interest charges. A weak one means higher costs or outright rejections.

Three credit bureaus, Experian, TransUnion, and Equifax, each maintain a version of your report. Errors in any one of them can drag your score down. You can request a free copy of each at AnnualCreditReport.com, once per year per bureau. Reviewing all three is the fastest way to spot inaccurate items that may be costing you points right now.

How Does Credit Affect Your Ability to Rent or Buy a Home?

Housing is where credit has its most immediate, visible impact.

Landlords run credit checks to predict tenant behavior. A low score or no score can result in a denial, a higher security deposit, or a requirement to pay multiple months upfront. This creates a real barrier for people who have never used credit. They have done nothing wrong, but they have no history to show.

For homebuyers, the stakes are higher. Mortgage lenders use credit scores to set interest rates. A difference of 50 to 100 points can mean thousands of dollars more per year in mortgage payments. Across a 30-year loan, the difference between a fair score and a good score can cost more than a second car.

Our clients who come to us before a home purchase, rather than after a rejection, consistently get better outcomes. When you repair or build credit 6 to 12 months before applying for a mortgage, you give yourself room to negotiate better terms.

How Does Credit Affect Employment?

Some employers check credit reports during the hiring process, especially for roles that involve financial responsibility, handling cash, or access to sensitive information.

This is not universal, and state laws vary. Several states restrict or prohibit employer credit checks. But where it is allowed, a credit report with collections, judgments, or unpaid accounts can cost you a job offer.

The employer never sees your score; they see a modified version of your credit report. But the content is the same. Late payments, charge-offs, and unpaid debts appear, and they can raise red flags around financial judgment.

According to the LendingPoint survey, 48% of respondents said they believed poor credit could cause trouble getting a job or security clearance. That concern is grounded in reality for anyone in finance, government, or security-related fields.

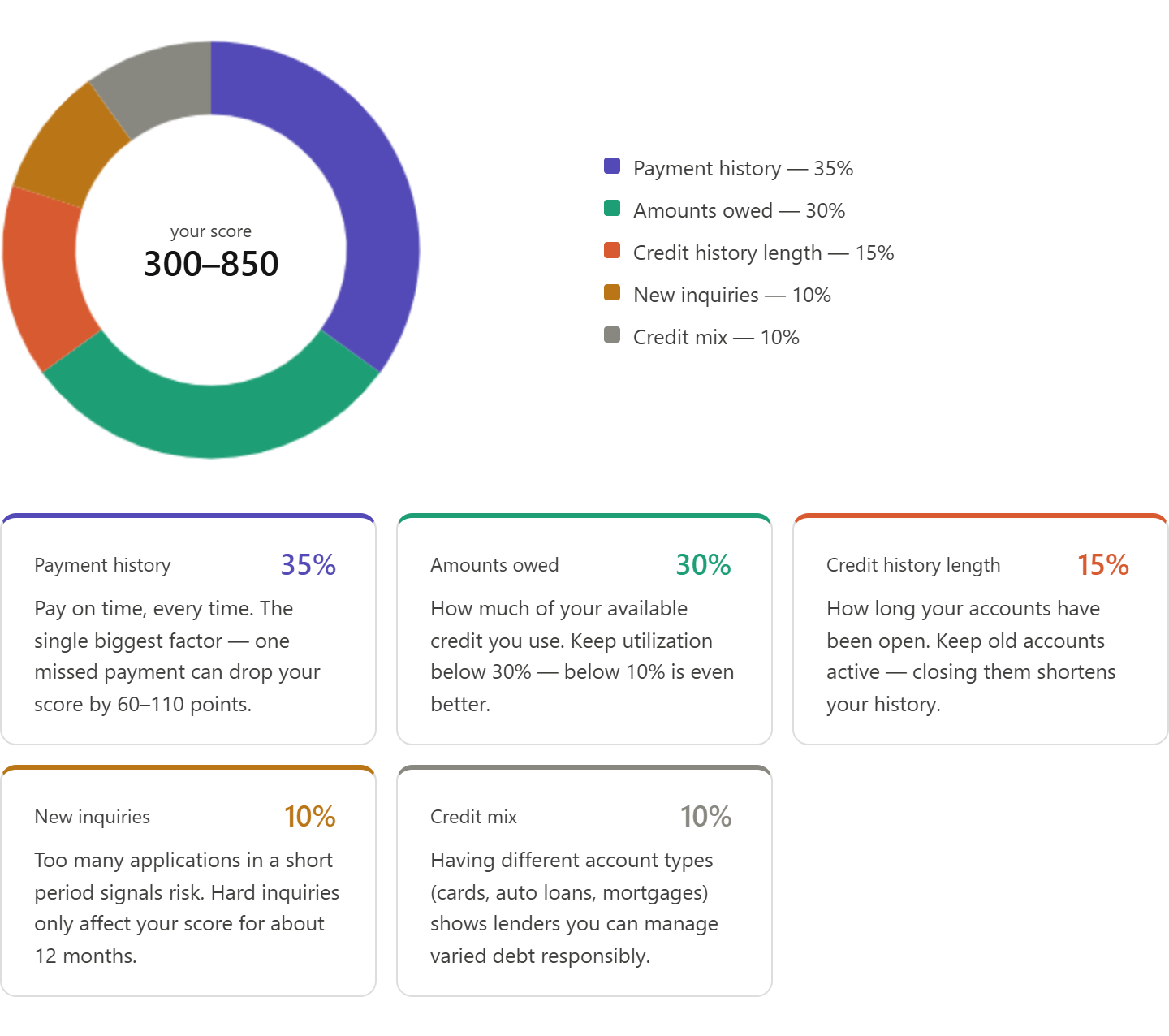

What Factors Make Up Your Credit Score?

Your credit score is calculated from five categories. Each one carries a different weight, and knowing them helps you protect and build your score strategically:

Payment history alone drives over a third of your score. One or two missed payments can drop a strong score by 60 to 110 points. That drop is fast. Recovery takes months, sometimes years.

Can Bad Credit Be Fixed?

Yes. Credit is not permanent. Every item on your report has rules that govern how long it can stay there. Most negative items fall off after seven years. Bankruptcy takes up to 10 years.

More importantly, inaccurate items can be removed at any time. Under the Fair Credit Reporting Act (FCRA), you have the right to dispute any information that is incorrect, incomplete, or unverifiable. The credit bureau must investigate and remove it if the creditor cannot verify the data.

This is the core of credit repair. Our firm disputes inaccurate items, outdated accounts, and errors that clients did not even know existed. We have seen scores jump 80 to 120 points within 90 days when multiple inaccurate items are removed at once.

Start by getting your free reports from AnnualCreditReport.com. Check every account. Look for accounts you do not recognize, incorrect balances, and duplicate entries. Dispute what is wrong.

Bad Credit Could Be Costing You Thousands

Your credit score affects mortgage rates, apartment approvals, car loans, insurance costs, and more. The longer negative items stay on your report, the more expensive life becomes.

✔ Get a professional review of your credit report

✔ Find inaccurate negative items hurting your score

✔ Learn the fastest path toward better credit

No obligation • Personalized review • Trusted credit repair guidance

How Long Does It Take to Build Credit?

Building credit from scratch typically takes 3 to 6 months to generate a FICO score. That requires at least one account reporting to the bureaus. Rebuilding damaged credit takes longer, typically 12 to 24 months to see meaningful improvement, depending on the severity of the damage.

The fastest path to building credit includes three steps:

Open a secured credit card or become an authorized user on someone else's account.

Keep your balance below 10% of your credit limit at all times.

Pay on time, every month, without exception.

Consistency matters more than speed. Lenders want to see a sustained pattern of responsible behavior, not a single month of perfect payments.

Frequently Asked Questions

Does checking your own credit score hurt it? No. Checking your own score is a soft inquiry. Only hard inquiries from lenders reviewing your application can affect your score, and only temporarily.

What credit score do you need to rent an apartment? Most landlords look for a score of 620 or higher. Some premium properties require 700 or above. Below 580 often results in a denial or a large deposit requirement.

What credit score do you need to buy a house? FHA loans allow scores as low as 580 with a 3.5% down payment. Conventional loans typically require a 620 or higher. The best mortgage rates are reserved for scores of 740 and above.

Is it possible to get credit with no credit history? Yes. Options include secured credit cards, credit-builder loans, becoming an authorized user, and some alternative-data credit programs. Starting early matters. Every month you wait is a month of credit history you cannot get back.

Credit is one of the most practical tools in your financial life and one of the most misunderstood. The sooner you understand what it controls, the more power you have to use it in your favor.