Discovering Acceptance Now collections on your credit report can be alarming, especially considering that 79% of credit reports contain mistakes or serious errors. Unfortunately, this collections account can hurt your credit score for up to seven years from the date of your first missed payment. We understand how stressful this situation can be when you're trying to maintain good financial health or apply for loans.

In fact, having a collections account on your report significantly reduces your chances of getting approved for loans or other important financial services. However, it's important to know that Acceptance Now Collections is a legitimate company, not a scam.

Additionally, while paying a debt in collections changes your status from "unpaid" to "paid," the collection still remains on your report for that seven-year period.

In this comprehensive guide, we'll walk you through everything you need to know about Acceptance Now collections, how it affects your credit score, and what steps you can take to address this issue effectively.

What is Acceptance Now Collections?

Acceptance Now Collections is a legitimate debt collection agency that appears on credit reports when they've either purchased your debt or are collecting it on behalf of another company.

Why is Acceptance Now on your credit report?

If you're seeing their name on your report, it means there's likely an unpaid balance that has been transferred to them for collection.

How Acceptance Now acquires debt

Acceptance Now Collections typically obtains debt through two primary methods.

First, they purchase delinquent accounts from creditors who have given up trying to collect themselves (often called a "charge-off"). They generally pay just pennies on the dollar. Sometimes as little as 1/10th of the original amount, just to acquire these debts.

Second, they may act as a third-party collector, working on behalf of other companies to recover money for a fee.

One notable connection is with Rent-A-Center, which operates as "Acceptance Now" inside nearly 1,300 independently owned furniture stores, including Ashley Furniture and Rooms to Go. In one documented instance, Rent-A-Center sold over 18,000 accounts deemed seriously in arrears to collection agencies.

What it means if they appear on your report

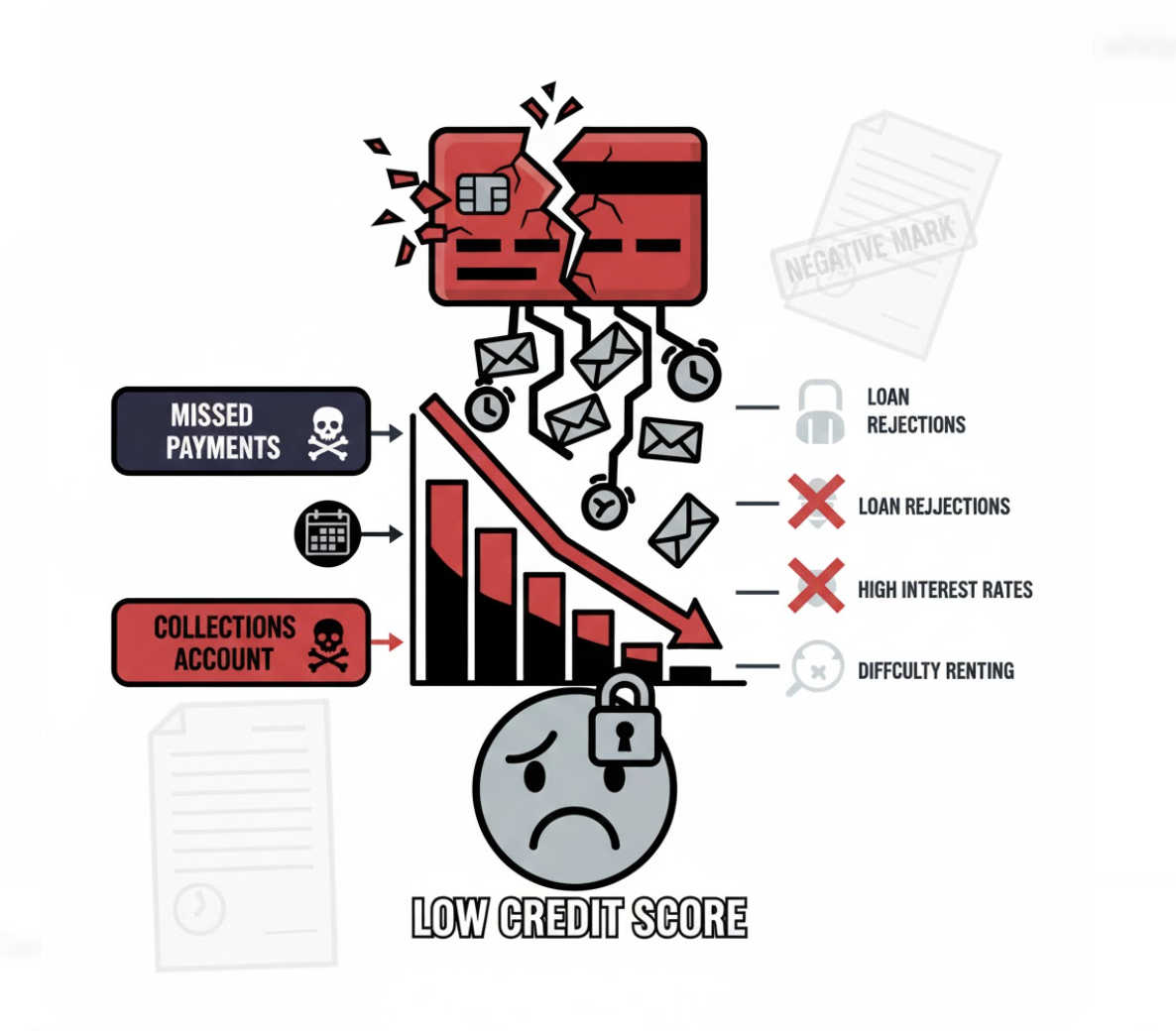

When Acceptance Now Collections appears on your credit report, it creates a significant negative impact that can last up to seven years from the date of your first missed payment. This collection entry is considered a derogatory mark that can severely lower your credit score.

As a result, you'll likely face greater difficulty getting approved for new loans or credit cards. Furthermore, this negative mark can lead to higher insurance rates and increased variable interest rates on existing credit cards.

Common reasons for being contacted

People are typically contacted by Acceptance Now Collections because they have fallen behind on payments for merchandise obtained through rent-to-own arrangements. These arrangements often involve furniture or other household items, as evidenced by accounts from consumers who purchased bedroom sets and other furnishings.

According to the Federal Trade Commission, aggressive collection tactics are common. They received 2,779 complaints about Rent-A-Center and Acceptance Now between January 2016 and June 2017, with more than 90% citing aggressive collection methods.

If you're receiving calls from them, it means they're actively attempting to collect what they believe you owe.

Rather than ignoring these contacts, it's important to understand your options and legal rights.

How Acceptance Now Collections affects your credit score

Having Acceptance Now collections on your credit report can devastate your credit health. Collections accounts are viewed as serious negative events by credit scoring models, often resulting in substantial score drops between 50 to 100 points or more.

Impact of collections on credit history

Collections fall under payment history, which accounts for approximately 35% of your FICO® Score 10 T and VantageScore® 4.0 calculations.

Consequently, when Acceptance Now reports a collection, it signals to lenders that you've failed to meet payment obligations. This negative mark can substantially harm your creditworthiness, particularly since unpaid collections typically cause more damage than paid ones.

Moreover, even if you eventually pay the debt, the collection's presence continues to impact your credit profile.

How long it stays on your report

Acceptance Now collections remain on your credit report for seven years plus 180 days from when your account first became past due.

Notably, this seven-year clock starts from the date of your first missed payment that led to the collection, not from when Acceptance Now acquired your debt. Despite settling the debt, your credit report simply changes the status from "unpaid" to "paid collection," but the entry itself persists for the full seven-year period.

The timeline doesn't reset if your debt gets sold to different collection agencies.

How it affects loan approvals and interest rates

The presence of Acceptance Now collections can severely limit your financial options:

- Mortgage applications - Collections affect your Debt-to-Income ratio (DTI), potentially decreasing your maximum mortgage qualification amount or resulting in denial

- Higher interest rates - Lenders view collections as high-risk indicators, subsequently charging higher rates to compensate

- Insurance premiums - Many insurers check credit reports and raise rates when collections appear

Ultimately, resolving collections prior to applying for new credit is advisable. Newer credit scoring models like FICO® Score 9 and VantageScore 3.0/4.0 ignore paid collections when calculating scores, which might help restore your creditworthiness faster than with older scoring models that continue considering paid collections.

How to remove Acceptance Now Collections from your credit report

Removing Acceptance Now Collections from your credit report requires strategic action. A staggering 79% of credit reports contain mistakes or serious errors, making verification your first priority.

Step 1: Check for errors or outdated info

Begin by obtaining copies of your credit reports from all three bureaus through AnnualCreditReport.com. Review each report carefully, noting any inaccuracies regarding account numbers, payment history, or the date of delinquency. These details will form the foundation of your dispute.

Step 2: Dispute with credit bureaus

File formal disputes with each credit bureau showing the error. Send detailed letters explaining precisely what information is incorrect. The bureaus must investigate within 30 days.

Step 3: Request debt validation

Within 30 days of initial contact, demand debt validation from Acceptance Now. Under the FDCPA, they must verify the debt's legitimacy. During this period, collection activities must pause until they provide proper verification.

Step 4: Consider a pay-for-delete (with caution)

Although controversial, negotiating a pay-for-delete agreement might remove the collection. Get any agreement in writing before making payment. Remember this only removes the collection account, not the original delinquency.

Step 5: Work with a credit repair company

Professional agencies like ours, ASAP Credit Repair USA can work on complex disputes. We understand credit laws and can often achieve better outcomes than handling it yourself.

Should you pay, settle, or ignore Acceptance Now Collections?

When dealing with Acceptance Now Collections, you have three main choices: pay, settle, or ignore.

Each option carries different consequences for your credit and financial health.

When paying might help

Paying your Acceptance Now debt changes your credit report status from "unpaid" to "paid," but remember—the collection still remains on your report for seven years from the date of first delinquency. Nevertheless, some newer credit scoring models give less weight to paid collections, potentially helping your score recover faster.

Risks of settling without removal

Settling your debt with Acceptance Now might lower your balance, yet it still marks as a collection on your report. Furthermore, debt settlement companies typically charge 15% to 25% of the settled amount. Bear in mind that any forgiven debt over $600 becomes taxable income, requiring you to pay taxes on that amount.

Why ignoring can backfire

Ignoring collection attempts is the worst approach you can take.

First, debt collectors may escalate to legal action. Second, if they win a judgment, they could garnish your wages or freeze bank accounts. Above all, the collection stays on your credit report, continuing to damage your score.

Understanding your legal rights under FDCPA and FCRA

The Fair Debt Collection Practices Act protects you from:

- Harassment and abusive practices

- Communication at inconvenient times (before 8am/after 9pm)

- Inaccurate debt reporting

You also have the right to request debt validation and dispute inaccuracies under both FDCPA and FCRA.

Conclusion

Dealing with Acceptance Now Collections presents challenges, but understanding your options gives you power over the situation. Throughout this guide, we've seen how collections can impact your credit score by dropping it 50-100 points and potentially limiting your financial opportunities for seven years. Therefore, taking immediate action rather than ignoring the problem remains your best strategy.

Your credit report deserves careful examination since nearly 80% contain errors that might be disputed. Additionally, requesting debt validation within the first 30 days provides crucial protection under federal law. While paying the debt won't remove the collection immediately, newer credit scoring models do treat paid collections more favorably than unpaid ones.

Above all, remember your rights under the Fair Debt Collection Practices Act. Collection agencies must treat you with respect and provide accurate information about your debt. Consequently, you can dispute inaccuracies, request verification, and even negotiate settlements when appropriate.

Whether you choose to pay in full, negotiate a settlement, or dispute the debt entirely depends on your specific circumstances. However, one thing remains clear - addressing collections proactively almost always yields better results than avoidance. Take control of your financial future today by using the knowledge and strategies we've outlined to effectively manage Acceptance Now Collections on your credit report.