If your auto refinance was denied in 2026, you are not alone, and the reason is almost always something fixable. The auto loan market tightened sharply heading into 2026. According to CNBC Select, 15.2% of auto loan applicants were rejected in October 2025. That number more than doubled from just 6.7% in June 2025. Lenders are being stricter. Subprime borrowers are taking the hardest hit.

I run a credit repair company. This year, our team has already reviewed dozens of auto refinance denials from clients who had no idea what went wrong. They applied, expecting a lower rate. They got a denial letter instead.

The good news is that most of these denials trace back to a short list of causes. Know which one blocked you, fix it directly, and your next application stands a much better chance.

Why Was My Auto Refinance Denied in 2026?

Lenders evaluate several factors when you apply to refinance a car loan. A denial means your application failed to meet one or more of their requirements.

Federal law requires every lender to send you an adverse action notice within 30 days of denying your application. That notice must list the specific reasons for the denial. If you haven't received it yet, check your email and physical mail. It is on its way.

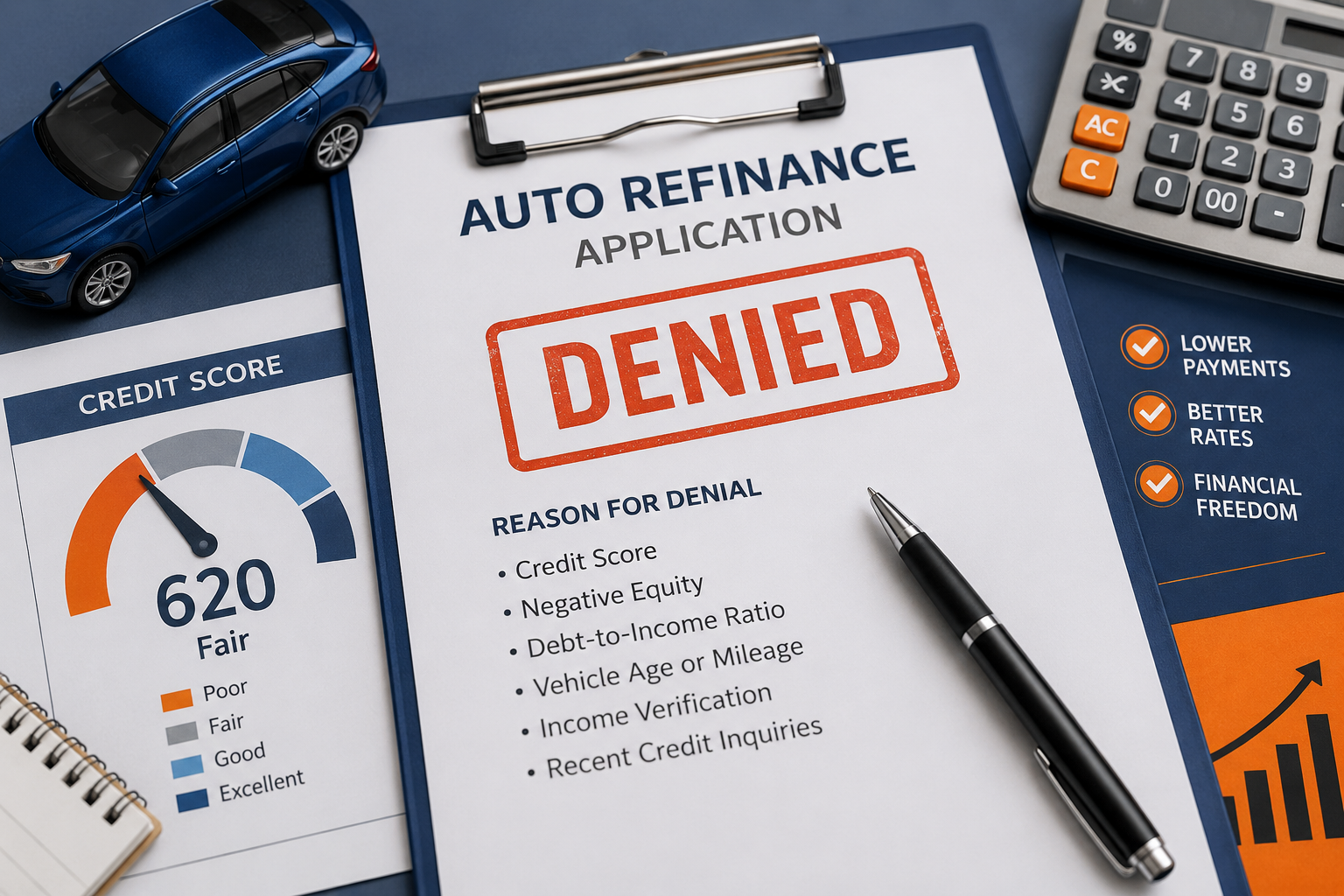

The most common reasons auto refinance applications get denied in 2026:

Credit score below the lender's minimum threshold

Negative equity on the vehicle (you owe more than the car is worth)

Debt-to-income ratio that is too high

Vehicle age or mileage outside the lender's guidelines

Insufficient or unstable income

Too many recent hard inquiries on your credit report

Each of these is fixable. But you need to know which one applies before you apply again.

What Are the Most Common Reasons for Auto Refinance Denial?

Low Credit Score

Your credit score is the first filter most lenders apply. Auto refinance lenders tend to prefer borrowers with scores of 660 or higher. Below that threshold, approval odds drop, and the rates offered rise sharply.

According to LendingTree's Q4 2025 marketplace data, borrowers with poor credit (under 580) paid nearly double the average APR compared to borrowers with very good credit (740 to 799). The average auto refinance rate as of early 2026 sits at 7.76%. Subprime borrowers are paying well above that.

A score below 660 does not make refinancing impossible. But it limits your lender options and raises the rate you'll pay. Improving your score before reapplying is almost always worth the wait.

Negative Equity on the Vehicle

Negative equity means you owe more on your car loan than the car is currently worth. Lenders call this being "underwater." It is one of the most common denial triggers in 2026.

According to Edmunds data cited by iTHINK Financial, 29.3% of trade-ins in Q4 2025 were underwater. Most of that negative equity comes from vehicles purchased during the high-price market of 2022 and 2023, when buyers paid inflated prices and took on large loan balances.

Most refinance lenders cap their loan-to-value (LTV) ratio at 120% to 130%. If your balance exceeds that cap relative to the car's current value, the lender will decline the application. Continuing to make payments for 12 to 24 more months often builds enough equity to qualify.

High Debt-to-Income Ratio

Your debt-to-income ratio (DTI) compares your total monthly debt payments to your gross monthly income. Refinance lenders use it to judge whether adding a new loan structure creates risk.

Most auto refinance lenders look for a DTI below 40% to 45%. If your monthly obligations for rent or mortgage, car payment, credit cards, and other debts together exceed that share of your income, lenders see you as overextended.

Your income does not appear on your credit report. But you report it on the application, and lenders verify it. If your DTI is too high, paying down other debts before you reapply can shift your profile enough to qualify.

Vehicle Age or Mileage Limits

Refinance lenders treat the vehicle itself as collateral. Older cars and high-mileage vehicles lose value faster, which increases the lender's risk if you default.

Most lenders will not refinance a vehicle that is more than 10 years old or has more than 100,000 to 150,000 miles. Specific limits vary by lender. Some credit unions have more flexible guidelines than traditional banks. If your vehicle is close to these limits, a credit union may be your best option.

Unstable or Insufficient Income

Lenders want to see consistent income before approving any loan. Recent job changes, gaps in employment, or self-employment income without clear documentation can all trigger a denial.

Most refinance lenders ask for recent pay stubs, W-2s, or tax returns to verify income. Self-employed borrowers typically need at least two years of tax returns to show stable earnings. If your income situation has changed recently, waiting until your employment history stabilizes strengthens your application.

Too Many Recent Hard Inquiries

Every time you formally apply for a loan or credit card, a hard inquiry appears on your credit report. Multiple recent inquiries signal to lenders that you may be in financial trouble or shopping aggressively for credit.

If you applied to several lenders within a short window, the inquiries stack up. Most lenders allow a short rate-shopping window of 14 to 45 days where multiple auto inquiries count as one. Outside that window, each application creates a separate mark.

The six causes above cover the vast majority of auto refinance denials. Read your adverse action notice carefully. It will point you to exactly which one blocked your application.

What Credit Score Do I Need to Refinance a Car in 2026?

There is no universal minimum, but here are the general score ranges lenders work with:

300 to 579 (Poor): Very few refinance lenders will approve at this range. Credit unions with flexible programs are your best option.

580 to 659 (Fair): Some approval options exist, but expect higher rates and stricter terms.

660 to 699 (Near Prime): Approval odds improve meaningfully here. Rates will still be above average.

700 to 739 (Good): Most mainstream refinance lenders will work with you at competitive rates.

740 and above (Very Good to Exceptional): You qualify for the best rates most lenders offer.

According to Caribou's refinance data, approval odds decline noticeably once your FICO score falls below 660. That threshold is where most lenders draw the line between prime and subprime risk.

What Is Negative Equity and Why Does It Block My Refinance?

Negative equity means your loan balance is higher than your car's current market value. For example, if you owe $22,000 on a car worth $17,000, you are $5,000 underwater.

Lenders decline these applications because the vehicle does not provide enough security for the loan. If you default, the lender cannot recover the full balance by selling the car.

The fastest way out of negative equity is time. Making regular on-time payments reduces your balance faster than the car depreciates in many cases. At the 18 to 24 month mark on most loans, borrowers often cross from underwater to having usable equity.

You can also make extra payments toward your principal to close the gap faster. Even $100 to $200 extra per month accelerates equity buildup significantly. Once your balance drops to within 120% of the car's value, most lenders will consider your refinance application.

Does a Denied Auto Refinance Hurt My Credit Score?

The denial itself does not show up on your credit report and does not affect your score. However, the hard inquiry from your application does.

One hard inquiry typically lowers your score by two to five points. That impact fades after about 12 months and disappears from your report completely after two years.

The bigger concern is applying to several lenders at once without a rate-shopping strategy. Submit multiple applications within a focused 14-day window. Most credit scoring models count all auto loan inquiries within that period as a single inquiry. That way, you compare options without stacking multiple score hits.

Can I Appeal or Reapply After Being Denied?

Yes. Some lenders have a reconsideration process where you can speak with a loan officer directly. Call the lender's number on your denial notice and ask if a manual review is available.

Manual reviews work best when:

Your denial was based on one specific issue, which you can explain clearly

Your score is close to the lender's minimum requirement

You have documentation that adds context, such as proof of a recent income increase

If the lender does not offer reconsideration, move to a different lender. Credit unions are often more flexible than banks and may approve applications that larger institutions decline.

How Long Should I Wait Before Reapplying?

Wait at least three to six months unless you can fix the root cause faster. Applying again too soon without addressing the reason for the denial almost always produces a second denial. All it adds is another hard inquiry.

Use the waiting period to act on whatever your adverse action notice flagged. If the issue was your credit score, spend three months paying balances down and keeping all payments on time. If the issue was negative equity, continue making regular payments until your balance drops. If the issue was DTI, pay off smaller debts to lower your monthly obligations.

Auto Refinance Denied?

Fix the Credit Issues Blocking Your Approval

A denied refinance is not the end. ASAP Credit Repair can help review your credit report, identify inaccurate negative items, and build a stronger profile before you apply again.

Start Your Credit Review TodayNo pressure. Just a clear look at what may be hurting your approval odds.

What Can I Do Right Now to Get Approved for Auto Refinance?

Start with your adverse action notice. Read every reason listed. Then act on each one in order of how quickly you can fix it.

Here is what works, based on what we see most often with clients:

Pull your credit report. Go to AnnualCreditReport.com and check all three bureaus for errors. Dispute anything inaccurate.

Lower your credit utilization. Pay down credit card balances below 30% of each card's limit. This can lift your score within 30 to 60 days.

Avoid new applications. Stop applying for any new credit until after your refinance is approved. Every hard inquiry counts against you.

Try a credit union. Credit unions often have more flexible LTV limits, lower rate floors, and more willingness to work with near-prime borrowers than large banks.

Add a co-signer. A co-signer with strong credit can shift the application into a better risk tier. Lenders may weight the stronger score more heavily, depending on their policy.

Make extra principal payments. If negative equity is the issue, putting extra money toward your loan balance each month is the fastest path to eligibility.

Last quarter, clients who followed this checklist and waited the appropriate time before reapplying came back to us with approvals from credit unions at rates between 6.5% and 8.9%, compared to the 18% to 24% rates they had been paying on their original loans. The savings were real and immediate.

A denied auto refinance in 2026 is not a permanent answer. It is a list of things to fix. Pull your adverse action notice, identify the specific cause, and use the steps above to address it before you apply again. At ASAP Credit Repair, we review your full credit profile and help you build the strongest possible application before your next submission. Reach out and we will walk you through where to start.