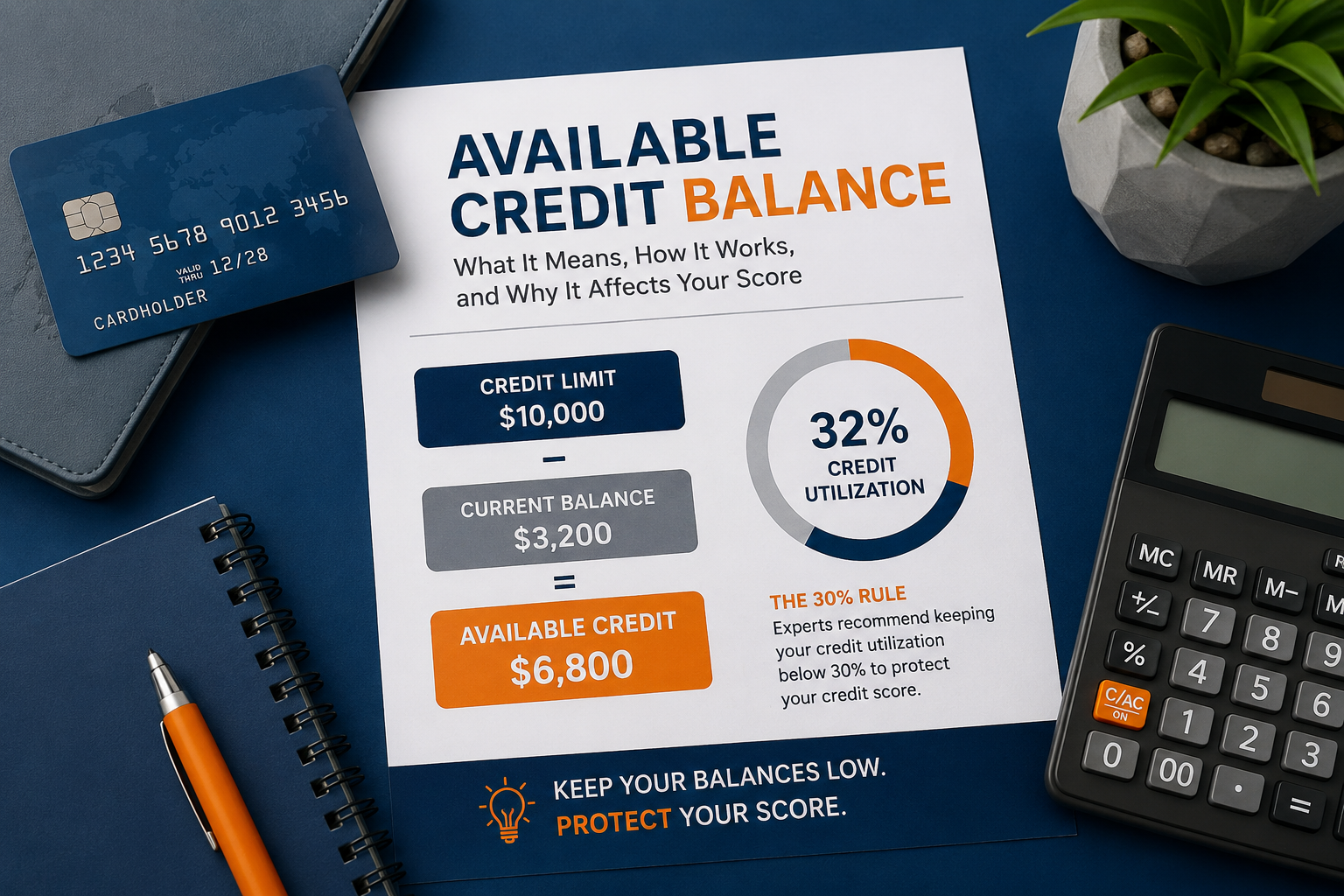

Your available credit balance is the amount of money you can still spend on a credit card right now. The formula is simple: credit limit minus your current balance equals available credit.

Running a credit repair company, I see the same confusion come up week after week. Clients stare at two numbers on their card statement and have no idea which one matters more. One of the clearest cases I remember was a client who had a $10,000 credit limit, a $9,200 balance, and no idea why her score dropped 45 points. Her available credit was $800. That gap told the whole story.

This confusion is widespread. A thread on r/personalfinance asked users to explain the difference between credit limit and available credit. Over 400 people commented. Most of them had been misreading their own statements for years. The Consumer Financial Protection Bureau (CFPB) confirms that credit utilization, which is directly tied to your available credit, is one of the most misunderstood factors in personal finance. And according to the Motley Fool, the average American now carries $6,715 in credit card debt, with a national average credit utilization rate sitting at 29%. That is one percentage point away from the threshold where lenders start to see you as a risk.

What Is an Available Credit Balance?

Available credit is the portion of your credit limit that you have not spent yet. Every time you make a purchase, your available credit goes down. Every time you make a payment, it goes back up.

Here is the exact formula:

Credit Limit minus Current Balance equals Available Credit

If your credit limit is $5,000 and your current balance is $1,500, your available credit is $3,500. That $3,500 is what you can spend before hitting your limit.

Your available credit changes every day. New charges reduce it. Payments restore it. Pending transactions that have not been posted yet can also lower it temporarily.

Card issuers display your available credit in your app, on your monthly statement, and in your online account. Check it before any large purchase. A declined transaction at checkout usually means one thing: your available credit is too low for the charge you tried to make.

What Is the Difference Between Available Credit and Credit Limit?

These two numbers look similar but serve different purposes.

Your credit limit is the maximum amount your card issuer will lend you. It stays fixed unless the issuer changes it or you request an increase. It is the ceiling.

Your available credit is what is left underneath that ceiling at any given moment. It moves up and down based on your spending and payments.

A Simple Example

You have a credit card with an $8,000 credit limit. You spend $3,200 on it this month. Your available credit is now $4,800. Your credit limit is still $8,000. Nothing about the limit changed. Only your available credit has shifted.

If you pay $1,000 toward your balance, your available credit rises to $5,800. The credit limit still stays at $8,000.

The key distinction: your credit limit is static, and your available credit is fluid.

What Is the Difference Between Available Credit and Current Balance?

Your current balance is what you owe right now. It includes every posted purchase, fee, and interest charge on your account.

Your available credit is what you have left to spend.

The two numbers move in opposite directions. When your current balance goes up, your available credit goes down by the same amount. They always add up to your credit limit.

Pending Transactions and the Gap Between Numbers

Here is where many people get confused. A purchase you made today may not post to your account for 24 to 48 hours. During that window, your current balance might not reflect the charge yet. But your available credit may already be reduced. Card issuers often place a hold on funds for pending transactions.

This is why your current balance and your available credit do not always seem to line up. Always trust your available credit number as the accurate picture of what you can spend right now.

How Does Available Credit Affect Your Credit Score?

Available credit directly controls your credit utilization ratio. And credit utilization makes up 30% of your FICO score. It is the second most important factor, right behind payment history.

Your utilization ratio is your total balance across all cards divided by your total credit limit across all cards. Low available credit means a high balance relative to your limit. That is what lenders call high utilization, and it signals financial stress.

The 30% Rule

The CFPB and most credit experts recommend keeping your credit utilization below 30%. In practice, people with the highest credit scores tend to keep it under 10%.

Here is a real-world example of why this matters. In our credit repair office alone, we reviewed 85 client files last year where the primary reason for score drops was utilization creeping above 30%. None of those clients had missed a payment. The damage came entirely from letting available credit shrink too low.

Experian data confirms this trend. As of 2025, the average credit utilization in the United States sits at 29%, right at the edge of that 30% threshold.

Per-Card Utilization vs. Overall Utilization

FICO tracks utilization in two ways. It looks at your overall utilization across all cards, and it looks at each card separately. A maxed-out card can hurt your score even if your overall utilization looks fine. Keep both numbers in check.

What Happens When You Use All Your Available Credit?

Using all your available credit maxes out your card. Your available credit drops to zero, and your utilization hits 100%. This is one of the fastest ways to damage a credit score.

Maxing out a single card can drop your score by 30 to 60 points, depending on your credit profile. Lenders see this as a red flag. It suggests you may be overextended financially.

Beyond the credit score hit, practical problems follow. Card issuers may decline future purchases. Some issuers charge over-limit fees if you exceed your credit line. A small auto-charge, such as a streaming subscription, can push you over the limit without warning.

According to U.S. total credit card debt data from the Federal Reserve Bank of New York, Americans collectively owe $1.252 trillion on credit cards as of Q1 2026. A significant portion of that debt sits on maxed-out or near-maxed-out cards. The people holding those balances pay the most in interest and carry the weakest credit scores.

Can You Spend More Than Your Available Credit?

In most cases, no. Card issuers block transactions that exceed your available credit.

Some cards offer over-limit protection. With that feature, a transaction goes through even if it exceeds your available credit. But the issuer charges an over-limit fee, and the balance still accrues interest.

The CFPB requires card issuers to get your consent before enrolling you in over-limit protection. If you never agreed to it, your card will decline the transaction rather than let you overspend.

Avoid relying on over-limit protection. The fees and the score impact are not worth it.

How to Increase Your Available Credit

More available credit gives you a larger cushion and keeps your utilization ratio low. Three reliable methods increase it.

1. Make Payments Early or More Often

You do not have to wait for your statement due date. Pay down your balance mid-cycle and your available credit rises before the next statement closes. This is one of the most underused tactics for managing utilization in real time.

2. Request a Credit Limit Increase

Call your card issuer and ask for a higher credit limit. Many issuers grant increases automatically after 6 to 12 months of on-time payments. Others require a formal request. A higher limit with the same balance means lower utilization and more available credit.

One important note: some issuers run a hard inquiry when you request a limit increase. Ask whether the request triggers a hard pull before you proceed. A hard pull can temporarily lower your score by 5 to 10 points.

3. Open a New Credit Card

Adding a new card increases your total available credit across all accounts. If your balances stay the same, your overall utilization drops. This helps your score, but only if you do not add more debt to your existing cards.

Be strategic here. Opening too many cards in a short period triggers multiple hard inquiries, which can lower your score temporarily. Space out new applications by at least six months when possible.

How to Monitor Your Available Credit

Most card issuers offer real-time balance updates in their mobile apps. Set up push notifications or balance alerts so you know when your available credit drops below a certain amount.

Check your available credit before major purchases. Know your utilization percentage, not just your dollar balance. If your card has a $5,000 limit and your balance is $1,400, your utilization is 28%. That is still under 30%, but one more large purchase could push you over.

Pull your free credit report at AnnualCreditReport.com at least once a year to confirm the balances and limits your card issuers are reporting to the credit bureaus. Errors in reported limits can raise your utilization on paper even when your actual spending is responsible.

Low Available Credit Hurting Your Score?

High credit card balances can lower your score fast. ASAP Credit Repair USA can help you review your credit report, spot problem areas, and build a plan to improve your credit.

Get Your Credit Report ReviewTrusted credit repair help for people ready to take control of their score.

Why Available Credit Matters Beyond Your Credit Score

A high available credit balance does more than help your score. It gives you a financial buffer for emergencies. It keeps you from relying on high-interest debt when unexpected expenses hit. And it builds the kind of credit profile that earns better terms on loans and mortgages.

The connection between available credit and real financial outcomes is direct. WalletHub reports that U.S. consumers added $43 billion in new credit card debt during Q2 2025, more than triple the post-recession average. Most of that debt came from people spending beyond their available credit cushion, not from planned borrowing.

Protect your available credit the same way you protect your cash. The number on your screen is not just a spending limit. It is a signal to every lender who pulls your credit file.