A 649 credit score is close enough to qualify for many mortgage programs.

That is both the good news and the bad news.

The good news is that many lenders will work with borrowers in this range.

The bad news is that you're sitting near a credit score boundary where even a small improvement can make a noticeable difference.

I've seen borrowers rush into pre-approval at 649, only to discover that lowering a few credit card balances could have improved their terms within a month or two.

That does not mean you should always wait.

It means you should understand what a 649 score actually means before submitting an application.

The biggest opportunity may not be approval.

It may be pricing.

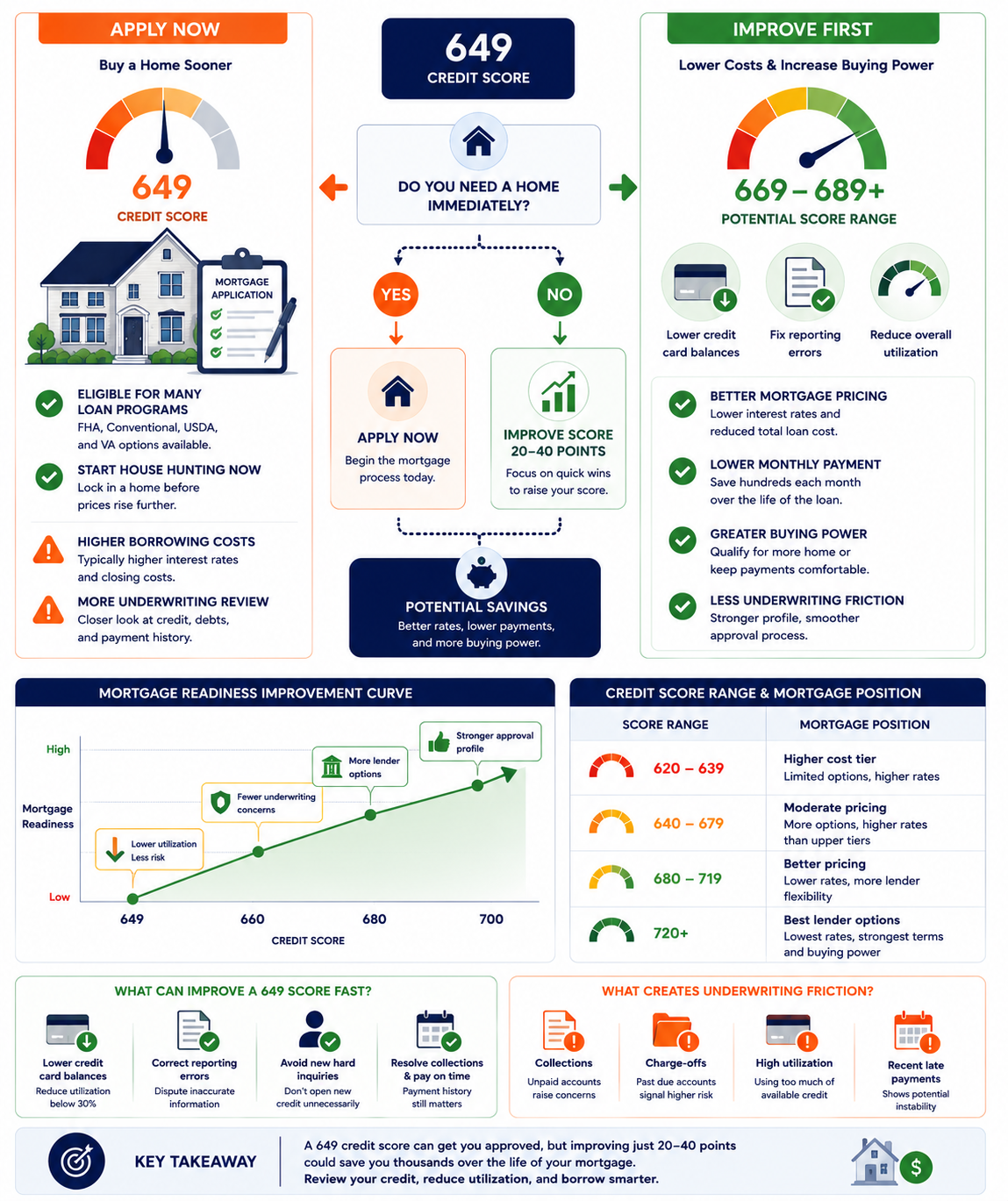

Should You Apply for a Mortgage With a 649 Credit Score or Wait?

A 649 credit score can qualify for a mortgage today, but it may also be close enough to a better pricing tier that waiting could make sense.

The visual below shows how small score improvements can affect borrowing costs, underwriting friction, and overall mortgage readiness.

Can You Get Approved for a Mortgage With a 649 Credit Score

Yes. A 649 score qualifies for FHA loans and conventional loans. FHA requires 580 minimum for 3.5% down. Conventional requires 620 minimum. Both are below 649. VA loans are available to eligible veterans with no agency-set minimum , most VA lenders approve at 580 or above. USDA typically processes best at 640+, where a 649 qualifies. Approval is not the obstacle. Rate and underwriting friction are the real issues at 649.

- FHA loans. 649 qualifies comfortably. FHA rates at this score tier are often lower than conventional before mortgage insurance is added. FHA MIP is mandatory for the life of the loan with under 10% down. Some FHA lenders still require collections to be resolved regardless of score.

- Conventional loans. 649 qualifies. But 649 sits at the lower end of the 640-679 LLPA tier. The same tier where Benzinga and conventional loan analysts note that LLPA charges often make FHA more economical than conventional for borrowers below 660.

- VA loans. No agency minimum. Most VA lenders approve at 580+. A 649 qualifies. VA rates are the lowest available for eligible borrowers regardless of score tier , no monthly mortgage insurance and no LLPA surcharges.

- USDA loans. 640 is the streamlined processing threshold. A 649 qualifies for streamlined review. Below 640 requires manual underwriting, which is slower and requires more documentation.

Why 649 Is an Important Mortgage Score

649 is important because it sits near two pricing boundaries. The first is 620 , where conventional loans become available. Most 649 borrowers already cleared that. The second is 680 , where LLPA pricing becomes more favorable and conventional loans often become cheaper than FHA. 649 is 31 points from that boundary. For many borrowers, that 31-point gap is achievable in 60 to 90 days. That makes 649 a decision score, not just an approval score.

Most people with 580 ask whether they can qualify at all.

Most people with 720 ask about getting the best rate.

People with 649 ask a different question. "Should I apply now, or spend 60 days improving first?" That is the right question. And the answer changes the entire financial outcome of the mortgage.

The 649 borrower who waits 60 days and reaches 680 enters a new pricing tier. The rate drops. The monthly payment drops. The lifetime interest cost drops significantly. The same borrower who applies at 649 today gets approved , but pays more every month for 30 years.

Should You Apply Now or Wait 60 Days

Apply now if the right home is found, income is stable, utilization is already low, and no quick score improvements are available. Wait 60 to 90 days if credit cards are highly utilized, reporting errors exist, or one specific action could move the score 20 to 30 points quickly. The 60-day test: can utilization reduction get the score to 660 or 680 before the current opportunity closes?

- Found the right home at the right price and sellers are not waiting

- Income is stable and DTI is already within guidelines

- Credit card utilization is already under 30% , no quick score boost available

- Collections are resolved or do not affect this loan type

- VA loan eligible , no LLPA surcharges affect pricing

- Plan to refinance within 2-3 years after score improves naturally

- Credit card balances are above 50% of limits , utilization fix could add 20-40 points in one cycle

- Reporting errors exist that can be disputed and corrected in 30-45 days

- One collection is in active dispute and likely to be deleted within 90 days

- Score is 649 from utilization alone , reaching 680 is realistic in 60 days

- Home prices in the target market are stable , delay carries no opportunity cost

- Getting to 680 would save $50-$80/month for 30 years , $18K-$29K lifetime

What Mortgage Rate Position Does a 649 Score Usually Receive

| Credit Score Range | Rate Position | vs 700-Score | LLPA Tier Impact |

|---|---|---|---|

| 760+ | Best available rates | -0.75 to -1.0% | Minimum LLPA |

| 720-759 | Very competitive | -0.25 to -0.40% | Low LLPA |

| 700-719 | Good , some premium | Baseline | Moderate LLPA |

| 680-699 | Fair , noticeable premium | +0.30 to +0.45% | Higher LLPA |

| 640-679 (649 is here) | Higher , near LLPA maximum | +0.44 to +0.74% | High LLPA , FHA often better |

| 620-639 | Highest risk tier , conventional | +0.80 to +1.10% | Near-maximum LLPA |

The Fastest Ways to Improve a 649 Credit Score Before Applying

The fastest improvements from 649 come from reducing credit card utilization and disputing reporting errors. Both can produce results within 30 to 60 days. Getting from 649 to 680 in 60 days is realistic when high utilization is the primary cause. The target is the 680 LLPA threshold , not just any score increase. Crossing that line is worth more than gaining 20 points that stay within the same tier.

- Pay credit card balances to under 10% of each card's limit before the statement closes. This is the single fastest action available. If utilization is causing the 649, paying cards down can add 20 to 50 points in one billing cycle. Do it before the statement closes , the lower balance needs to report to the bureaus before the score updates.

- Dispute reporting errors on all three bureau reports. Pull reports at AnnualCreditReport.com. Look for wrong dates, wrong balances, accounts not yours, and collections with inaccurate information. One removed error can add 15 to 50 points in 30 to 45 days.

- Avoid all new hard inquiries for 60 to 90 days. Each new application costs 5 to 10 points. Rate shopping with multiple mortgage lenders in a 14 to 45 day window counts as one inquiry under FICO's mortgage shopping window rule. But opening credit cards, auto loans, or personal loans during this period damages the score being protected.

- Do not close any existing credit cards. Closing a card removes its credit limit from the utilization calculation. The same balances on remaining cards now represent a higher percentage of a lower total limit. Utilization rises. Score drops. Keep old cards open.

The full timeline of how many points each action produces and how quickly , from low utilization to collection disputes to authorized user additions , is covered in the credit score improvement timeline guide. The same actions apply at 649 , and the fastest ones are still the utilization moves that reset every billing cycle.

How Much Can 20 Points Matter at 649

The important lesson: score gains within the same tier produce minimal rate improvement.

Going from 649 to 669 is a 20-point improvement. It stays in the 640-679 tier. The LLPA adjustment does not change. The rate barely moves.

Going from 649 to 680 is a 31-point improvement. It crosses a tier boundary. The LLPA drops. The rate drops. The monthly payment drops. The savings are real and they compound over 30 years.

The goal is not "improve my score." The goal is "cross the next tier boundary." Those are different targets.

Why Some 649 Borrowers Get Better Mortgage Terms Than Others

The credit score triggers the LLPA pricing tier. It does not fully determine the terms. Two borrowers at 649 can receive meaningfully different rates and conditions based on their down payment, debt-to-income ratio, cash reserves, employment history, and whether collections appear in the file. The score opens the door. The full profile determines what is on the other side.

- Down payment size. A 649 borrower putting 20% down receives better LLPA pricing than one putting 3.5% down. The down payment directly reduces the risk the score already signals. More down payment = lower rate even within the same score tier.

- Debt-to-income ratio. A 649 borrower at 29% DTI looks very different from one at 46% DTI. Low DTI is a compensating factor that offsets score concerns in underwriting. It may also allow for more favorable lender overlays.

- Cash reserves. Two to six months of mortgage payments in savings after closing. Underwriters call this "reserves." Reserves demonstrate that a temporary income disruption would not immediately cause a missed payment. At 649, reserves carry more weight than at 720.

- Employment history. Two or more years at the same employer , or in the same field , signals stable income. Job hopping or a recent self-employment transition adds underwriting friction to an already scrutinized 649 file.

- Collections in the file. A 649 with no collections reads differently from a 649 with two recent collections. Same score. Different risk profile. Collections at 649 often require lenders to impose conditions that a borrower with the same score but a clean file would not face.

What Underwriters See When They Review a 649 Score

Underwriters do not just see the number 649. They see a complete credit file. A 649 from two years of rebuilding after a single missed payment looks different from a 649 with three collections and a recent charge-off. The score starts the review. The file finishes it. At 649, underwriters are specifically looking for compensating factors to justify approval at a borderline score level.

Automated underwriting systems evaluate the file first.

Fannie Mae's DU or Freddie Mac's LP runs the application against agency guidelines. A 649 often returns "Approve/Eligible" or "Refer with Caution" depending on the full file profile. "Approve/Eligible" moves to standard processing. "Refer with Caution" moves to manual underwriting , which is slower, requires more documentation, and carries higher denial risk.

Manual underwriting at 649 means a human reviews every negative item. Each collection gets explained. Employment gaps get documented. Each derogatory mark gets weighed against the compensating factors in the file.

The borrower who prepares for this , with reserves in the bank, a clean 12-month payment history, a letter of explanation for any negative items, and a low DTI , survives manual underwriting at 649. The borrower who walks in with a clean score but no preparation often does not.

As Experian's mortgage rate data confirms, 649 borrowers represent a meaningful segment of approved mortgages , but they consistently pay a rate premium and face more documentation requirements than borrowers even 20 to 30 points higher.

Can Collections Hurt Mortgage Approval With a 649 Score

Yes , and at 649, collections can matter more than the score itself. The score technically qualifies. But a collection , especially housing-related , can trigger additional conditions, required payoffs, or outright denial even when the number is above the minimum. At 649, the file is under more scrutiny than a 700+ borrower. Every negative item gets evaluated. Collections do not get ignored because the score qualifies.

FHA lenders commonly require collections over $1,000 to be resolved before closing.

A 649-score borrower with a $1,400 apartment collection may need to pay or dispute it before the loan closes , regardless of the score. Conventional lenders may ignore individual small collections under Fannie Mae guidelines, but many apply their own stricter overlay policies. At 649, overlays are common.

Apartment collections create specific concern. An underwriter evaluating a mortgage application from someone who left an apartment with an unpaid balance is evaluating whether that pattern is likely to repeat with a mortgage. The score does not answer that question. The collection does.

Address collections before applying when possible. If a collection is disputable , inaccurate charges, insufficient validation, re-aged dates , work the dispute process before submitting the application.

649 Credit Score vs 680 Credit Score

| Factor | 649 Score | 680 Score |

|---|---|---|

| LLPA pricing tier | 640-679 , higher LLPA | 680-699 , next tier, lower LLPA |

| Estimated rate ($300K loan) | ~7.35% | ~7.05% |

| Monthly P+I | ~$2,074 | ~$2,012 |

| Monthly difference | ~$62 less per month at 680 | |

| 30-year difference | ~$22,320 less total interest at 680 | |

| Conventional vs FHA | FHA often better (high LLPA) | Conventional starts to compete |

| Approval odds (est.) | ~65% approval rate | ~78% approval rate |

| Underwriting friction | More , manual review more likely | Less , more automated approvals |

| Timeline to reach 680 from 649 | Typically 30-90 days with utilization reduction if high utilization is the cause | |

How Close Are You to Mortgage Readiness

The utilization and collections rows are the ones most often flagged at 649. Both are actionable before applying. Utilization fixes in one billing cycle. Collections take 30 to 90 days for disputes. Know which ones apply before deciding whether to apply today or wait.

Is a 649 Credit Score Good Enough to Buy a House

Yes. Many borrowers buy homes every year with a 649 credit score. The approval is real. The mortgage is real. The house is real. The question is what the mortgage costs compared to what it would cost if the score were 680. The answer , approximately $62 more per month and $22,000 more over 30 years , is the calculation worth making before signing anything.

| Issue Holding Score at 649 | Fix Timeline | Potential Score Impact |

|---|---|---|

| High credit card utilization | 30 to 60 days | +20 to +50 points , fastest action available |

| Reporting errors on the file | 30 to 90 days | +10 to +50 points per corrected item |

| Collection accounts | 3 to 12 months | +20 to +70 points if deleted |

| Charge-offs | 6 to 24 months | +30 to +90 points if deleted |

| Recent hard inquiries | 3 to 12 months | Small, temporary; inquiries age off over time |

As noted by The Mortgage Reports' 2026 rate analysis, every 20-point increase in credit score saves approximately 0.15 to 0.25 percentage points on the mortgage rate — and a 760+ score currently earns approximately 6.15% while a 660-score earns approximately 7.20% on a 30-year fixed, a gap that costs $228 more per month on a $280,000 loan. As ConsumerAffairs confirms, improving from 620 to 760 saves $156 per month and over $56,000 in total interest on a $300,000 mortgage. The 649-to-680 slice of that improvement , $62 per month, $22,000 over 30 years , is the most achievable part of that journey for a borrower who addresses utilization before applying.

For the direct comparison of how rate tiers change across every score level from 630 to 760+, and the exact monthly payment and total interest calculations for each tier on a $300,000 loan, the mortgage rate guide for 630 score borrowers covers the same LLPA structure that affects 649 borrowers , because both scores share the same pricing tier dynamics.

Can I buy a house with a 649 credit score?

Yes. A 649 score qualifies for FHA loans (minimum 580), conventional loans (minimum 620), and VA loans for eligible veterans. USDA loans process efficiently at 640+. The bigger question is not approval , it is whether the rate offered at 649 is the best you can get, or whether improving the score 20 to 30 points first would meaningfully reduce the lifetime cost of the mortgage. For many borrowers at 649, a 60-day delay to reach 680 saves more than $22,000 over the life of the loan.

Is 649 enough for FHA?

Yes. FHA requires 580 for 3.5% down. 649 clears that threshold by 69 points. FHA may also offer better pricing than conventional at this score level because FHA uses a flatter risk structure compared to Fannie Mae and Freddie Mac's aggressive LLPA tiering. At 649 on conventional, LLPA charges add significantly to the rate. FHA's flatter premium structure can produce a lower total monthly payment even after mandatory MIP is included.

How quickly can I raise a 649 credit score before applying?

If high credit card utilization is the cause, 20 to 50 points are achievable in one billing cycle , 30 to 60 days. That alone could push 649 to 680 or above. Reporting errors resolve in 30 to 45 days when disputed. Collections take 3 to 12 months. Pull all three bureau reports at AnnualCreditReport.com first. Find the specific cause. The fix timeline depends entirely on what is causing the 649 , and utilization is the only one that resets in a single month.

Is 649 close to a better mortgage rate tier?

Yes. 649 is 31 points from the 680 LLPA tier boundary. That crossing saves approximately $62 per month and $22,000 over 30 years on a $300,000 loan. 649 is also 71 points from the 720 tier, where conventional pricing becomes very competitive, and 111 points from 760 where best-tier rates apply. The 680 target is the most realistic and most impactful near-term goal for most 649 borrowers.

-

What Mortgage Rate Can You Get With a 630 Credit Score? 630 and 649 share the same LLPA pricing tier (640-679) and the same underwriting dynamics. This covers the exact rate and payment comparison for the 640-679 tier vs higher score tiers , with the rate chart, the cumulative interest line graph showing how much the tier crossing saves over 30 years, and the buy-now-vs-wait framework that applies directly to the 649 decision. All rate data confirmed from Curinos/Experian May 2026.

-

How Available Credit Can Raise Your Credit Score Faster Than You Think The fastest way most 649 borrowers can reach 680 before applying is by reducing credit card utilization. This covers exactly how available credit affects the FICO score, why the impact updates every billing cycle, and what the score improvement looks like at each utilization tier. The 30-to-60-day utilization fix is the most direct path from 649 to 680 , and this article is the mechanics guide for executing it.

-

How Long Does It Take to Raise a Credit Score? Realistic Timelines Going from 649 to 680 is the same mechanics as going from any score to any target , the path depends on what is causing the current score. This covers the realistic timeline for each action: utilization in 30-60 days, disputes in 30-90 days, collections in 3-12 months, charge-offs in 6-24 months. The bar chart showing points gained per action and timeline is the planning tool every 649 borrower needs before deciding whether to apply now or wait.