Did you know that available credit on credit card have a direct influence on your credit rating?

A lot of people spend months trying to improve their credit score while completely ignoring one of the fastest-moving factors in credit scoring.

Available credit.

I've seen borrowers gain points without paying off collections, opening new accounts, or waiting years for negative items to age.

They simply lowered their credit card balances.

That surprises many people.

The reason is simple.

Credit scoring models pay close attention to how much of your available credit you're using.

A maxed-out card tells lenders one story.

A card with plenty of available credit tells a very different one.

That difference can affect:

credit scores

mortgage approvals

auto loan rates

credit card approvals

and sometimes much faster than people expect.

How Available Credit Can Raise Your Credit Score Faster Than You Think

Available credit affects your credit utilization ratio, which is one of the most influential factors in credit scoring. Lower utilization generally helps credit scores, while high utilization often lowers scores and creates additional underwriting concerns.

Why Available Credit Matters More Than Most People Think

Most people focus on payment history. Pay on time. Build a streak. Wait for the score to climb. That is partially right. Payment history is 35% of FICO. But utilization , driven directly by the available credit on credit cards , is 30%. The difference is speed. Payment history builds over months and years. Available credit changes every billing cycle. Improving utilization produces score movement faster than almost anything else in the credit file.

The misconception: a clean payment record automatically creates a strong score.

The reality: three years of perfect payments with 80% credit card utilization may still produce a 590 score. The payment history earns credit in one FICO category. The high utilization loses points in another. Both run simultaneously. Both count.

Fixing available credit on a credit card is the only credit repair action that resets every month.

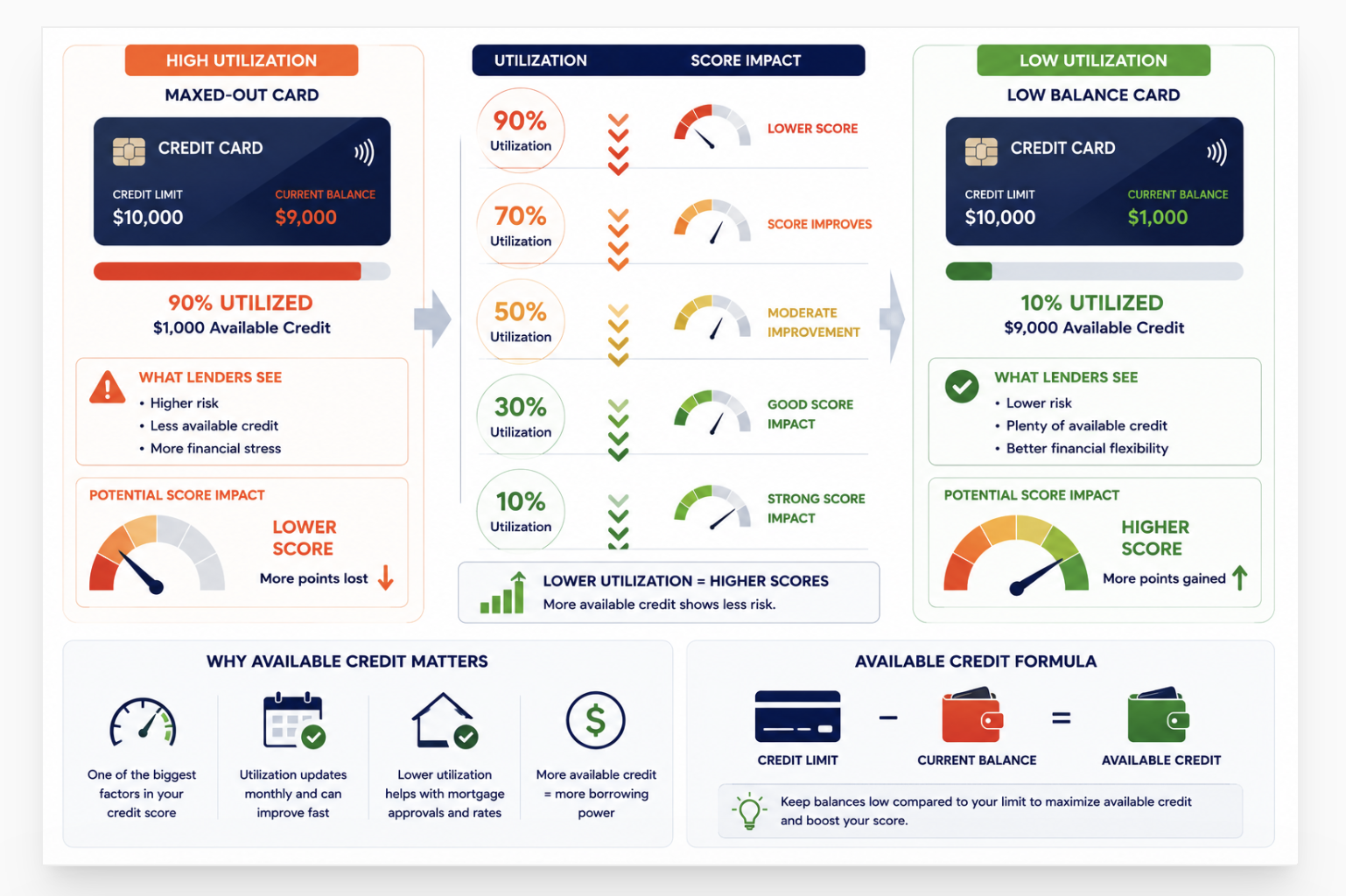

What Is Available Credit

Available credit is the unused portion of a credit card's limit. A card with a $10,000 limit and a $3,000 balance has $7,000 in available credit. That produces 30% utilization. More available credit means lower utilization. Lower utilization signals responsible credit management to scoring models. Less available credit , from high balances or low limits , increases utilization and suppresses scores.

FICO evaluates two utilization signals simultaneously.

The utilization on each individual card. And the total utilization across all cards combined. Both matter independently.

One card at 90% hurts the score even if every other card is empty. The maxed-out card registers as its own risk signal in the model. Paying down that specific card produces a targeted, measurable improvement , separate from any change to the total.

How Credit Utilization Affects Credit Scores

The score impact of utilization is non-linear. Getting from 90% to 50% helps. From 50% to 30% helps more. Crossing under 10% produces the strongest benefit. Experian puts 30% as the threshold where the negative effect becomes "more pronounced." myFICO confirms under 10% is the target for maximum scoring benefit. The lower the utilization on available credit, the stronger the scoring signal.

| Utilization Rate | Available Credit | Typical Score Impact |

|---|---|---|

| Below 10% | 90%+ available | Strong , maximum scoring benefit |

| 10% to 30% | 70-90% available | Good , consistent with strong-credit borrowers |

| 30% to 50% | 50-70% available | Moderate risk , Experian notes 30% as the "more pronounced" threshold |

| 50% to 75% | 25-50% available | Higher risk , noticeable score suppression |

| Above 75% | Under 25% available | Significant score pressure , most impactful negative signal after payment history |

Why Maxed-Out Credit Cards Hurt Scores

A maxed-out credit card with 95% utilization signals to the FICO model that nearly all available credit is consumed. This reads as financial stress. The score drops significantly. It stays suppressed until the balance drops. Clean payment history on the same card does not offset the utilization damage. The two factors score independently every month.

Here is the disconnect most people do not see.

They pay on time. Every month. Think the score reflects that discipline. The score does see it. But the score also sees that 95% of the credit limit is in use. Both signals register. Both matter. Neither cancels the other.

A borrower with perfect payment history and 90% utilization on available credit can score in the 550s. The same borrower at 8% utilization , same payment record, same accounts, same everything else , may score in the 680s. One variable. The balance relative to the limit.

The Fastest Credit Score Points Often Come From Utilization

Utilization is the only major FICO factor that resets every billing cycle. Pay down a balance before the statement closes. The lower balance reports to the bureaus. The score reflects the change within 30 days. No dispute required. No new account needed. No waiting years for a negative to age off. Just a lower balance , and a score that moves immediately.

The comparison matters here. Every other score-building action takes time.

Disputes take 30 to 90 days , and may not succeed. New accounts take 6 to 12 months to build meaningful age. Collections take 3 to 12 months to dispute and remove. Payment history improvements take 12 to 24 months to meaningfully accumulate.

Utilization resets in one billing cycle.

That speed difference is why available credit on a credit card is the first action in every score improvement plan.

How Available Credit Affects Mortgage Approval

High credit card utilization damages mortgage applications in two ways simultaneously. It suppresses the credit score that determines rate pricing. And it adds minimum payment obligations that count in the debt-to-income ratio. A borrower with $8,500 on a $10,000 limit qualifies for less house at a higher rate than the same borrower with $1,000 on that card , even with identical income, employment, and payment history.

The rate impact is significant. A utilization reduction that moves a score from 630 to 670 can drop the mortgage rate by 0.40 to 0.60 percentage points. On a $300,000 30-year loan, that difference is approximately $85 to $115 per month and $30,000 to $40,000 in total interest.

The DTI impact is equally real. Minimum payments on revolving debt count directly in the debt-to-income ratio. A $8,500 balance generates a minimum payment of $150 to $250 per month. That amount reduces the monthly mortgage payment a lender approves. The same borrower with $1,000 on the same card has a $25 minimum payment. The available credit difference changes not just the rate , it changes how much house can be financed.

Underwriters also evaluate revolving debt patterns directly. High utilization across multiple cards signals credit dependence. That pattern raises concern independent of the score number itself. Three cards all near their limits produces more underwriting scrutiny than the same score with low, distributed balances.

The specific rate and payment difference across credit score tiers , including exactly how much each score tier costs on a $300,000 mortgage , is detailed in the mortgage rate guide for 630 credit score borrowers.

Can Paying Down Credit Cards Raise Your Score in 30 Days

Often yes. Utilization recalculates every billing cycle. Pay the card down before the statement closing date. The lower balance reports to the bureaus at that statement. The score reflects the change within 30 days. As Experian confirms directly: borrowers "could see a positive effect on scores in as little as 30 days" after a lower utilization reports. The key is the statement close date , not the payment due date.

As Experian's utilization guide confirms, traditional credit scores treat utilization as a snapshot , not a trend. Last month's 90% does not follow the score into this month. Pay down the balance. This month's utilization is this month's score signal. The slate resets with every statement close.

How Much Available Credit Should You Have

The target is a percentage, not a dollar amount. Keep each credit card below 30% of its limit. Below 10% per card is ideal for maximum scoring benefit. A $5,000-limit card: keep the balance under $500. A $10,000-limit card: under $1,000. Also, do not close cards to create available credit , closing a card removes the limit from the calculation and can increase total utilization, hurting rather than helping the score.

- Under 10% per card. This is the zone myFICO associates with maximum scoring benefit for the amounts owed factor. Under 10% on every individual card , not just the total , is the optimal configuration.

- Under 30% total. Across all cards combined. $15,000 in combined limits: keep the total balance under $4,500.

- Not zero. A 0% utilization across all cards means no revolving credit activity is reporting. The FICO model sees no current credit management signal. Keep at least one card active with a small monthly purchase paid in full. This demonstrates responsible, ongoing credit use.

- Watch individual cards separately. Total utilization at 20% means nothing if one card sits at 85%. FICO scores both dimensions independently. One high-utilization card requires its own targeted paydown.

Should You Request a Credit Limit Increase

Sometimes. A credit limit increase creates more available credit on a credit card without requiring a balance paydown. The same $3,000 balance on a $5,000 limit is 60% utilization. On a $10,000 limit, it drops to 30%. One request. Meaningfully lower utilization. The catch: some issuers run a hard inquiry to approve the increase, which costs 5 to 10 score points. Ask before requesting.

- Soft-pull increase: No inquiry. No score cost. Immediate utilization improvement. Request it when available , almost always worth doing.

- Hard-pull increase: Costs 5 to 10 points from the inquiry. Calculate whether the utilization improvement outweighs the penalty. On a $5,000 card with $4,000 balance , 80% utilization , an increase to $10,000 drops utilization to 40%. That improvement likely justifies the 5-point inquiry cost.

- The behavioral risk: More available credit on a credit card means more room to accumulate debt. If spending behavior drove high utilization before, a limit increase alone does not solve the underlying problem , it temporarily lowers the ratio while creating more exposure.

Why Some Borrowers Stay Stuck Despite Paying On Time

Payment history and utilization score independently. Perfect payment history earns credit in the 35% payment history category. High available credit usage loses points in the 30% utilization category. The two run simultaneously. A borrower with a perfect three-year payment record and 80% credit card utilization may score 580. The same payment record with 8% utilization may score 670. One change. Enormous outcome difference.

This is the most common frustration in credit repair.

Three years of on-time payments. Score stuck at 588. The borrower assumes the payment streak is building the score. It is , slowly. But high utilization suppresses the score at the same pace. The two cancel each other out.

Payment history builds over years. Utilization resets every month. The fastest path to a higher score addresses both factors , not just the one that takes longer.

Fix available credit on the credit cards first. It is the only action that shows up in the score within 30 days. Then let the payment history continue building in the background while the utilization stays low.

Available Credit vs Credit Score , Real Example

| Available Credit | Balance | Utilization | Risk Level |

|---|---|---|---|

| 90% available | $1,000 | 10% | Low , Optimal |

| 70% available | $3,000 | 30% | Moderate |

| 50% available | $5,000 | 50% | Elevated |

| 25% available | $7,500 | 75% | High |

| 10% available | $9,000 | 90% | Very High |

What Utilization Percentage Do Mortgage Lenders Like

Under 30% , and under 10% is better. Mortgage underwriters evaluate revolving debt patterns directly in the credit file, not just the score number. Three cards all near their limits signal credit dependence. The same score with low balances and high available credit signals a borrower who manages credit responsibly. Getting under 30% before applying addresses both the score and the underwriting optics simultaneously.

Underwriters use a judgment the industry informally calls "revolving debt concentration."

It does not show up on a scoring matrix. It shows up when a human reviews the credit file. An underwriter sees $22,000 in combined revolving balances on $25,000 in combined limits. The score is 640. The underwriter still sees a borrower using 88% of available revolving credit. That pattern raises questions about financial stability that the score alone does not fully answer.

Getting utilization under 30% before applying changes both the number and the picture. As myFICO confirms, keeping utilization below 10% , combined with consistent on-time payments , is the configuration associated with the strongest FICO scores. Mortgage lenders reviewing files at that utilization level see a borrower who manages available credit on credit cards with clear discipline.

Can Available Credit Help You Reach a Mortgage Score Faster

For many borrowers, improving available credit on credit cards is the fastest path to a mortgage-ready score. Not because it removes negative items. Because it changes how scoring models evaluate the 30% of the FICO calculation controlled by amounts owed. A 40-point score jump from utilization reduction can move a borrower from one rate tier to the next , saving $25,000 to $40,000 over a 30-year loan , without any dispute process, new accounts, or waiting periods.

The sequence matters for mortgage preparation.

Fix available credit on credit cards first , it moves in one billing cycle and improves both the score and the underwriting picture. Then dispute any reporting inaccuracies , takes 30 to 90 days. Then let payment history continue building in the background over the remaining months before application.

Most borrowers run these in the wrong order. They spend months on disputes before addressing a simple utilization problem that would have moved the score in 30 days.

The full credit score improvement timeline , including exactly how many points each action produces and how quickly, starting from different score levels , is covered in the realistic credit score improvement guide. Utilization reduction is at the top of that list for a reason.

As U.S. News confirms in their credit utilization analysis, the amounts owed category , which utilization controls , accounts for 30% of the FICO score. That makes available credit on a credit card one of the most directly actionable levers any borrower has before a loan application.

Does available credit on a credit card affect your credit score?

Yes. Available credit determines your utilization ratio , what percentage of the credit limit is in use. Utilization makes up 30% of a FICO score. More available credit means lower utilization. Lower utilization produces better scores. The score updates within 30 days when a lower balance reports at the statement close. Both total utilization across all cards and each individual card's utilization matter independently in the FICO calculation.

Is 30% credit utilization still good for your score?

30% is better than 50%, 70%, or 90%. But it is not optimal. Experian identifies 30% as the threshold where the negative scoring effect becomes "more pronounced." myFICO recommends below 10% for maximum benefit. Crossing from 30% to under 10% on each card produces meaningful additional score improvement. 30% is the minimum target. Under 10% is the actual goal for borrowers seeking mortgage-qualifying scores.

How quickly does credit utilization update on a credit score?

Most credit card issuers report balances to the bureaus at the statement close date , typically once per month. When the lower balance reports, the utilization calculation updates and the score reflects the change at the next scoring update. For most borrowers, the full cycle takes 30 to 60 days from when the payment clears to when the score fully reflects the improvement across all three bureaus.

Does closing a credit card improve or hurt available credit?

Closing a credit card almost always hurts available credit and raises utilization. When a card closes, its credit limit is removed from the total available credit calculation. The same balances on remaining cards now represent a higher percentage of a lower total limit. Utilization increases. The score drops. Keep old cards open , especially cards with no annual fee , even if unused. The available credit they contribute to the calculation is valuable.

-

What Mortgage Rate Can You Get With a 630 Credit Score? Utilization directly controls the score tier that determines mortgage rate pricing. This covers the exact dollar cost of each score tier on a $300,000 30-year mortgage , including the rate table, monthly payment comparison, and the cumulative interest chart showing what a 40-point score improvement from utilization reduction is worth over 30 years. The connection between available credit and mortgage cost is made concrete with confirmed May 2026 rate data.

-

How Long Does It Take to Raise a Credit Score? Realistic Timelines Utilization reduction sits at the top of the action timeline because it moves in a single billing cycle. This article covers every credit improvement action with point estimates and timelines , how much utilization paydown gains versus disputes versus authorized user additions versus credit builder accounts. The comparison shows exactly why available credit is always the first action, not the last.

-

Credit Score Ranges , What Each Tier Opens for Borrowers Improving available credit on a credit card moves the score. This covers what each score milestone actually means in practice , which loan programs open, what rate tiers change, what approval thresholds shift at 580, 620, 660, 680, and 720. Knowing the specific financial difference between tiers gives utilization reduction a concrete target rather than just "raise your score."